Empty roads, grounded aircraft, falling tourist and international student numbers, plunging car sales, empty super market shelves, disrupted supply chains…

Fig 1: Empty roads in Wuhan in February 2020

China Car Sales Slump 92% in First Half of February on Virus

21 Feb 2020

Fig 2: Chinese car sales were down since June 2018

That all sounds like peak oil has hit except that oil prices are low now. Which may change of course as low oil prices may mean that US shale oil is likely to peak earlier than otherwise would have been the case.

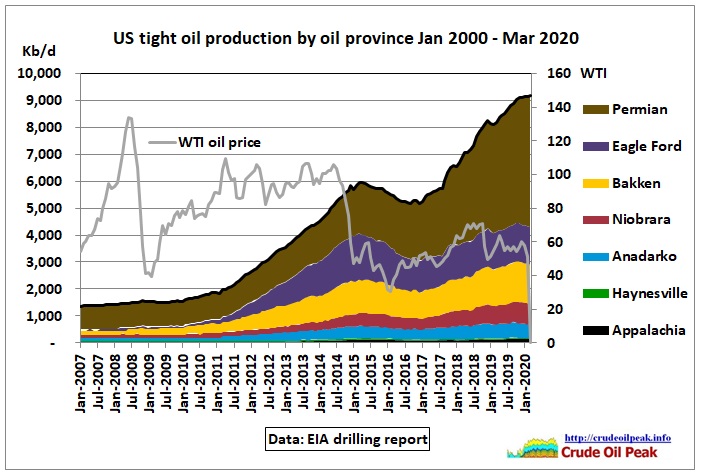

Fig 3: US tight oil production

https://www.eia.gov/petroleum/drilling/

The graph shows that tight oil production took off when oil prices were around $100/barrel but peaked in March 2015 and then declined as oil prices dropped to $50/barrel. Production started to recover in September 2016 but almost half of the production (mainly from Bakken, Eagle Ford, Niobrara and Aanadako) has already peaked again in October 2019 and in March 2020 is estimated to be just 240 kb/d higher than the 2015 peak. The other half of the production, from the Permian (Texas) is still growing but monthly growth rates have declined from 180 kb/d in mid 2018 to 40 kb/d now. Recent data are preliminary.

Coronavirus Delivers Another Blow to Embattled Shale Drillers

29 Feb 2020

Frackers already faced financial woes in 2020, even before the virus threatened oil demand

Shale drillers were already braced for a tough year. Now the new coronavirus is putting them under even greater financial pressure.

Exploration and production companies are straining to slow growth—amid an oversupply of oil and gas—and cut spending to appease investors angry over poor returns. Now the virus has further weakened global demand for their products, posing a greater challenge to a sector where many companies are saddled with debt.

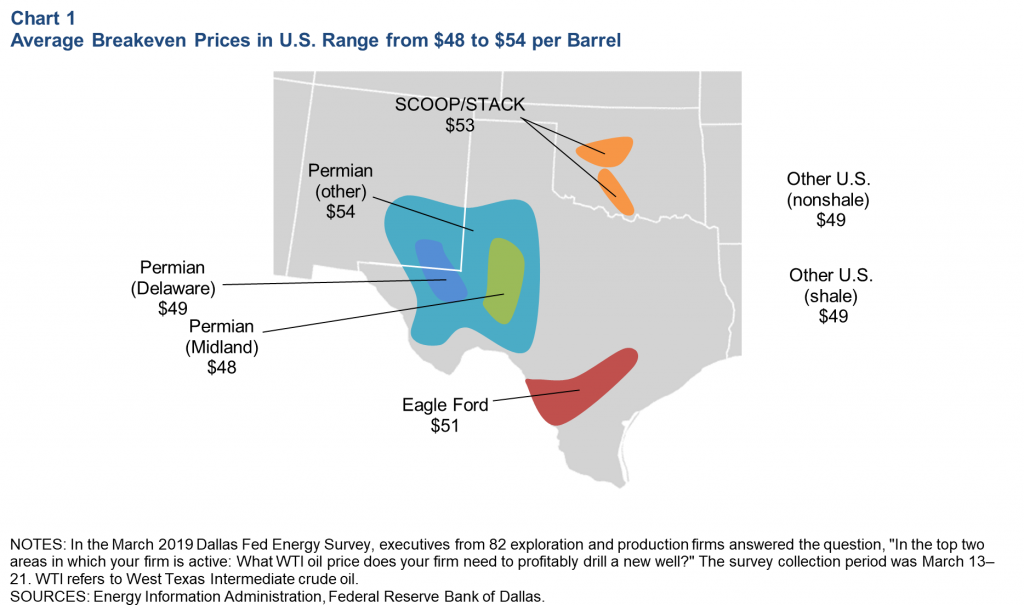

Fig 4: Breakeven oil prices in the US

https://www.dallasfed.org/research/economics/2019/0521

U.S. Shale Drillers Could Be Casualties of Oil-Price War

9 Mar 2020

Standoff between Russia, Saudi Arabia over oil production cuts threatens to devastate U.S. frackers, who have little ability to withstand lower prices.

U.S. shale drillers are poised to be among the biggest losers in the oil-price war stoked by Russia and Saudi Arabia that has sent global prices crashing. Dozens of debt-addled companies, including Chesapeake Energy Corp. and Whiting Petroleum Corp., were already facing financial difficulties even before U.S. benchmark prices plummeted 25% to $31.13 a barrel Monday, the largest drop since 1991.

https://www.wsj.com/articles/u-s-shale-drillers-could-be-casualties-of-oil-price-war-11583769768

Why is this all so important? Because in many historical peak oil scenarios unconventional oil plays a major mitigating role.

So what were some of the peak oil scenarios? In the following, there is a selection, by no means complete.

(1) 1998 “The end of cheap oil” Colin Campbell and Jean Laherrere

“Our analysis of the discovery and production of oil fields around the world suggests that within the next decade, the supply of conventional oil will be unable to keep up with demand.

….. economists like to point out that the world contains enormous caches of unconventional oil that can substitute for crude oil as soon as the price rises high enough to make them profitable.

….Theoretically, these unconventional oil reserves [Orinoco, tar sands, shale deposits] could quench the world’s thirst for liquid fuels as conventional oil passes its prime. But the industry will be hard-pressed for the time and money needed to ramp up production of unconventional oil quickly enough.

…..In view of these potential obstacles [air pollution, heavy metals and sulfur], our skeptical estimate is that only 700 Gbo will be produced from unconventional reserves over the next 60 years.

….The switch from growth to decline in oil production will thus almost certainly create economic and political tension

….The world could thus see radical increases in oil prices. That alone might be sufficient to curb demand, flattening production for perhaps 10 years.”

https://nature.berkeley.edu/er100/readings/Campbell_1998.pdf

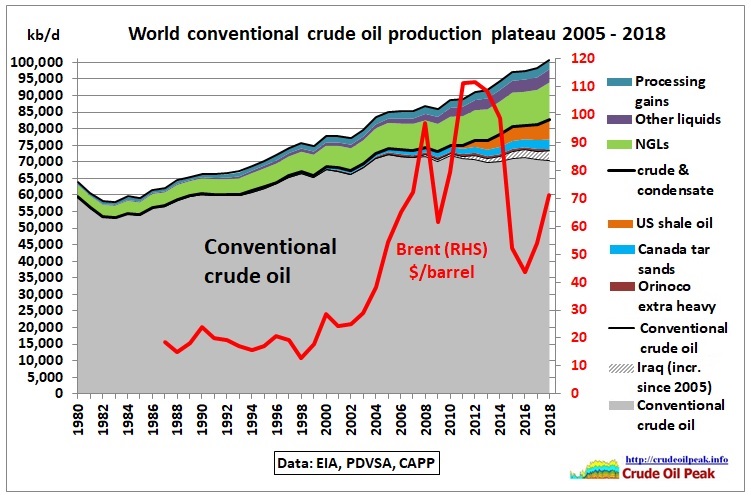

The predicted increase in prices started in 2002 as the North Sea peaked. Conventional crude oil production is basically flat since 2005.

Fig 5: Conventional oil production plus US shale oil, tar sands and natural gas liquids

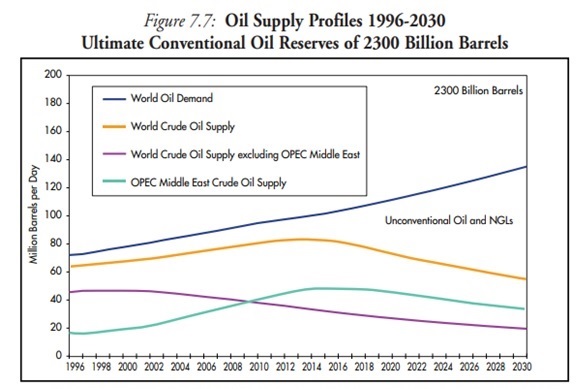

(2) 1998 IEA World Energy Outlook

A peak in conventional oil production was predicted between 2010 and 2020, (Ultimate Reserve of 2,300 Gb). But a “balancing item of unidentified unconventional oil” (tar sands, extra heavy oil, gas to liquids) of 19.1 mb/d in 2020 is expected to fill the gap between demand growing at 2% pa and conventional production. Therefore, the IEA in 1998 did not analyse any impact of peak oil except predicting higher oil prices of $25 in 2013/14, a cap given by the production cost of tar sands and extra heavy oil (table 7.15).

Fig 6: Oil supply scenario for an ultimate of 2,300 Gb in the WEO 1998

https://jancovici.com/wp-content/uploads/2016/04/World_energy_outlook_1998.pdf

Shale oil was not on the radar although fracking was known but $100 oil prices which triggered the 2011 shale boom were unimaginable.

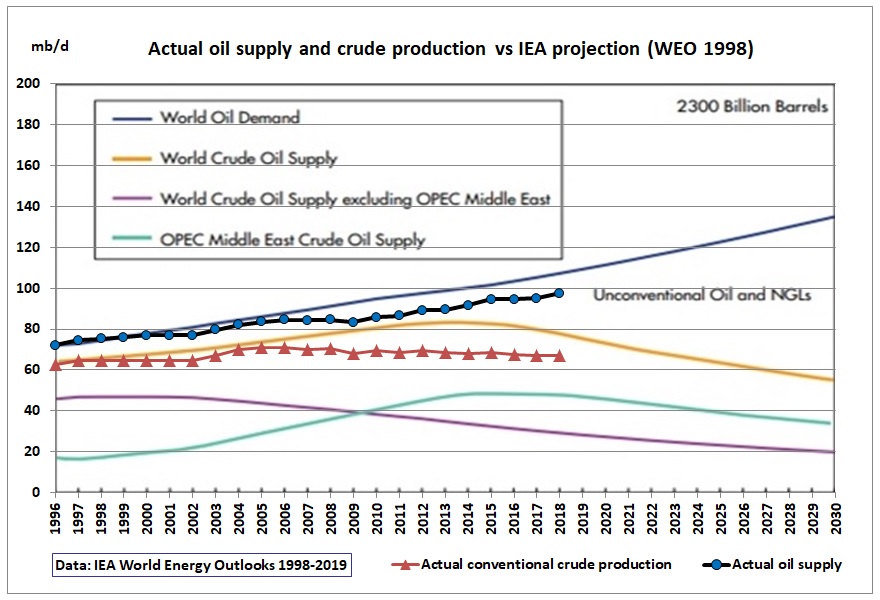

In the following graph we insert actual oil supply and crude production data from all the IEA World Energy Outlooks in the above Fig 7.7, for comparison.

Fig 7: Actual vs projected oil production in WEO 1998

We see that actual conventional crude production started to peak in 2006 at 71 mb/d and in 2014 was 14 mb/d lower than projected in 1998.

(3) 2005 Hirsch report “Peaking of World Oil Production: Impacts, Mitigation & Risk Management

Authors: Hirsch, Bezdek and Wendling

“For purposes of this study, the 1973-74 and 1979 disruptions are taken as the most relevant, because they are believed to offer the best insights into what might occur when world oil production peaks.”

Fig 8: German Autobahn during a Sunday driving ban in November 1973

The Hirsch report mentions as impacts:

- Increase in inflation and unemployment

- Declines in the output of goods and services

- Degradation of living standards

- Job losses not replaced when oil prices decrease

- Sectoral shifts of 10% or more of the labour force

- Economic losses will increase as volatile price cycles continue

- Disruptive inter-sectoral, interindustry and inter-regional effects

- Difficult monetary, fiscal and energy policy decisions

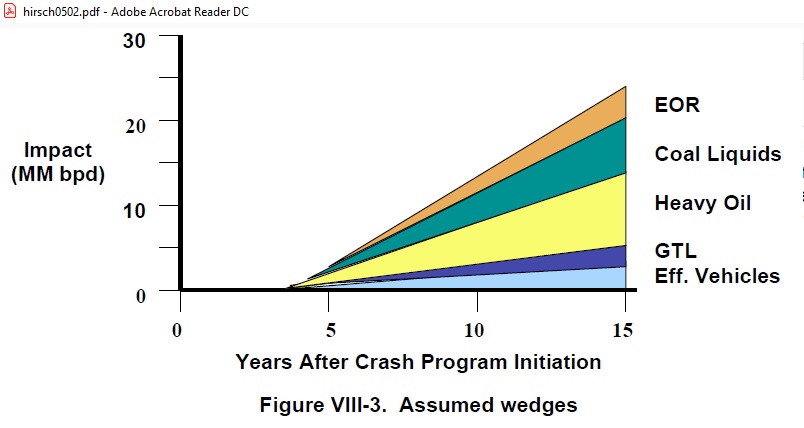

A mitigation wedge was proposed, with 16 mb/d of unconventional oil within 15 years

Fig 9: Feb 2005 PEAKING OF WORLD OIL PRODUCTION: IMPACTS, MITIGATION, & RISK MANAGEMENT

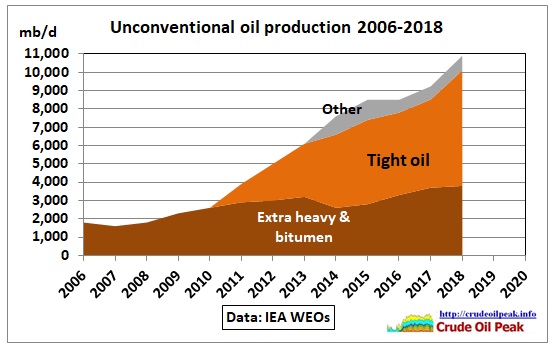

Enhanced oil recovery (EOR) was supposed to be 3.6 mb/d but was only 1.4 mb/d (WEO 2015). Coal to liquids and Gas to liquids (different from NGLs) never materialized in meaningful volumes. Extra heavy oil and bitumen are shown in the following graph. Again, tight oil was not in the mix Hirsch had envisaged but it turned out to make a difference in the mitigation wedge although it is an extra light oil which cannot be used by all refineries in any quantities.

Fig 10: Actual mitigation wedge of unconventional oil

Assuming a start of the mitigation when conventional oil peaked in 2006 the world achieved 11 mb/d after 13 years instead of 18 mb/d in Fig 9.

(4) 2005 Colin Campbell predicts credit crunch due to peak oil 2005

“….but apparently the banks lent more than they have on deposit, and at first sight you say that can’t be possible, but it turned out that it was. And it was because banks had confidence that the resulting expansion of all of this investment and debt and loans and everything was sufficient collateral for today’s debt. So expansion tomorrow covered the debt of today. But, unseen by anybody, or unrecognised, was that this expansion was not just money, it was the good old cheap energy to make the wheels turn and do everything.

So we now face the situation, I think quite soon, when, and this is happening, when the bankers begin to wake up and say, well, this expansion isn’t going to go on anymore without the cheap energy to make it happen. That means that the massive amount of debt throughout the world is losing its collateral. It’s getting a thin, thin cover.”

Published 27/10/2008

https://www.youtube.com/watch?v=lDNMjV6sumQ

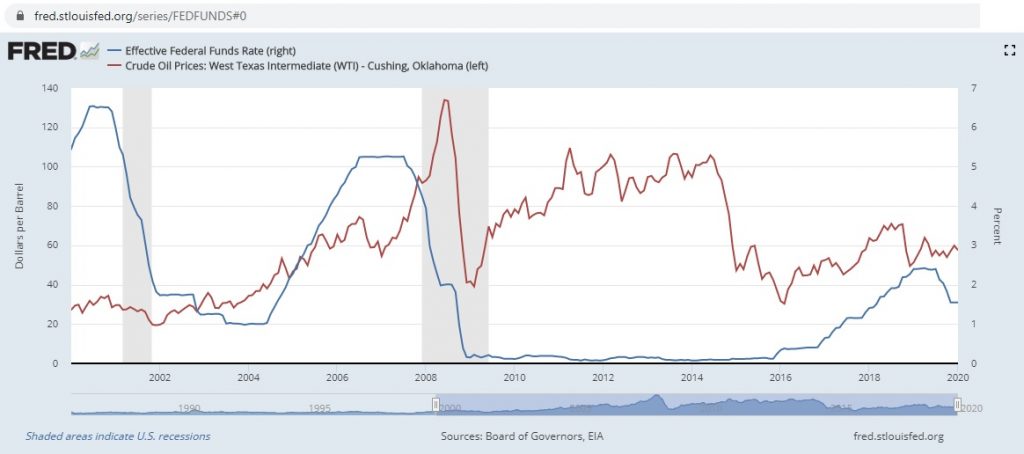

The response of the financial system to the 2008 oil price shock was to lower interest rates

Fig 11: US interest rates were lowered end 2007 and tentatively increased 10 years later

and to implement quantitative easing, in the US QE1-QE3, which both supported high oil prices (until 2014 after QE was ended) and provided cheap money for the US shale oil industry. This meant of course yet more debt.

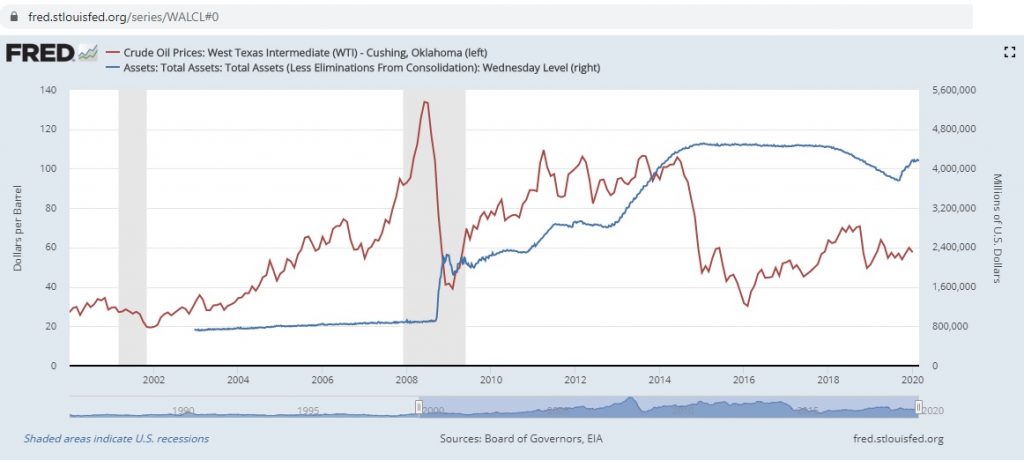

Fig 12: Quantitative Easing (asset purchases) started when low interest rates did not work

https://fred.stlouisfed.org/series/WALCL#0

The Corona virus crisis is now being compared with the financial crisis in 2009 which was caused by the 2008 oil price shock. Since then the world has been living on the steroids of unconventional oil, printed money and the political narrative of perpetual economic growth.

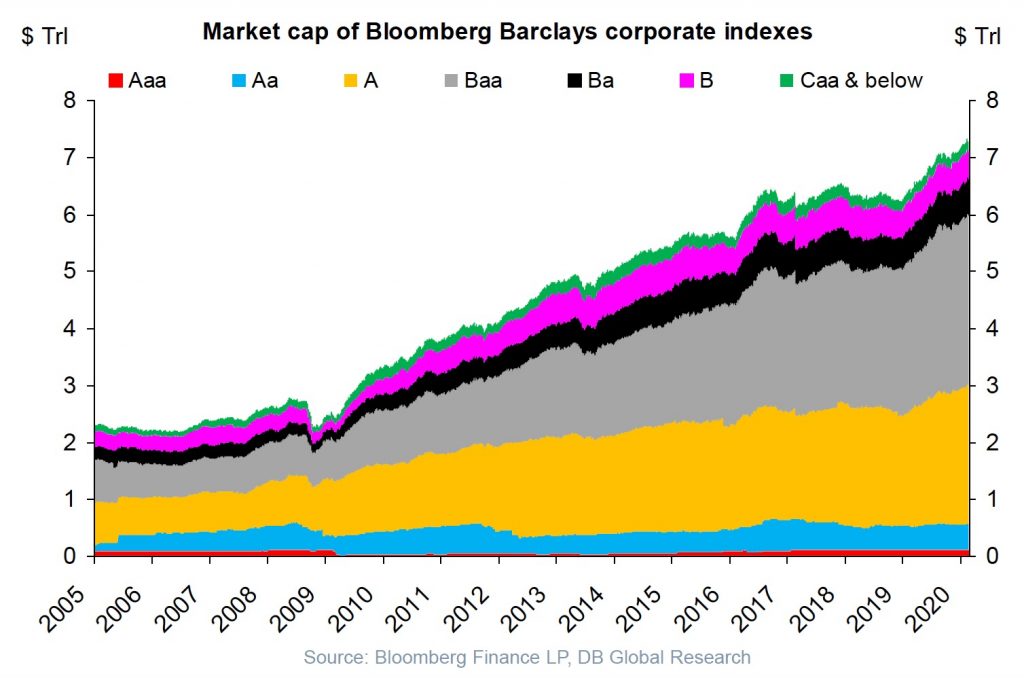

Fig 13: “One of the most dangerous charts in financial markets”

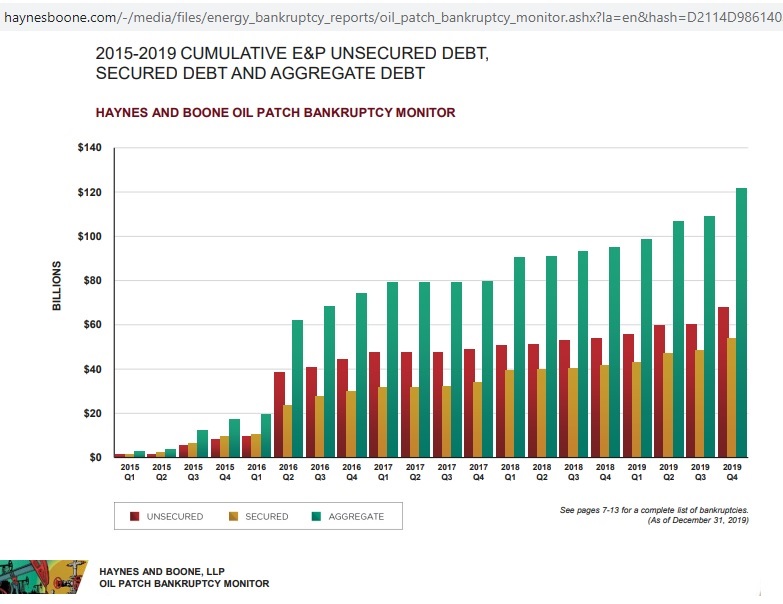

Fig 14: North American oil industry debt

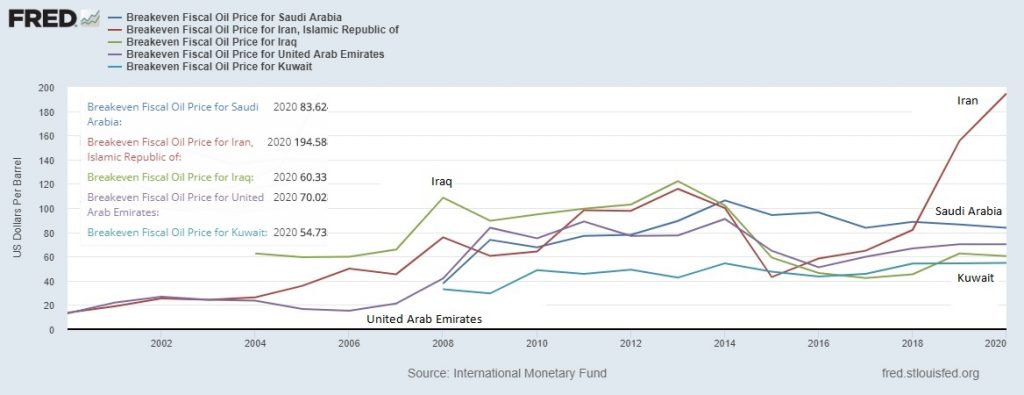

Fig 15: Fiscal Breakeven oil prices of 5 major oil suppliers in the Middle East

Oil price collapse will hurt Gulf states’ finances: Fitch

9 Mar 2020

LONDON (Reuters) – The collapse in oil prices will put pressure on government finances in the Gulf, credit rating agency Fitch said on Monday.

Fitch’s top Middle East and Africa sovereign analyst Jan Friedrich said a $10 drop in crude prices lowered fiscal revenues in the Gulf by 2-4% of GDP, depending on the country.

Summary

Recent travel and transport restrictions have given us the opportunity to relate peak oil predictions to the current state of the oil supply situation. These predictions were all based on higher oil prices which indeed materialized after the Iraq war. The problem we have since the 2008 oil price shock is that oil prices must be both affordable to consumers AND high enough for the oil industry to survive. The Corona virus is hitting an economy and financial system which have a precondition of accumulated debt incurred during the high oil price period and while the era of low cost oil has ended long ago.