The Budget 2017/18 assumes a Tapis oil price of $55/barrel. However, at such low oil prices, oil companies can’t make sufficient investments to offset decline in existing oil fields. Therefore, the International Energy Agency warned on 6th March 2017 – while the budget was prepared:

Fig 1: IEA warning

Fig 1: IEA warning

HOUSTON – Global oil supply could struggle to keep pace with demand after 2020, risking a sharp increase in prices, unless new projects are approved soon, according to the latest five-year oil market forecast from the International Energy Agency.

https://www.iea.org/newsroom/news/2017/march/global-oil-supply-to-lag-demand-after-2020-unless-new-investments-are-approved-so.html

This warning was not new. Already in February 2016 the IEA’s Executive Director, Fatih Birol advised Energy Minister Frydenberg in a meeting that low oil prices could put energy security at risk. A year later Birol had even a meeting with Prime Minister Turnbull:

Fig 2: Turnbull and Birol in February 2017. Oil not discussed?

Fig 2: Turnbull and Birol in February 2017. Oil not discussed?

While Treasury was busy preparing the 2017/18 budget – Fatih Birol also had a meeting with the Minister for Energy.

Although the main topic for discussion reportedly was Australia’s acute power supply crisis during a hot summer month the oil issue must also have been discussed especially as Australia continues to violate its IEA obligations to maintain a strategic oil reserve of 90 days net imports.

The Budget 2017/18, however, does not calculate an impact of higher oil prices in the last 2 years of its forecast period. Nor is all proposed infrastructure designed to help the economy coping with another oil shock. In the contrary, the Prime Minister himself will use taxpayers’ money to finance a 2nd Sydney airport assuming a 1st phase air traffic of 2 million additional passengers pa in the next decade. This will become a stranded asset if a crisis like in 2009 caused demand in Sydney to stagnate or, heaven forbid, to go backwards as it did in 2001/02.

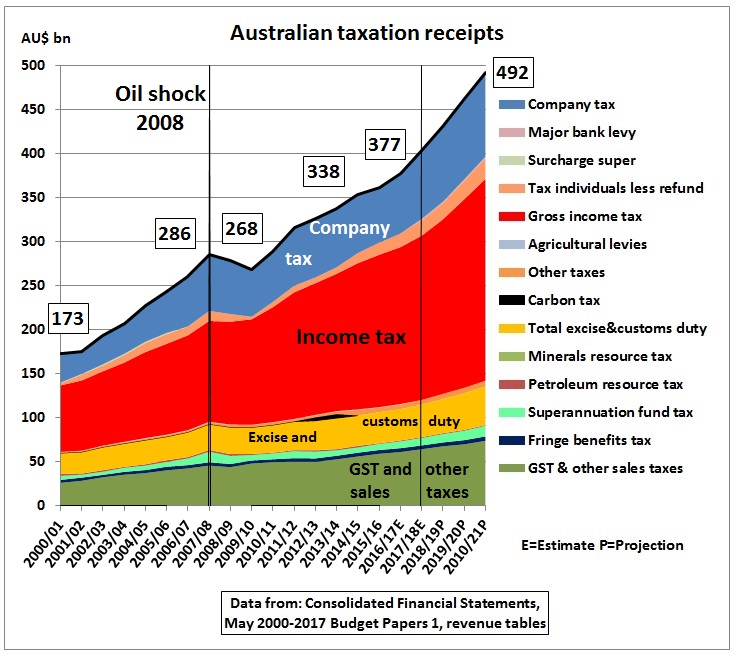

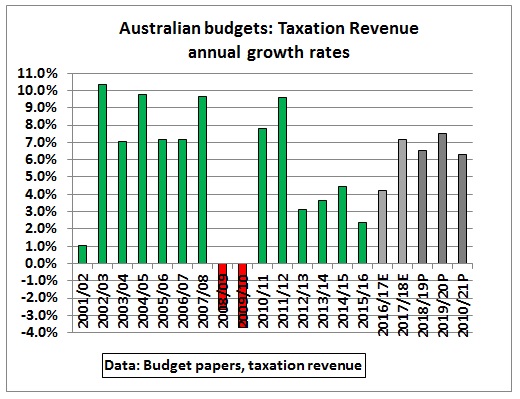

And if, for arguments sake, oil prices went up slowly to the required levels for sufficient investments in the oil sector then assumptions of GDP growth and tax receipts would be too optimistic. We see this in an enormous increase of taxation revenue:

Fig 3: Australian taxation revenue in 2017/18 budget papers (stacked)

Fig 3: Australian taxation revenue in 2017/18 budget papers (stacked)

What is still not recognized is that the 2008 oil price shock caused the financial crisis. Already in April 2009 James Hamilton wrote in an analysis of the 2007/08 US recession:

“And certainly to the extent that the oil shock made a direct contribution to lower income and higher unemployment, that would also depress housing demand. For example, the estimates in Hamilton (2008) imply that a 1% reduction in real GDP growth translates into a 2.6% reduction in the demand for new houses. Eventually, the declines in income and house prices set mortgage delinquency rates beyond a threshold at which the overall solvency of the financial system itself came to be questioned, and the modest recession of 2007:Q4-2008:Q3 turned into a ferocious downturn in 2008:Q4”

http://econweb.ucsd.edu/~jhamilton/Hamilton_oil_shock_08.pdf

In Australia, in February 2009, the government was forced to pump $42 bn stimulus into the economy.

Fig 4: Treasurer Swan and Premier Rudd trying to fill a hole in the economy

http://www.smh.com.au/articles/2009/02/04/1233423265116.html

Their work entered as “Labor’s debt” into the political debate even as recently as 2016. John Howard who was lucky enough to have lost the 2007 election would have faced the same situation, although he might have spent the stimulus in a different way.

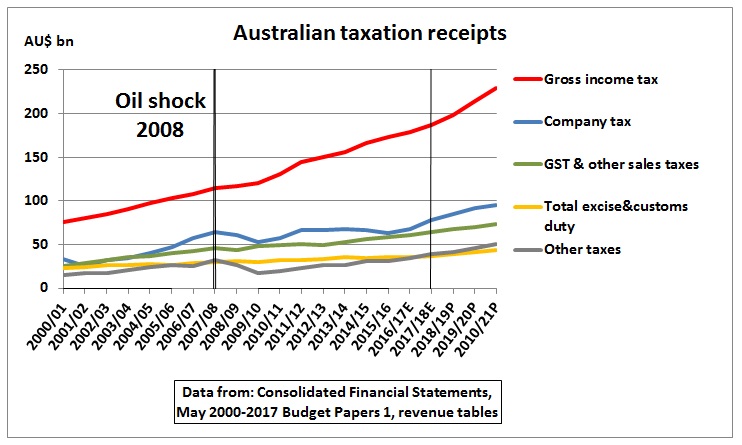

Fig 5: Australian taxation revenue in 2017/18 budget

Fig 5: Australian taxation revenue in 2017/18 budget

(line graph – not stacked)

The biggest hole came from a dip in company tax which remained practically flat since 2008.

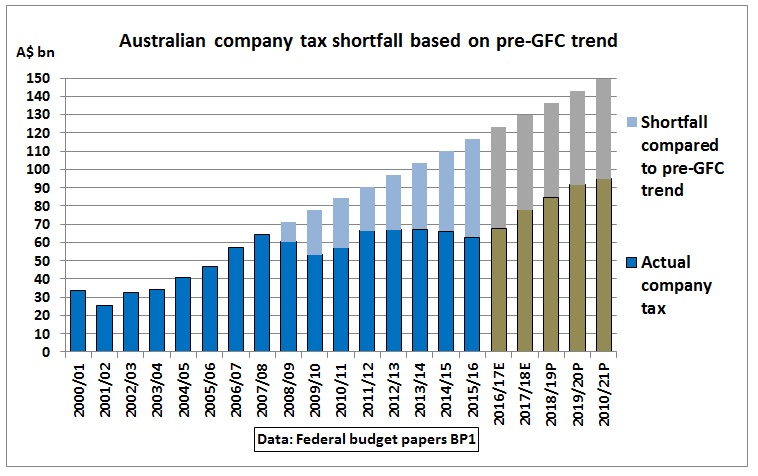

Fig 6: Company tax shortfall after the financial crisis (light blue and grey)

Fig 6: Company tax shortfall after the financial crisis (light blue and grey)

Up to 2016/17 a total of $306 bn revenue from company tax was lost. We see that the budget 2017/18 assumes that company tax resumes its pre-GFC growth path in the next years. This has been designed so that the budget comes back into surplus, an objective which remained elusive after the oil shock.

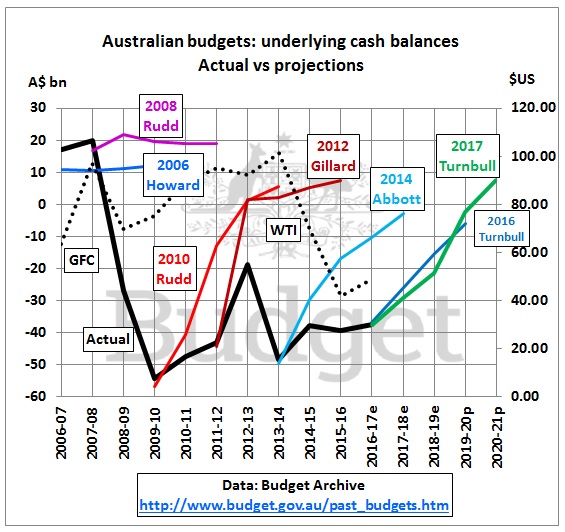

Fig 7: Underlying cash balance since Howard

Fig 7: Underlying cash balance since Howard

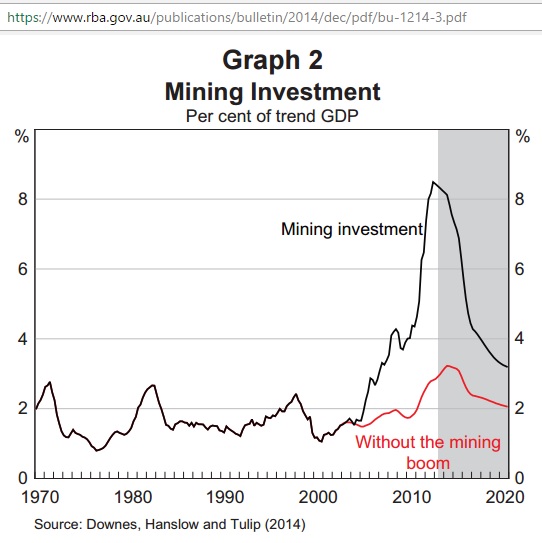

Many attempts have been made to get out of a negative cash balance. A low oil price is a good pre-condition for future budgets to get out of the red but there is a lag between a lower oil price and a better budget performance. Many other factors are at play like the end of the mining investment boom although this is also indirectly related to oil prices and their impact on commodity prices affordable by Australia’s trading partners.

Fig 8: Australia’s mining investment

Fig 8: Australia’s mining investment

https://www.rba.gov.au/publications/bulletin/2014/dec/pdf/bu-1214-3.pdf

The increase in investment spending in the mining sector from 2% of GDP in 2005 to 8% in 2013 helped Australia to bring back revenue growth to pre-GFC levels for 2 years.

Fig 9: Taxation revenue growth rates

Fig 9: Taxation revenue growth rates

As shown in Fig 9, revenue growth rates are estimated and projected to recover to quite high levels. Have they been modeled on future oil prices however difficult and uncertain this may be?

Let’s search for the word “oil” in budget paper 1. It occurs 7 times on 354 pages. It is contained in “turmoil” and “soil” (typical for many documents) so we have only 5 matches.

(1) Oil price assumption (p 2-6)

Note: The forecasts for the domestic economy are based on several technical assumptions. The exchange rate is assumed to remain around its recent average level — a trade‑weighted index of around 65 and a US$ exchange rate of around 76 US cents. Interest rates are assumed to move broadly in line with market expectations. World oil prices (Malaysian Tapis) are assumed to remain around US$55 per barrel.

(2) Trade and oil price (p 2-8)

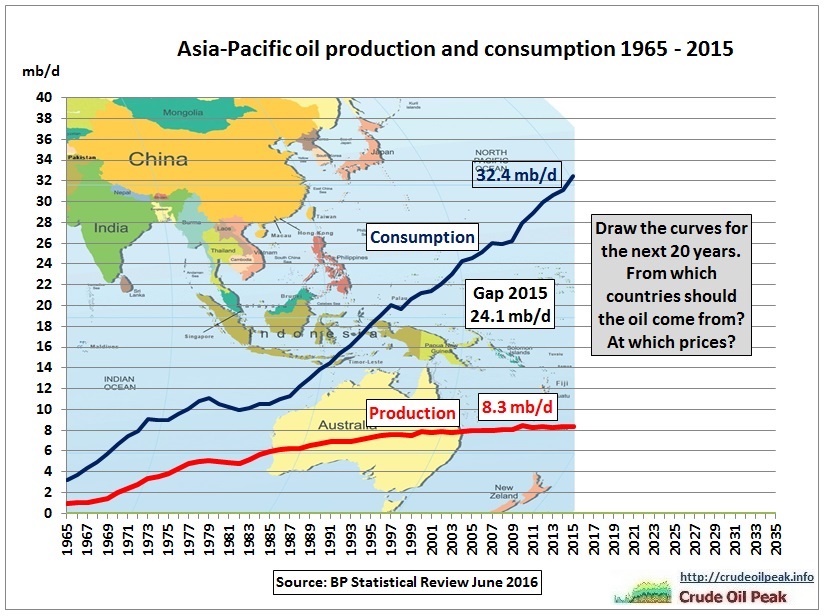

… there are positive signs in some of Australia’s key trading partners in Asia, with China, Japan and South Korea recording recoveries in export value growth in recent months. This follows a period of weakness over the past couple of years that is similar in magnitude to other significant trade downturns of the past 20 years. The recovery in export values partly reflects foreign exchange and commodity price movements, with oil prices regaining some ground over the past year from lows seen in early 2016. However, there is evidence of stronger growth in exports of capital goods from these countries, providing some positive indicators about global demand for investment goods.

Comment: Asia is a net importer of oil. So higher oil prices are not good news.

Fig 10: Oil production and consumption in Asia/Pacific

Fig 10: Oil production and consumption in Asia/Pacific

(3) Petroleum resource rent tax (p 5-13)

Petroleum resource rent tax (PRRT) receipts are forecast to grow by around 30 per cent in 2016-17 and remain at a similar level in 2017-18. Since the 2016-17 MYEFO, receipts are expected to be $50 million higher in 2016-17, $100 million higher in 2017-18 and $350 million higher over the four years to 2019-20. The revision to PRRT is consistent with higher Australian dollar oil prices.

PRRT liabilities depend on prices and volumes of the relevant commodities as well as deductions for expenditure, particularly capital expenditure which is immediately deductible. Expenditure deductions can be uplifted and carried forward to future years, so there can be long delays between a project starting production and having to pay PRRT. In a given year, projects may not pay PRRT if their pool of deductible expenditure exceeds their PRRT income.

On 30 November 2016, the Government announced an independent review into the operation of the PRRT, crude oil excise and associated Commonwealth royalties. The report was released on 28 April 2017 and is available on the Treasury website. The Government has accepted the recommendation of the report for further consultation prior to providing a considered response later in the year

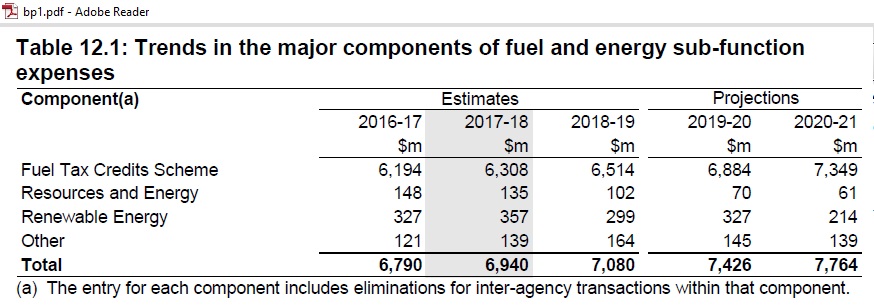

(4) Expenses on fuel and energy (p 6-33)

Fig 11: Subsidised mining truck

Fig 11: Subsidised mining truck

The fuel and energy function includes expenses for the Fuel Tax Credits and Product Stewardship Waste (Oil) schemes, administered by the Australian Taxation Office. It also includes expenses related to improving Australia’s energy efficiency, resource related initiatives, and programs to support the production and use of renewable energy

Fig 12: Fuel Tax Credit scheme costs more than $6bn pa on an increasing trend

Fig 12: Fuel Tax Credit scheme costs more than $6bn pa on an increasing trend

The major program within this function is the Fuel Tax Credits Scheme, which is estimated to decrease by 0.1 per cent in real terms from 2016-17 to 2017-18 and increase by 8.9 per cent in real terms from 2017-18 to 2020-21.

Accumulated borrowings in the period 2007-2018 for fuel and energy amounted to $5.2 bn, requiring $200m in interest payments in 2017-18, on a pro rata basis of total borrowings (table 7, p 4-18)

Scenario planning (Statement 8)

The budget’s scenario planning refers to following factors

- GDP dependent on exchange rate (effect on imports and exports)

- interest rates

- commodity prices

- events in the international economy

These factors impact on the forecasting of taxation receipts, payments and cash balances.

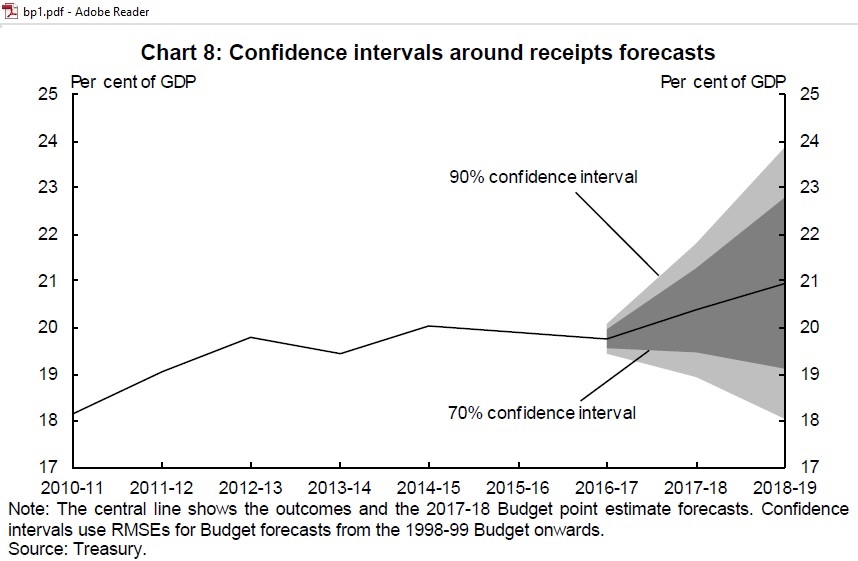

Fig 13: Receipt forecasts

Fig 13: Receipt forecasts

As Fig 13 shows, the uncertainties are huge, with 2018/19 forecast receipts between 18% and 24% of GDP. The resulting cash balances range from -4% of GDP to +2% of GDP.

Following scenarios were considered:

Scenario 1: Alternative path for the terms of trade

Scenario 2: Delayed recovery in non-mining business investment

Scenarios 3 and 4: Alternative output gap adjustment period assumptions

Scenarios 5 and 6: Alternative trend labour productivity growth assumptions

There is no oil shock scenario.

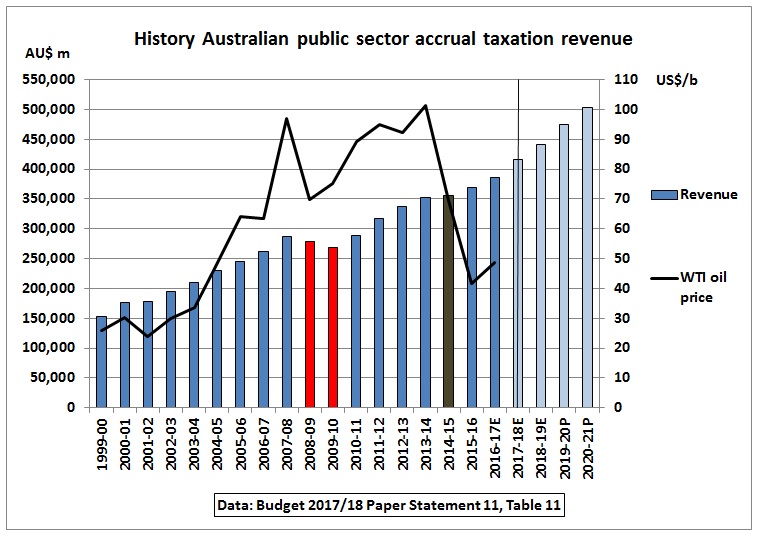

Fig 14: Taxation revenue vs oil price

Fig 14: Taxation revenue vs oil price

The 2008 oil price shock (and the ensuing financial crisis) left its mark on the taxation revenue (red columns). High oil prices in 2013-14 also dampened revenue growth although not as much as in 2008-2010 because of low interest rates.

Conclusion

Future oil markets have not been modeled. A prudent approach would have considered a worst case scenario. But this is not even on the government’s radar. It seems there is little consultation between the Treasurer and the Energy Minister on oil supply and oil prices. Or the problem is ignored altogether.

Related post:

28/6/2016 80% of Australian budget deficit comes from lower company tax revenue after GFC (part3)

http://crudeoilpeak.info/80-of-australian-budget-deficit-comes-from-lower-company-tax-after-gfc-part-3