Diesel is the most important fuel to sustain the economy.

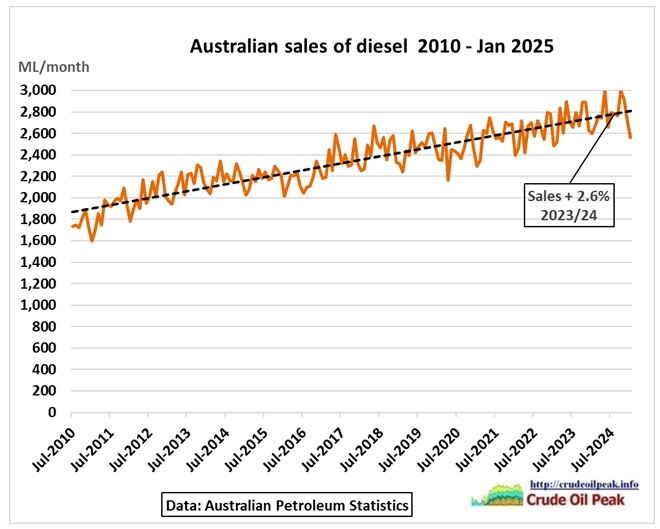

Fig 1: Australian Diesel consumption has been increasing on a long-term trend

Fig 1: Australian Diesel consumption has been increasing on a long-term trend

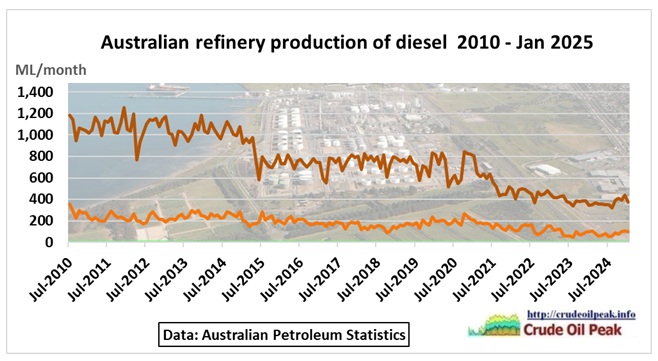

Fig 2: Australian refinery production of diesel in decline

Fig 2: Australian refinery production of diesel in decline

Only 2 refineries remain – Viva in Geelong (pic above) and Ampol Lytton in Brisbane. The use of indigenous oil in these refineries is also down, 25 years after Australian crude oil production peaked.

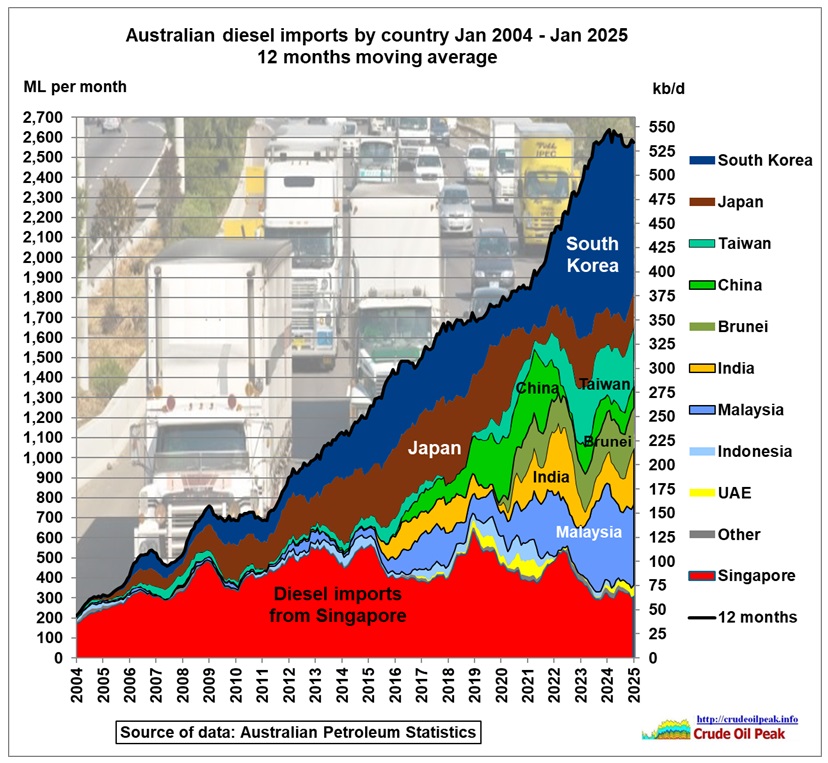

Increasing demand and closing refineries resulted in skyrocketing imports of diesel:

Fig 3: Australia’s Diesel imports by origin

Fig 3: Australia’s Diesel imports by origin

More than half (53%) of the imports come from countries potentially impacted by a military confrontation in East Asia: Taiwan, China, South Korea and Japan.

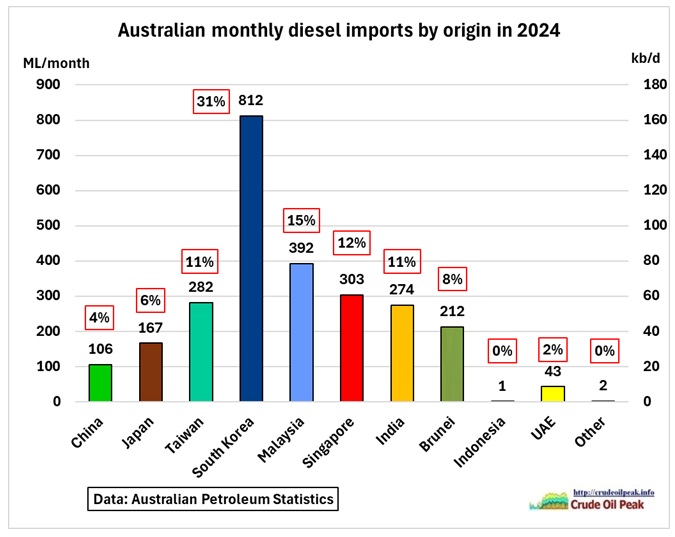

Fig 4: Diesel import shares

Fig 4: Diesel import shares

There are many recent – and conflicting – articles and documents about a possible invasion of Taiwan by China. There seem to be several military scenarios:

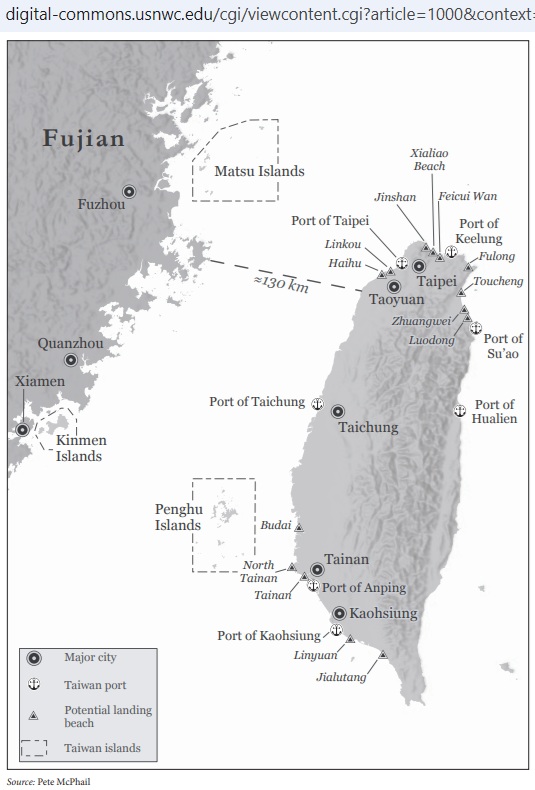

- Seizure of Kinmen (Quemoy) and Matsu island just 10 kms off the coast of China. These island already faced shelling in the 1950s https://history.state.gov/milestones/1953-1960/taiwan-strait-crises

Fig 5: Taiwan and location of Taiwanese islands

Fig 5: Taiwan and location of Taiwanese islands

- Air and maritime blockade of Taiwan including cutting off Taiwan’s vital imports

- Limited Force or Coercive Options to undermine the effectiveness or legitimacy of the Taiwan authorities, thereby mobilizing pro-Beijing members of the KMT party

- Precision missile and air strikes to destroy air bases, radar sites, missile depots, space- and communications facilities, but hopefully avoiding Taiwan’s semiconductor industry (TSMC) which has already decentralized manufacturing to Kumamoto (December 2024, Kyushu, Japan) and is currently building new factories in Arizona (2025) and Dresden, Germany (2027).

- Amphibious Invasion of Taiwan. CMSI Study No. 8 Prospects for a Cross-Strait Invasion (US Naval War College) https://digital-commons.usnwc.edu/cgi/viewcontent.cgi?article=1000&context=cmsi-studies

2027 is the year for the 21st CCP Congress during which Xi Jinping wants to secure his 4th five year term. Progress towards the declared objective of reunification with Taiwan would help him to be seen as following in the footsteps of Mao Zedong. The 100th anniversary of the PLA is also celebrated in 2027. The above quoted DoD report does not refer to 2027 as a possible deadline for an invasion but as a milestone for the PLA’s modernization goals.

There are recent reports about personnel purges of Xi’s allies in the PLA

https://jamestown.org/program/personnel-problems-are-becoming-personal-problems-for-xi-jinping/

No one knows how this internal power struggle will play out in relation to a Taiwan timetable.

The Air University in Alabama has listed a number of criteria which are under consideration by the leadership in Beijing.

Xi Jinping’s Taiwan Dashboard: Considering Xi’s Calculus for a Possible Move on Taiwan

21 Apr 2025

“This article dissects 13 key indicators shaping Beijing’s decision on whether and when to invade Taiwan, alongside four enduring factors reinforcing China’s long-term objective to acquire Taiwan. The analysis finds that 11 of the 13 indicators favor near-term action, suggesting a closing window of opportunity that could drive Xi toward a military solution sooner rather than later.”

Indicator 11 says: “Counterintuitive though it may seem, worsening ties between Beijing and Washington could lower the diplomatic cost of aggression, making it easier—not harder—for China to move against Taiwan.”

https://www.airuniversity.af.edu/JIPA/Display/Article/4168508/xi-jinpings-taiwan-dashboard-considering-xis-calculus-for-a-possible-move-on-ta/

In the meantime “worsening ties between Beijing and Washington” have evolved into Trump’s full scale trade war against China which will weaken both countries and introduces yet another factor into the “Taiwan Calculus”. And how would a possible military conflict with Iran play out both in terms of oil supplies for Asia and the scale of operations around Taiwan? Many questions.

Crudeoilpeak is not a military website. It looks at oil statistics.

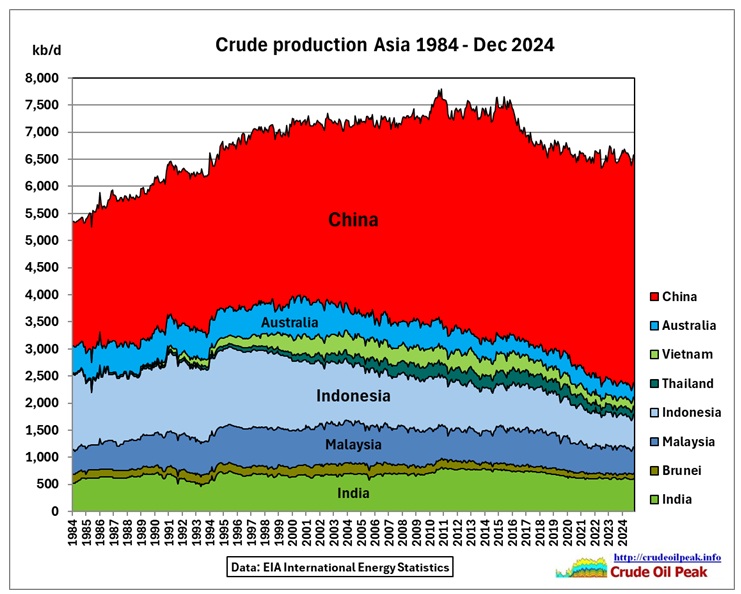

Fig 6: Crude oil production in Asia

China started to peak in 2015 which defined the total Asian peak. All other countries together peaked already in 2001.

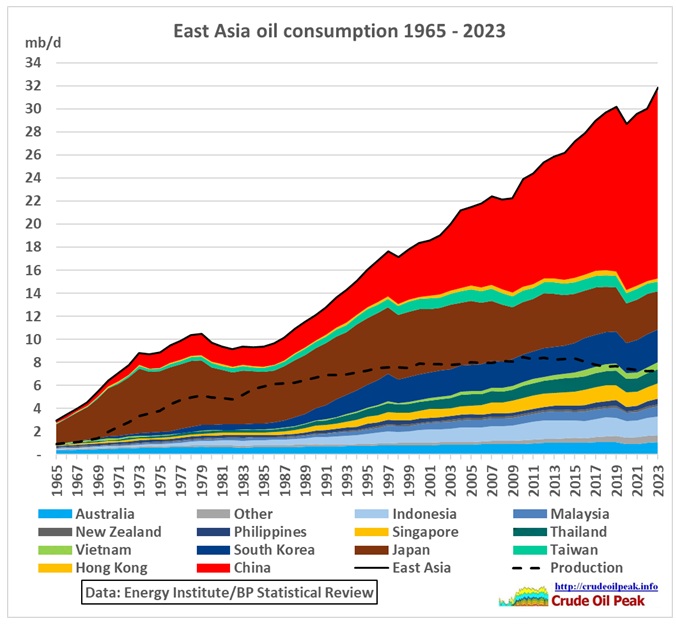

Fig 7: East Asia oil consumption (includes natural gas liquids)

Fig 7: East Asia oil consumption (includes natural gas liquids)

Data for 2024 will be available in June 2025.

Except for Japan, East Asian oil consumption has increased over 40 years, with 3 interruptions: the Asian Financial crisis in 1997/98, the 2008/09 oil price shock/GFC and the Wuhan virus.

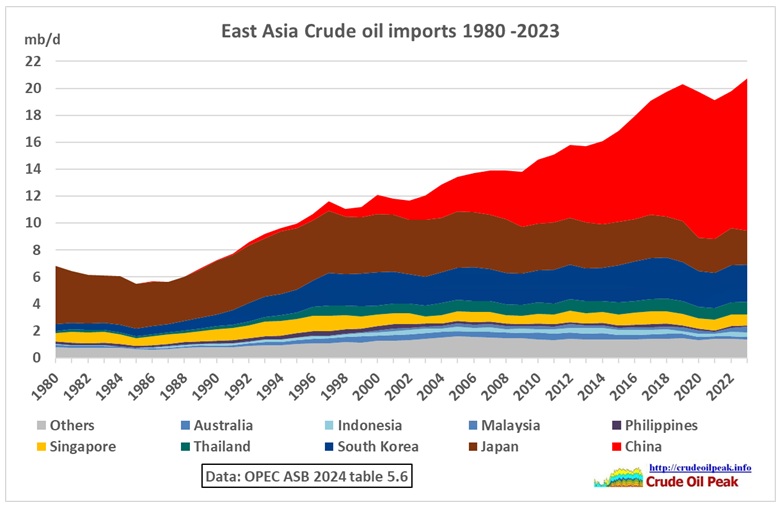

As a result of peaking oil production and rising oil consumption, crude oil imports have also increased substantially:

Fig 8: East Asia crude oil imports

In case of a blockade, China will selectively allow and protect tankers to its own refineries to pass through the Strait of Taiwan. Japan and South Korea would have to do the same in the Luzon and Miyako Straits, resulting in delays and higher costs.

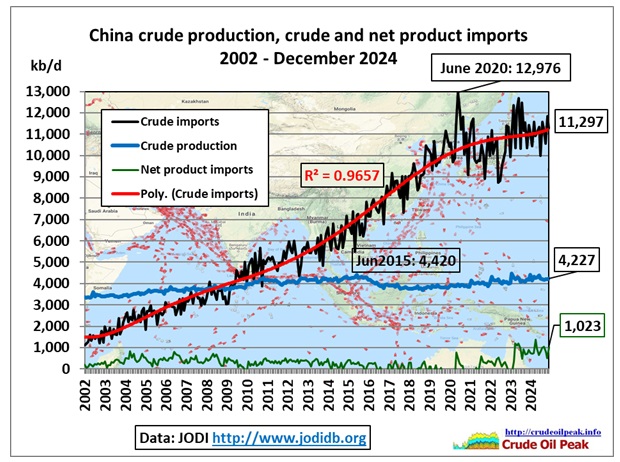

Fig 9: China crude oil production and imports

Fig 9: China crude oil production and imports

China’s crude oil imports stopped growing when the self-inflicted Wuhan virus hit.

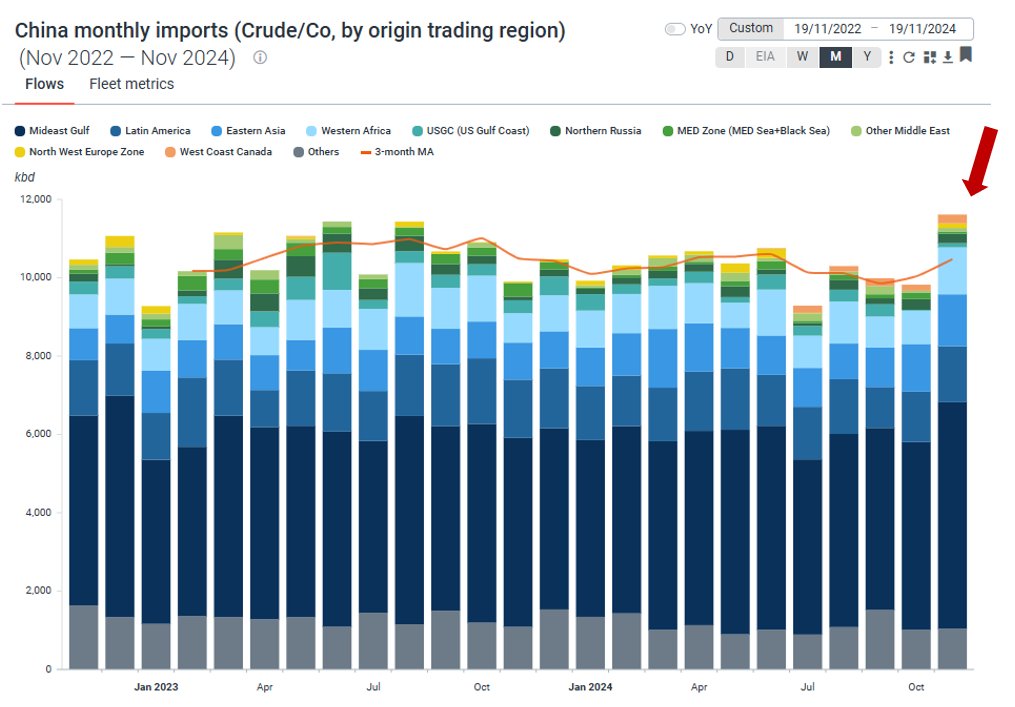

Fig 10: China’s crude oil imports mainly depend on the Middle East at about 50% (Kpler)

Fig 11: China oil infrastructure

Fig 11: China oil infrastructure

https://jpt.spe.org/map-china-oil-infrastructure-tracks-more-700-facilities

On 13 June 2024 the U.S.-China Economic and Security Review Commission had a hearing on

“China’s stockpiling and mobilization measures for competition and conflict”

https://www.uscc.gov/hearings/chinas-stockpiling-and-mobilization-measures-competition-and-conflict

Wars require a lot of energy. Therefore, increases in production and/or stockpile buildups often occur while a country plans a war.

The Baker Institute (Gabriel Collins) presented this statement titled (p 96)

“Energy Stockpiling as a China Strategic Warning Indicator”

Excerpts:

- China’s total crude storage tank capacity is now somewhere a bit north of 1.8 billion barrels—about 30% larger than total U.S. storage capacity, even though the US still consumes about 25% more oil than China does.

- Between 2016 and early 2024, China’s total observed aboveground crude oil inventory has ranged from 850 million to a bit over 1 billion barrels

- This number includes multiple aboveground strategic petroleum reserve sites with a total storage capacity of approximately 200 million barrels of crude oil

- China also has operational underground crude oil storage facilities at Huangdao, Jinzhou, Zhanjiang, and Huizhou, which between them could store at least 100 million additional barrels

- China could have nearly 300 million barrels of additional “headroom” across its oil storage complex if it chose to maximally stockpile ahead of an expected contingency

Strategic Warning Signals to Watch For

- Aboveground crude oil storage utilization rates topping 65% of capacity

- Construction of more underground crude oil storage facilities

- Increased levels of oil tanker activity indicating the filling of underground storage

- Construction of new cross-border oil pipelines or expansion of existing oil pipelines

- Increased activity at refined product storage depots within 500 miles of Taiwan

- Expansion of coal inventories above 3-year and 5-year averages

- Attempts to interfere with synthetic aperture radar (SAR) measurements

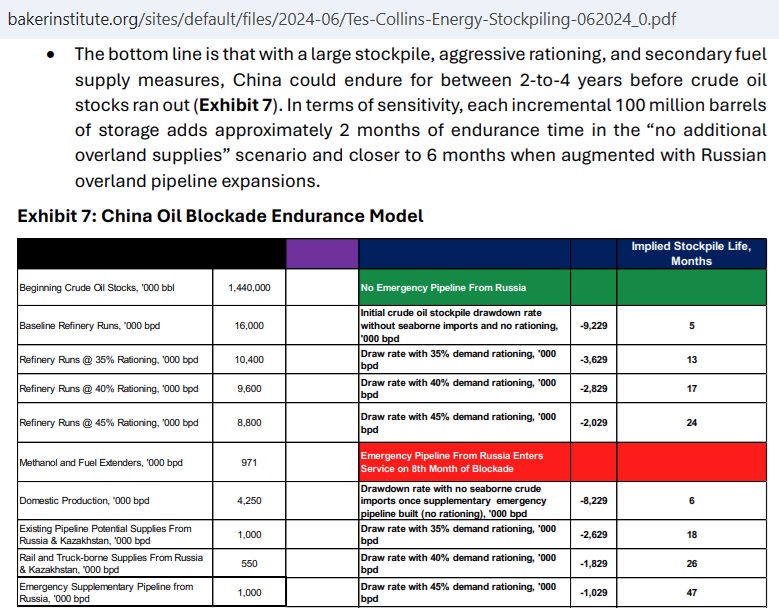

Fig 12: China Endurance Model (p 12)

The word “blockade” in exhibit 7 refers to a maritime blockade against China. Gabriel Collins wrote in 2018 this paper: “A Maritime Oil Blockade Against China—Tactically Tempting but Strategically Flawed”

https://digital-commons.usnwc.edu/nwc-review/vol71/iss2/6/

Baker’s endurance model does not say how the population would react under a 35% rationing nor how the economy would go to its knees even within a couple of months. However, there are many interesting articles in the reading and reference list of the above Baker Institute paper.

URSA SPACE has a series of articles on inventories in China, supporting the work of the Bake Institute

10 July 2024

Part 1: Monitoring China’s energy sector

https://ursaspace.com/blog/overview-china-risk-series/

18 July 2024

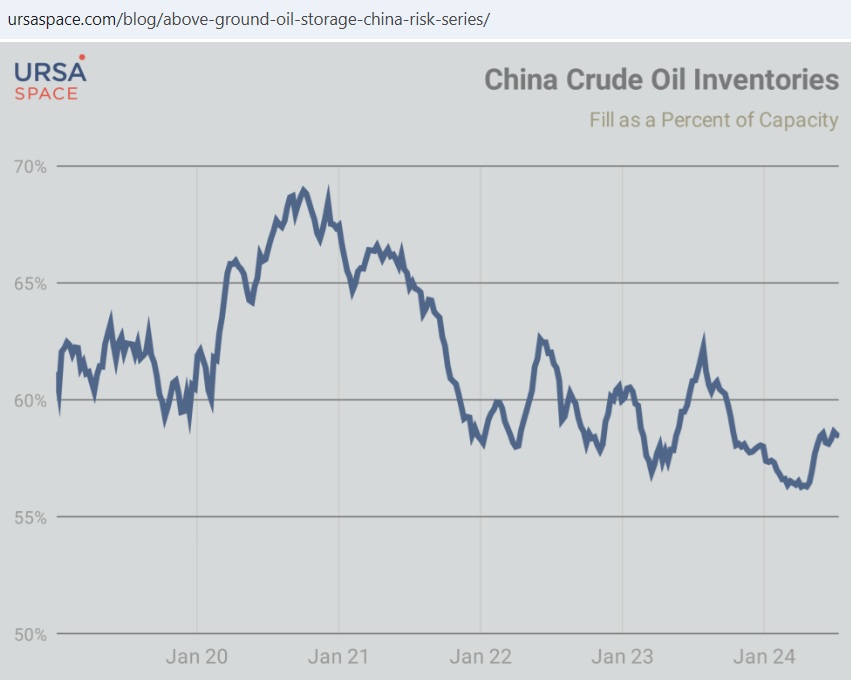

Part 2: China’s above ground oil storage

Fig 13: China crude oil inventories. Note the 65% “yellow flag”

https://ursaspace.com/blog/above-ground-oil-storage-china-risk-series/

In part 2 of this post we’ll look at how Australian fuel imports would be impacted.