The Federal government refused to financially help car manufacturers and airlines, arguing that companies need to get their “house in order”. The Federal budget is deep in the red. Yet, billions of dollars in subsidies are envisaged to be paid to toll-way operators with the objective to take away risks associated with traffic forecasts. In 4 previous road tunnel projects estimates of future traffic were inflated in planning documents with the objective to get these projects off the ground. But ultimately this led to their bankruptcy. How about if toll-way operators and their consultants first got their house in order? And that would start by doing a proper analysis of oil supplies for the planning period.

These conceptual contradictions and embellishments are worsened by total planning chaos on a procedural level. An “innovative” tender process has selected a contractor for a road tunnel project in Sydney before an EIS (environment impact study), a cost benefit analysis, debt repayment plans, oil & energy and CO2 calculations were done. We can assume that the outcome is pre-determined and the numbers in the EIS will be tweaked.

In the completion year 2019 US shale oil will have likely peaked, the Middle East further disintegrated and oil production in many countries continued its decline. Northconnex and other planned toll-way projects will increase Australia’s oil vulnerability and the economic burden of imported crude, imported fuel and imported cars and trucks which is being deducted from the domestic purchasing power.

North Connex tunnel: Tony Abbott and Barry O’Farrell give go-ahead to $3 bn project to link M1 and M2 in Sydney.

16/3/2014

“The Commonwealth will invest $405 million in the $3 billion NorthConnex to build the missing link between the M1 and M2 motorways to reduce congestion, shorten travel times and improve the safety of our roads.”

The project was signed off between the State Government and the former Labor federal government last year, with each committing more than $400 million in funding.

But the Prime Minister says it is now happening under his watch.

He says construction on the nine-kilometre tunnel will begin next year and is expected to be completed in 2019.

http://www.abc.net.au/news/2014-03-16/nsw-to-start-work-on-northconnex-tunnel/5324118

16 March 2014

Transurban announces preferred contractor for NorthConnex

Transurban today welcomed the announcement of the preferred contractor for the M1 to M2 project, now known as NorthConnex, taking the motorway project a step closer to reality.

Transurban’s Chief Executive Officer, Scott Charlton, said the consortium Lend Lease Bouygues had a design and construction proposal for the $3 billion project, which includes a construction budget of $2.65 billion along with land acquisition and project delivery costs. This is now subject to planning approval and finalisation of contract.

“We have gone through a unique and innovative competitive tender process to select Lend Lease Bouygues as the design and construction contractor. The twin tunnels will provide significant travel time savings for commuters and the freight network benefiting the NSW and Australian economies,” Mr Charlton said. http://www.transurban.com/140313_transurban_announces_preferred_tenderer.pdf

http://www.youtube.com/watch?v=cxU2x79xzd4

http://www.youtube.com/watch?v=cxU2x79xzd4

(1) World in 2019

4 road tunnels have already financially collapsed: X-city and Lane Cove tunnels in Sydney, Clem7 and Airport Link tunnels in Brisbane. Here we get the next candidate. Completion date of 2019? By that time we’ll see:

(1.1) the US shale oil peak

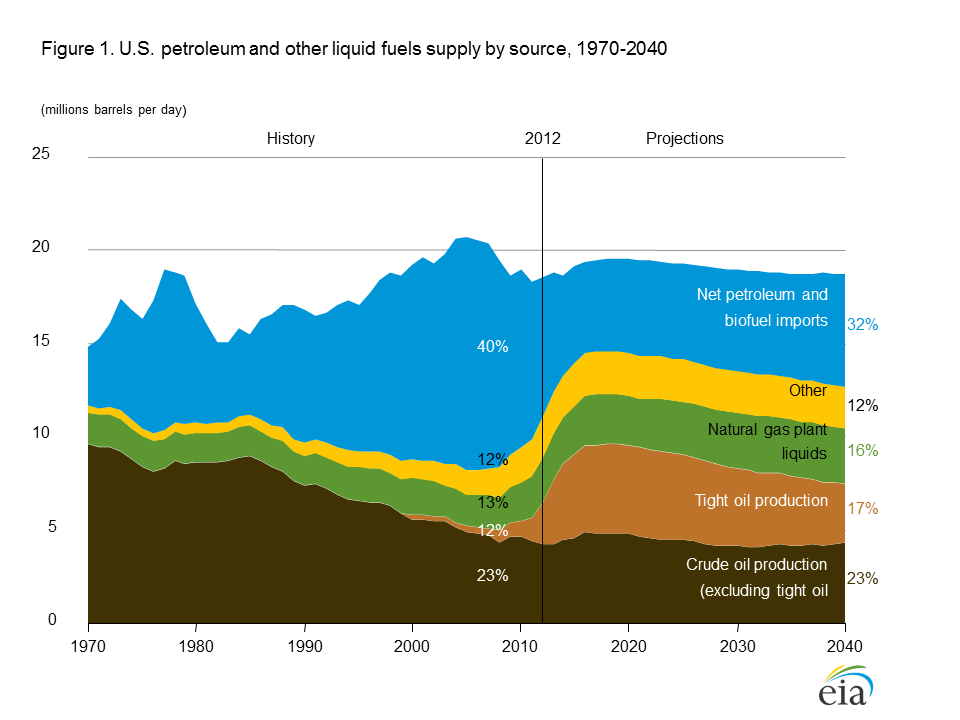

From the EIA’s Energy Outlook 2014 (early release):

http://www.eia.gov/forecasts/aeo/er/images/figure_1es-lg.png

{kind=link}

The US government’s own graph shows that contrary to misinformation about US energy independence, parroted by the media, the US will always import 5- 6 mb/d of oil and biofuels. Importantly, crude oil production starts a plateau of around 9.5 – 9.6 mb/d b (shale oil at 4.7 mb/d) by 2016, lasting until 2020 and followed by a slow descent. But there is disagreement among analysts about the decline rates of shale oil.

The mechanics of shale oil depletion is shown in this graph of the EIA drilling report:

http://www.eia.gov/petroleum/drilling/?scr=email

The upper part of the graph shows the monthly production declines in the Bakken field have been increasing to more than 60 kb/d. This means that more or more efficient drilling at around 80 kb/d has to be done every month not only to offset that decline but also to arrive at a net additional production growth of around 20 kb/d per month. There will be a point where decline in old wells is so high that new drilling can’t keep up. If, for argument sake, drilling were to stop (e.g. as a result of a credit crunch) decline would be a whopping 720 kb/d within 1 year, large enough to upset global oil markets. This is an insight from Rigzone, a professional blog of the oil and gas industry:

Musings: It’s Official – Oil Industry Enters The New Era Of Austerity

20/3/2014

Chevron is the latest major oil company to implicitly declare that the oil industry has entered a new era – one marked by higher costs and more disciplined capital investment programs that will require higher oil prices. Capital discipline forces companies to sacrifice production growth targets on the altar of increased profitability in order to boost returns to shareholders…

Unfortunately, the results of the shale revolution have been disappointing, leading to significant asset impairment charges and negative cash flows as the spending to drill new wells in order to gain and hold leases has exceeded production revenues, given the drop in domestic natural gas prices. Will that capital continue to be available, or will it, too, begin demanding profits rather than reserve additions and production growth?

Geoscientist David Hughes from Global Sustainability Research Inc. calculated a decline of 1.3 mb/d until 2025 in his slide show “Shale Revolution” for First Energy Capital:

.

http://legacy.firstenergy.com/UserFiles/HUGHES%20First%20Energy%20Nov%2019%202013.pdf

(1.2) Russia’s crude oil peak

http://www.hhs.se/SITE/news/Documents/5%20-%20James%20Henderson.pdf

When looking at what is currently happening around the Black Sea maybe the above graph explains something.

Oil flows through 2 pipelines to Black Sea ports will also be impacted by peak oil in Azerbaijan

http://crudeoilpeak.info/azerbaijan-peak

(1.3) Continuing decline in many countries

as shown in the following graph, at around 3-4% pa in the last 5 years

So by 2019 we can expect a total decline of around 5* 3% * 17 mb/d = 2.5 mb/d. More details are in this post:

World crude production 2013 without shale oil is back to 2005 levels

http://crudeoilpeak.info/world-crude-production-2013-without-shale-oil-is-back-to-2005-levels

(1.4) Further disintegration of the Middle East and increasing fuel import vulnerability

In another article, Rigzone describes latest developments, including conflicts between Saudi Arabia and Qatar:

Musings: The Challenges Facing Saudi Arabia Include More Than Oil

21/3/2014

As Saudi Arabia contains the most holy sites of the Islamic religion, the Saudi royal family is its custodian and protector. Recently, a new political struggle erupted when Saudi Arabia listed the Muslim Brotherhood as a terrorist organization and the country withdrawal of its ambassador from Qatar who has been supporting the Brotherhood. The United Arab Emirates, Bahrain and Egypt have followed suit, also withdrawing their ambassadors. The spat with Qatar started a couple of weeks ago at a Gulf Cooperation Council foreign ministers’ meeting held in Riyadh. Saudi Foreign Minister Saud bin Faisal declared that Qatar needed to shut down the television station Al-Jazeera, the Brookings Doha Center and the Rand Qatar Policy Institute if the emirate did not wish to be punished.

At the root of the Qatari dispute is a political clash between the emir of Qatar, Sheikh Tamin bin Hamad, and Saudi Arabia’s King Abdullah bin Abdulaziz over support for Islamist groups perceived to be terrorists by the old, autocratic rulers in the region. The principal focus is on Qatar’s support for the Muslim Brotherhood that was instrumental in helping to depose Egypt President Hosni Mubarak several years ago and replace him with the organization’s president, Muhammad Morsi. The Saudi monarchy has been supportive of the military rulers of Egypt who overthrew the Morsi regime late last year. Saudi Arabia, along with the United Arab Emirates, has sent billions of dollars in order to prop up the military government, with no end in sight to the political and economic chaos in the country.

The Saudi monarchy is, and has been, concerned about the 12% of its population that are Shiite and that live over the Kingdom’s petroleum reserves. The Kingdom is concerned about Shiite Political Islam, the ideology of the Iranian state, which it believes was behind the social unrest in Bahrain during the Arab Spring. Saudi was so concerned about the stability in Bahrain that it sent troops into the country to support the current ruler

The Saudi Royal family was described as both outraged and threatened by the role of Al Jazeera in the first years of the Arab Spring, which saw fellow potentates deposed in Tunisia and Egypt. They have become increasingly upset with Al Jazeera’s sympathetic television coverage of the secular and Islamist opposition in Egypt

4 OPEC countries Saudi Arabia, Iran, Iraq and Libya did not produce more crude oil in 2013 than in 2005 (dashed line). There will be fights over Iraq’s production quota. Saudi Arabia’s production dropped in 2006/07. When finally Khursaniyah came on stream it was not sufficient for an additional demand from China in 2008 for the Olympic Games. When the war started in Libya in 2011 Saudi Arabia could not respond quickly enough, although Khurais and the Shaybah extension had been started in 2009.

Australia depends 37% on the Middle East, directly from imported crude or indirectly from imported fuels:

.

This percentage will increase with every Australian refinery closing

24/6/2013 Australian oil and fuel dependency on the Middle East is 37%

http://crudeoilpeak.info/australian-oil-and-fuel-dependency-on-the-middle-east-is-37

(1.5) Further decline of International Oil Companies

supplying petrol and diesel to Australia

23/2/2014 Geelong refinery sold as Shell’s oil production continues to decline

http://crudeoilpeak.info/geelong-refinery-sold-as-shells-oil-production-continues-to-decline

.![]()

28/8/2013 Chevron’s oil production, sales decline by 5%

http://crudeoilpeak.info/chevrons-oil-production-sales-decline-5

As Caltex is closing in the 4th quarter of 2014 this means increasing vulnerability to spot fuel markets.

(1.6) 90 million new cars on China’s roads to compete with for crude/petrol

.

http://www.oica.net/category/production-statistics/

Most of these new cars will boost the car fleet, as scrappage rates are still low.

Vehicle fleet growth projected by the IEA in its WEO 2013 http://www.worldenergyoutlook.org/publications/weo-2013/

China’s oil demand has been growing almost steadily:

Average annual demand growth is 450 kb/d. For comparison: Australian total product sales are 950 kb/d. This means every 2 years China adds oil demand equivalent to 1 Australia. Data for these graphs are from: http://omrpublic.iea.org/

(2) Problems already during any tunnel construction

Why will there be another oil price spike in the next years?

Ex-Saudi Aramco geologist Dr. Husseini: My base oil price forecast in 2012 dollars still ranges between $105 and $120/barrel Brent with a volatility floor of $ 95/barrel and more probable upward spiking to $140/barrel within 2016/2017.

The realities of the 2009 Oil & Money [conference] forecast of a limited plateau of oil supplies have been pretty much vindicated since then. The oil plateau may now be inflated by about 1 – 2 Mbd of high cost unconventional oils but all major forecasters see this as pretty much transitional. The plateau itself remains a reality and unfortunately its duration is still unlikely to extend beyond the end of this decade.”

http://peak-oil.org/2014/01/13716/

.

Dr. Husseini’s 2009 oil production projection was 600 kb/d lower than actual production. Adjusting for this and adding 2 mb/d for US shale oil gives the blue line in the above graph. Comparing shifted production with growing oil demand shows that a gap opens in the 2nd half of this decade, widening towards 2030. More details are in this post:

15/3/2014 Ex-Saudi Aramco geologist Dr Husseini predicts oil price spikes of USD 140 by 2016-17: graphs

http://crudeoilpeak.info/ex-saudi-aramco-geologist-dr-husseini-predicts-oil-price-spikes-of-usd-140-by-2016-17-graphs

We don’t know under whose watch that will happen but it won’t be a happy ending for a road tunnel under construction. The last time we had an oil price spike it triggered a financial crisis. In addition, the Australian Dollar is expected to go down so petrol and diesel prices will go up:

14/3/2014 Goldman Sachs: AUD heading to US80 cents

http://www.smh.com.au/business/markets/currencies/australian-dollar-heading-to-us80c-goldman-sachs-20140314-34qpl.html

The ACCC had calculated what a lower AUD will mean:

15/12/2013 Lucky country dodged $2 a litre bullet – for now

http://crudeoilpeak.info/lucky-country-dodged-2-a-litre-bullet-for-now

Conclusion:

In this 1st part we have been looking at oil supplies in the next years. US shale oil has moved the moment of the truth a couple of years into the future but ultimately decline in conventional oil fields will win, not governments and banks ignoring it. The next part will analyse which documents have been prepared for the road tunnel and whether a range of benefit cost ratios have been calculated before spending serious design money and starting land acquisitions.