This post will be updated from time to time

https://treasury.gov.au/review/economic-reform-roundtable

Energy is the economy and the economy is energy

On the eve of the talkfest:

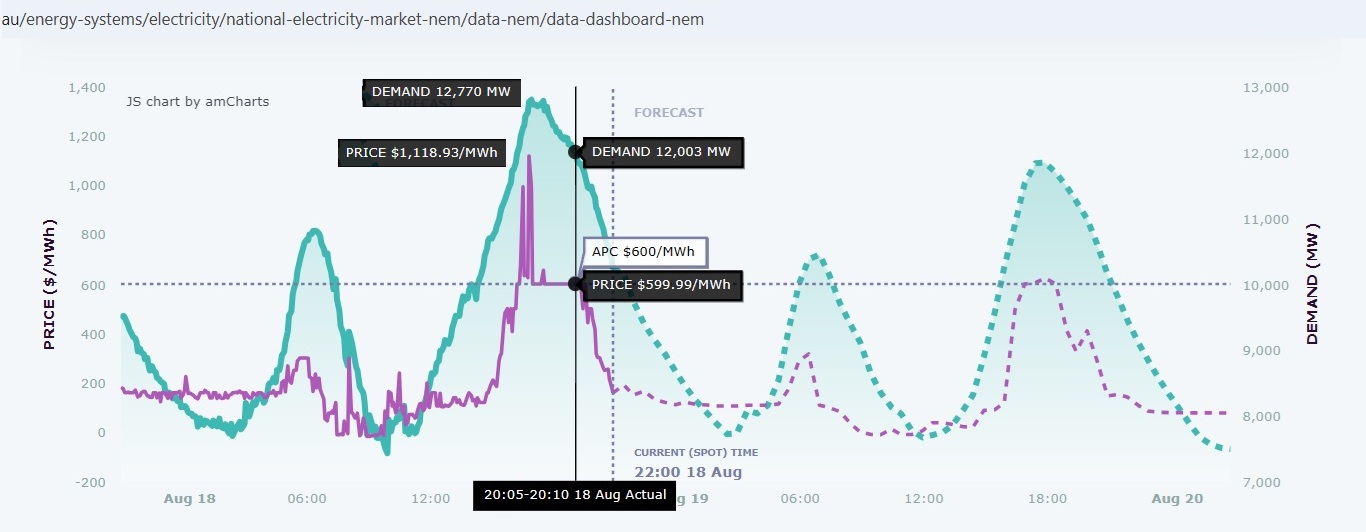

128570 RESERVE NOTICE 18/08/2025 05:43:38 PM

Actual Lack Of Reserve Level 1 (LOR1) in the NSW region – 18/08/2025

AEMO ELECTRICITY MARKET NOTICE

Actual Lack Of Reserve Level 1 (LOR1) in the NSW region – 18/08/2025

An Actual LOR1 condition has been declared under clause 4.8.4(b) of the National Electricity Rules for the NSW region from 1730 hrs.

The Actual LOR1 condition is forecast to exist until 1900 hrs

The capacity reserve requirement is 1716 MW

The minimum capacity reserve available is 1281 MW

Manager NEM Real Time Operations

https://www.aemo.com.au/market-notices?

Reasons?

Eraring EO1 (usually 700 MW) had already gone off-line on 5th August. So the available capacity was:

Bayswater 4×660=2,640 MW

Eraring 3×700=2,100 MW

Mt Piper 2 units 1,430 MW

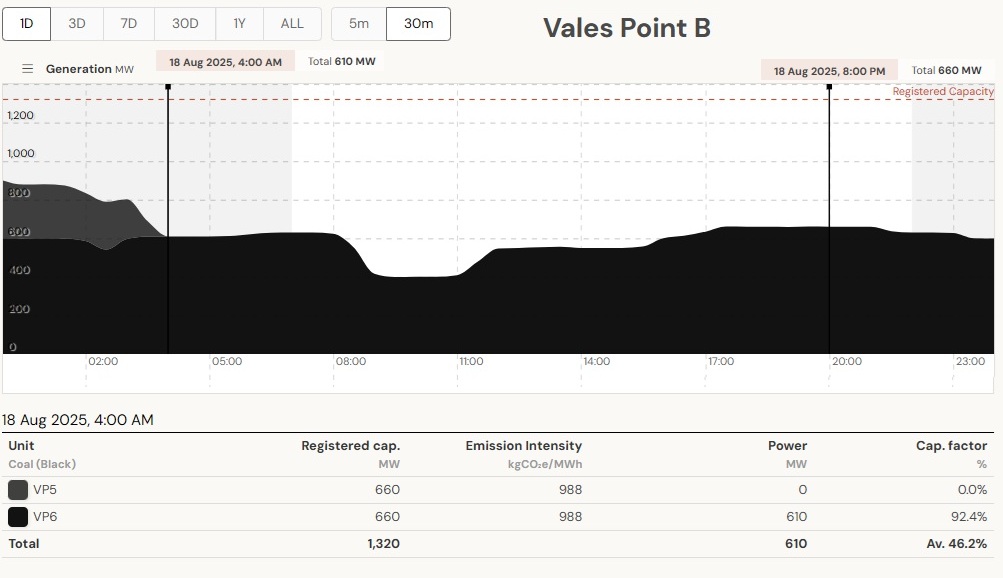

Vales Point VP6 660 MW

Total 4 plants 6,830 MW

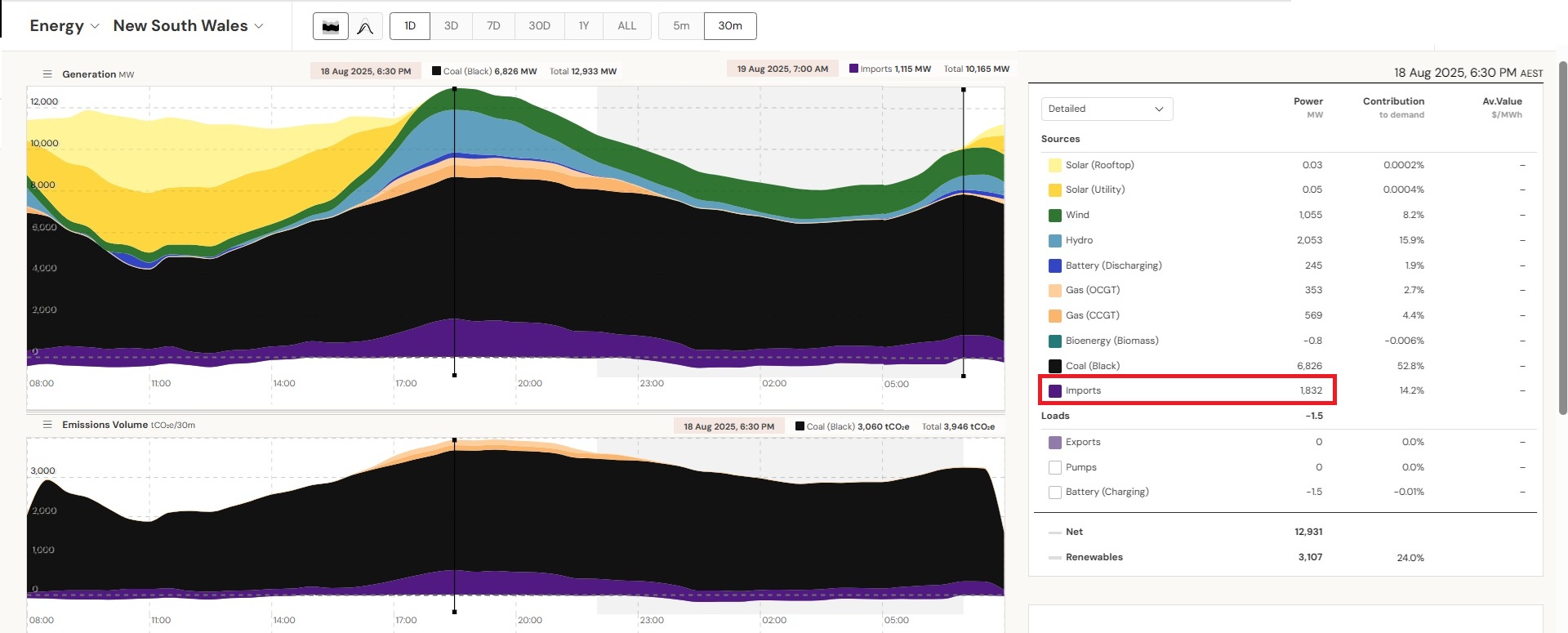

Fig 2: NSW power generation 18/19 Aug. Available coal maxed out at 6,826 MW

High imports of 1,832 MW at 6:30 pm, much of which from Queensland where power supplies were also tight (battery discharge 491 MW)

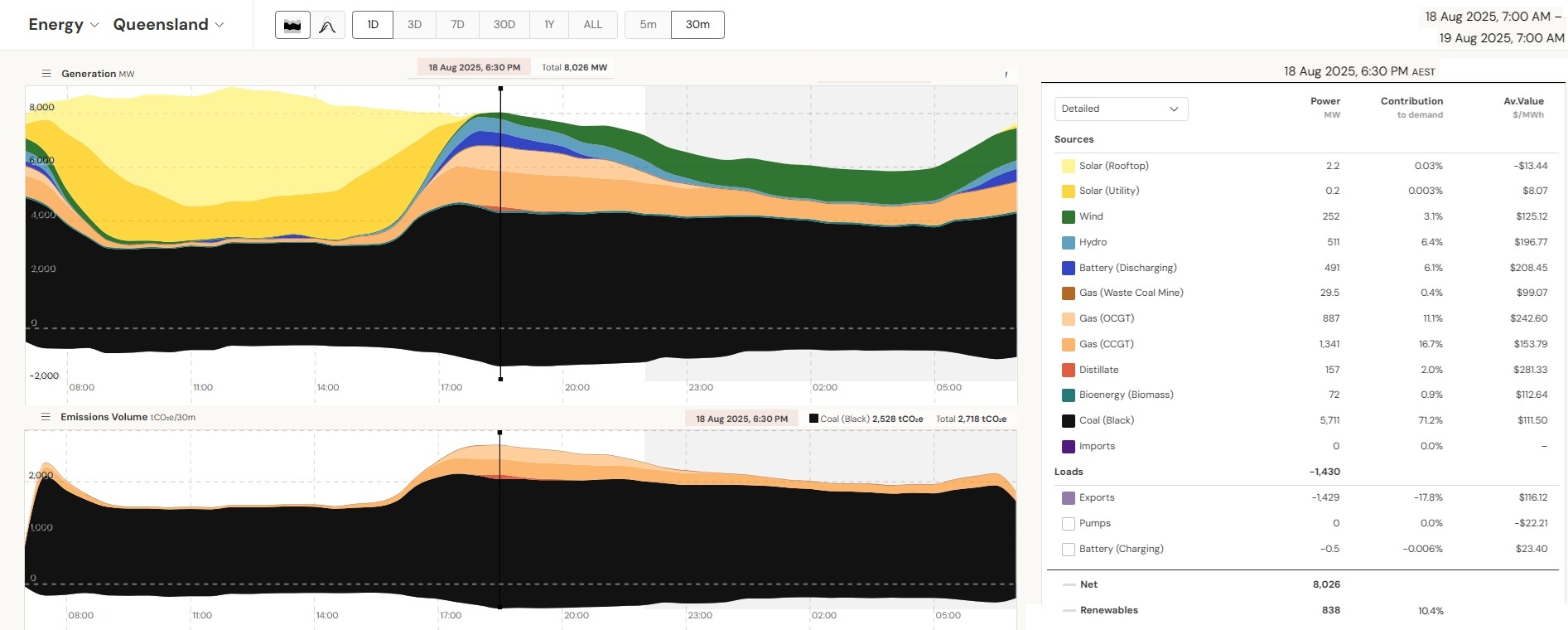

Fig 3: Queensland power generation, even diesel used for 157 MW, and power exports 1,429 MW to NSW

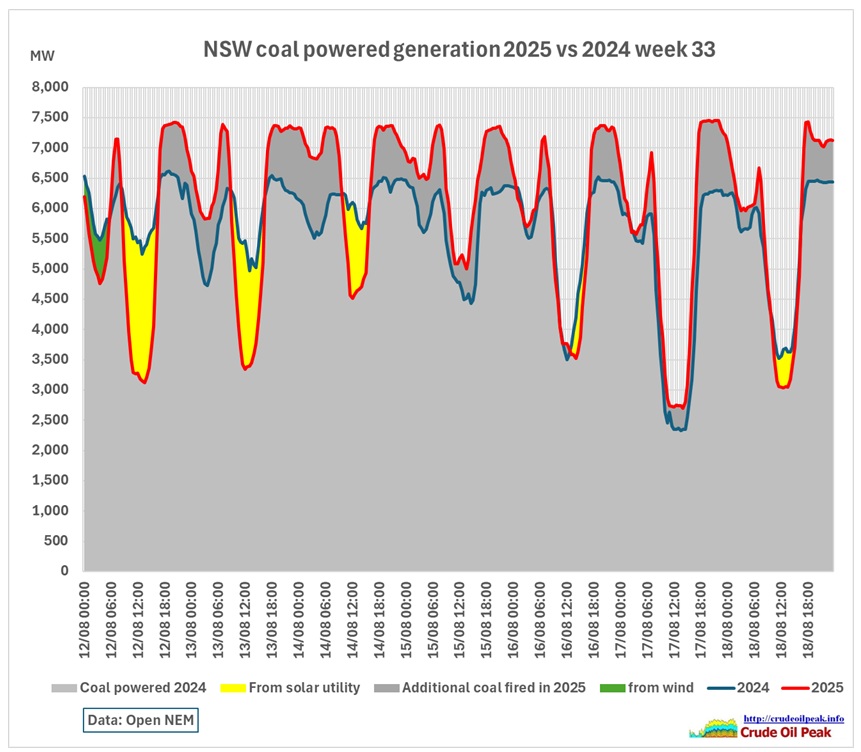

In week 33, coal fired power in 2025 was around 800 MW higher than in 2024.

Fig 4: The dark grey areas are higher coal fired power generation in 2025

Fig 4: The dark grey areas are higher coal fired power generation in 2025

The periods of lower coal fired power in 2025 during daytime can be seen to come from solar utility.

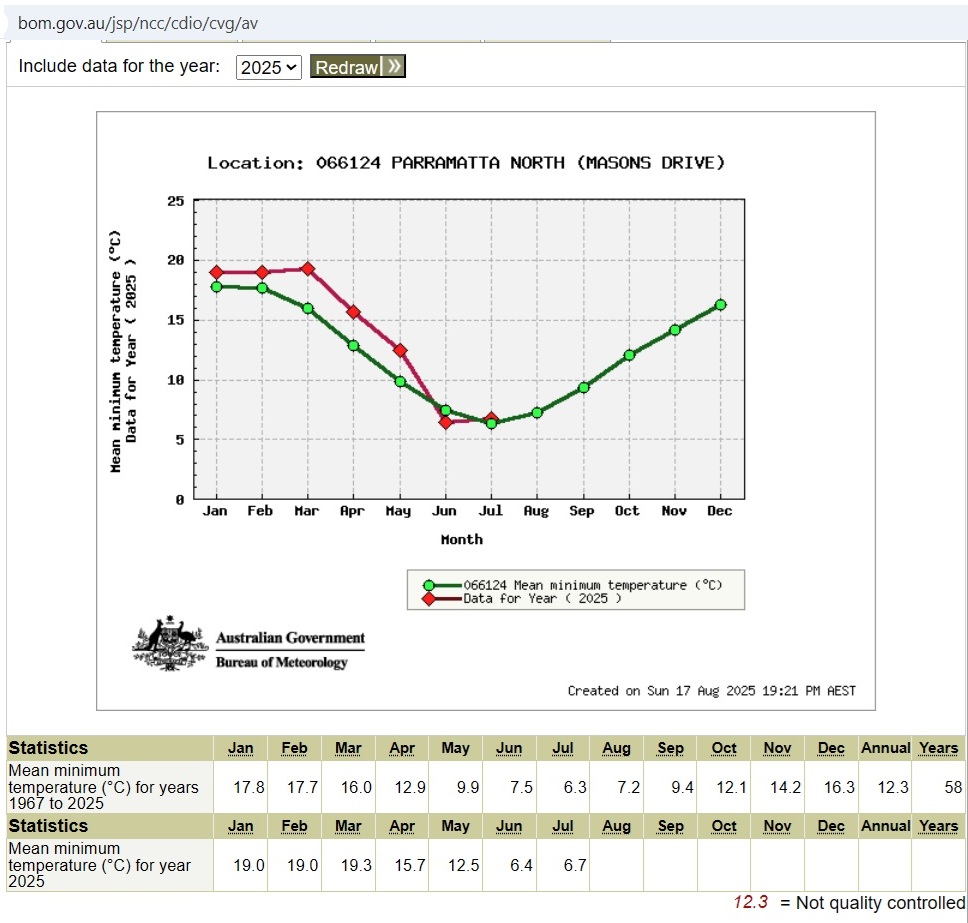

What could be the reasons for this? Was it colder than last year?

Fig 5: Temperatures in Parramatta

Fig 5: Temperatures in Parramatta

June 2025 was a bit cooler than the mean, July 2025 a touch warmer, while August data have yet to be published. Not a record cold winter as it seems.

Let’s look at what is said on energy and productivity:

19 Aug 2025

Fig 5: Woodside boss Meg O’Neill says East Coast should follow WA’s lead in gas reservation policy The Business https://www.youtube.com/watch?v=wHCDk2v6SpY

Here is an extract from that interview:

Alicia: “Manufacturers like Blue Scope say soaring energy prices in Australia are prohibitive to doing business here. Does Woodside recognize that as a problem?”

Meg: “Oh, absolutely. In fact in our submission to the economic productivity round table we were very clear that the key to Australia’s prosperity historically has been affordable, reliable energy. Australia’s industry was built on the back of really cheap coal and very affordable natural gas. We are very committed to doing our part to ensure that the domestic market is well supplied. But we need to make sure that we’re getting all the red and green tape and the lawfare out of the way that’s impeding development today.”

Alicia: “Your industry recently indicated support for a gas reservation policy in the face of East Coast gas shortages. Do you think it will happen?”

Meg: “I do. I think there’s a growing realization that we need to have some mechanisms in place to ensure that gas is provided to the domestic customers. I think folks, you know, in the east coast look over to Western Australia and see a domestic market reservation policy that has served the domestic market very well. If you look in our results you’d see that the prices we get in WA are about half of what we get in the East Coast market. So there’s, I think, a great understanding that what works in WA could well work in the East Coast if we have all the regulatory setting correct.”

Alicia: “Is it entirely up to the government? Should Australian consumers and businesses have first access to the gas produced here before having to buy it back at higher international prices?”

Meg: “I think it’s important to recognize and maybe I’ll speak to the West Coast market predominantly. You know these big gas fields would not have been developed if the gas could not be exported as LNG. The gas field that we developed, Northwest Shelf, at the point in time when we developed it, there was no domestic gas market. The government took a lot of risk underpinning the Dampier to Bunbury pipeline. They basically built a pipeline from the far northwest corner of the state down to Perth to enable industry to buy gas off that pipeline. All of that has worked very well together but we wouldn’t have been able to invest in those fields if it was only for the domestic market. You got to recognize that the LNG investment in many ways unlocks the potential to develop more domestic gas resources.”

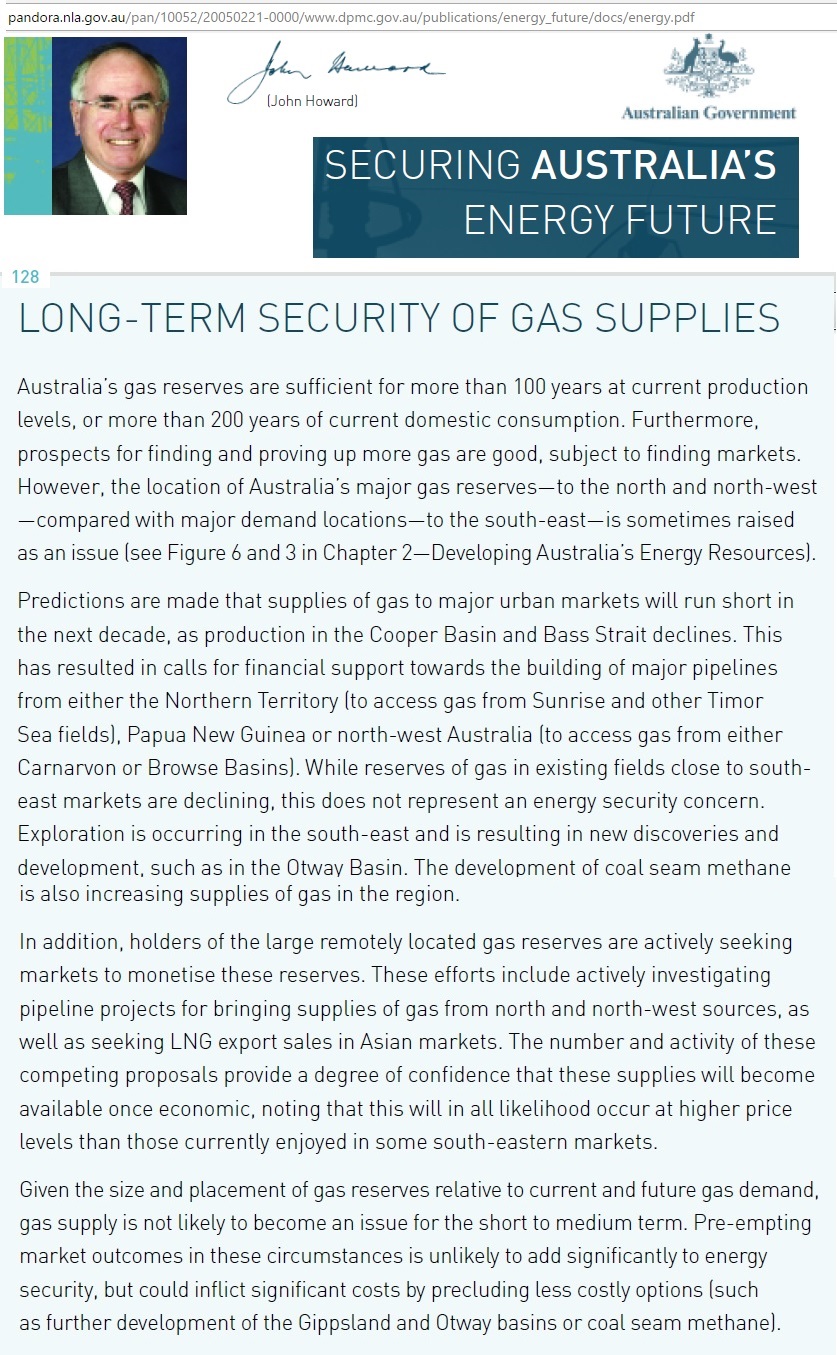

We have to stop it here. Good effort by Alicia. But Meg’s arguments are the same as those in then Prime Minister John Howard’s fundamentally flawed Energy White Paper of 2004:

Howard:

“Australia’s gas reserves are sufficient for more than 100 years at current production levels,

or more than 200 years of current domestic consumption”

“Predictions are made that supplies of gas to major urban markets will run short in the next

decade, as production in the Cooper Basin and Bass Strait declines. This has resulted in calls

for financial support towards the building of major pipelines from either the Northern

Territory (to access gas from Sunrise and other Timor Sea fields), Papua New Guinea or

north-west Australia (to access gas from either Carnarvon or Browse Basins). While reserves

of gas in existing fields close to southeast markets are declining, this does not represent an

energy security concern. Exploration is occurring in the south-east and is resulting in new

discoveries and development, such as in the Otway Basin. The development of coal seam

methane is also increasing supplies of gas in the region.”

“In addition, holders of the large remotely located gas reserves are actively seeking markets

to monetise these reserves. These efforts include actively investigating pipeline projects for

bringing supplies of gas from north and north-west sources, as well as seeking LNG export

sales in Asian markets. The number and activity of these competing proposals provide a

degree of confidence that these supplies will become available once economic, noting that

this will in all likelihood occur at higher price levels than those currently enjoyed in some

south-eastern markets.”

If you cannot believe it, here is a screen shot from the 2004 energy white paper.

Fig 6: From John Howard’s Energy White Paper 2004

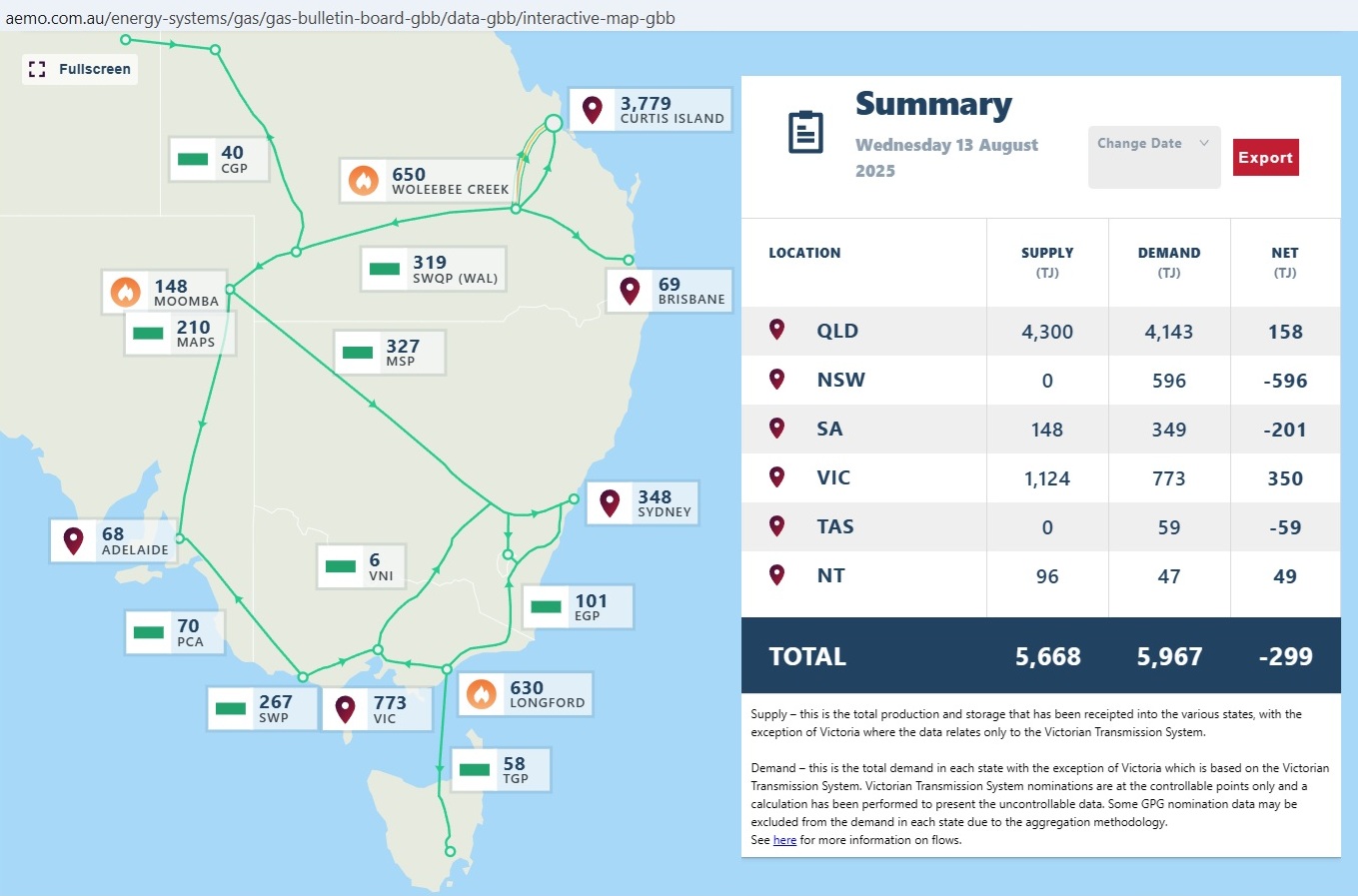

This wrong assessment (very likely drafted by the gas industry) is the root cause for the east coast gas crisis. Will the current government muster the strength to limit LNG exports from Gladstone? The following graph shows the gas flows on the east coast:

Fig 7: East coast gas flows in August 2025

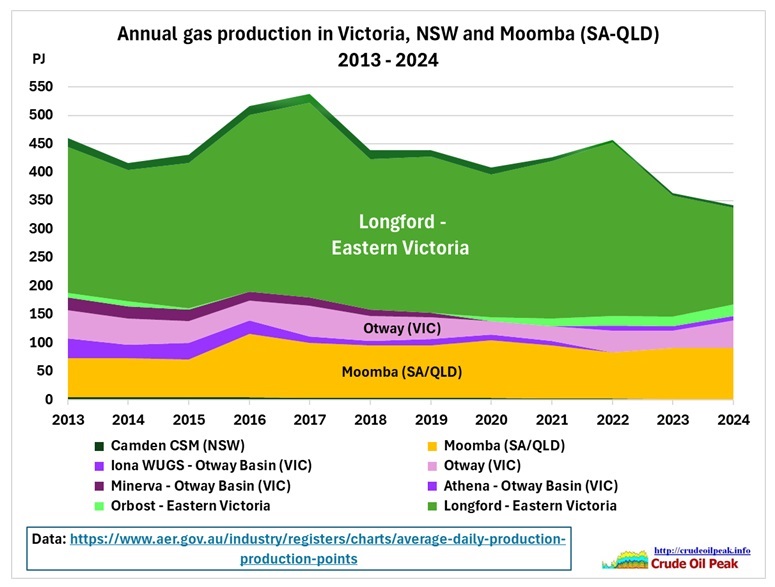

6.3x of NSW consumption is wasted in LNG exports from Curtis island (Gladstone). While conventional gas production is in decline:

Fig 7: Conventional gas production in Victoria

20 Aug 2025

The 2nd day was dominated by Australia’s housing crisis. The Australian government stubbornly ignores/denies the negative impact of immigration on the availability and cost of housing. The situation is so desperate that the development of construction standards is tinkered with:

Pause on construction rules could come soon

After warnings from Housing Minister Clare O’Neil that red tape was dragging down housing approvals — and leaked Treasury documents indicating the government was considering a pause on the National Construction Code — attendees also agreed such a move should take place.

The National Construction Code lays out minimum requirements for buildings on everything from fire exits and accessibility to insulation and capacity for electric vehicle chargers.

But while the room agreed changes to safety standards should continue, attendees discussed possible pauses on “non-essential” rules of the construction code, such as new requirements to lift energy efficiency standards.

New South Wales Treasurer Daniel Mookhey said a pause on the code was needed, though the finer details were being worked through.

https://www.abc.net.au/news/2025-08-20/productivity-summit-super-funds-housing-construction-code-epbc/105678536

Housing approvals for the

National Housing Accord

The Accord includes an initial aspirational target agreed by all parties to build one million new well‑located homes over 5 years from mid‑2024. The Commonwealth and states and territories agreed to update this target at National Cabinet in August 2023 to 1.2 million new well‑located homes over 5 years from mid‑2024

https://treasury.gov.au/policy-topics/housing/accord

On 14 May 2024, the Australian Government announced that the planning levels for the 2024–25 permanent Migration Program (Migration Program) will be set at 185,000 places.

https://immi.homeaffairs.gov.au/what-we-do/migration-program-planning-levels

Over 5 years that would be 925k.

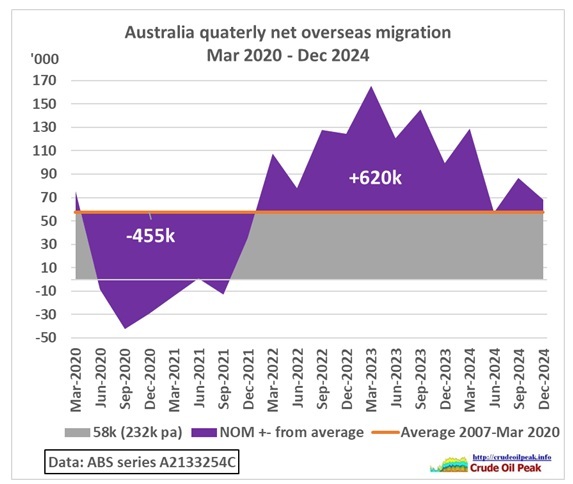

Let’s have a look at actual NOM statistics:

Fig 8: NOM balance through the Wuhan virus crisis and “catch-up” recovery period

We can see that the NOM loss (-455k) has already been overcompensated (+620k) as of December 2024.

Related posts:

16 Aug 2025

Sydney’s wintry midnight electrification 12-13th August 2025, based on coal

https://crudeoilpeak.info/sydneys-wintery-midnight-electrification-12-13-august-2025-based-on-coal

3 Aug 2025

Premier NSW energy guzzler in winter: coal plants running at 90 % capacity during critical evening periods

https://crudeoilpeak.info/premier-nsw-energy-guzzler-in-winter-coal-plants-running-at-90-capacity-during-critical-evening-periods