West of the Shetland Islands, the battle against oil decline is over for BP. SPGlobal reports:

BP halts production at oldest West of Shetland oil facility Foinaven on asset decline

15 Apr 2021

London — BP has halted production at its oldest West of Shetland oil facility, Foinaven, citing the age of the facility [Petrojarl] and operational challenges, as several BP facilities in the region suffer output setbacks.

Fig 1: FPSO (Floating Production Storage Offloading) Petrojarl Foinhaven, 250 m long, 280 kb storage

Fig 1: FPSO (Floating Production Storage Offloading) Petrojarl Foinhaven, 250 m long, 280 kb storage

https://www.teekay.com/petrojarl-foinaven/

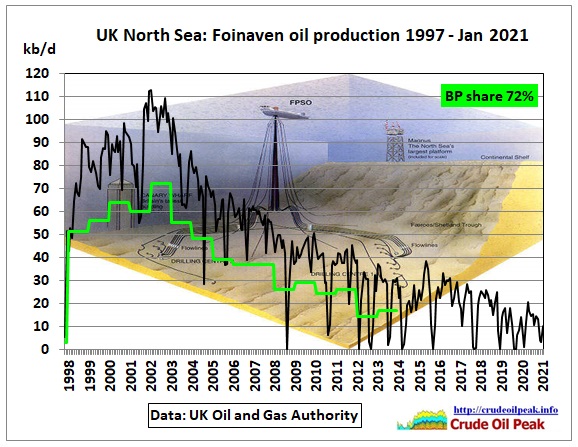

Production from the deepwater field dropped sharply again last year, to 12,000 b/d, far off its 2002 peak of 113,000 b/d.

BP said the field could still contain up to 200 million barrels of resources, which could still be extracted with further investment in alternative facilities, but the current facilities were no longer viable.

“Work had been underway to consider options to extend the life of the vessel out to 2025,” BP said. “However, it has now been concluded that, due to its age and the demands of operating West of Shetland, even with material further investment the Petrojarl Foinaven is not the right vehicle to recover the remaining resources from the Foinaven fields.”

https://www.spglobal.com/platts/en/market-insights/latest-news/oil/041521-bp-halts-production-at-oldest-west-of-shetland-oil-facility-foinaven-on-asset-decline

Let’s have a look at the Foinhaven production, using data from the UK Oil and Gas Authority (OGA):

Fig 2: Foinhaven oil production history

Fig 2: Foinhaven oil production history

Underlying image: https://www.offshore-technology.com/projects/foinaven/

Off the continental shelf at 400-600 m water depth

Using above OGA data, 393 mb have been produced until January 2021. In BP’s 1998 Form 20-F, Foinhaven’s BP share of reserves(72%) were given as 193 mb, i.e. a total of 268 mb. That oil was extracted by 2007 when production had dropped to half its peak. The reserve growth was therefore 125 mb, but at a much lower and still declining production level.

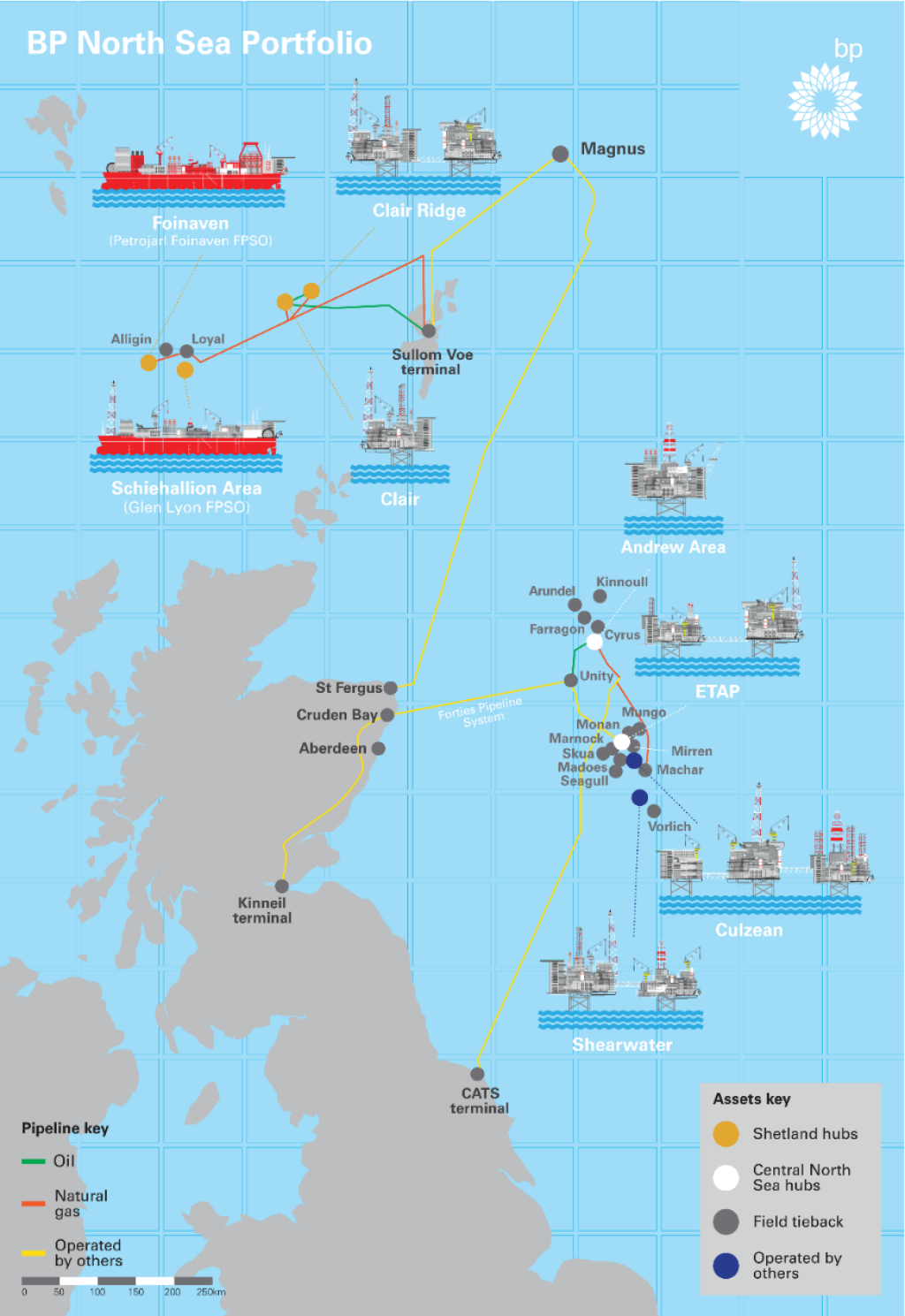

Foinhaven is located 190 kms west of the Shetland Islands as shown on this map:

Fig 3: BP’s oil fields, production platforms and floating storage ships

Fig 3: BP’s oil fields, production platforms and floating storage ships

https://www.bp.com/en_gb/united-kingdom/home/where-we-operate/north-sea/north-sea-portfolio.html

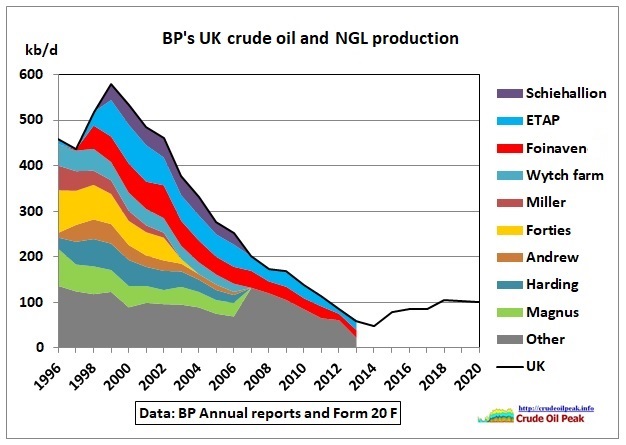

What happened to all the other fields on this map? We use data from BP’s annual reports and Form 20-F submissions.

Fig 4: BP’s UK oil production peaked in 1999

Fig 4: BP’s UK oil production peaked in 1999

Note that field-by-field production data have been merged into the “other” category in 2007 and ended completely in 2013. We’ll use data from the UK Oil and Gas Authority to look at details, fill in the blanks and see where that uptick in production comes from.

(A) Fields sold

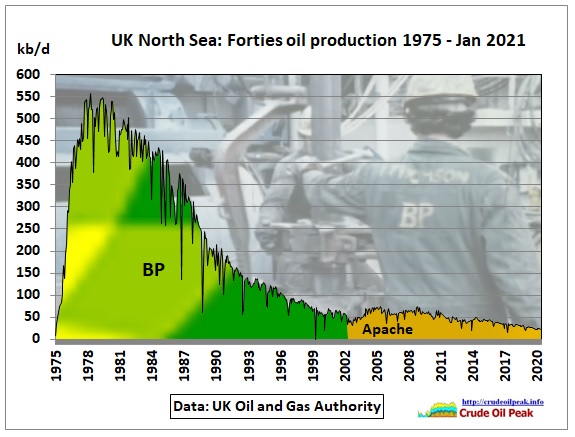

The most famous oil field in Fig 4 is Forties.

Fig 5: Forties oil production (cumulative 2,800 mb)

Fig 5: Forties oil production (cumulative 2,800 mb)

Forties was sold to Apache in 2003

https://www.offshore-technology.com/projects/forties-oilfield-a-timeline/

BP sold Forties North Sea pipeline to Ineos in 2017

Energy giant Ineos has struck a deal to acquire the Forties Pipeline System in the North Sea from BP for US$250m (£199m).

The pipeline transports about 450,000 barrels of oil per day on average – about 40% of UK production.

https://www.bbc.com/news/uk-scotland-scotland-business-39476674

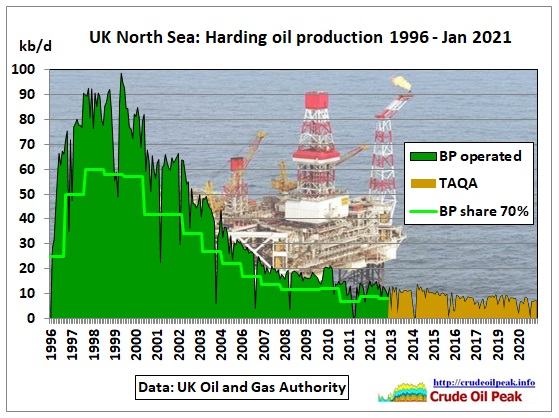

Harding was sold to TAQA in 2013

Fig 6: Harding oil production (cumulative 283 mb)

Fig 6: Harding oil production (cumulative 283 mb)

Fig 7: Location of Bruce, Harding, Miller fields

Fig 7: Location of Bruce, Harding, Miller fields

https://www.oedigital.com/news/445140-bp-sells-bruce-rhum-keith-stakes

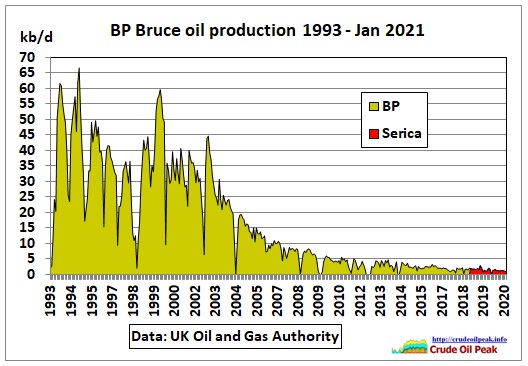

Bruce was sold to Serica Energy in 2017

Fig 8: Bruce oil production (cumulative 166 mb). Of which BP share 37%

Fig 8: Bruce oil production (cumulative 166 mb). Of which BP share 37%

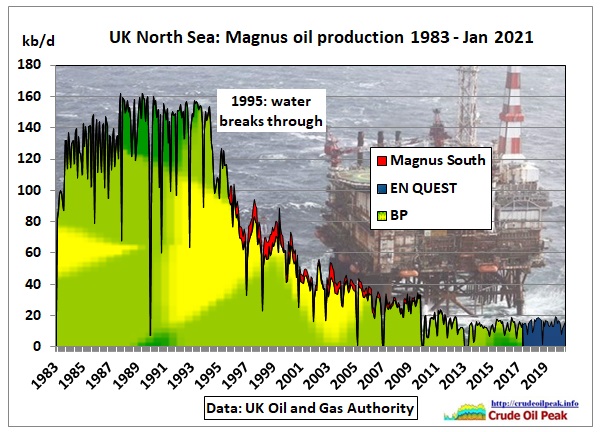

Magnus was sold to Enquest in 2017

Fig 9 : Magnus oil production. BP share 85%

Fig 9 : Magnus oil production. BP share 85%

Cumulative production by Jan 2021 was 884 mb or 145 million m3. Jean Laherrre did a trend analysis in 2008 with an estimate of something between 140 and 150 million m3, quite close.

http://aspofrance.viabloga.com/files/JL-IGC2008-part2.pdf

Daily production is now only 1/10 of peak production.

BP to sell part of interests in Magnus field and Sullom Voe terminal in UK North Sea to EnQuest

24 Jan 2017

Included in the agreement are: 25% of BP’s 100% stake in Magnus, 25% of BP’s interests in a number of associated pipelines and a 3% interest in the Sullom Voe Terminal from BP Exploration Operating Company Limited’s (BPEOC) current total 12% stake. The sale price of $85 million is expected to be met by EnQuest from the sharing of future cash flows from the assets and the agreement will not include any upfront payment to BP.

https://www.bp.com/en_gb/united-kingdom/home/news/press-releases/bp-to-sell-part-interests-magnus-field-and-sullom-voe-to-enquest.html

BP annual report 2018

In October EnQuest notified BP that it would exercise its option to acquire the remaining 75% of BP’s stake in the Magnus field and associated infrastructure

Disposals in upstream sector

Losses included $335 million resulting from the disposal of our interest in the Magnus field and associated assets in the UK North Sea

https://www.bp.com/content/dam/bp/business-sites/en/global/corporate/pdfs/investors/bp-annual-report-and-form-20f-2018.pdf

(B) Fields for sale

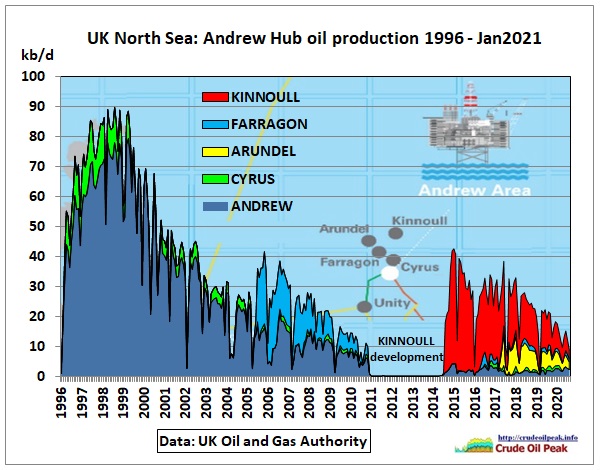

Fig 10: Andrew hub oil production (shut down May 2011 to allow Kinnoull tie-back)

Fig 10: Andrew hub oil production (shut down May 2011 to allow Kinnoull tie-back)

Cumulative production and BP share: Andrew (170 mb, 62.75%), Cyrus (22 mb, 100%), Arundel (8 mb, 100%), Farragon (22 mb, 67%), Kinnoull (39 mb, 62.75%)

Geological details: https://www.spe-aberdeen.org/wp-content/uploads/2018/05/Arundel-Field-Central-North-Sea-A-Single-Well-Development-on-a-Complex-Small-Field-Rory-Leslie.pdf

(The Unity platform shown above is part of the Forties pipeline which was sold in 2017 to Ineos)

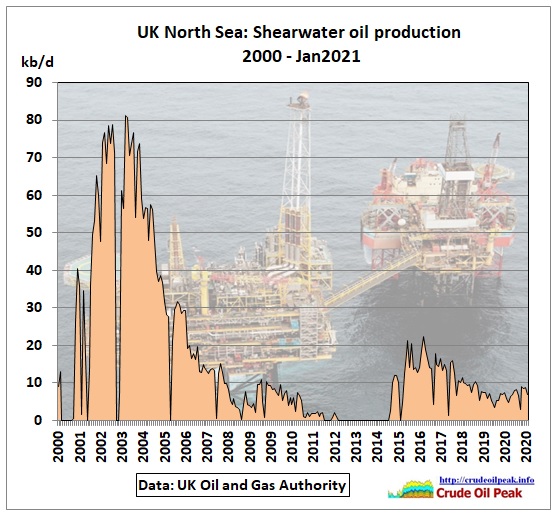

Fig 11: Shearwater oil production (cumulative 120 mb, BP 27.5%)

Fig 11: Shearwater oil production (cumulative 120 mb, BP 27.5%)

The Shell-operated Shearwater field (BP ownership share 28%) is a high-pressure, high-temperature gas condensate field located in the Central North Sea. Shearwater was brought online in 2000 and has been developed through two fixed platforms. Shearwater remains among the biggest producing fields in the North Sea and is anticipated to continue operating into the 2020s.

https://www.bp.com/en_gb/united-kingdom/home/where-we-operate/north-sea/north-sea-portfolio.html

Andrew and Shearwater are now up for sale. The following articles describe how difficult it is to sell mature North Sea assets.

June 2019

BP relaunches Shearwater oilfield sale after Shell talks end – sources

BP is again seeking buyers for its stake in the Shearwater oilfield in the British North Sea after talks with Royal Dutch Shell fell through, industry and banking sources said. https://www.reuters.com/article/bp-shearwater-idUSL8N23E229

June 2020

BP sweetens North Sea assets sale after oil price slump

Oil giant BP has agreed to heavily discount the price of North Sea assets it is planning to sell to Premier Oil

The two companies reached a deal in January which would have seen Premier pay $625m (494m) for BP’s interests in the Shearwater and Andrew fields.

https://www.bbc.com/news/uk-scotland-scotland-business-52936223

Oct 2020

Premier Oil, BP North Sea Deal Falls Through

Premier Oil abandoned its plans to buy North Sea fields from BP for $210 million after Premier was taken over by rival Chrysaor, marking a small dent in BP’s $25 billion disposals target.

https://www.oedigital.com/news/482200-premier-oil-bp-north-sea-deal-falls-through

Jan 2021

BP Relaunches Sale of Stakes in North Sea Assets

According to Reuters, it is unclear how much BP could raise from the sale of these assets in the aging North Sea basin, but their value is unlikely to exceed $80 million following the collapse in oil prices.

https://jpt.spe.org/bp-relaunches-sale-of-stakes-in-north-sea-assets

Mar 2021

BP Is Said to Field Final Offers for North Sea Assets

Oil and gas producers Tailwind Energy Ltd., Serica Energy Plc, Ithaca Energy Ltd., EnQuest Plc and newcomer Waldorf Production U.K. Ltd. have been considering binding offers for some or all of the assets, the people said, asking not to be identified discussing confidential information.

https://www.rigzone.com/news/wire/bp_is_said_to_field_final_offers_for_nsea_assets-18-mar-2021-164921-article/

(C) Fields decommissioned

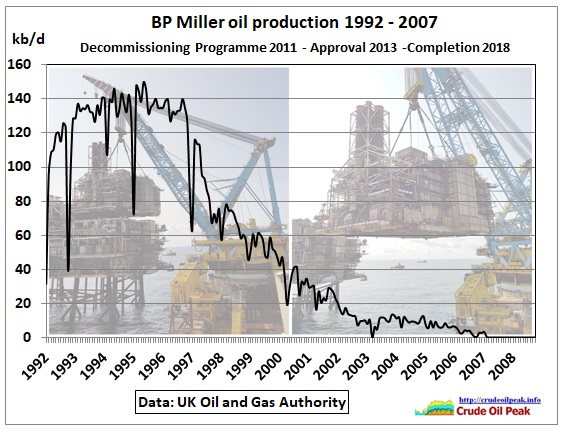

Fig 12: Miller oil production (cumulative 344 mb)

Fig 12: Miller oil production (cumulative 344 mb)

BP’s Decommissioning programme 2011

https://www.bp.com/content/dam/bp/country-sites/en_gb/united-kingdom/home/pdf/Miller_Decomm_Programme.pdf

PHOTO: Taking apart BP’s Miller platform in North Sea

Apr 2018

https://www.offshore-energy.biz/photo-taking-apart-bps-miller-platform-in-north-sea/

DECOMMISSIONING INSIGHT 2018

https://oilandgasuk.co.uk/wp-content/uploads/2019/03/OGUK-Decommissioning-Insight-Report-2018.pdf

Conclusion:

That’s all history. But it shows us what happens after peak oil, a glimpse into the future of many other offshore fields around the world which have to produce at high rates to survive a harsh, corrosive environment.

To be continued: BP’s remaining fields in operation and still producing, reserve growth analysis