In part 1 we were looking at BP’s oil field sold (A), for sale (B) or decommissioned (C).That was a sobering experience. In part 2 we analyse fields which are still in production for BP.

(D) Fields still producing for BP

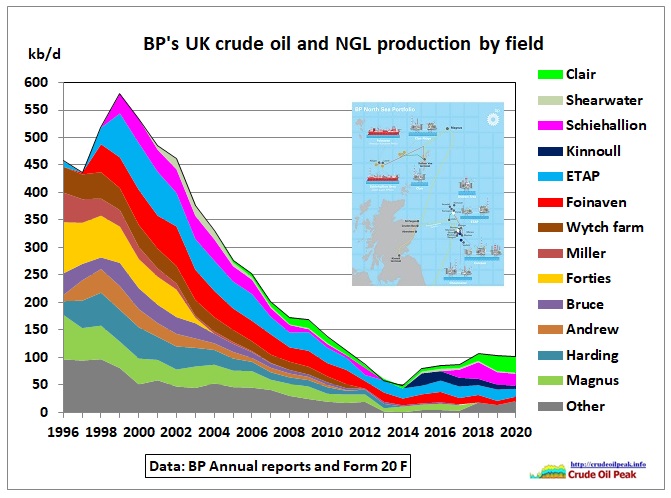

Clair and Clair Ridge

Fig 13: Fig Clair and Clair Ridge are producing into the Sullom Voe Terminal on the Shetland Islands

Fig 13: Fig Clair and Clair Ridge are producing into the Sullom Voe Terminal on the Shetland Islands

Clair has a long history

It was discovered in 1977 but a paper for Petroleum Geology Conference Series in 1993 reported that although the oil in place was measurable in billions of barrels “the success of the discovery well was never repeated and commercial test production rates were never achieved” https://pgc.lyellcollection.org/content/4/1/1409

August 2004

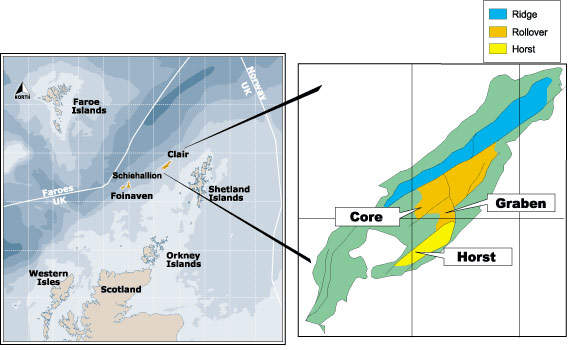

Clair Phase 1 is targeting 250-300 MMbbl in the Core, Graben, and Horst segments. The area to be covered is laterally extensive and will be drained via high step-out, extended-reach wells. Hughes describes these as “middle of the park technology for BP – we certainly drill tougher wells elsewhere in the world.” Most of the wells will be around 3 km long, but two will extend 6 km into the Horst region, with a further three extending to 5 km.

https://www.offshore-mag.com/business-briefs/equipment-engineering/article/16756978/clair-development-reflects-fasttrack-lowcost-advances

Fig 14: Location of Clair and segments

Fig 14: Location of Clair and segments

https://www.offshore-technology.com/projects/clair/

BP inaugurates Clair

Feb 2005

Tony Hayward, BP’s chief executive, exploration and production, and Mike O’Brien, Minister of State for energy and e-Commerce, officially inaugurated the BP-operated Clair oilfield.

“With an estimated 5 Bbbl of oil in place in Clair, this is very much the start of the journey. Providing that a stable business and fiscal environment remains, we believe this first phase of production will allow us to unlock more of the Clair reservoir,” Hayward says

The first part of the field development will access recoverable reserves of 250 MMbbl of oil, with plateau production expected to reach 60,000 b/d of oil and 15 MMcf/d of gas.

https://www.offshore-mag.com/home/article/16764774/bp-inaugurates-clair

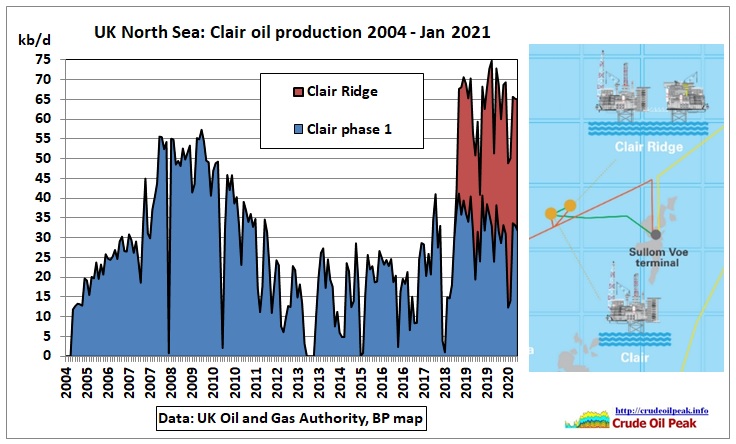

So recoverable reserves would be 250/5,000 = 5%., a very low recovery rate. When the Clair field peaked in 2008-2009 at 50 kb/d the plateau did not last long while just 60 mb had been produced ( 24% of the expected reserves). Conceptual engineering studies for the next phase Clair Ridge were done by AMEC in that year.

https://www.nsenergybusiness.com/projects/clair-ridge-development-project-north-sea/

Cumulative production for Clair was 180 mb by Jan 2021. BP had a share of 28.6 % but increased it to 45.1% in 2018

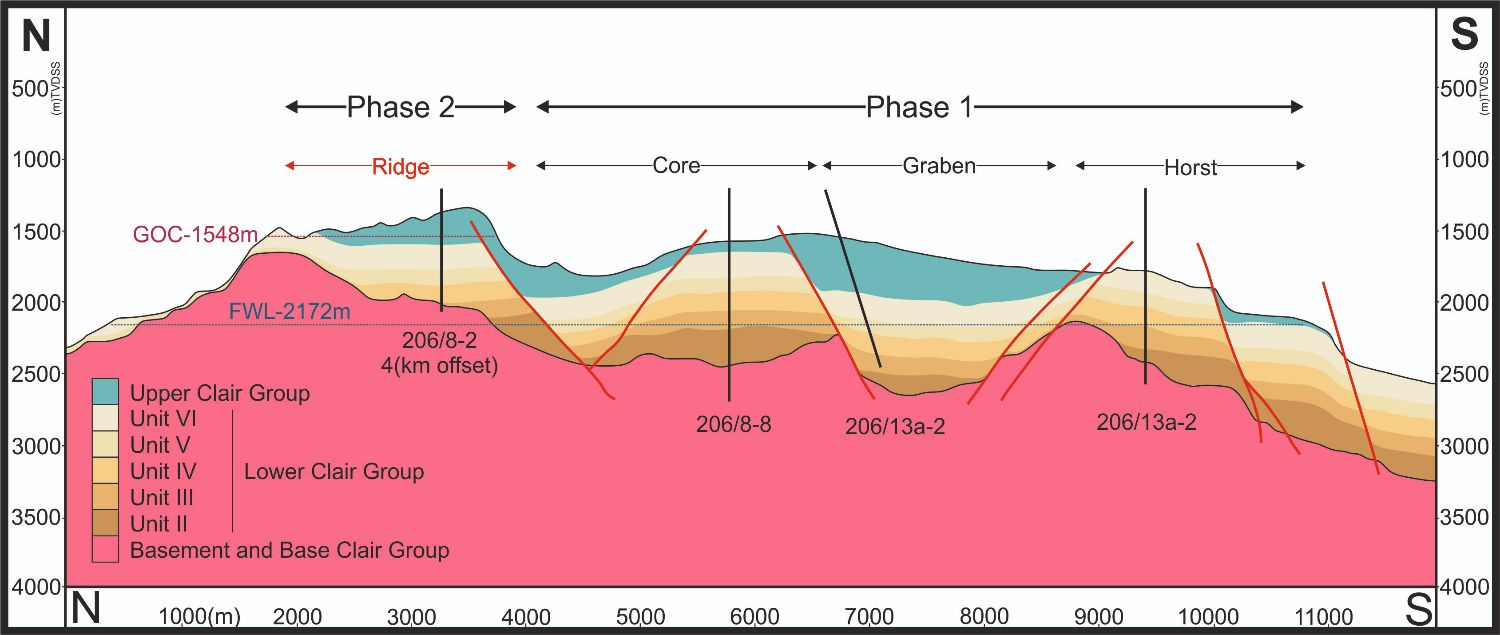

Fig 15: Clair field geologic profile

Fig 15: Clair field geologic profile

https://www.arcgis.com/apps/MapJournal/index.html?appid=915ac37815784c5192d63020591d00be

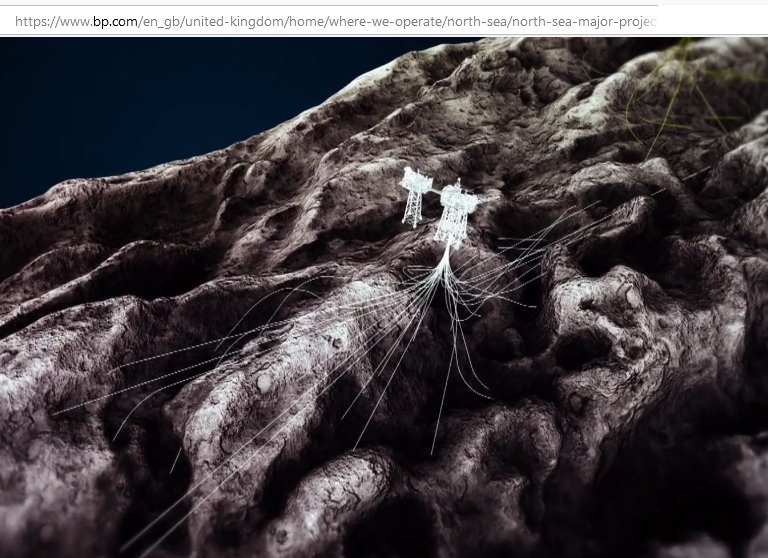

Fig 16: Extended reach laterals of Clair Ridge platforms

Fig 16: Extended reach laterals of Clair Ridge platforms

https://www.bp.com/en_gb/united-kingdom/home/where-we-operate/north-sea/north-sea-major-projects/clair-ridge.html

BP starts-up Clair Ridge production

23 November 2018

First offshore deployment of BP’s ground-breaking LoSal® enhanced oil recovery technology.

Clair Ridge is the second phase of development of the Clair field, 75 kilometres west of Shetland. The field, which was discovered in 1977, has an estimated seven billion barrels of hydrocarbons.

The new facilities, which required capital investment in excess of £4.5 billion, are designed for 40 years of production. The project has been designed to recover an estimated 640 million barrels of oil with production expected to ramp up to a peak at plateau level of 120,000 barrels of oil per day.

Bernard Looney, BP Chief Executive Upstream, said: “The start-up of Clair Ridge is a culmination of decades of persistence. Clair was the first discovery we made in the West of Shetland area in 1977. But trying to access and produce its seven billion barrels proved very difficult. We had to leverage our technology and ingenuity to successfully bring on the first phase of this development in 2005.

“And now more than 40 years after the original discovery, we have first oil from Clair Ridge, one of the largest recent investments in the UK. This is a major milestone for our Upstream business and highlights BP’s continued commitment to the North Sea region.”

https://www.bp.com/en/global/corporate/news-and-insights/press-releases/bp-starts-up-clair-ridge-production.html

The maximum production so far was 41 kb/d in February 2020 and cumulative production over 2 years was 25 mb by Jan 2021. There is a long way to go.

BP to pause Clair South project

May 2020

Progress on the third phase of the Clair oil field to the west of Shetland has been put on hold due to the coronavirus pandemic.

The Clair South project, led by BP, has been postponed until 2022.

https://www.ogv.energy/news-item/bp-to-pause-clair-south-project

Fig 17: Sullom Voe Terminal on the Shetland Islands

Fig 17: Sullom Voe Terminal on the Shetland Islands

SP Global reports:

BP’s flagship UK oil fields hit by production setbacks: partner

18 Mar 2021

London — BP’s flagship Clair and Schiehallion oil fields in the UK West of Shetland area have both been performing below expectations, with remedial measures such as new drilling expected to take time to implement, minority stakeholder Chrysaor (7.5% in Clair, 10% in Schiehallion) said in a March 18 statement.

Schiehallion and Clair, located in a harsh maritime environment in the eastern Atlantic, have both undergone multi-billion dollar upgrades in the last decade, with new production facilities installed in 2017 and 2018 respectively. BP has described the region as its main focus in terms of UK growth prospects, rather than the conventional North Sea.

The fields produce heavy crude, rather than light sweet grades such as Brent and Forties that contribute to the Dated Brent benchmark, with Clair crude loaded at Sullom Voe in the Shetland Islands and Schiehallion crude shipped directly to Rotterdam for processing.

BP has previously stressed that Clair, with some 7 billion of reserves, should be seen as a multi-decade project, with oil accumulations spread over a large area and requiring multiple phases of development.

BP has described the North Sea region as a core to its upstream oil and gas business even as it expects to reduce its production globally by 40% by 2030.

https://www.spglobal.com/platts/en/market-insights/latest-news/oil/031821-bps-flagship-uk-oil-fields-hit-by-production-setbacks-partner

7 Gb “reserves” should read “resources” or even oil in place.

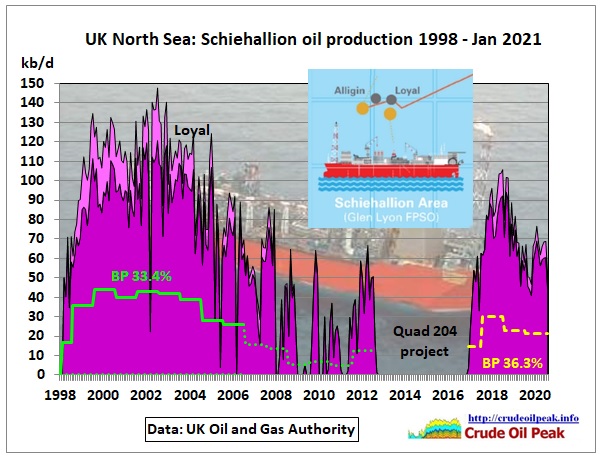

Schiehallion Area

Fig 18: Schiehallion and Loyal oil production (BP interest 33.4%, Quad 204 36.3%)

Fig 18: Schiehallion and Loyal oil production (BP interest 33.4%, Quad 204 36.3%)

OGA data show cumulative production of 380 mb by 2013, including Loyal.

From the BP website:

Quad 204 Project (45 kboe/d net = 36% of 125 kboe/d)

Schiehallion and the adjacent Loyal fields were first developed in the mid-1990s and have produced nearly 400 million barrels of oil since production started in 1998. With the fields’ redevelopment through the Quad 204 project, BP and co-venturers expect to unlock a further estimated 450 million barrels of resources, extending the life of the fields out to 2035 and beyond. Production from the project is expected to ramp up to a plateau level of 130,000 barrels equivalent per day (boe/d) in 2018.

Since the Quad 204 project was sanctioned in 2011, over £2bn of contracts have been awarded to UK companies.

Note that BP mentions further 450 mb of resources, not reserves. Between 2017 and Jan 2021, 93 mb have been produced.

The plateau of 130 kb/d was never reached. It maxed out at 80 + 11 (Loyal) = 91 kb/d. Production has gone down to 63 kb/d in 2020. Alligin produced a mere 7 kb/d. If we assume a petering out of production to 2035, that would be a total of 190 mb.

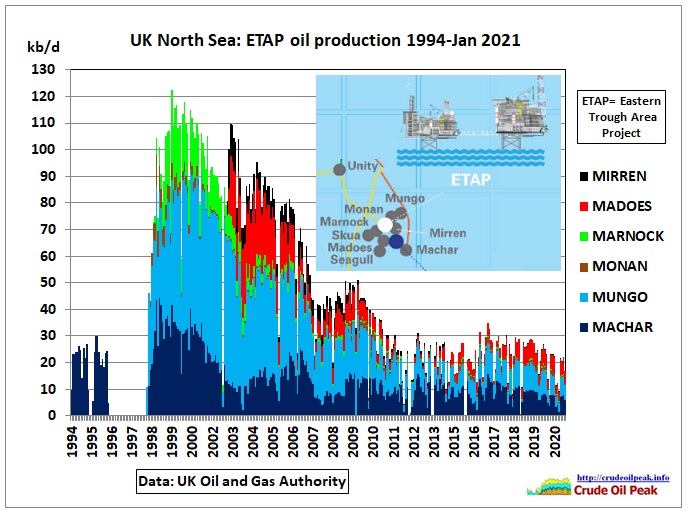

Eastern Trough Area Project (ETAP)

Fig 19: ETAP oil production history (cumulative 417 mb)

Fig 19: ETAP oil production history (cumulative 417 mb)

ETAP ranks as one of the largest and most commercially complex North Sea oil and gas developments of the past 20 years; multiple fields with varying ownership sharing a central processing facility (CPF). bp operates six of the seven ETAP fields; Machar, Madoes, Mirren, Mungo, Monan and Marnock. The non-operated Seagull field (BP ownership share 50%) will be tied back to the ETAP CPF with first production expected in 2021. We are exploring options to develop another new field, Skua, through the ETAP hub.

ETAP came on stream in July 1998 with an estimated production life of 20 years. However, a multi-million-pound investment programme in 2015 secured its future well into the 2030s.

https://www.bp.com/en_gb/united-kingdom/home/where-we-operate/north-sea/north-sea-portfolio.html

(E) Onshore

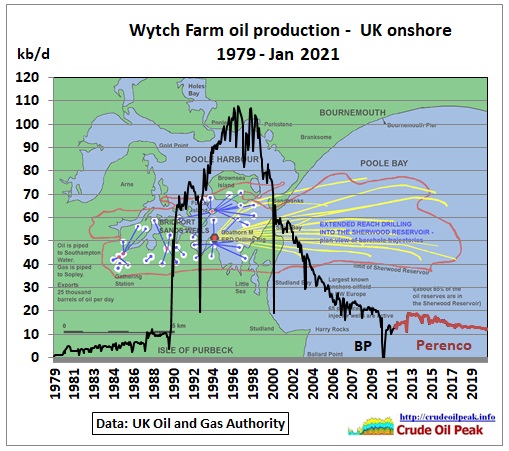

Wytch Farm (Dorset)

Fig 20 : Wytch Farm oil production (cumulative 501 mb by Jan 2021)

Fig 20 : Wytch Farm oil production (cumulative 501 mb by Jan 2021)

https://wessexcoastgeology.soton.ac.uk/Oil-South-of-England.htm

BP sold Wytch Farm in December 2011 to Perenco

https://www.bp.com/en/global/corporate/news-and-insights/press-releases/bp-agrees-sale-of-wytch-farm-to-perenco-uk-limited.html

The underlying image shows extended reach wells going offshore. In 1998, proved reserves were given as 190 mb (gross), cumulative production (mainly Sherwood reservoir) until end 2011 was 172 mb. Perenco produced 49 mb since 2012.

Altogether now

We are now able to fill the blanks in Fig 4 (part 1)

Fig 21 : The recent production increase came from Kinnoull, Schiehallion and Clair Ridge

Fig 21 : The recent production increase came from Kinnoull, Schiehallion and Clair Ridge

But this increase is only half of what BP expected in 2017

Northern highlights: reasons to be cheerful for the North Sea oil and gas business

20 April 2017

Production is set to double

BP’s production in the North Sea will more than double by 2020 to around 200,000 barrels of oil per day. Major projects will be the driver behind this, like the new Glen Lyon Floating Production Storage and Offloading (FPSO) vessel which will extend and expand recovery from the Schiehallion and Loyal oil fields located West of Shetland through to 2035.

In addition, the second-phase development of the giant Clair field, Clair Ridge is expected onstream in 2018 with production expected to hit over 100,000 barrels of oil per day at its peak.

https://www.bp.com/en/global/corporate/news-and-insights/reimagining-energy/north-sea-optimism-reasons-to-be-cheerful.html

Reserve Analysis

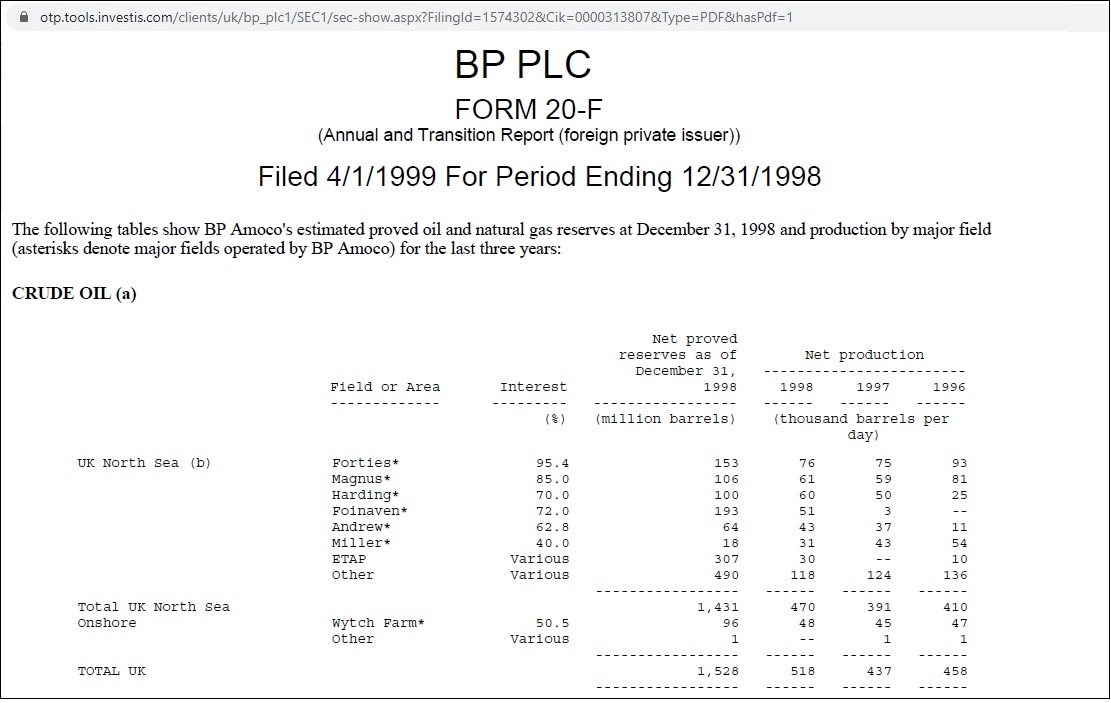

Fig 22: BP’s 1998 proved reserves

Fig 22: BP’s 1998 proved reserves

1998 was the last time BP published net proved reserves (BP share of gross reserves) by field. From then on only aggregate data were given. However, reserve Y-o-Y changes were categorized as follows:

Improved recovery

Extensions, discoveries and other additions

Revisions of previous estimates

Purchases of reserves in place

Sales of reserves in place

Production

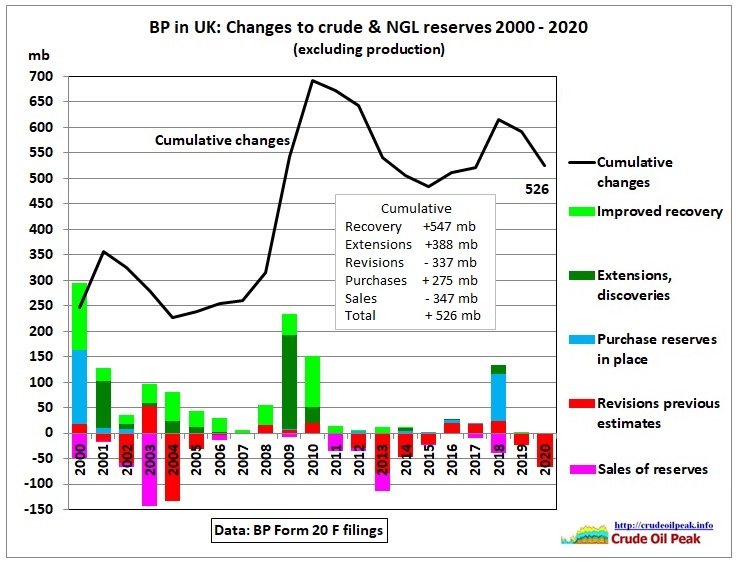

Fig 23: BP’s changes in reserves by type in UK

Fig 23: BP’s changes in reserves by type in UK

Explanation of major items:

2000

— In the UK Continental Shelf, we added almost 200 mmboe of oil and gas reserves, predominantly from improved recovery projects in Foinaven and Magnus.

2003

The sale of BP’s interest in the Forties field was completed in April 2003

2013

The major disposal transactions during 2013 were the sale of our interests in the Harding (BP 70%), Maclure (BP 37.04%), Braes (BP 27.7%), Braemar (BP 52%) and Devenick (BP 88.7%) fields in the North Sea to TAQA Bratani Ltd

2018

Purchased a 16.5% interest in the UK’s Clair field from ConocoPhillips – increasing our share to 45.1%. Disposal of BP’s interest in the Magnus field in the North Sea

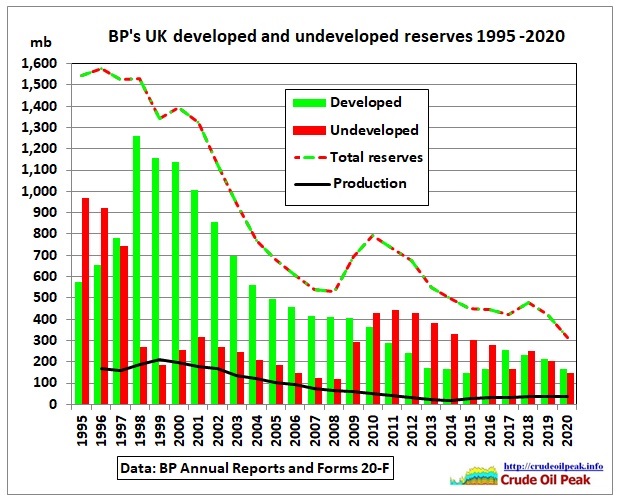

Fig 24: Developed vs undeveloped reserves

Fig 24: Developed vs undeveloped reserves

In the last 3 years the ratio of developed to undeveloped reserves was around 50/50

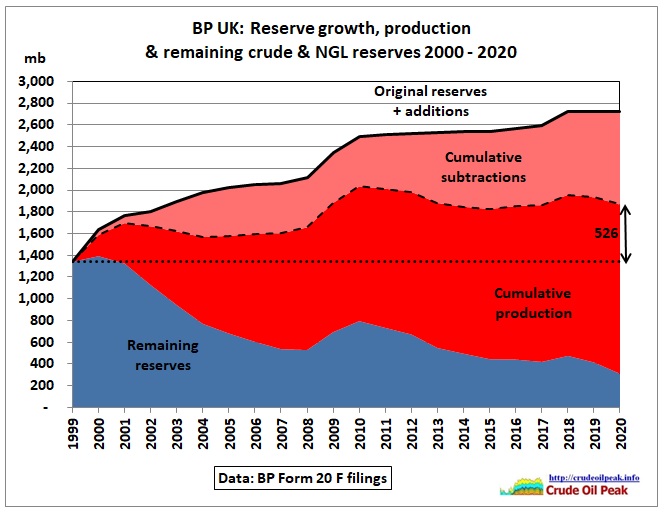

Fig 25 : Remaining reserves declined by 80% since 1999

Fig 25 : Remaining reserves declined by 80% since 1999

Additions consist of upward revisions of previous estimates, purchases of reserves in place, field extensions and discoveries plus improved recoveries.

Cumulative subtractions consist of sales of reserves and downward revisions of previous estimates.

Conclusion

BP’s production in the North Sea has stabilised at around 100 kb/d during the last 3 years. Remaining reserves have dropped considerably. The R/P ratio is currently around 8 years. The future hinges mainly on the St Clair field.

Previous post

30/4/2021

BP peak oil (UK decline, asset sales and decommissioning part 1)

https://crudeoilpeak.info/bp-peak-oil-uk-decline-asset-sales-and-decommissioning-part-1