Fig 1: Aljazeera video on truck lines October 2021. Shortages could last for months

Fig 1: Aljazeera video on truck lines October 2021. Shortages could last for months

https://www.youtube.com/watch?v=Sy_uiSlgbIA

BBC reporting:

China rations diesel amid fuel shortages

29/10/21

Petrol stations in many parts of China have begun rationing diesel amid rising costs and falling supplies.

Some truck drivers are having to wait entire days to refuel, according to posts on social media site Weibo.

China is currently in the midst of a massive power crunch, as coal and natural gas shortages have closed factories and left homes without power.

And this latest issue is only likely to contribute to an ongoing global supply chain crisis, say analysts.

“The current diesel shortages seem to be affecting long distance transportation businesses which could include goods meant for markets outside of China,” said Mattie Bekink, China Director at the Economist Intelligence Unit.

https://www.bbc.com/news/business-59059093

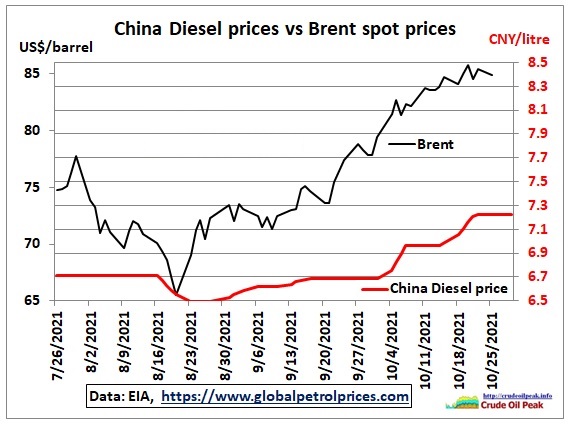

Fig 2: Comparison Chinese Diesel prices – Brent spot prices

Fig 2: Comparison Chinese Diesel prices – Brent spot prices

Images of queuing trucks are in stark contrast to what we find when googling for truck sales:

Fig 3: Line-up of new trucks for the Chinatrucks website

Fig 3: Line-up of new trucks for the Chinatrucks website

https://www.chinatrucks.com/statistics/2020/0221/article_9181.html

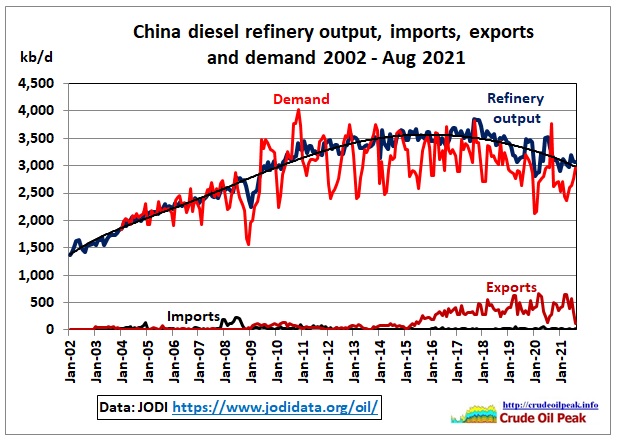

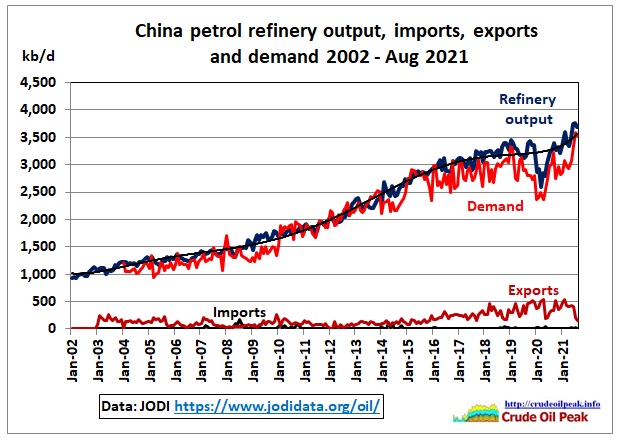

Let’s have a look at statistics from JODI https://www.jodidata.org/oil/

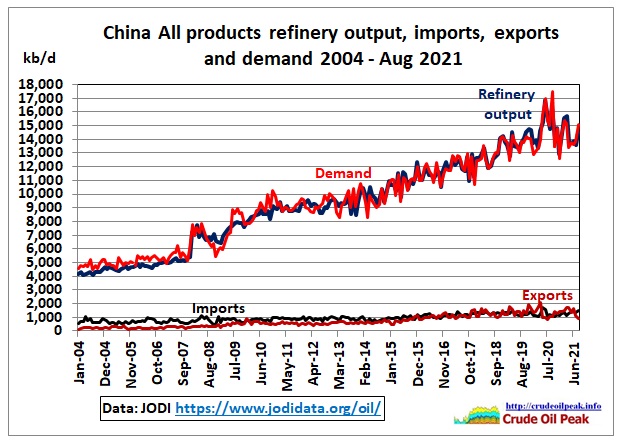

Fig 4: China’s diesel demand, refinery output, imports and exports

Fig 4: China’s diesel demand, refinery output, imports and exports

China’s refinery output of diesel started to hit a ceiling of 3.5 – 3.6 mb/d in 2014. Diesel consumption is a pretty good indicator for economic activities.

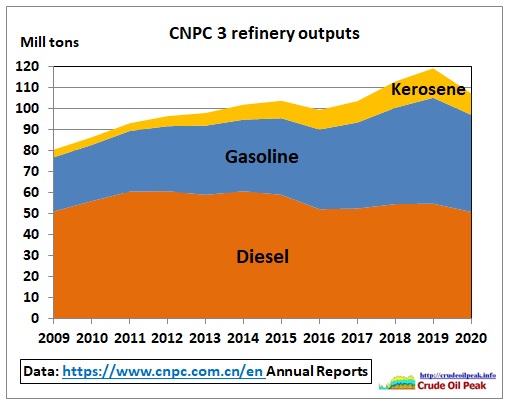

Fig 5: China National Petroleum Company: Diesel, gasoline, kerosene production

Fig 5: China National Petroleum Company: Diesel, gasoline, kerosene production

CNPC’s annual reports show diesel production peaked between 2011 and 2014 at 60 million tons (1.23 mb/d), dropping thereafter to an average of 54 mt pa.

In 2018, Reuters reported:

China’s diesel demand has peaked, gasoline to peak 2025: CNPC research

18 Sep 2018

BEIJING (Reuters) – China’s diesel demand has peaked and gasoline will peak in 2025, while natural gas demand will increase over the next two decades to feed a massive gasification campaign, according to a forecast released on Tuesday by a research arm of a state energy group.

https://www.reuters.com/article/us-china-energy-forecast-cnpc-idUSKCN1LY0Z0

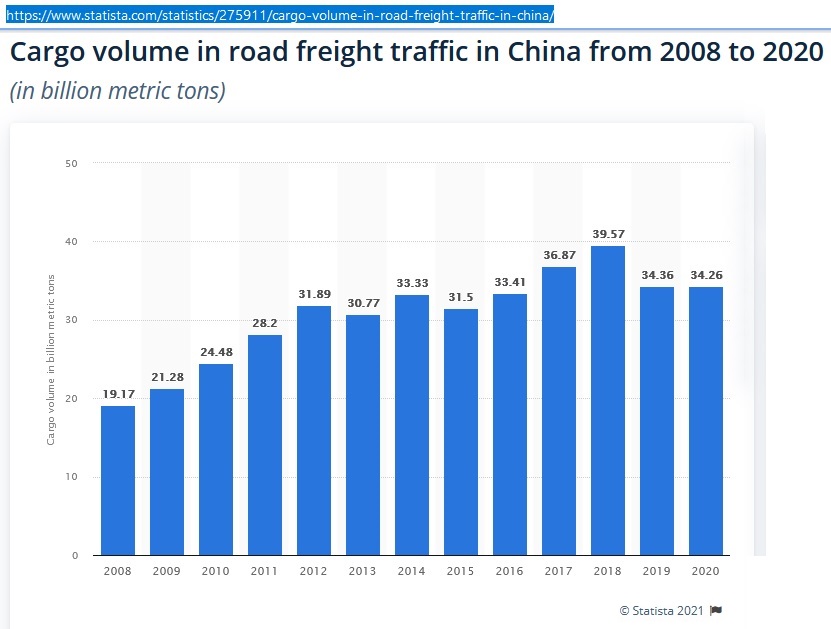

Fig 6: China’s road freight volumes in billion metric tons peaked in 2018

Fig 6: China’s road freight volumes in billion metric tons peaked in 2018

https://www.statista.com/statistics/275911/cargo-volume-in-road-freight-traffic-in-china/

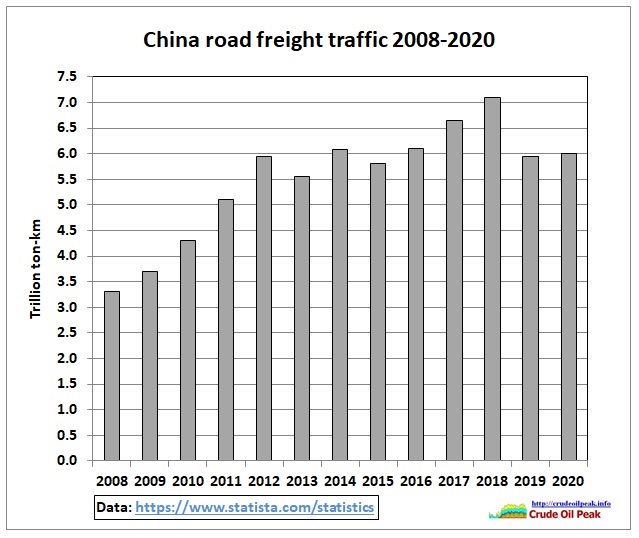

Diesel consumption is of course proportional to freight measured in ton-km

Fig 8: China’s road freight traffic in ton-km

Fig 8: China’s road freight traffic in ton-km

Since we are at it, we look at the other fuels:

Fig 9: Petrol seems to go back to its previous growth path

Fig 9: Petrol seems to go back to its previous growth path

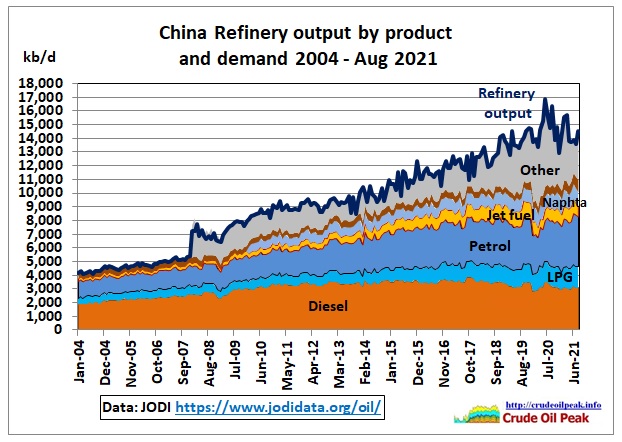

Fig 10: China’s refinery output by fuel

Fig 10: China’s refinery output by fuel

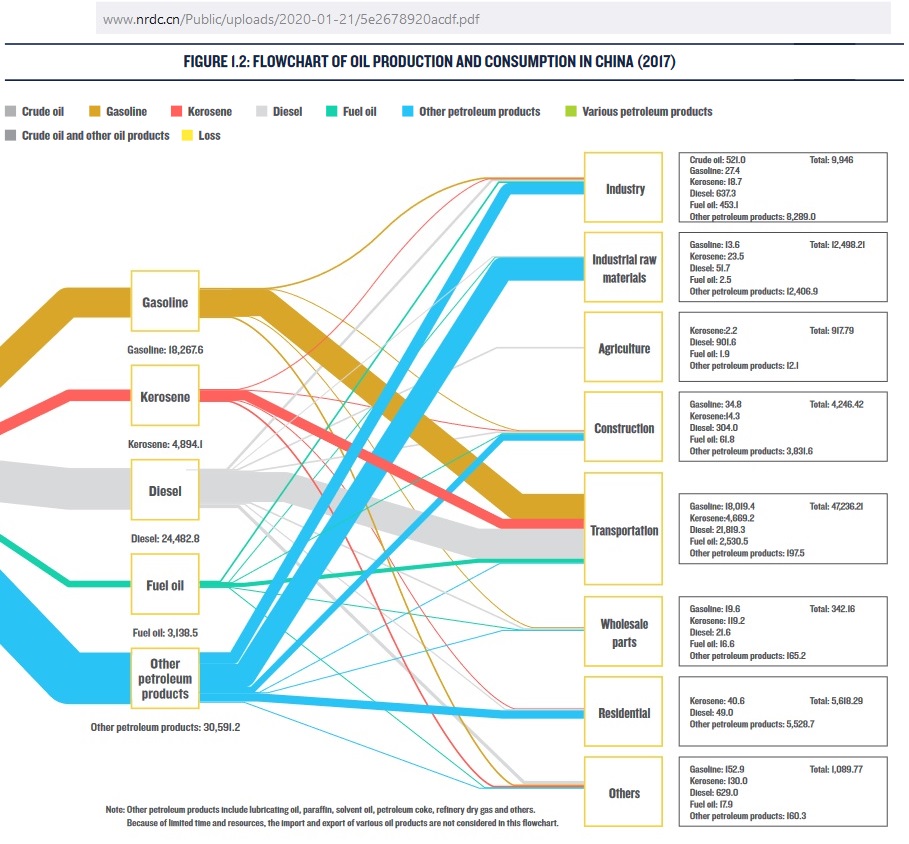

“Other products” were increasing until June 2020 to 6 mb/d, then dropping back to 3.5 mb/d by August 2021. Their use is shown in the following oil flow diagram:

Fig 11: China’s oil flow and end use

Fig 11: China’s oil flow and end use

The above graph is from the Natural Resources Defense Council (NRDC, a leading U.S. environmental group) in a 2019 report titled “China Oil Consumption Cap Plan and Policy Research Project”

http://www.nrdc.cn/Public/uploads/2020-01-21/5e2678920acdf.pdf

It is worthwhile reading this report in full but this goes beyond the scope of this article.

Fig 12: China’s oil consumption by sector

Fig 12: China’s oil consumption by sector

Fig 13: From 2013-2019, refinery output increased by 760 kb/d but then stagnated

Fig 13: From 2013-2019, refinery output increased by 760 kb/d but then stagnated

Generally, refinery output and demand are in balance, as are imports and exports

Fig 14: China in peak oil mode since 2015

Fig 14: China in peak oil mode since 2015

The production peak is very flat, at around 4 mb/d. Imports are the biggest problem.

Impact for Australia

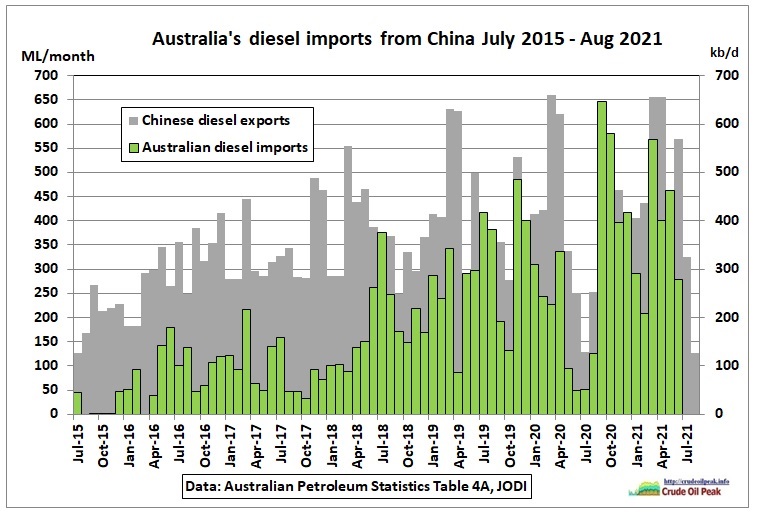

Fig 15: Australia’s diesel imports from China (green columns, LHS) vs. China’s diesel exports (grey columns, RHS in kb/d)

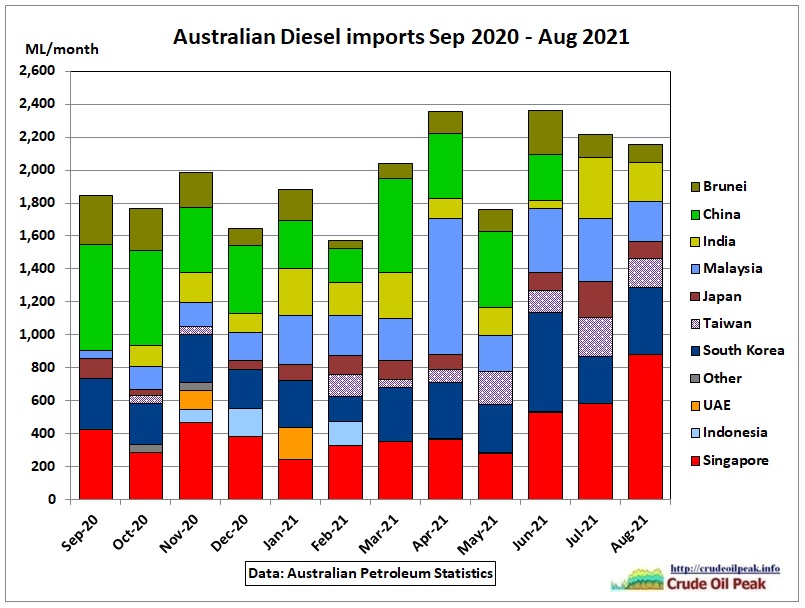

Fig 16: Australian diesel imports in the last 12 months

Fig 16: Australian diesel imports in the last 12 months

Australia had become dependent on Diesel imports from China and Brunei (with a brand new Chinese refinery). After the closure of several refineries Australian fuel importers have become very skilled at finding sources wherever they can. In July and August 2021, Singapore and India replaced China. For how long, remains to be seen.

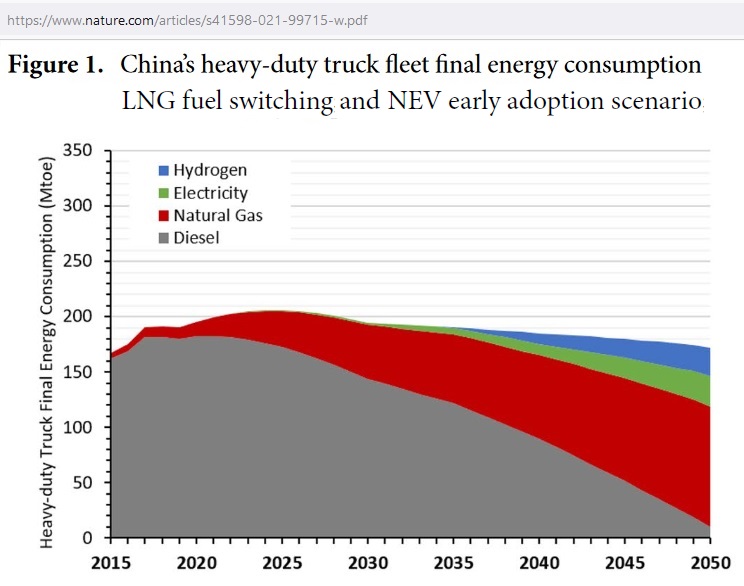

China’s diesel peak was a long time in the making and shows that nothing grows endlessly. The last graph shows how this peak could be transformed into a transition scenario (although many will object to the role of gas in it)

Fig 17: One among many transition paths away from oil based fuels for trucks

Fig 17: One among many transition paths away from oil based fuels for trucks

Source: Near and long-term perspectives on strategies to decarbonize China’s heavy-duty trucks through 2050

https://www.nature.com/articles/s41598-021-99715-w.pdf

Conclusion:

Diesel supplies should not be taken for granted. Apart from current uses, Diesel is needed as construction fuel for the many projects to decarbonize the economy. The transition to replace Diesel must happen before there are Diesel shortages for supply reasons. The world should learn from the Covid supply chain lessons.