This post describes a series of price spikes in NSW which happened between Tuesday the 7th and Wednesday the 8th of May 2024. The following Fig 1 and Fig 2 are screen shots of AEMO’s dashboard (Australian Energy Market Operator)

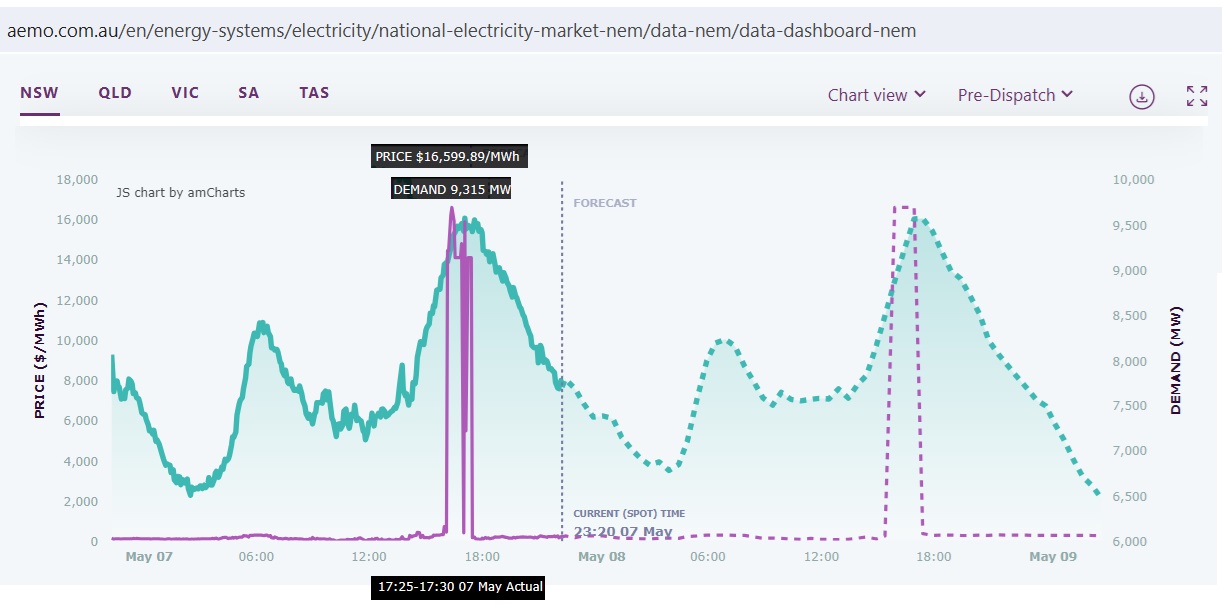

Fig 1: May 7th price spikes up to 16,600 $/MWh at peak hour. Demand 9,300 MW

Fig 1: May 7th price spikes up to 16,600 $/MWh at peak hour. Demand 9,300 MW

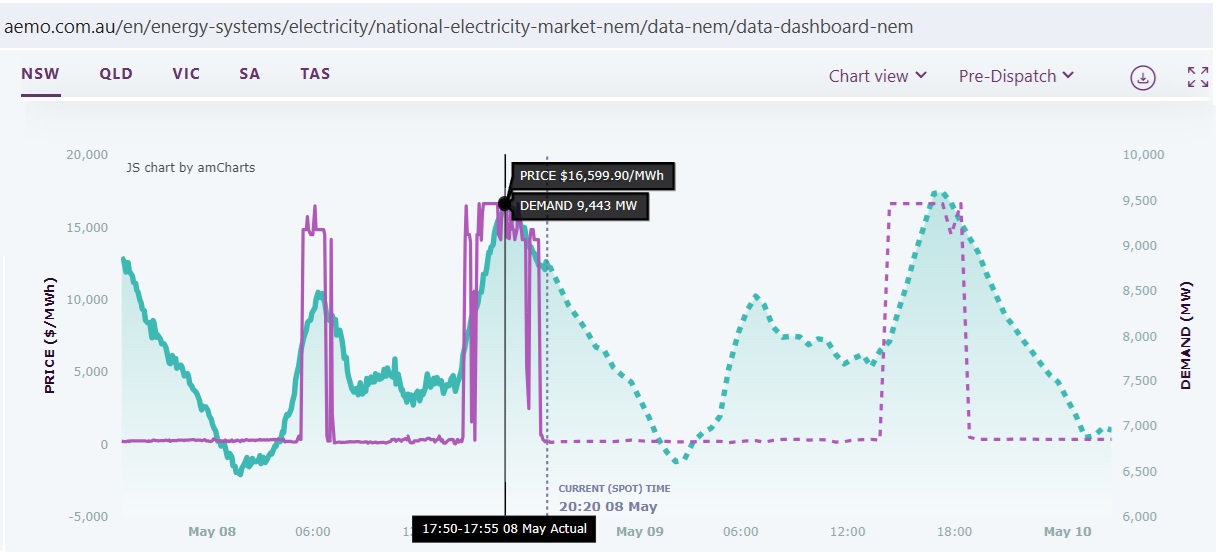

Fig 2: May 8th price spikes both in the morning (!) and afternoon

Fig 2: May 8th price spikes both in the morning (!) and afternoon

These 2 price spikes were not short lived but lasted for 1 hr 15 min in the morning (14,900 $/MWh) and 4 hrs 10 min (14,200 $/MWh), unprecedented.

AEMO had to impose administered price caps according to its NEM rules:

116554 ADMINISTERED PRICE CAP 09/05/2024 03:55:11 AM

AEMO has determined that the rolling sum of the uncapped spot prices for

the NSW1 region over the previous 2016 trading intervals has exceeded

the cumulative price threshold (CPT) of $1,490,200.00.

In accordance with Clause 3.14.2(b) of the National Electricity Rules,

AEMO has determined that an administered price period will commence at

the trading interval starting 0405 hrs on 09 May 2024 and will continue

through to the end of that trading day

https://aemo.com.au/market-notices

The CPT is calculated over 7 days

• the sum of the regional reference prices (spot prices) in the energy market for the previous 2,016 trading intervals (equivalent to seven days) exceeds the cumulative price threshold (CPT); or

• the sum of the ancillary service prices for a market ancillary service for the previous 2,016 trading intervals (equivalent to seven days) exceeds the CPT.

https://aemo.com.au/-/media/files/electricity/nem/security_and_reliability/dispatch/policy_and_process/guide-to-administered-pricing.pdf

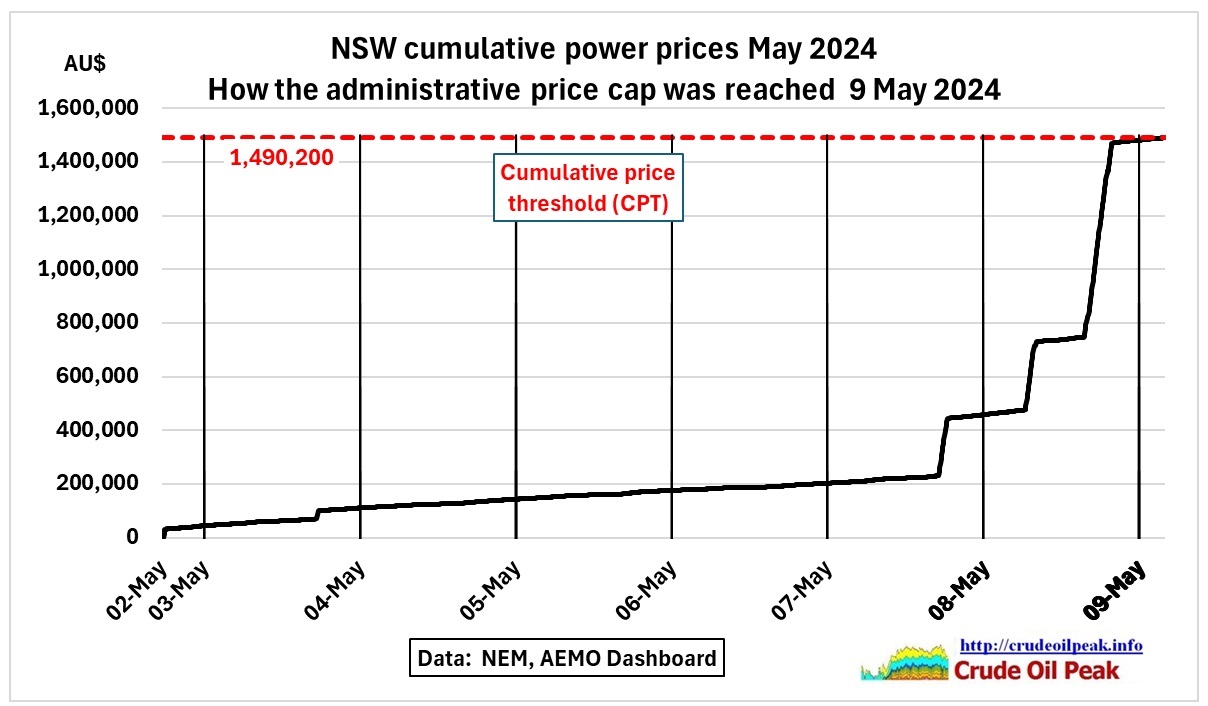

Let’s have a look at how this developed over time:

Fig 3: Consecutive price spikes add up and hit the threshold on May 9th

Fig 3: Consecutive price spikes add up and hit the threshold on May 9th

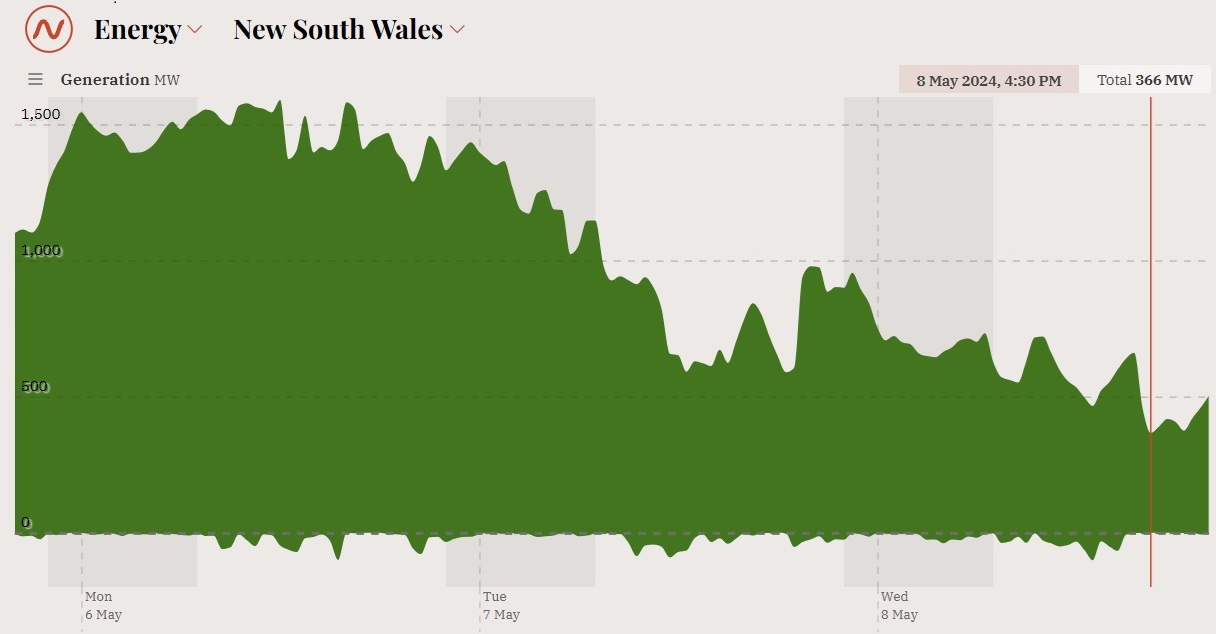

How did that happen? In the following Fig 4 the price spikes have been drawn in a generation-by-fuel graph.

Fig 4: NSW power generation by fuel and periods of price spikes between vertical lines

Fig 4: NSW power generation by fuel and periods of price spikes between vertical lines

We see 3 price spikes coincide with demand peaks and limited generation from coal. At the time of the peaks the combined capacity factor of all coal plants was 62%-64%, 51%-53% and 48%-57% respectively.

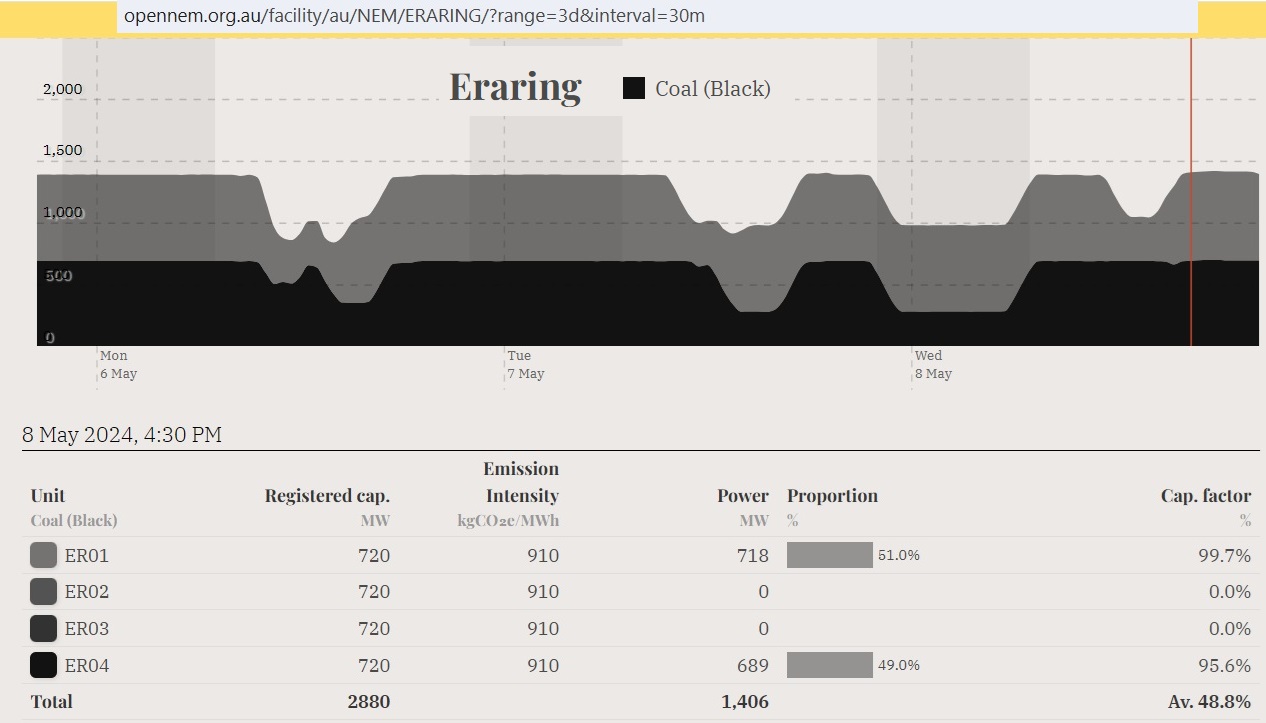

Fig 5: Only two of Eraring’s four units were in operation

Fig 5: Only two of Eraring’s four units were in operation

Unit ER02 was on an unplanned maintenance since May 2nd and ER03 had experienced an unplanned forced outage on May 3rd. Unit ER04 did not reach its rated capacity.

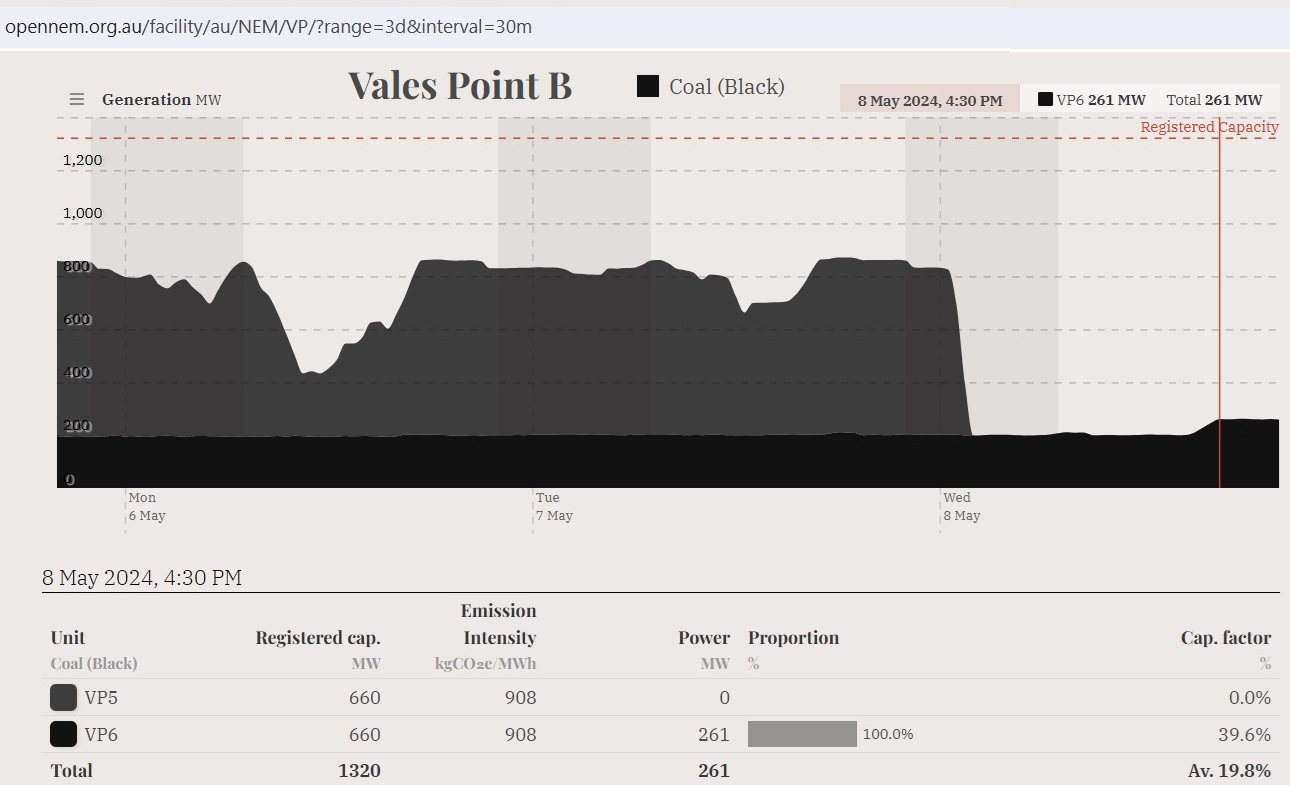

Fig 6: Vales Point VP5 tripped on 8 May 1:30 am

Fig 6: Vales Point VP5 tripped on 8 May 1:30 am

7/10/2022

Sale of Vales Point: How will Czech brown coal baron Pavel Tykac with

business registered in Liechtenstein impact on NSW coal and energy markets?

http://crudeoilpeak.info/sale-of-vales-point-how-will-czech-brown-coal-baron-pavel-tykac-with-business-registered-in-liechtenstein-impact-on-nsw-coal-and-energy-markets

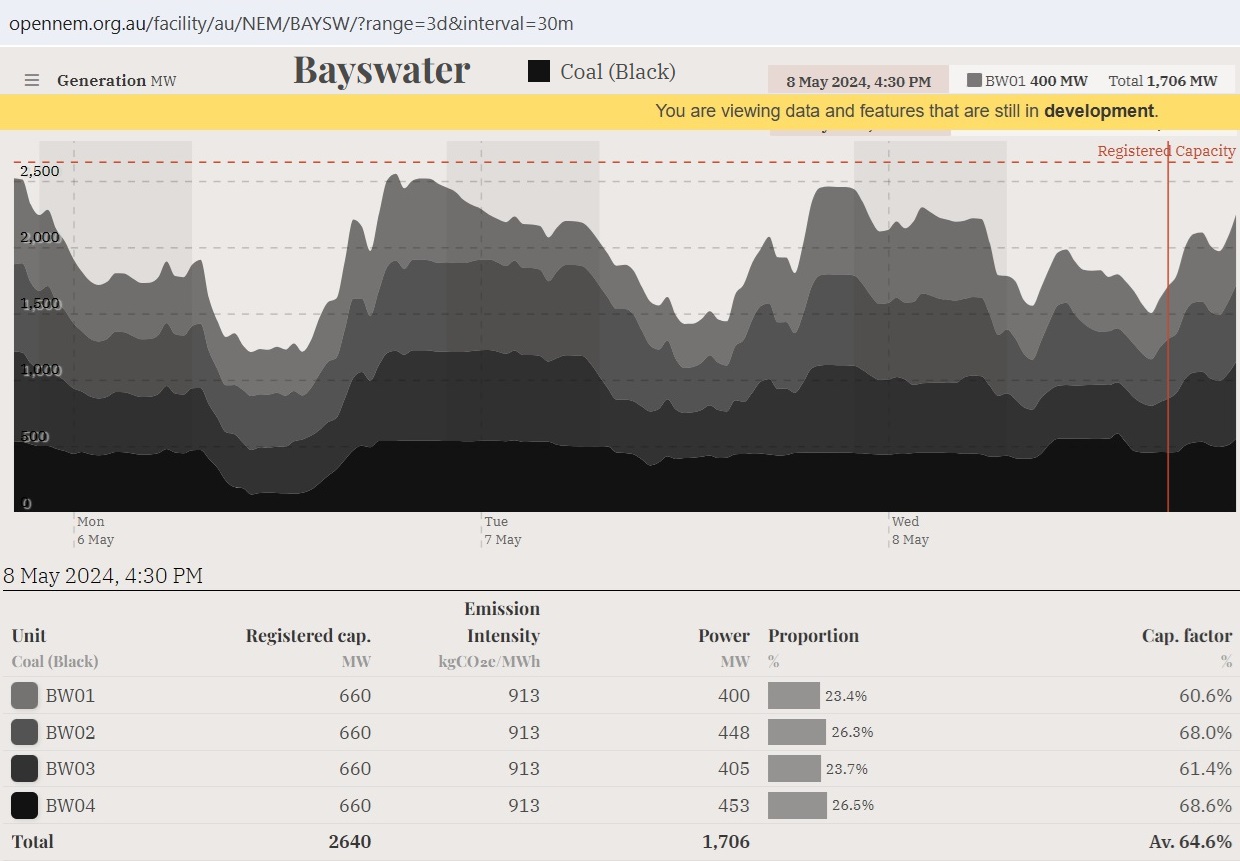

Fig 7: Bayswater was running at 65% of its capacity at the critical time of 4:30 pm on May 8th

Fig 7: Bayswater was running at 65% of its capacity at the critical time of 4:30 pm on May 8th

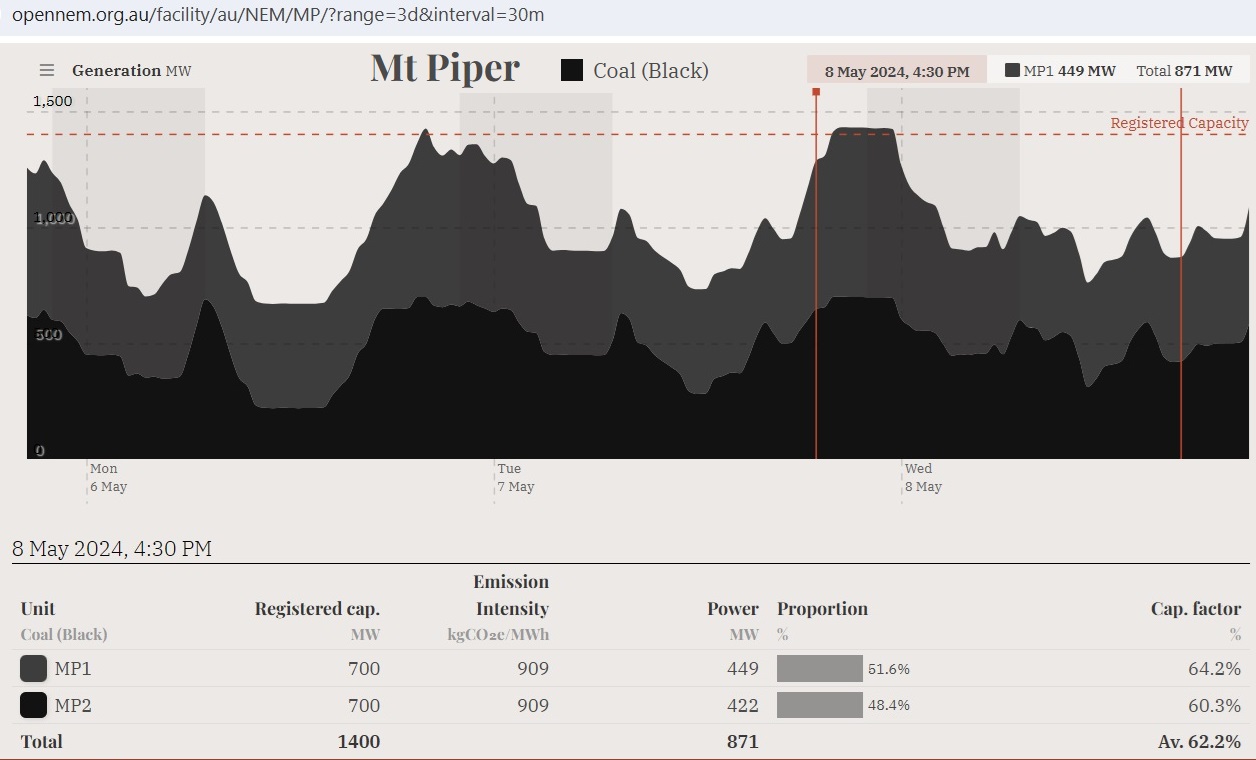

Fig 8: Mt Piper was generating on a bumpy plateau on May 8th, not exceeding 70%

Fig 8: Mt Piper was generating on a bumpy plateau on May 8th, not exceeding 70%

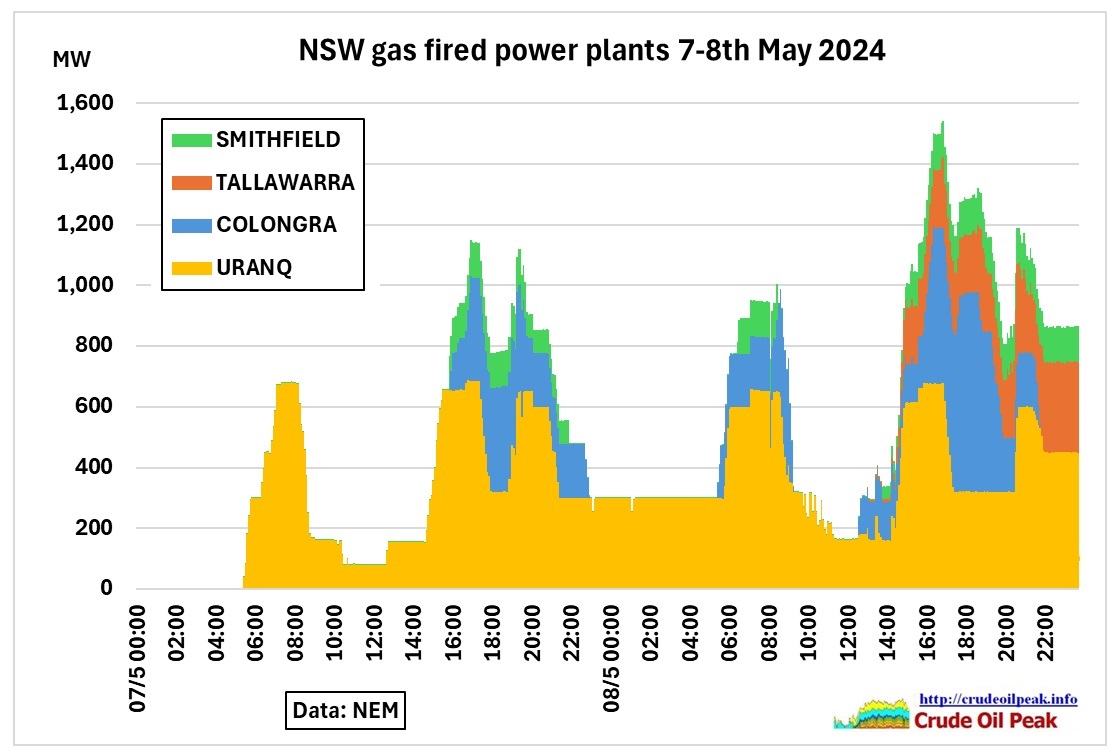

Fig 9: NSW depends heavily on gas peaking plants

Fig 9: NSW depends heavily on gas peaking plants

https://wattclarity.com.au/articles/2024/05/08may-review-nsw-gas-gen-bidding/

Fig 10: Gas fired peakers. Tallawarra B was not in operation since Apr 9th

Fig 10: Gas fired peakers. Tallawarra B was not in operation since Apr 9th

Delving deeper, into gas-fired peaker performance in NSW on Tue 7th May and Wed 8th May

10 May 2024

https://wattclarity.com.au/articles/2024/05/08may-review-nsw-gas-gen-bidding/

Fig 11: Generation from wind declined over 3 days

Fig 11: Generation from wind declined over 3 days

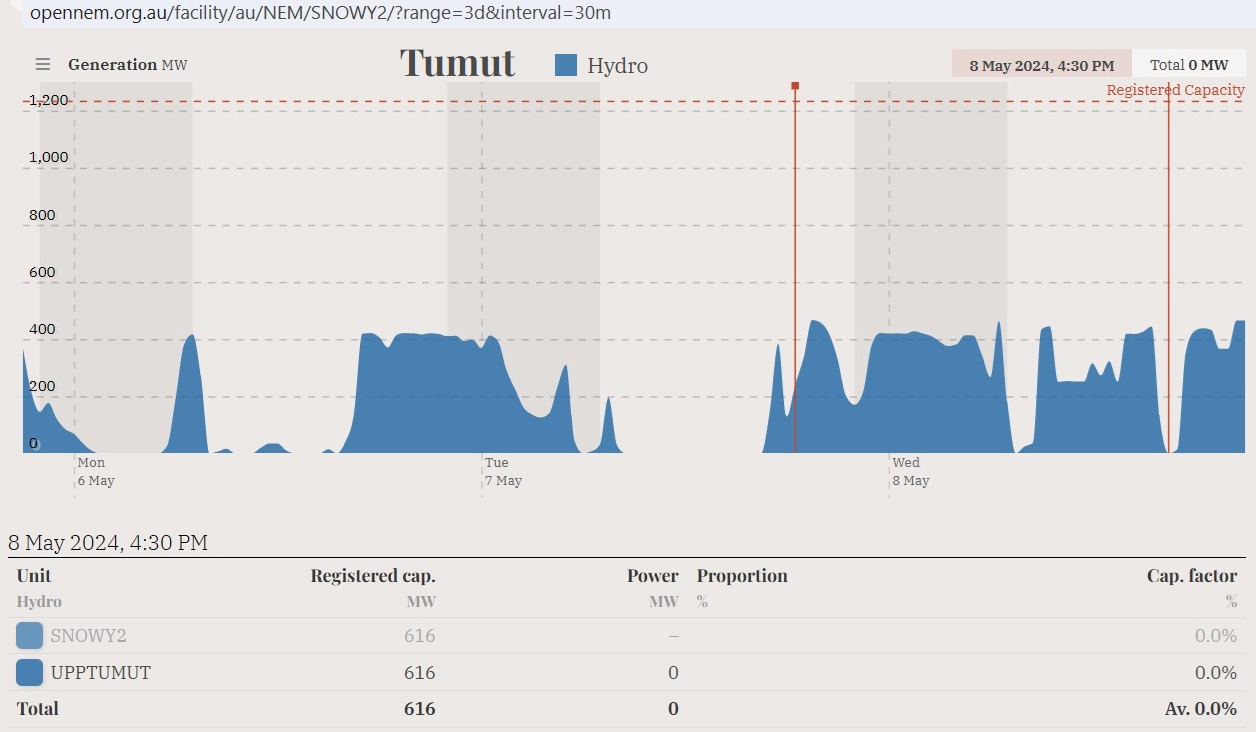

Fig 12: Upper Tumut had a drop in generation of 400 MW at the beginning of the afternoon peak May 8th

Fig 12: Upper Tumut had a drop in generation of 400 MW at the beginning of the afternoon peak May 8th

There were 3 Lack of Reserve warnings

Fig 13: Table showing Lack of Reserve (LOR) warnings 8 May 2024

Fig 13: Table showing Lack of Reserve (LOR) warnings 8 May 2024

Summary:

The price spikes are indicators that the NSW power supply has severe problems to cope with multiple and simultaneous challenges like peak demand after sunset (in winter), unplanned outages of coal fired power plants, lack of wind and availability of gas fired plants.