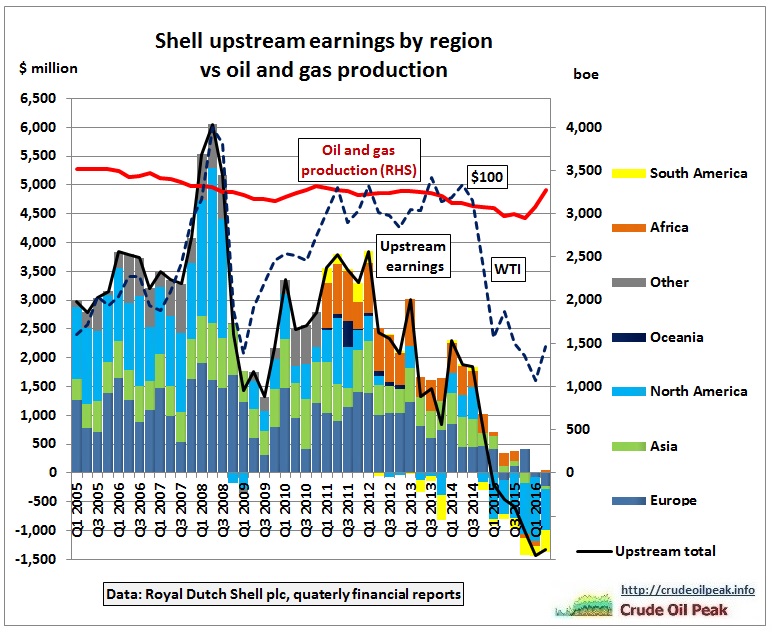

Shell’s upstream earnings1) were in the red since the 1st quarter of 2015 according to first half 2016 reports. Earnings peaked at US$ 6 bn in the 2nd quarter of 2008 and declined to US$ -1.3 bn in the 2nd quarter of 2016.

Oil and gas production

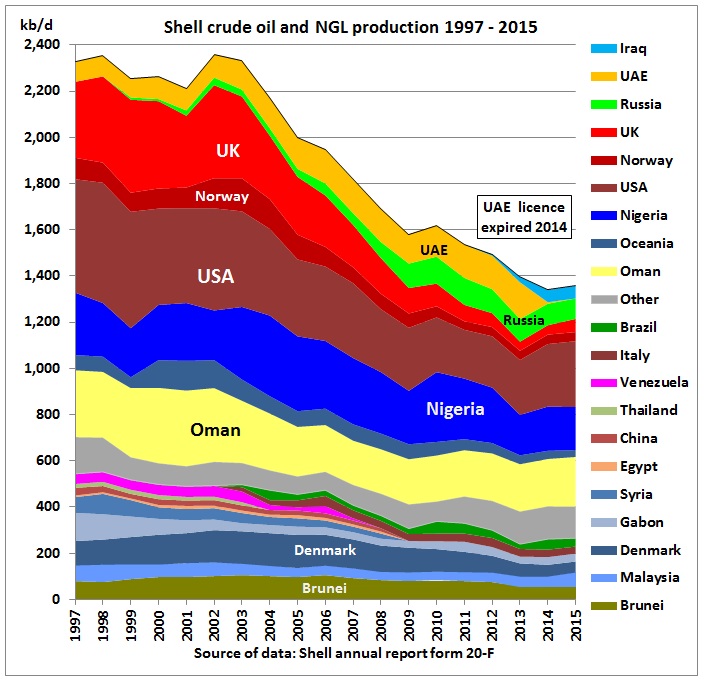

Fig 1: Shell’s crude oil and NGL production

http://www.shell.com/investors/financial-reporting/sec-form-20-f.html

We can see that in response to the conventional peak in 2002 of its long-term assets Shell tried to compensate decline and diversify into:

- Russia (Fig 1)

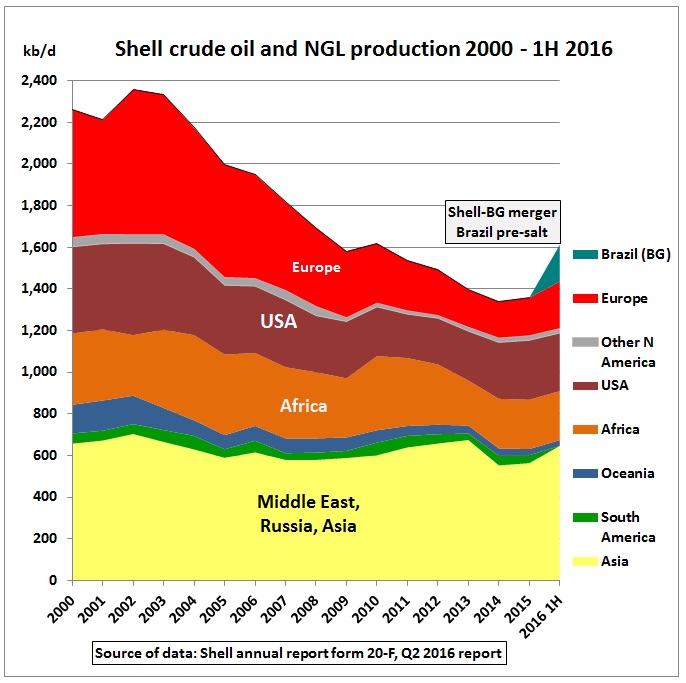

- Iraq (Fig 2)

- Syn-crude from tar sands (Fig 2)

- Brazil sub-salt (Fig 2)

Fig 2: Shell crude, NGL and syncrude production

Half-yearly data for 2016 are not available on country level so we have to use the very strange group of Middle East, Russia and Asia of the half yearly report in order to show the 1H 2016 Brazil uptick after the BG merger.

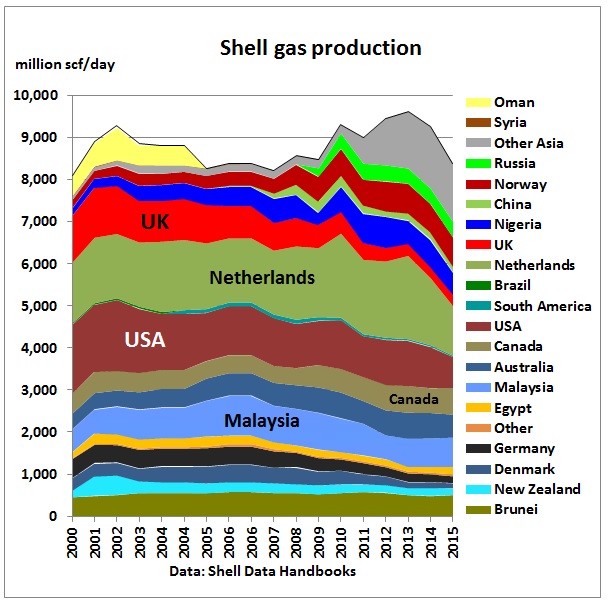

Fig 3: Shell gas production

Note the sharp drop in gas production in the Netherlands after 2012.

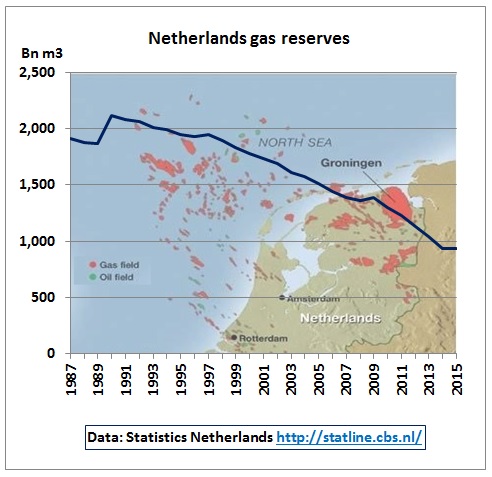

Netherlands literally running out of gas

17/9/2016

The European Union’s biggest natural gas producer is running out of reserves.

The Netherlands, also the region’s largest trading hub for the fuel, has used up almost 80 percent of its natural gas reserves, Dutch statistics office CBS said on Friday. Production fell 38 percent over the previous two years and is set to fall further as the government limits extraction because of earthquakes in Groningen, the province that houses the EU’s largest gas deposit, it said.

The nation of about 17 million people is struggling to contain tremors linked to gas production by a joint venture of Exxon Mobil Corp. and Royal Dutch Shell Plc that has damaged thousands of homes. The government budget has been hit by the caps on extraction and declining wholesale prices, with gas accounting for just 3 percent of state income in 2015, down from 9 percent two years earlier, the CBS said.

https://www.energyvoice.com/oilandgas/europe/119556/netherlands-literally-running-gas/

Fig 4: Gas reserves in the Netherlands

Upstream Earnings

Let’s see how the oil production peak and the bumpy gas production plateau impacted on Shell’s upstream earnings:

Fig 5: Shell upstream earnings vs oil and gas production

(5,800 scf gas = 1 barrel oil equivalent)

Data are from this website:

Fig 5 shows:

- Up to the financial crisis earnings were proportional to oil prices and the drop in production was covered up

- After the financial crisis earnings were less than expected after oil prices rebounded

- After the oil price drop in 2014, from $100 to $50, earnings did not just halve, but went into the red

This means a structural change is happening. It is getting harder and harder to make money by producing oil and gas and selling it at an acceptable price.

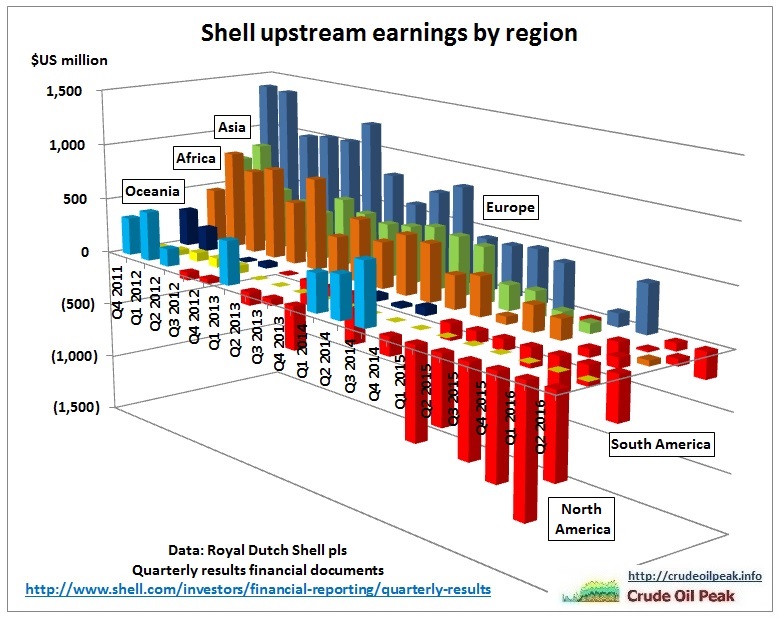

Here is another 3D view of Fig 5

Fig 6: Shell upstream earnings by region

In the 2nd quarter of 2016, all regions except Africa were in the red. The biggest losses are in North America.

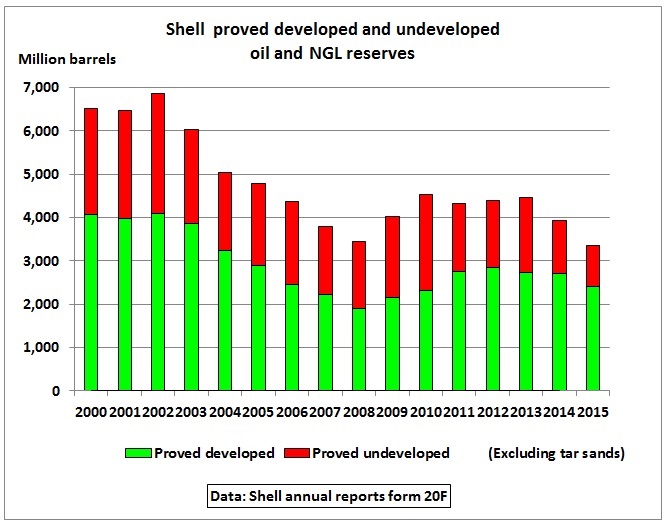

Reserves

Fig 7: Shell’s proved oil and NGL reserves

Reserves are on a downward trending roller coaster.

Conclusion:

If oil prices remain low, no one knows how long oil companies will survive. They are not charity organisations. Even if oil prices were to come back to $100 over a period of several years (which would kill the global economy for good because of the high debt accumulated during the previous high oil price episode), earnings would be unlikely to come back to pre-2008 levels. It seems that the international oil supply system is financially unstable. Governments should heed the warnings coming from analysing oil company data. As a minimum nor more oil dependent infrastructure should be built. Better of course are rail projects but the time is running out.

Note:

1) Earnings excluding integrated gas (which incorporates LNG marketing and trading) and excluding identified (exceptional, non-recurring) items