Fig 1: Australian crude oil and condensate production

Fig 1: Australian crude oil and condensate production

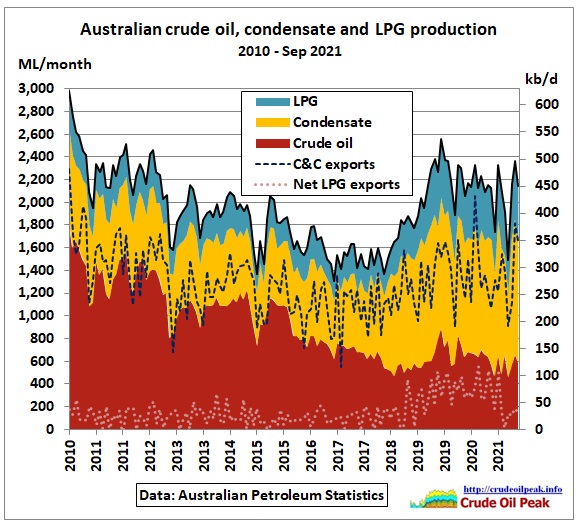

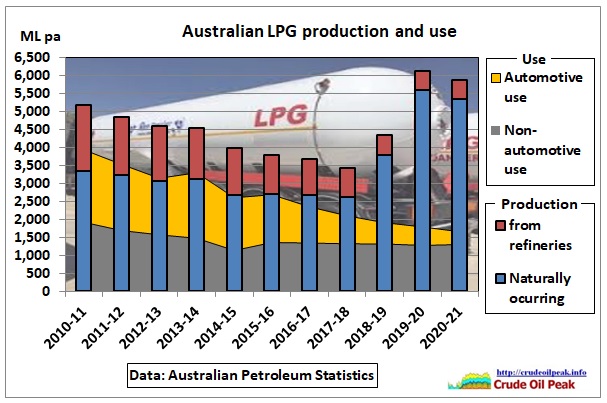

Australian crude production is on a long term decline trend. Condensate has rebounded in 2018 due to an increase from offshore LNG, but since Australian refineries can’t use much condensate it is exported and that’s why we see an increase in C&C exports. Another light fraction, LPG, also grew over the same time period allowing more exports – while LPG automotive use has declined. See graph in the Appendix.

Fig 2: Australian crude oil imports by country

Fig 2: Australian crude oil imports by country

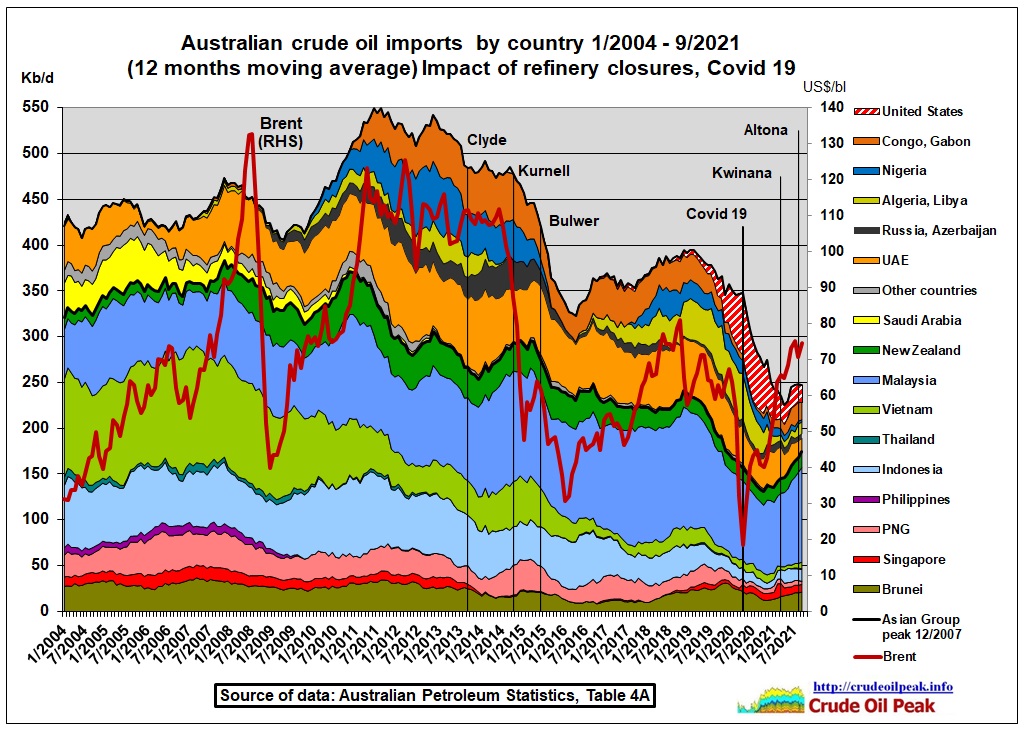

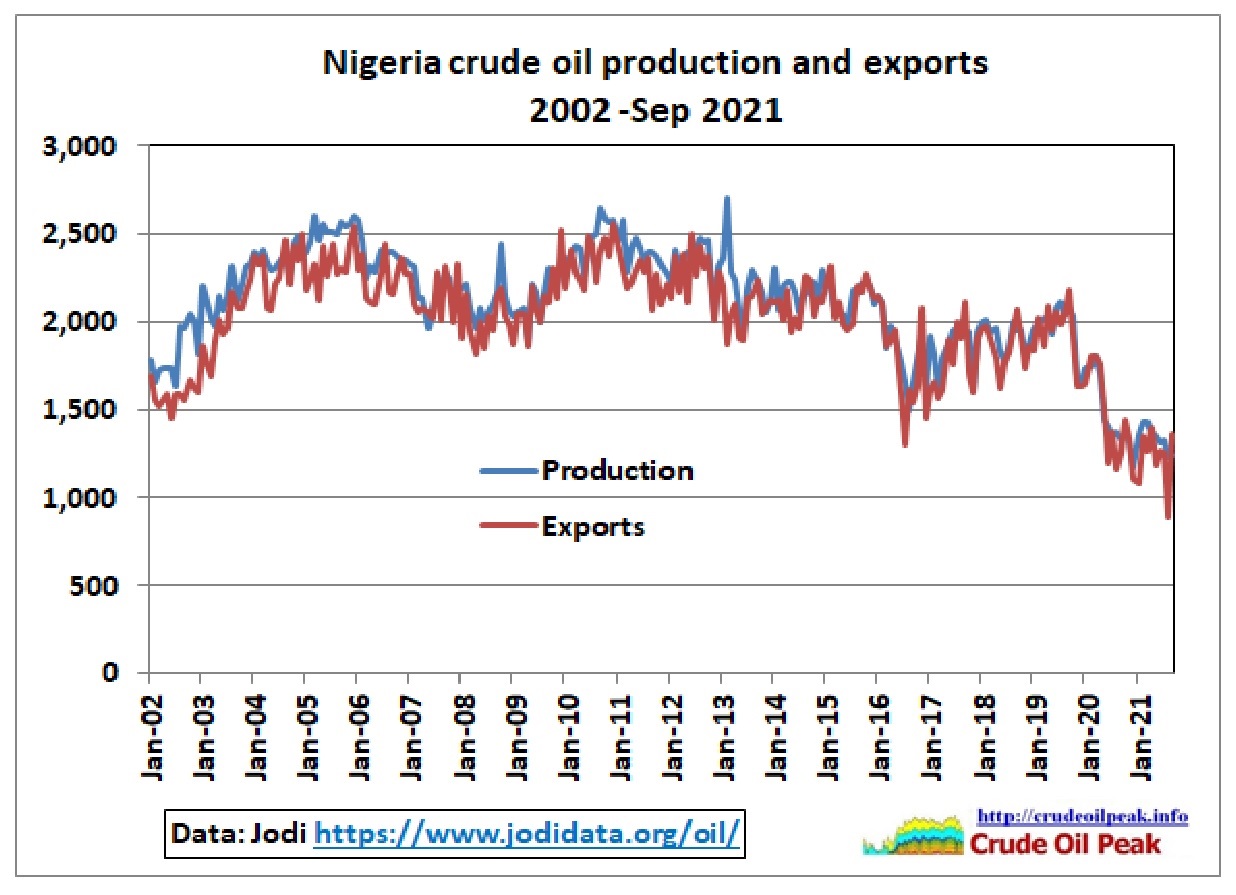

As oil production in neighbouring Asia Pacific countries peaked between 2007 and 2011 (see Fig 8 below), Australian refineries started to diversify their sources of supplies into West Africa (Congo, Gabon, Nigeria), but oil production there declined. Here is the example of Nigeria:

Fig 3: Nigerian crude oil production and exports

Fig 3: Nigerian crude oil production and exports

26 Aug 2021

“A lack of upstream investment in Nigeria along with OPEC+ cuts has contributed to a steady fall in its oil production over the past decade.

All of Nigeria’s oil refineries, with a combined nameplate capacity of 445,000 b/d, are currently shut, following years of neglect, even as NNPC has been looking to reform the sector for almost a decade.”

Therefore, “Nigeria currently exports almost all of the crude and condensate it produces.”

https://www.spglobal.com/platts/en/market-insights/latest-news/oil/082621-refinery-news-nigerias-nnpc-to-supply-300000-bd-of-crude-to-dangote-refinery

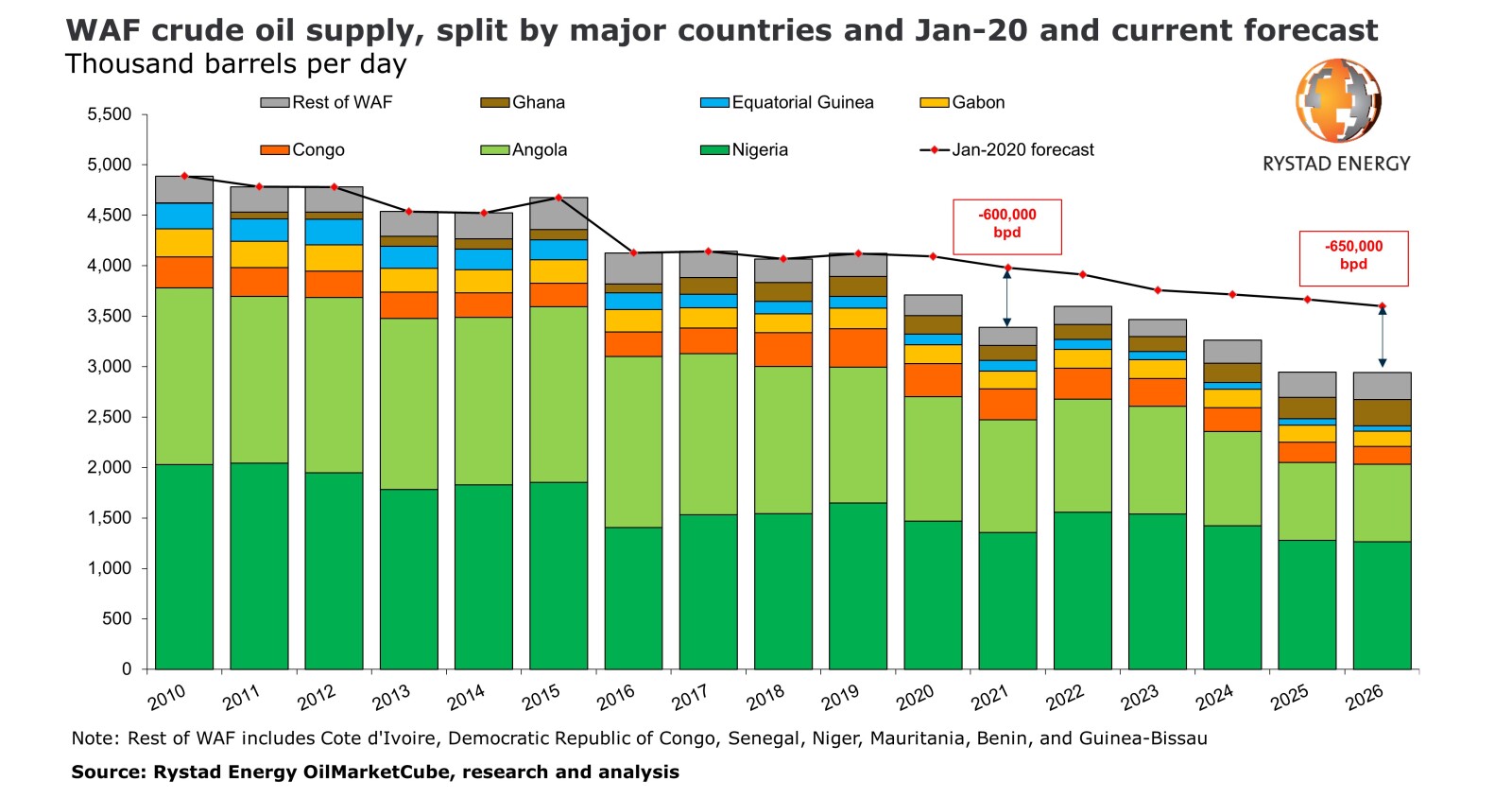

Rystad, a Norwegian energy consultant, forecasts further decline in West Africa

Fig 4: Rystad adjusted production forecast downwards due to lack of CAPEX

Fig 4: Rystad adjusted production forecast downwards due to lack of CAPEX

https://www.rystadenergy.com/newsevents/news/press-releases/low-jet-fuel-demand-and-structural-obstacles-push-west-africas-crude-output-into-lasting-decline/

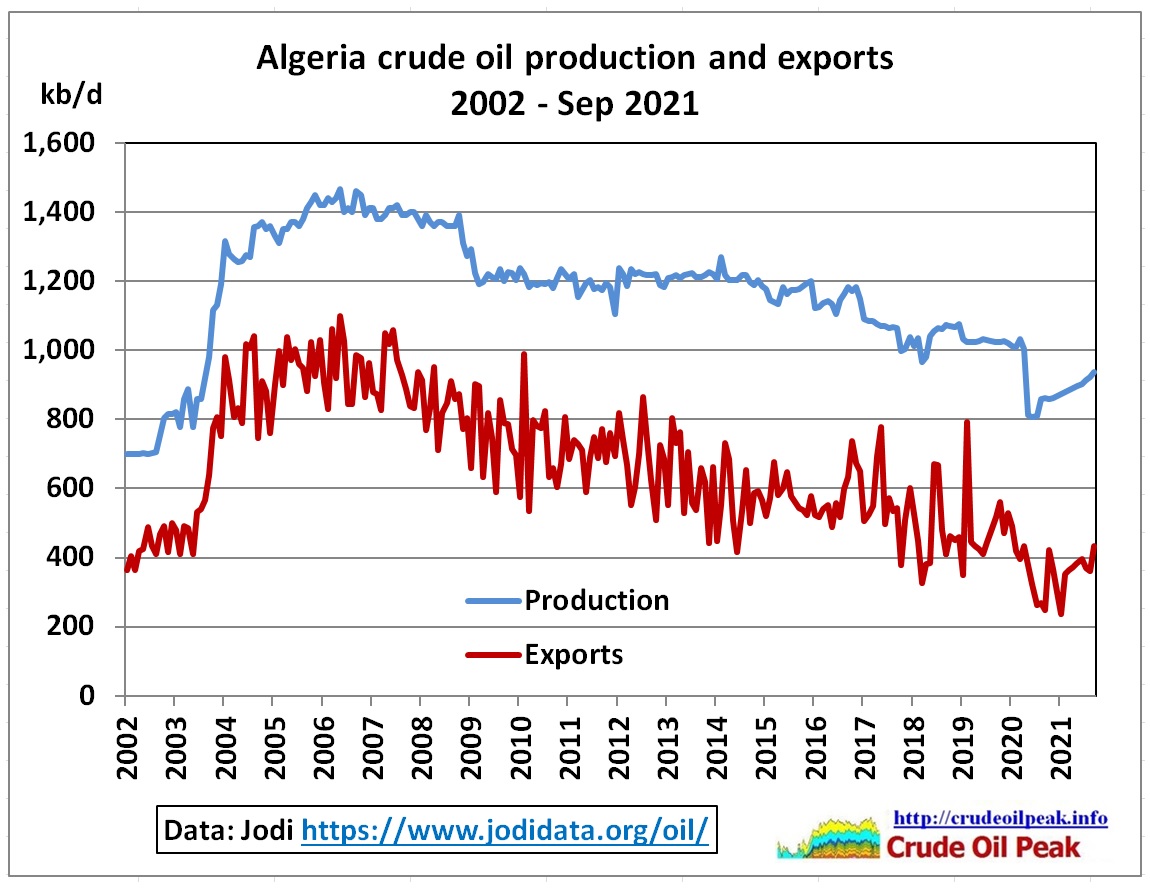

Another example is Algeria in North Africa (see in Fig 2: AU imports from Algeria and Libya)

Fig 5: After oil production and exports peak it is more difficult to import oil

Fig 5: After oil production and exports peak it is more difficult to import oil

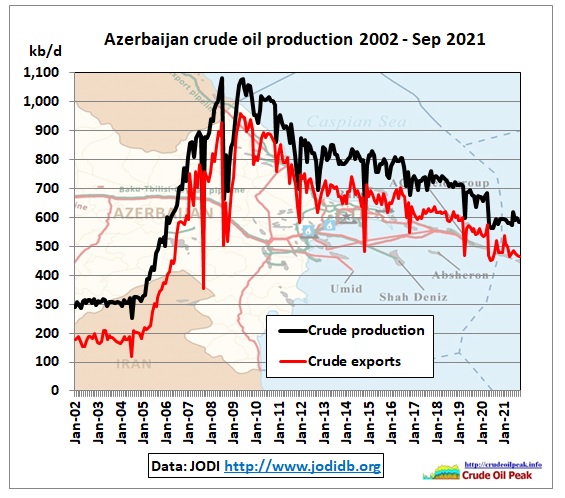

Fig 6: Azerbaijan crude production and exports

Fig 6: Azerbaijan crude production and exports

Australian refineries even sourced their crude from Russia and Azerbaijan. But all these efforts were apparently too difficult in competition with more modern, much larger refineries in Asia. 3 Australian refineries closed and crude imports dropped accordingly.

Billion-dollar burden weighs on ailing refiners

12 Sep 2020

COVID-19 has intensified the crisis for Australia’s remaining oil refineries while the need for costly upgrades clouds their future, just when retaining critical manufacturing has become a priority.

https://www.afr.com/companies/energy/billion-dollar-burden-weighs-on-ailing-refiners-20200910-p55u78

Then 2 more refineries shut down

14/11/2020

Australia’s BP Kwinana refinery closure: peak oil context

https://crudeoilpeak.info/australias-bp-kwinana-refinery-closure-peak-oil-context

15/2/2021

Exxon-Mobil’s refinery closure in Australia: peak oil context

https://crudeoilpeak.info/exxon-mobils-refinery-closure-in-australia-peak-oil-context

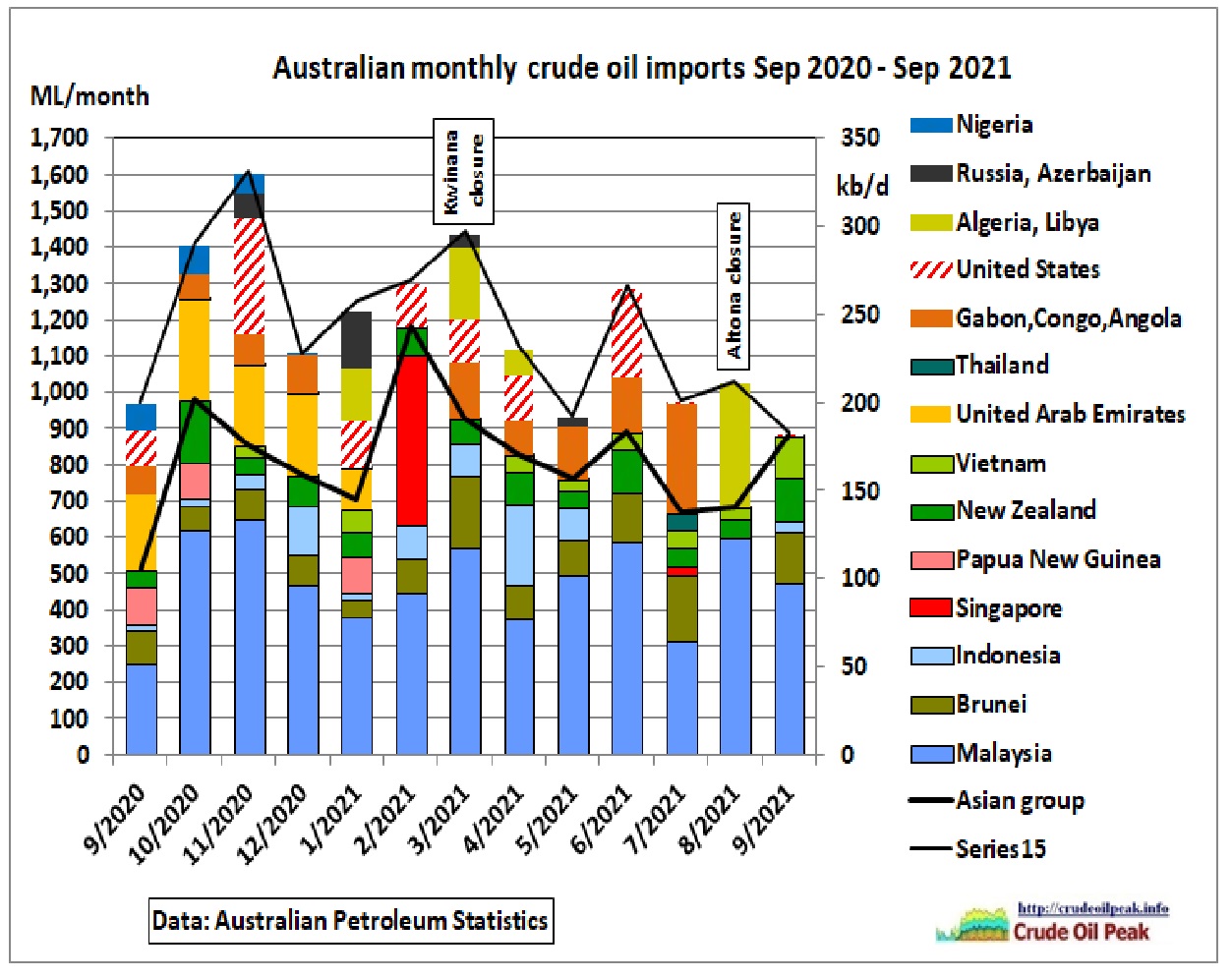

Let’s have a look at the last year:

Fig 7: Monthly crude imports

Fig 7: Monthly crude imports

Long term imports from the UAE ended because these were used by the Kwinana refinery. In the last 4 months imports from outside Asia came again from Africa, but at a reduced volume compared to 2011/19, and from the US. Oil production in the Asian group has of course peaked:

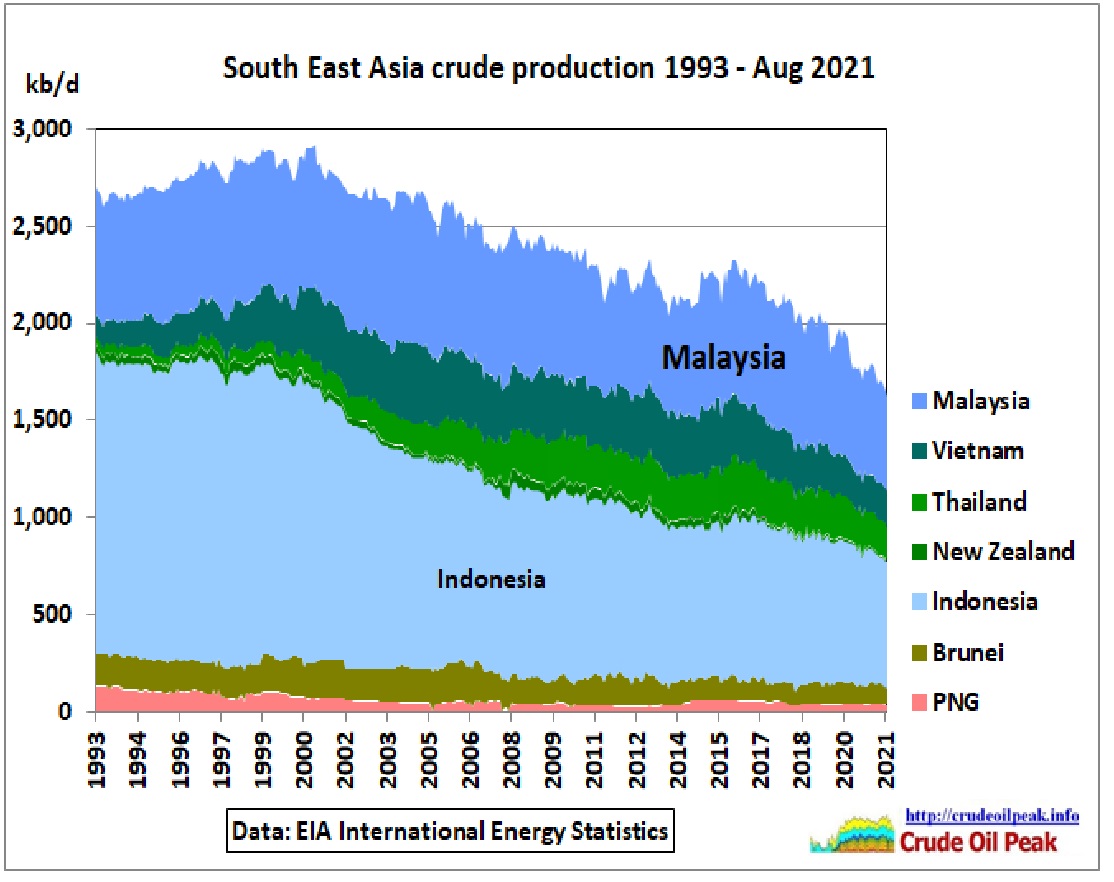

Fig 8: Crude production in South East Asia

Fig 8: Crude production in South East Asia

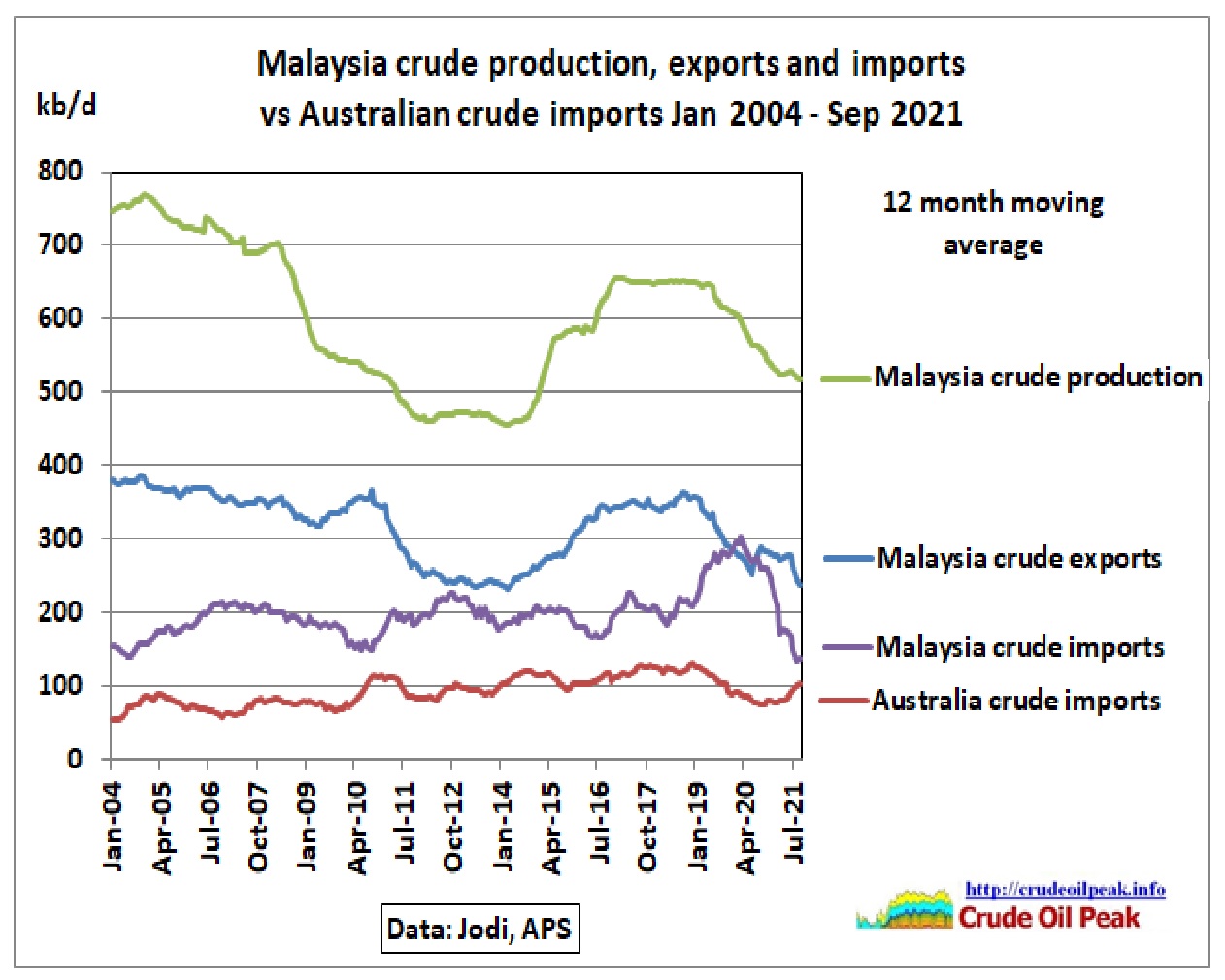

Given the high percentage of Australian imports from Malaysia (around half of all imports), the 2nd Malaysian peak 2015-2017 is most relevant and is worth looking at.

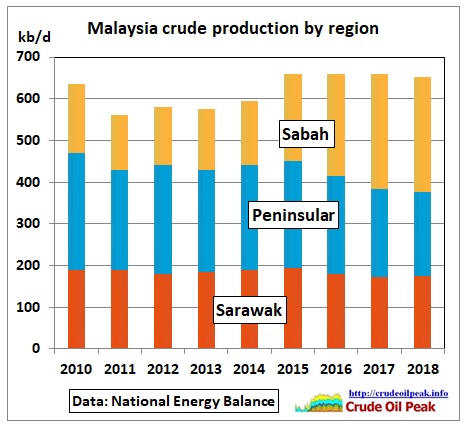

The 2nd peak comes from a production increase in Sabah (East Malaysia on the island of Borneo)

Fig 9: Malaysian oil production by region, mostly offshore

Fig 9: Malaysian oil production by region, mostly offshore

Sabah can just about compensate for decline on the Peninsula.

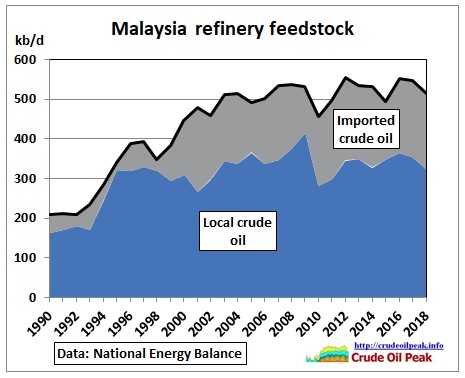

Malaysia needs to keep its refineries going (500 kb/d).

Fig 10: Malaysian refineries: feedstock by source

Fig 10: Malaysian refineries: feedstock by source

https://www.st.gov.my/en/contents/files/download/111/National_Energy_Balance_20181.pdf

Malaysia needs to import oil for blending in their refineries. The ratio is approximately 200 kb/d imported and 300 kb/d local crude. That is important to know when looking at the oil balance in the following graph:

Fig 11: Malaysia’s oil balance and Australian crude imports

Fig 11: Malaysia’s oil balance and Australian crude imports

After Malaysian oil production peaked in 2004 at around 800 kb/d crude exports went down but rebounded due to the above mentioned production increase. In 2021, exports were back to 2012 levels. So there is little scope for a sustainable increase in Australian crude imports (100 kb/d) from Malaysia, should other sources fail over a prolonged period.

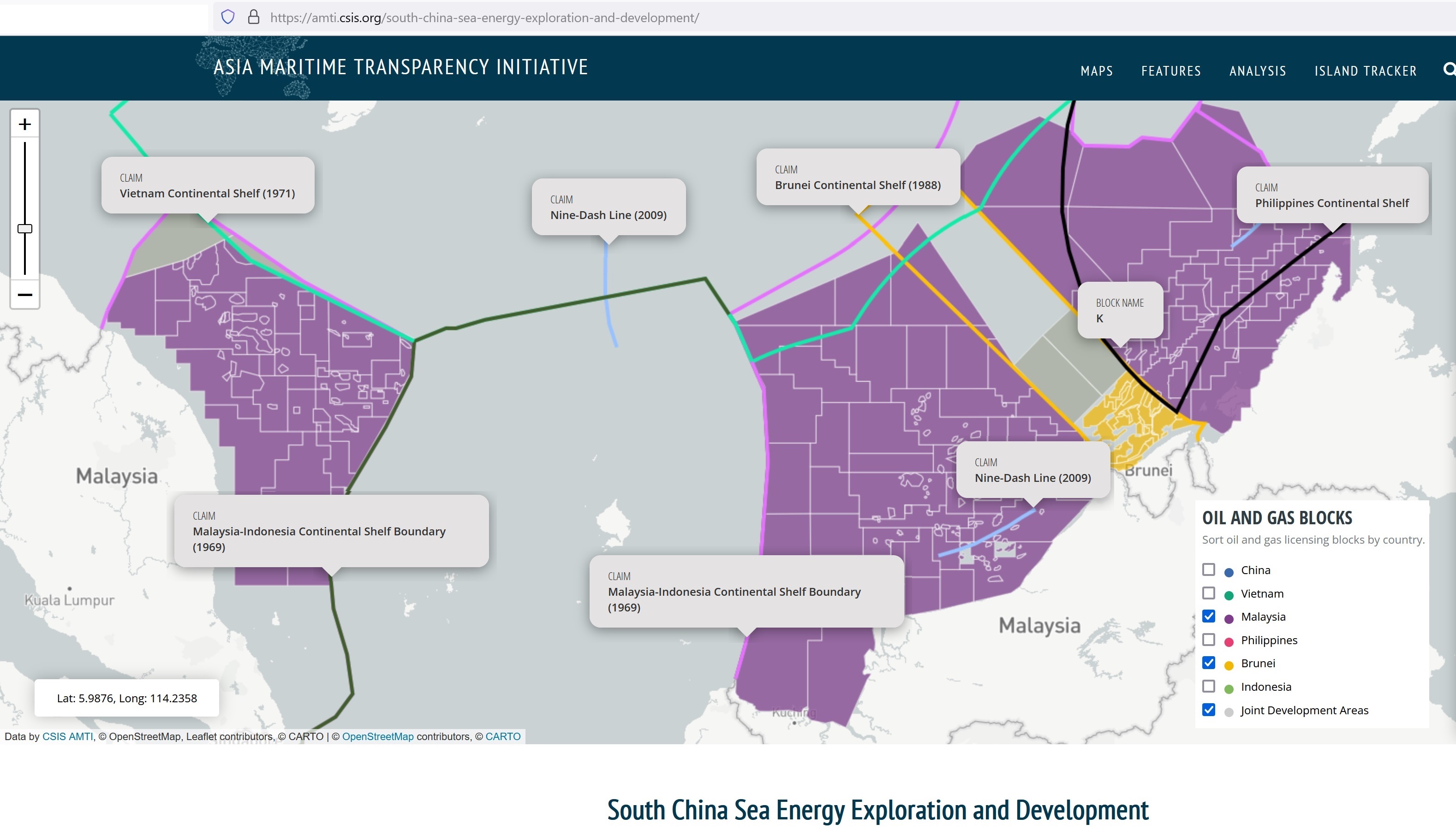

We also should not forget that oil and gas fields offshore Sarawak and Sabah are located close to or within the 9 dash line area claimed by China.

Fig 12: Map showing Malaysia’s EEZ offshore blocks, 9-dash line and other claims

Fig 12: Map showing Malaysia’s EEZ offshore blocks, 9-dash line and other claims

https://amti.csis.org/south-china-sea-energy-exploration-and-development/

Just where recent production increases happened and/or where new exploration takes place, e.g. Block K (Siakap North Petai) mentioned in the article below, the Chinese Coast Guard is harassing drilling ships:

12 Nov 2021

“Over the last four months, Chinese vessels have been contesting Indonesian and Malaysian oil and gas activity in the South China Sea in the latest instance of what is now an established pattern. Chinese law enforcement has maintained a continuous presence at the site of new Indonesian drilling north of the Natuna Islands since early July and a Chinese survey ship conducted seabed surveys in Indonesia’s exclusive economic zone (EEZ) and continental shelf. Another Chinese vessel simultaneously conducted a seabed survey of Malaysia’s continental shelf in apparent retaliation for new drilling off Sabah. Satellite imagery and commercial automatic identification system (AIS) data reveal several close encounters between the China Coast Guard (CCG) and Indonesian law enforcement and navy, as well as the visit of a U.S. aircraft carrier near the site of the standoff—but neither appeared to have much effect on the CCG. At the time of publishing, Chinese law enforcement remains active at the Indonesian drilling site.”

https://amti.csis.org/nervous-energy-china-targets-new-indonesian-malaysian-drilling/

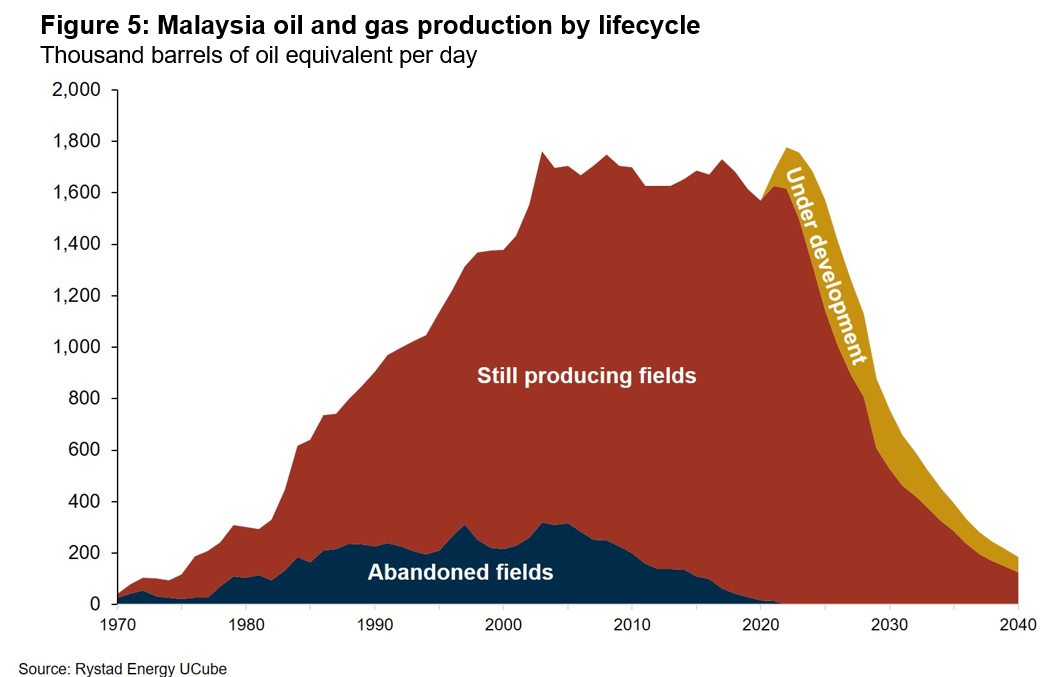

Perhaps the most telling analysis comes from research published in February 2021 by the Norwegian oil & energy consultant Rystad:

Fig 13: Malaysian oil and gas production forecast with decline after the mid 20s

Fig 13: Malaysian oil and gas production forecast with decline after the mid 20s

For the above graph, gas is converted to barrels of oil equivalent. Rystad’s report writes:

“Malaysia’s oil and gas production has been relatively steady over the past 20 years and is currently at about 1.6 million barrels of oil equivalent per day. After 2022–2023, however, production is set to decline steeply, even with projects that are currently under development. The country is therefore facing an urgent need to reverse or slow down this trend and encourage investment both into exploration and exploitation.”

https://www.rystadenergy.com/newsevents/news/newsletters/EandP/ep-february-2021/

After this excursion into what’s happening in a key country in South East Asia let’s return to Australia’s crude oil import problem. The Federal Government belatedly took some action:

Australia’s fuel security package

30 June 2021

The government is committed to securing Australia’s long term refining capacity by building on the fuel security package that was introduced in the 2020-21 Budget. New measures introduced in the 2021-22 Budget include:

- a variable fuel security services payment (FSSP) to pay refineries for the fuel security service that they provide and maintain sovereign capability

- up to $302 million to support infrastructure upgrades at refineries to bring forward the introduction of better fuels from 2027 to 2024

- $50.7 million to design and implement a fuel security framework, to administer the government’s fuel security activities including a minimum stockholding obligation (MSO) and the FSSP.

https://www.energy.gov.au/government-priorities/energy-security/australias-fuel-security-package

The deal involves the 2 remaining refineries Lytton in Brisbane (Caltex/Ampol, 109 kb/d) and Geelong (Viva, 120 kb/d) to remain operational until mid 2027.

Note that Rystad’s forecast for Malaysia looks like a scenario for net zero emissions by 2050, a kind of race between peak oil and action on climate change.

However, we are by no means ready yet to replace e.g. diesel with a carbon free alternative fuel. If, for argument’s sake, we had diesel shortages before 2030, not only would supply chains break down (we had a foretaste of that in the last 2 Covid years) but all vital – and often gigantic – projects to get away from coal fired power would get delayed.

Conclusion: The demise of Australian refineries is part of the peak oil process in a very complex way.

Part 2 of this post:

10/12/2021

Australian fuel import dependencies Sep 2021 data

https://crudeoilpeak.info/australian-fuel-import-dependencies-sep-2021-data

Previous articles:

8/9/2021

Australia’s diesel imports on record high: Update June 2021

https://crudeoilpeak.info/australias-diesel-imports-on-record-high-update-june-2021

12/1/2020

Australia’s oil consumption highly vulnerable to events in the Middle East

http://crudeoilpeak.info/australias-oil-consumption-highly-vulnerable-to-events-in-the-middle-east

2/5/2019

Australian fuel security review ignores peak oil in China 2015 (part3)

http://crudeoilpeak.info/australian-fuel-security-review-ignores-peak-oil-in-china-2015-part-3

10/5/2018

Update on Australian oil import vulnerability May 2018

http://crudeoilpeak.info/update-on-australian-oil-import-vulnerability-may-2018

Appendix

Fig 14: Automotive use of LPG is in decline

Fig 14: Automotive use of LPG is in decline

“The number of LPG registered vehicles has also fallen in the last five years.”

https://www.racq.com.au/living/articles/Wheres-the-LPG