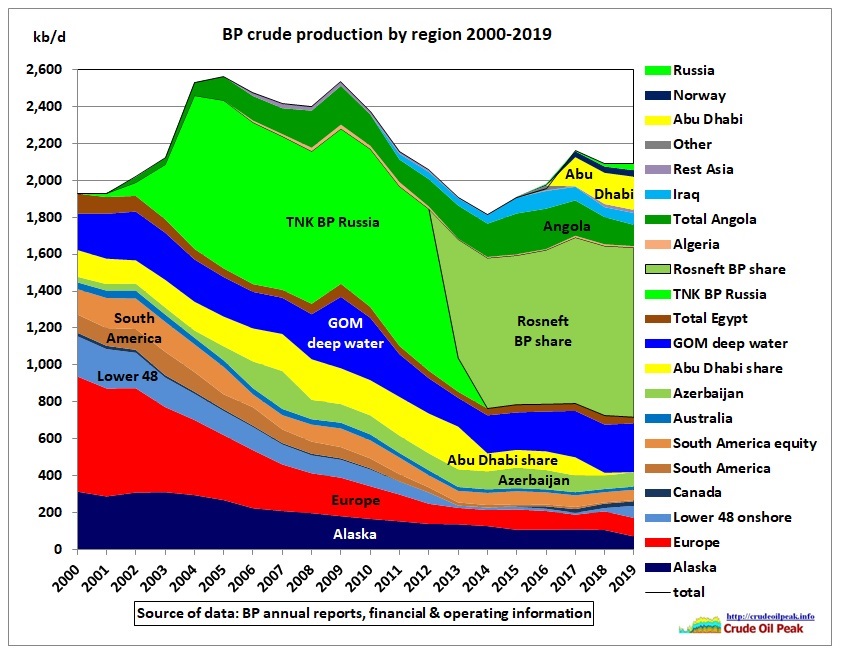

Fig 1: BP is in peak oil mode

Fig 1: BP is in peak oil mode

BP shuts down Kwinana refinery with 600 jobs expected to go, Commonwealth says no impact on fuel security

30 Oct 2020

Fig 2: Kwinana refinery in Perth

Refining activities will wind down over the next six months, with the new [product import] terminal expected to open in 2022.

The Federal Government has expressed disappointment over the refinery closure.

Energy Minister Angus Taylor said …… the Government expected BP to deliver on its commitment to supporting workers during a challenging period, but that closure of the refinery would not impact Australian fuel supplies.

“We will ensure Australia maintains a sovereign refining capability to support local industry, meet our nation’s needs during an emergency, and protect motorists from future higher prices,” he said.

The Minister’s statement seems to be wishful thinking. 3 refineries already closed in the last 8 years

2013 Shell Clyde refinery, 85 kb/d in Sydney

2014 Caltex Kurnell refinery, 125 kb/d in Sydney

2015 BP Bulwer refinery, 102 kb/d in Brisbane

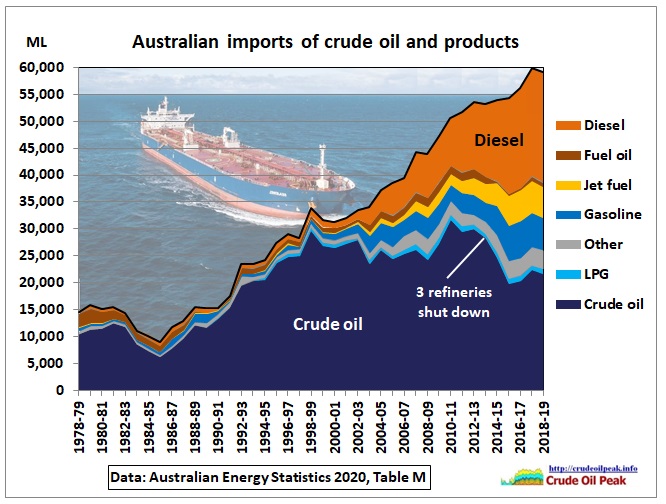

The following graph shows the impact of these previous closures on crude and product imports:

Fig 3: Crude imports dropped and replaced by product imports

Fig 3: Crude imports dropped and replaced by product imports

https://www.energy.gov.au/publications/australian-energy-update-2020

The growth in diesel consumption explains why the government was forced to invest $200 million in a competitive grants program to build an additional 780 ML of onshore diesel storage

Media release 14 Sep 2020

https://www.minister.industry.gov.au/ministers/taylor/media-releases/boosting-australias-fuel-security

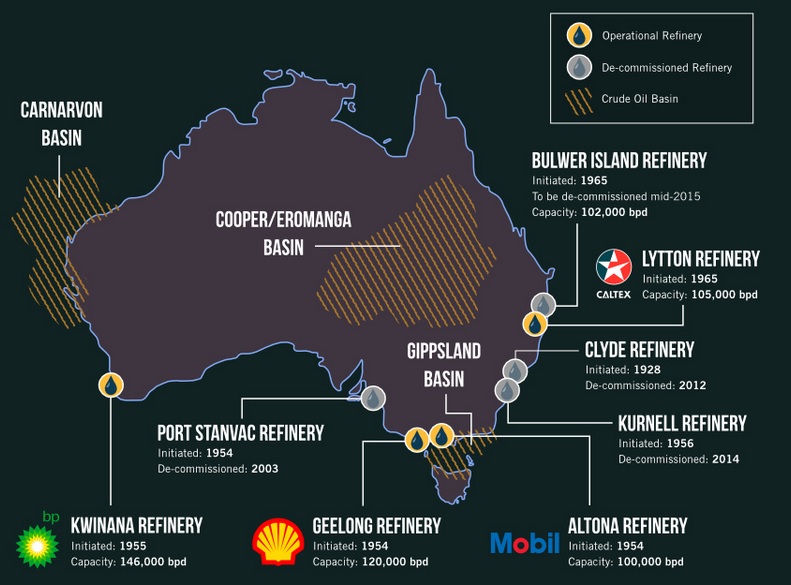

Fig 4: After the Kwinana closure there will be only 3 refineries

Fig 4: After the Kwinana closure there will be only 3 refineries

https://www.festanks.com.au/crude-oil-refining-in-australia-infographic/

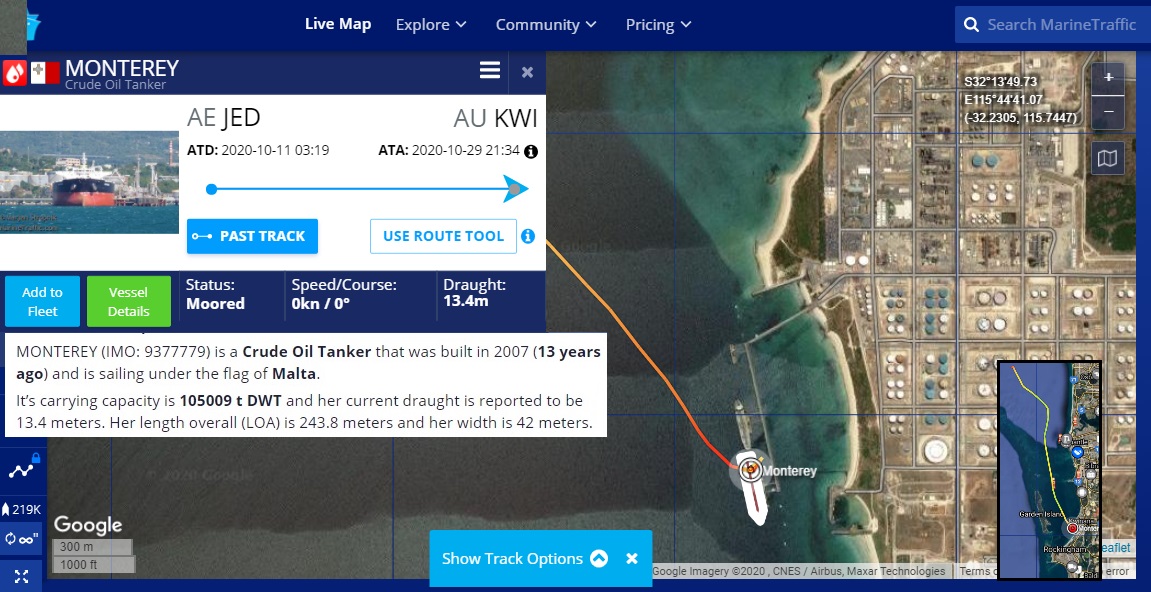

As BP made its announcement a crude oil tanker from UAE was in port.

Fig 5: Crude oil supply from United Arab Emirates (port of Jebel Dhanna)

Fig 5: Crude oil supply from United Arab Emirates (port of Jebel Dhanna)

UAE is an important crude oil source for Australian refineries as shown in this graph:

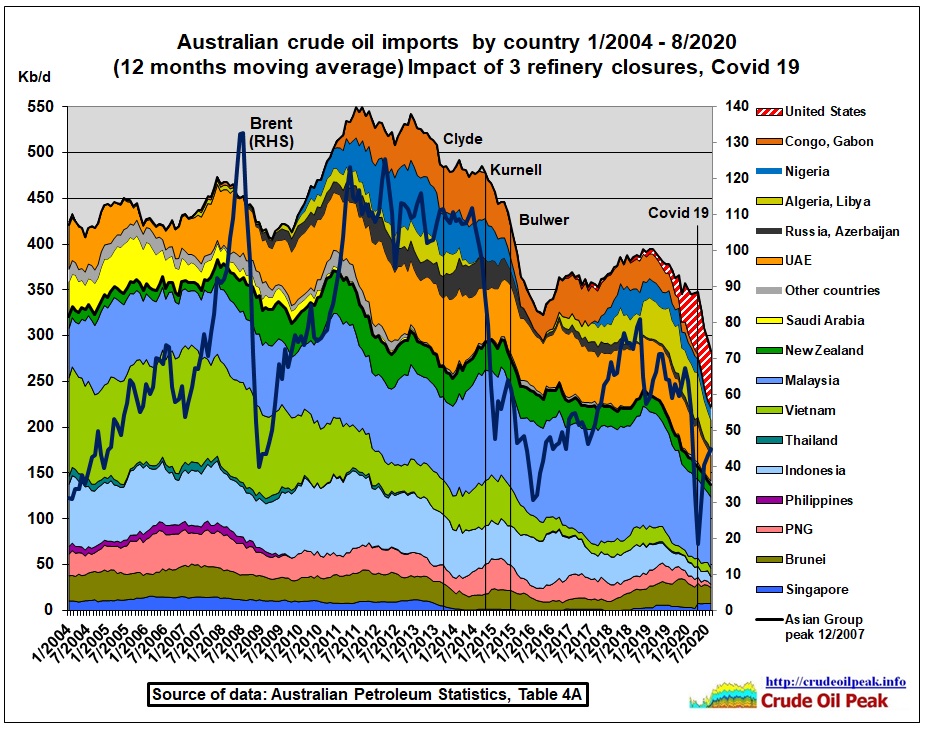

Fig 6: Australian crude imports by country

Fig 6: Australian crude imports by country

Australian crude imports from neighbouring countries peaked in 2007, 7 years after crude oil production in the Asia Pacific outside China peaked in 2000 (see Fig 7). In order to secure growth needed for the mining boom declining imports from Asia were replaced by imports from West Africa (Nigeria, Gabon, Congo) and North Africa (Algeria and Libya). Then 3 refineries shut down between 2013 and 2015, dramatically reducing crude import requirements. In 2019, West African Imports were replaced by imports from the US.

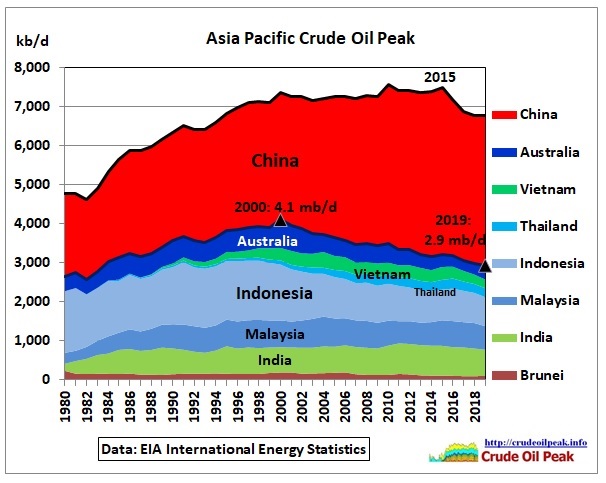

Fig 7: Crude oil peaks in Asia Pacific

Fig 7: Crude oil peaks in Asia Pacific

Asia Pacific crude production since 2000 is down by around 30%, forcing Australian refineries to look for crude from far corners of the world. Australian oil production declined twice as fast as in the rest of Asia.

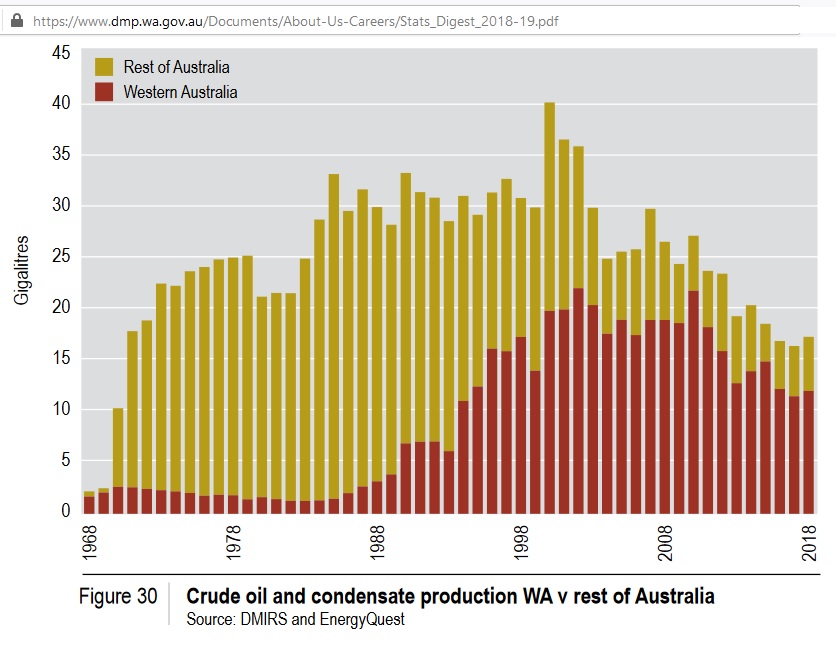

Fig 8: Around 70% of Australia’s crude oil and condensate production comes from the Carnarvon basin in WA (see Fig 4)

Fig 8: Around 70% of Australia’s crude oil and condensate production comes from the Carnarvon basin in WA (see Fig 4)

https://www.dmp.wa.gov.au/Documents/About-Us-Careers/Stats_Digest_2018-19.pdf

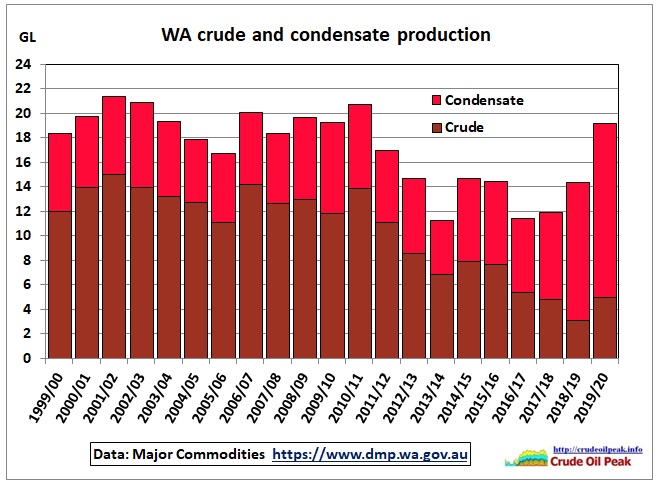

What’s worse, increasing volumes of Australian oil are condensates which Australian refineries can’t process.

Fig 9: Western Australia’s crude and condensate production

Fig 9: Western Australia’s crude and condensate production

https://www.dmp.wa.gov.au/About-Us-Careers/Latest-Statistics-Release-4081.aspx

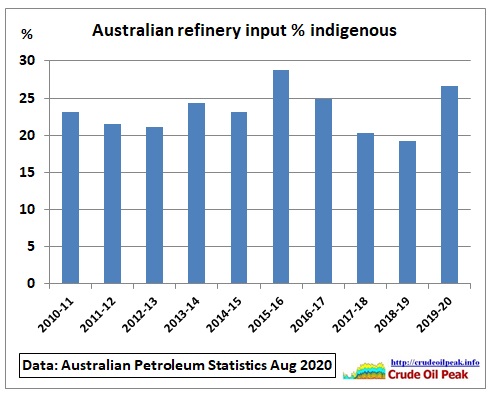

Fig 10: Australian refineries can only process 20-25% of indigenous oil supplies

Fig 10: Australian refineries can only process 20-25% of indigenous oil supplies

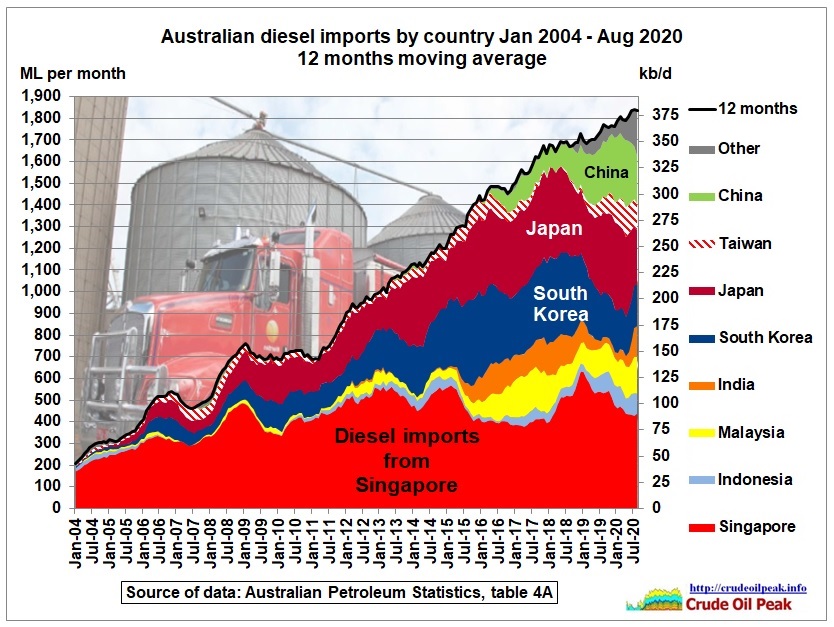

As refineries close, imports of fuels soar:

Fig 11: Diesel imports from South/East Asia

Fig 11: Diesel imports from South/East Asia

The public knows Australia is importing fuels from Singapore, but as refining capacities are limited there, imports increasingly come from East Asia.

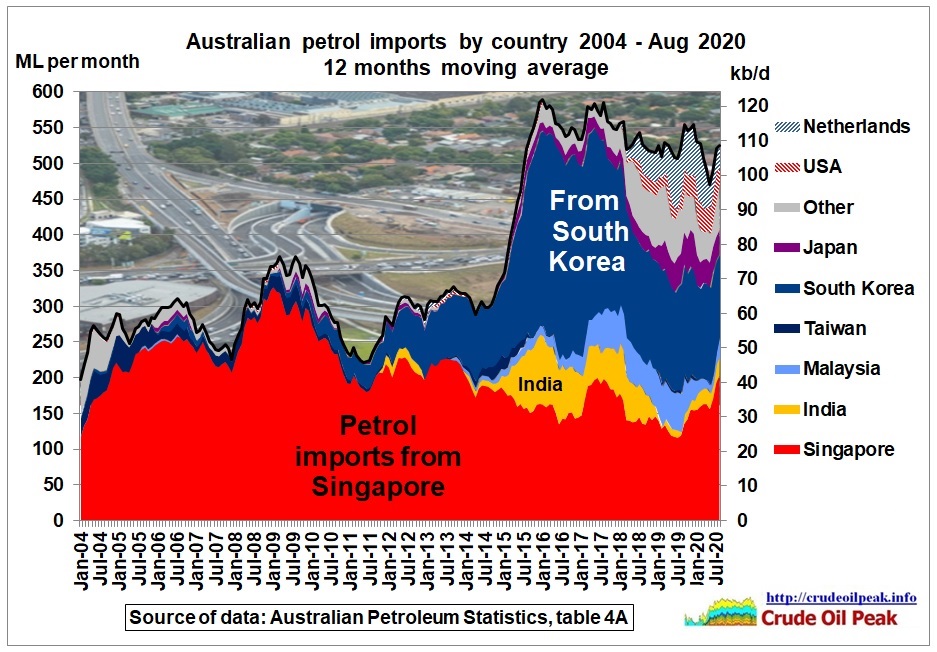

Fig 12: Petrol imports

Fig 12: Petrol imports

In the last 2 years a diversification away from India and South Korea took place, with spot cargos from UK, Belgium, Estonia, Latvia and Lithuania!

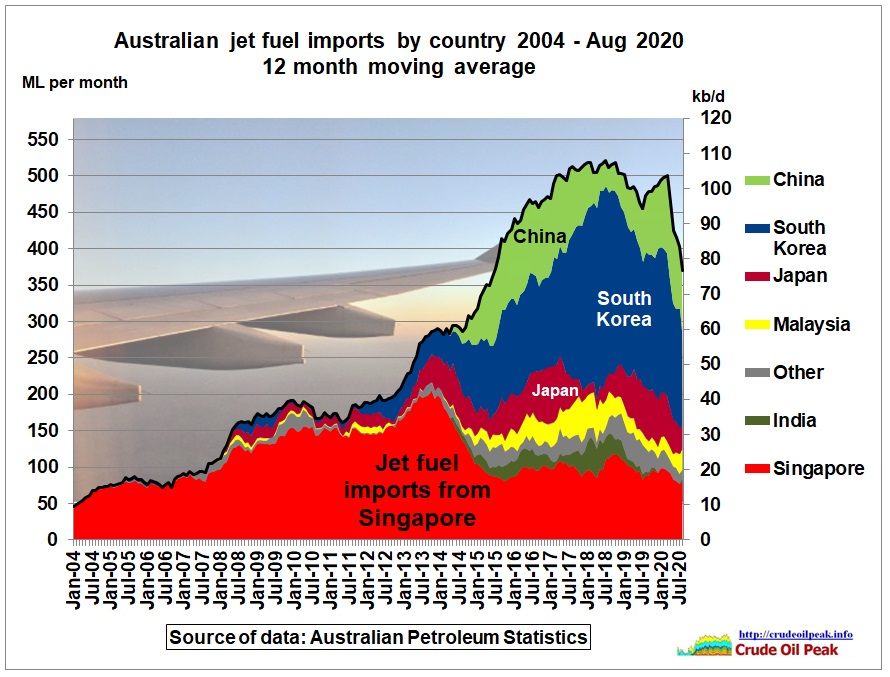

Fig 13: Jet fuel imports dropped when Covid-19 hit

Fig 13: Jet fuel imports dropped when Covid-19 hit

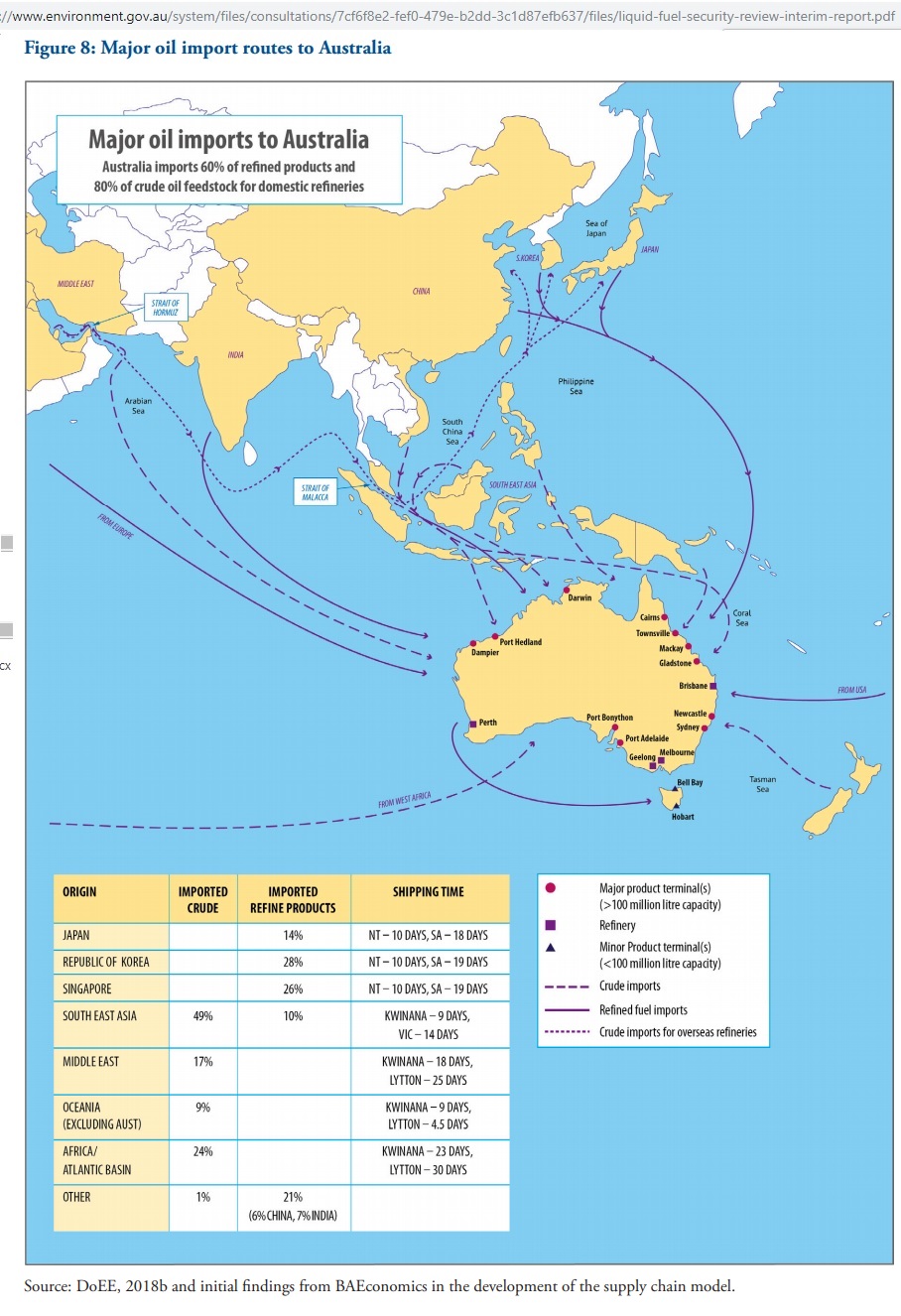

From the Federal Government’s Liquid Fuel Security Review (Interim Report, April 2019):

Fig 14: Oil trading routes critical for Australia

Fig 14: Oil trading routes critical for Australia

https://www.environment.gov.au/system/files/consultations/7cf6f8e2-fef0-479e-b2dd-3c1d87efb637/files/liquid-fuel-security-review-interim-report.pdf

One of the biggest vulnerabilities is the crude oil supply route to Japan and South Korea via the South China Sea.

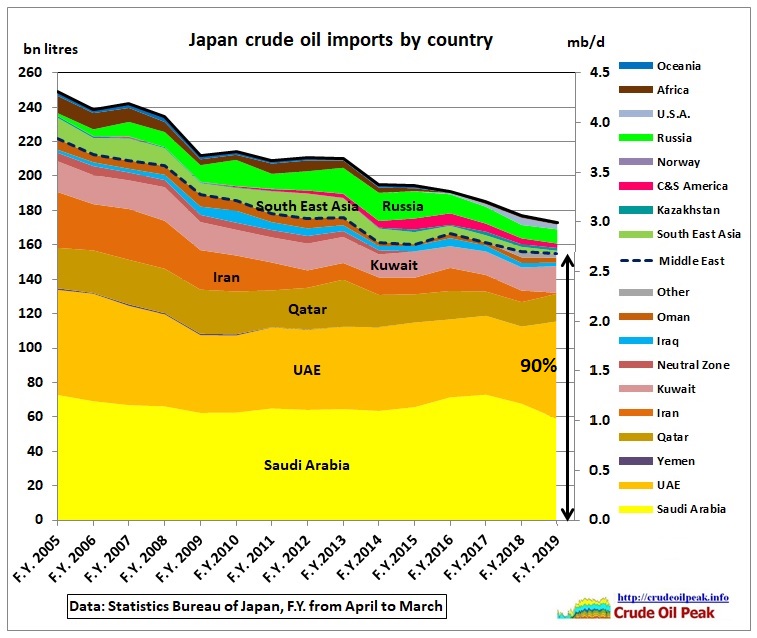

Fig 15: Japanese crude imports by country

Fig 15: Japanese crude imports by country

Japan’s import dependence on the Middle East was 90% in 2019.

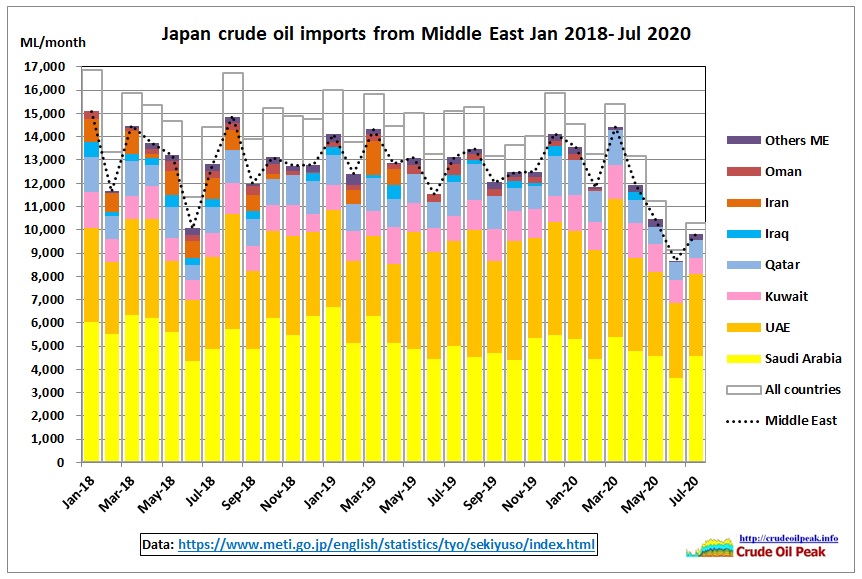

Fig 16: Japanese crude imports from the Middle East (monthly)

Fig 16: Japanese crude imports from the Middle East (monthly)

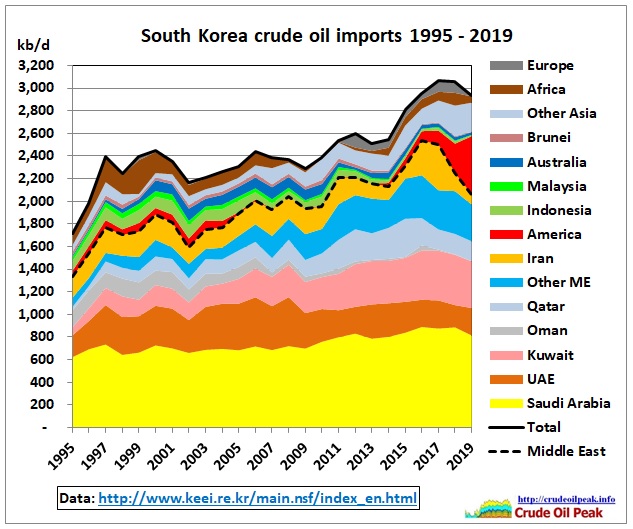

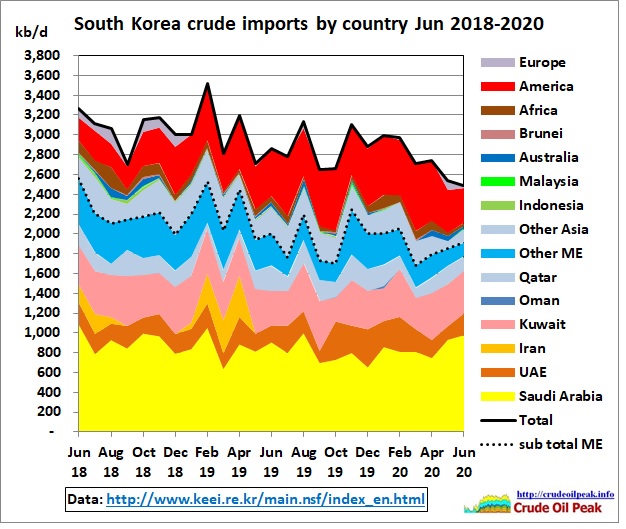

The South Korean data are from the Korea Energy Economics Institute

Fig 17: South Korean crude oil imports

Fig 17: South Korean crude oil imports

http://www.keei.re.kr/main.nsf/index_en.html

Fig 18: South Korea crude imports in last 2 years

Fig 18: South Korea crude imports in last 2 years

Conclusion:

The closure of yet another refinery in Australia is to be seen in the context of an ongoing process of peaking oil production in various countries. The Morrison government has not completed its final report on fuel security but the 2019 interim report is aware of oil/fuel supply vulnerabilities. It mentions the Australian oil production peak but is otherwise shy to analyse the impact of peak oil, especially in Asia and in particular China. It readily accepts IEA’s 2018 assumption that US shale oil production would double by 2025. It quotes international projections of a global oil demand peak by 2030 with a gradual decline starting in 2040 but thinks that Australian demand for liquid fuels in 2040 will be higher than in 2019.

The Corona virus pandemic has of course changed all these projections while peak oil is looming in the background. Federal and State governments have unfortunately embarked on highly oil vulnerable projects like the 2nd Sydney airport plus associated infrastructure and more road tunnels without a proper fuel supply analysis. There is no detailed fuel transition program in place with committed volumetric targets, timelines and budgets to replace Australia’s consumption of around 1 million barrels/day. A technology road map is not enough. That should have started with Howard’s 2004 energy white paper but he thought it unnecessary at the time, 1 year after the war in Iraq designed to stop the 1st crude oil peak in 2005 which happened anyway as predicted and caused the financial crisis in 2009. A decade later Howard’s scholars are (still) in government right now and suffer from the consequences of his failures. It is high time Australian governments face reality and stop new, fuel hungry projects. As refineries close, the writing is on the wall.

Update

10 March 2021

“Oil refining activities have now ceased and fuel imports have started,” BP said. “All processing at the plant is in the shutdown phase, which will be completed by the end of March 2021.” There will be no impact to the supply of fuel products, the company said.

The Kwinana refinery relied almost totally on imported crude. Seaborne crude deliveries to Kwinana averaged 132,000 b/d between the start of 2018 and late October last year, when BP announced the plan to close the refinery, according to Vortexa data. The majority of this comprised 47,000 b/d of light sour Murban crude from Abu Dhabi, 42,000 b/d of light sweet Malaysian grades — mainly Kimanis and Bunga Orkid — and 21,000 b/d of US light sweet WTI.

Crude imports fell to 104,000 b/d in November-January. A 240,000 bl cargo of Abu Dhabi Murban crude discharged on 1 February and no crude has been delivered since then.

Combined imports of gasoline, diesel and jet fuel to Kwinana surged to a record 46,000 b/d in February, up from less than 2,000 b/d a year earlier and an average of 17,000 b/d over the previous three months, the Vortexa data show.

https://www.argusmedia.com/en/news/2194471-bp-to-close-australia-kwinana-refinery-in-march-update

Previous posts:

13/4/2011

Australia’s fuel import vulnerability increases as Sydney’s Clyde refinery is closing

http://crudeoilpeak.info/australias-fuel-import-vulnerability-increases-as-sydneys-clyde-refinery-is-closing

9/4/2014

Why the closure of BP’s Brisbane Bulwer refinery reduces Australia’s energy security

http://crudeoilpeak.info/why-the-closure-of-bps-brisbane-bulwer-refinery-reduces-australias-energy-security

Related posts:

30/6/2020

Peak oil in Asia Update June 2020 (part 1)

https://crudeoilpeak.info/peak-oil-in-asia-update-june-2020-part-1

15/7/2020

Peak oil in Asia Update June 2020 (part 2)

https://crudeoilpeak.info/peak-oil-in-asia-update-june-2020-part-2

17/8/2020

Peak oil in Asia Update June 2020 (part 3)

https://crudeoilpeak.info/peak-oil-in-asia-update-june-2020-part-3

10/9/2020

Peak oil in Asia Update June 2020 (part 4)

https://crudeoilpeak.info/peak-oil-in-asia-update-june-2020-part-4

Quoted post:

8/11/2004

Critique of Energy White Paper June 2004

http://crudeoilpeak.info/critique-of-energy-white-paper-june-2004