This is part 2 of the post from 19 March

https://crudeoilpeak.info/where-does-australia-get-its-diesel-from-update-january-2026

In many previous posts on Australia’s oil import vulnerability this website has used monthly data from The Australian Petroleum Statistics (APS)

https://www.energy.gov.au/publications/australian-petroleum-statistics-2026

But now the Department of Climate Change, Energy and the Environment has come into the foreground by publishing weekly updates on Minimum Stockholding Obligations for fuels.

More fuel for regional Australians

13 March 2026

The Albanese Government will help to address fuel supply chain disruption by releasing up to 20 per cent of the baseline Minimum Stockholding Obligation [MSO] for petrol and diesel.

This will allow the release of up to 762 million litres of petrol and diesel from Australia’s domestic reserves, where these can be targeted towards localised market disruption. This will take time to move through Australia’s long and complex supply chain from where fuel is held to the regional areas where it’s needed.

Relaxing the MSO will also serve as a contribution to the International Energy Agency’s global collective action. This temporary reduction in the MSO could be equivalent to up to 5 million [=790 ML] barrels.

https://minister.dcceew.gov.au/bowen/media-releases/more-fuel-regional-australians

These are the numbers:

Diesel MSO 2,742 ML x 20% = 548.4 ML; revised MSO 2,200 ML (rounded)

Petrol MSO 1,067ML x 20% = 213.4 ML; revised MSO 700 ML (rounded)

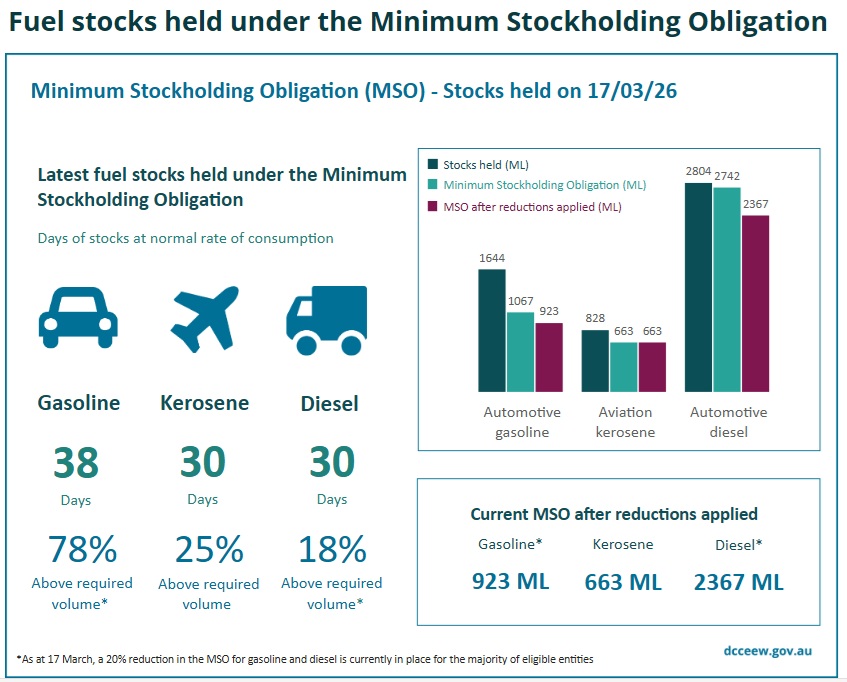

Fig 1: Stockholding snapshot 17 March 2026

Fig 1: Stockholding snapshot 17 March 2026

Apparently, the reductions have not been fully applied yet. The above graph is the 3rd in a series (3rd,10th,17th) so let’s put this into a time series graph:

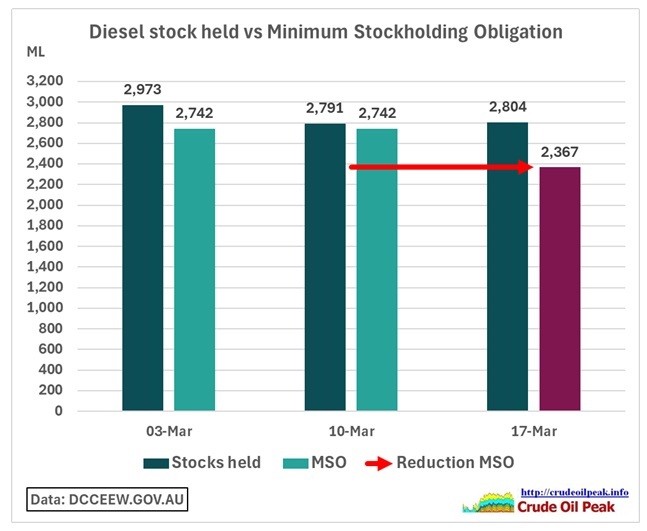

Fig 2: Comparison MSO for the last 3 weeks

Diesel stocks held decreased in one week by 182 ML (6%) to 2,791 ML on 10/3/26. Since then they remained practically on the same level (2,804 ML on 17/3/26). These numbers will change from week to week. MSO days have slipped by 2 days. The reduction to 2,367 ML comes pretty close to the January 2026 stock of 2,407 ML reported in the APS (see Fig 4 below)

The Minister points out that the MSO reduction is NOT to be considered as a liquid fuels emergency:

13 March 2026

MINISTER FOR CLIMATE CHANGE AND ENERGY, CHRIS BOWEN:

….

JOURNALIST: Do we have the power to ration fuel?

BOWEN: Look, I have a lot of powers under the Fuel Emergency Act. States have various powers. They’re not being contemplated at this point.

What we don’t have is the power, as the Act is constituted and the rule determined by my predecessor Angus Taylor, to prioritise fuel for farmers over others.

https://minister.dcceew.gov.au/bowen/transcripts/press-conference-sydney-nsw-6

How can we verify these “stocks held” numbers? We find the Australian Petroleum Statistics which have been extensively used on this website have different data. This is because APS reports stocks on land and domestic waters while MSO data include all tankers in the EEZ. It is debatable whether it is wise by DCCEEW to include the EEZ because tankers can be diverted from this zone by the highest bidder. In practice that might happen on the northern approached to Australia.

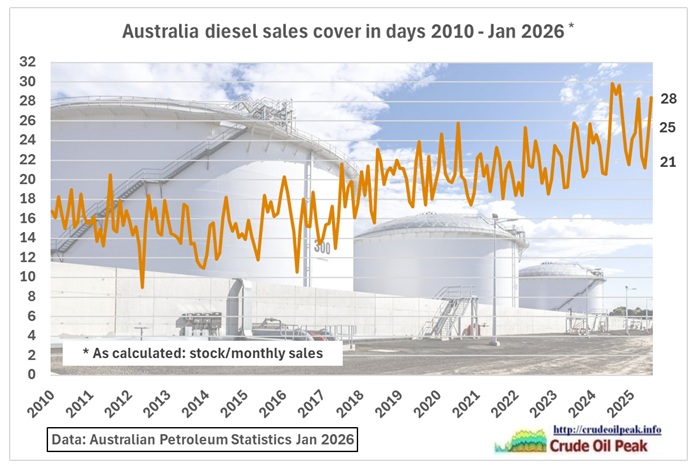

Fig 3: Diesel sales were on an upward path since 2010

Fig 3: Diesel sales were on an upward path since 2010

The trendline reached monthly sales of 2,860 ML in Jan 2026. The increase over the last 15 years was around 70 ML pa. (2.4%). The daily sales are around 2,860/30.4 = 95 ML/day. This means that the stock loss reported on 10th March (Fig 2) was equivalent to 2 days of sales.

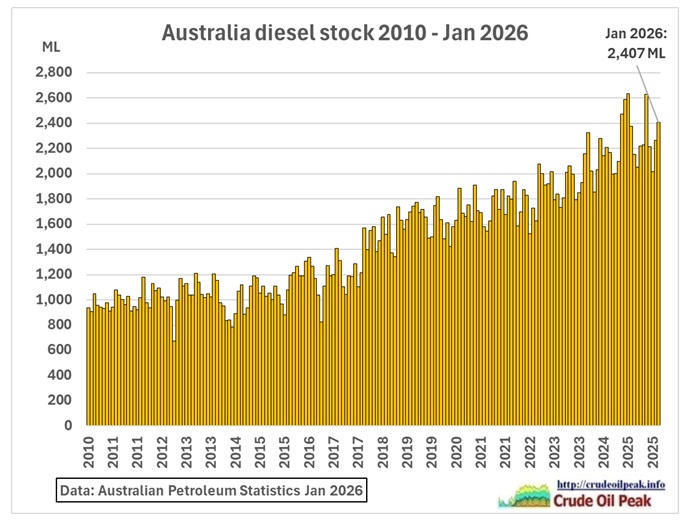

Fig 4: Diesel stock 2010 – Jan 2026

Diesel stocks have equally increased. Just like with sales, there is quite some variability in stocks. The average in the last year was 2,300 ML plus/minus up to 300 ML.

Please note: stocks held in the following locations: domestic refineries, import terminals, major marketing and bulk terminals, marine bunkering facilities, major airports, on-site at major users (e.g. mining), onboard vessels in Australian waters (domestic coastal shipping only but not the entire EEZ).

https://www.energy.gov.au/sites/default/files/2022-12/stockholding_guidance_note_v2.docx

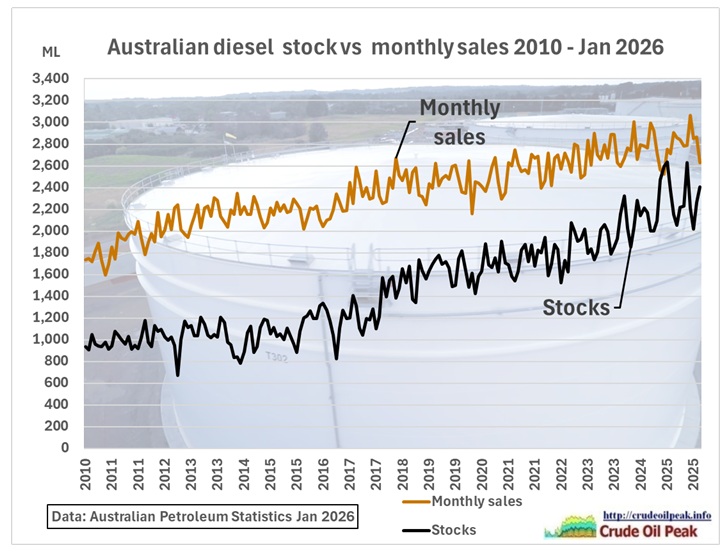

Let’s compare sales and stocks in one graph:

Fig 5: Australian diesel stock vs monthly sales

We can see that stocks are approaching 1 month of sales. Dividing stocks at the end of the month by monthly sales and multiplying by number of days in a month gives us the cover in days in that month:

Fig 6: Diesel sales cover in days

Fig 6: Diesel sales cover in days

As we can see there can be quite some differences of several days from month to month.

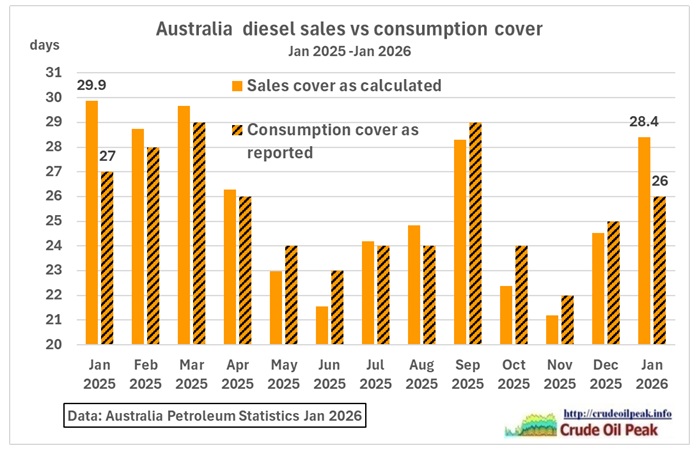

APS also has in the sheet “consumption cover” a column “diesel oil (days)”. On average, there is not much difference (0.2 days) but it can be 2 days.

Fig 7: Diesel sales cover vs consumption cover

Fig 7: Diesel sales cover vs consumption cover

Calculated sales cover and reported consumption cover are different from month to month

Stock on land and in water:

There was a question in Parliament on 2/3/26 “how much diesel in days do we currently have in store on Australian soil?” The Energy Minister’s answer was 34 days, the highest in 15 years.

https://www.aph.gov.au/Parliamentary_Business/Hansard/Hansard_Display?bid=chamber/hansardr/29140/&sid=0025

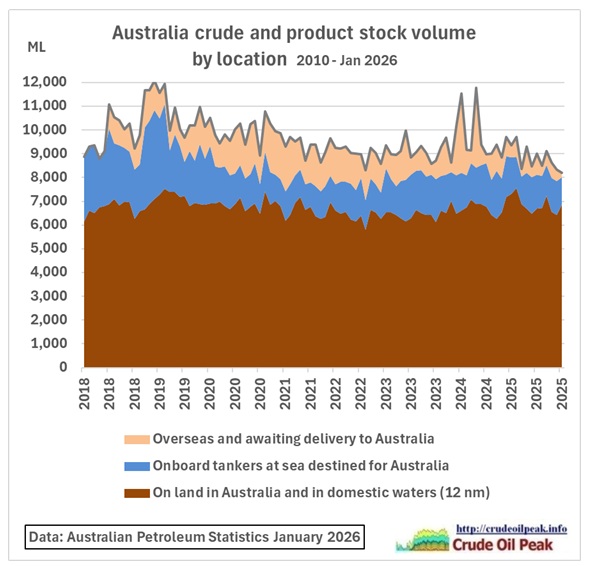

The Australian Petroleum Statistics usually cover stocks on land and in domestic waters (approaching Australian ports). In their XLS files there is one sheet “stock volumes incl. on the way” which also includes stocks outside domestic waters e.g. in the EEZ which the DCCEEW is using for their minimum stockholding calculations. Unfortunately, these data are not available by fuel.

Fig 8: Australian crude and product stocks by location

Fig 8: Australian crude and product stocks by location

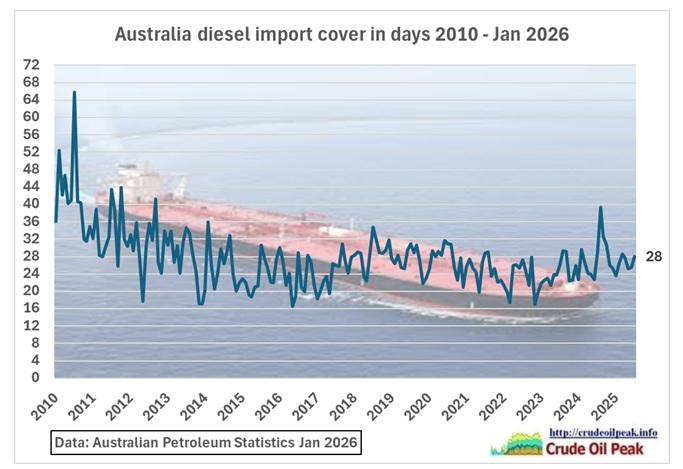

We can also divide stocks by monthly imports and get this graph:

Fig 9: Diesel import cover

Fig 9: Diesel import cover

We can see that the diesel import cover is also lower than 1 month.

MSO requirements were introduced by the Morrison Government in June 2021 but implemented by the Albanese Government in July 2023

The Fuel Security Bill 2021 gives effect to key measures in the Government’s comprehensive fuel security package included in the 2021-22 Budget.

The reforms will:

establish a minimum stockholding obligation (MSO) requiring fuel importers and refiners to maintain a level of petrol, diesel and jet fuel; and

create a fuel security services payment (FSSP) to support refiners during loss-making periods and enable them to continue refining until 30 June 2027.

https://www.minister.industry.gov.au/ministers/taylor/media-releases/delivering-fuel-security-and-protecting-jobs

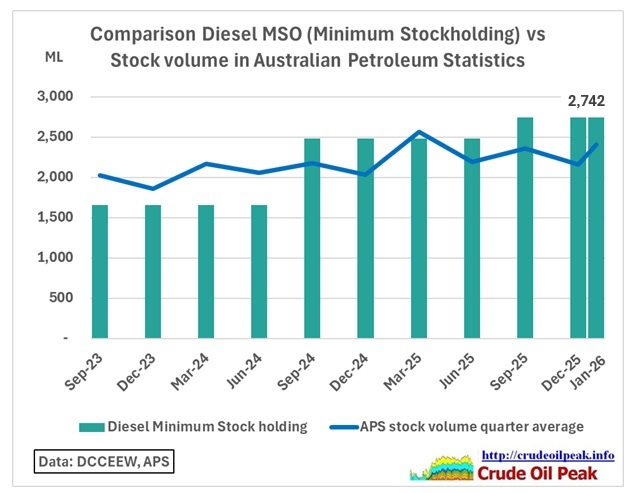

Let’s compare MSO requirements with what we have used so far in the Australian Petroleum Statistics:

Fig 10: Comparison MSO data with APS stock data

Fig 10: Comparison MSO data with APS stock data

MSO data are from here:

https://www.dcceew.gov.au/energy/security/australias-fuel-security/minimum-stockholding-obligation/statistics#download

We can see that MSO requirements were first set to be under the APS stock volumes. In July 2024 the requirements were increased and the industry apparently struggled to adapt. In July 2025 the MSO was again increased to the level in force when the Iran war crisis started (2,742 ML). The MSO data are now higher because they include tankers in Australia’s EEZ.

In the next post we’ll look at whether sales volumes can be used to verify stock levels.