http://www.naturalgasintel.com/topics/101-fayetteville-shale

http://www.naturalgasintel.com/topics/101-fayetteville-shale

We had these headlines a couple of months ago:

BHP’s $50 billion shale oil blunder

23/8/2017

BHP slapped $US4.75 billion ($6 billion) down on the table to buy the rights from Chesapeake Energy to around half-a-million acres of prospective shale gas reserves at Lafayette in Arkansas.

http://www.abc.net.au/news/2017-08-23/bhp-billion-dollar-shale-oil-blunder/8832698

‘They went too hard’ – BHP’s retreat wins plaudits

22/8/2017

Mr Mackenzie conceded BHP’s entry into the onshore US shale industry was “poorly timed, we paid too much” for the assets.

“We would like to get on with the exit from shale,” he said, adding that BHP would “be patient to make sure we restore value for shareholders”.

http://www.smh.com.au/business/mining-and-resources/they-went-too-hard–bhps-retreat-wins-plaudits-20170822-gy1jfq.html

This post’s focus is the Fayetteville shale gas in the US State of Arkansas. The following map is from a BHP investor presentation in February 2011, shortly before BHP bought shale gas acreage from Chesapeake in March 2011.

Fig 1: Location of the Fayetteville shale

Fig 1: Location of the Fayetteville shale

Let’s hit the road, on route 65 from Conway (Arkansas) towards Greenbrier where many new subdivisions were built like this one:

Fig 2: Testifying to the newly found wealth – as long as it lasts.

Fig 2: Testifying to the newly found wealth – as long as it lasts.

You can buy 5 acre lots for US$ 80,000 and the average house costs just 140 grand.

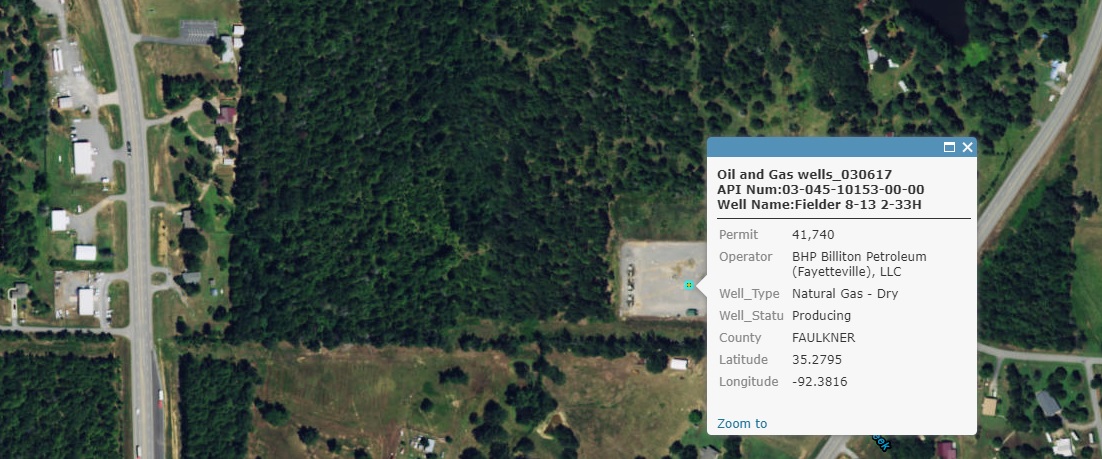

5 kms north of Greenbrier we find BHP gas well Fielder 8-13 2-33H, carved out of a forest lot.

Fig 3: BHP gas wells in Fayetteville

Fig 3: BHP gas wells in Fayetteville

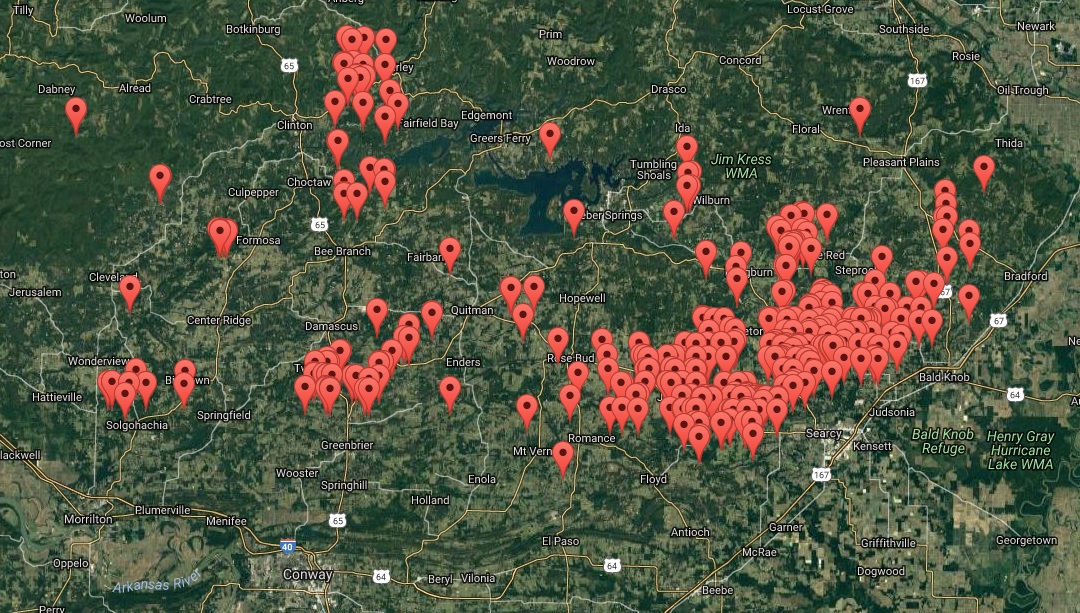

Fig 4: BHP well locations in Fayetteville

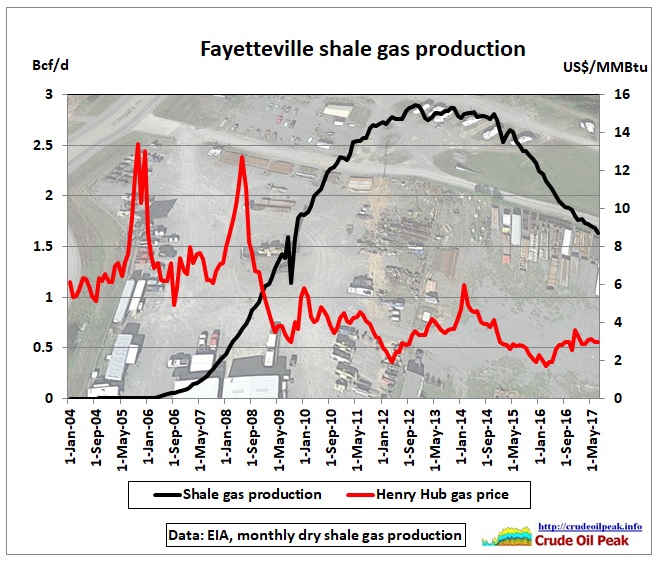

The production history shows that BHP went into shale just 1 ½ years before the whole basin started to peak:

Fig 5: Fayetteville shale gas production up to July 2017

Fig 5: Fayetteville shale gas production up to July 2017

https://www.eia.gov/tools/faqs/faq.php?id=907&t=8

An undulating peak of production is clearly visible between mid 2012 and mid 2014

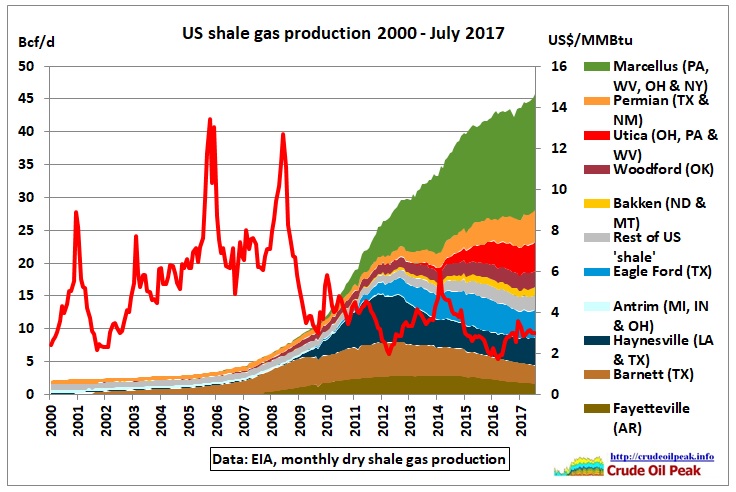

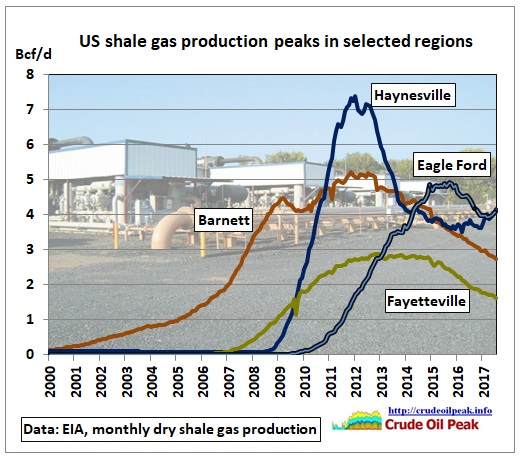

How does Fayetteville fit into the whole US picture?

Fig 6: US shale gas production by region

Fig 6: US shale gas production by region

Following 4 regions have peaked: Haynesville (Jan 2012), Barnett (Nov 2011), Eagle Ford (Sep 2015) and Fayetteville (Nov 2012). Their common peak was in Aug 2012, with 17.3 Bcf/d. In July 2017 their production was 12.7 Bcf/d, 27% lower over 5 years.

Fig 7: Shale gas production history in 4 peaking regions

Fig 7: Shale gas production history in 4 peaking regions

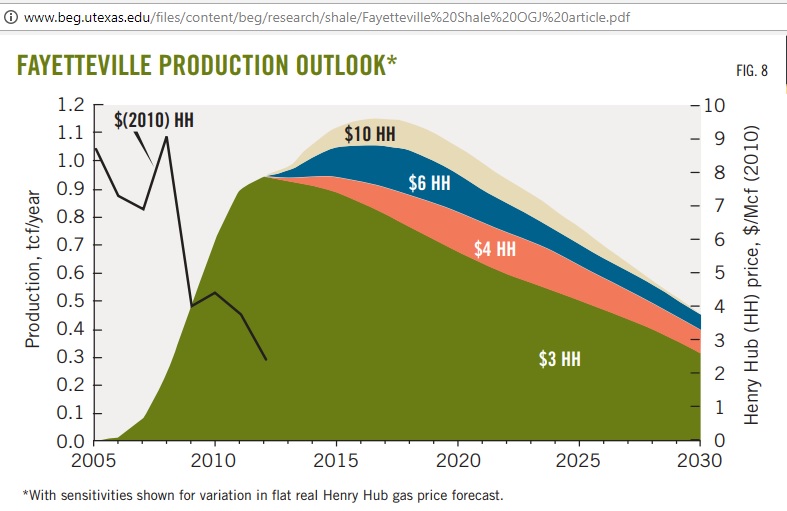

Is the Fayetteville peak a result of low gas prices? The following graph shows that even with higher gas prices, there would have been a peak:

Fig 8: Fayetteville gas production as function of gas price

Fig 8: Fayetteville gas production as function of gas price

The above graph is from a 2014 article in the Oil and Gas Journal by the Bureau of Geologic Economy (BEG) in the University of Texas using data up to 2011 (which should have been also available to BHP at the time)

“In the environment of a $4/Mcf natural gas price at Henry Hub, production reaches a plateau in 2012-2015 abd begins a gradual decline as annual well count decreases as a function of limited higher quality drilling locations.

These better locations in Tiers 1 through 3 are developed and the lower tiers do not justify development at this price. The outlook yields a full-field EUR of 18.2 tcf, which includes the 6.1 tcf expected from 3,689 wells drilled through 2011.

The production outlook and resulting EUR are only moderately sensitive to natural gas price. Higher prices will extend the buildup and plateau period. Natural gas price is only one fo the variables considered. We developed high and low cases around the base to capture the impact of other key variables.”

http://www.beg.utexas.edu/files/content/beg/research/shale/Fayetteville%20Shale%20OGJ%20article.pdf

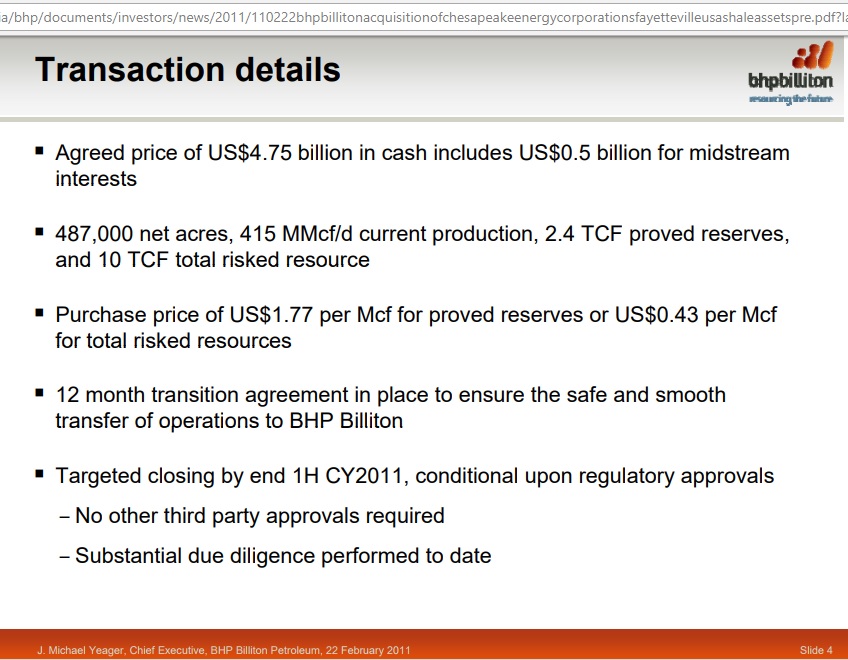

How did BHP present its Fayetteville acquisition in 2011 to shareholders? These are the transaction details: Fig 9: Slide 4

Fig 9: Slide 4

The proved reserve to production ratio would be 2,400 Bcf / (415 MMcf/d x 365) = 16 years

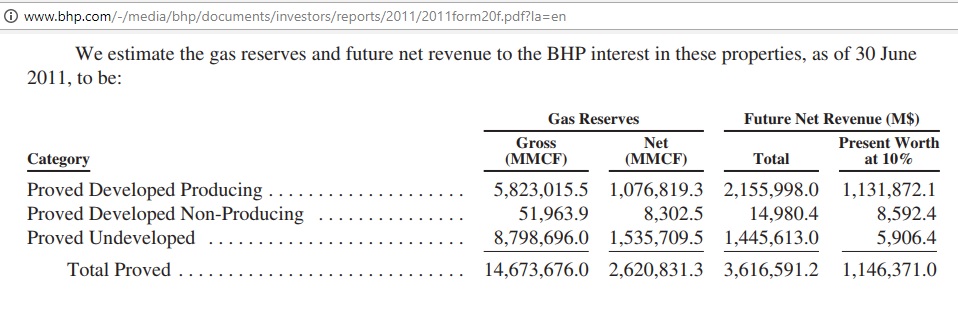

In BHP’s 2011 20F form to the SEC (p 103) proved developed and undeveloped reserves as at June 2011 were given as 415 MMboe implying a reasonable conversion factor of 5.78 Mcf per barrel of oil.

The estimate was done by Netherland Sewell & Associates, Inc. (NSAI), exhibit 99.2 (p 565). Note that in the following table the reserves are actually higher (2.6 tcf)

Fig 10: Sewell’s reserve table

Fig 10: Sewell’s reserve table

“The estimates shown in this report are for proved reserves. No study was made to determine whether probable or possible reserves might be established for these properties. Proved undeveloped locations in this report are based on BHP’s planned drilling program of operating eight rigs for five years for the operated properties and the expectation that historical drilling rates will be maintained for non-operated properties for four years. Estimates of proved undeveloped reserves have been included for certain locations that generate positive future net revenue but have negative present worth discounted at 10 percent based on the constant prices and costs discussed in subsequent paragraphs of this letter. These locations have been included based on the operators’ declared intent to drill these wells, as evidenced by BHP’s internal budget, reserves estimates, and price forecast. This report does not include any value that could be attributed to interests in undeveloped acreage beyond those tracts for which undeveloped reserves have been estimated. Reserves categorisation conveys the relative degree of certainty; reserves subcategorization is based on development and production status. The estimates of reserves and future revenue included herein have not been adjusted for risk.

…….

For the purposes of this report, we did not perform any field inspection of the properties, nor did we examine the mechanical operation or condition of the wells and facilities

……

The average price of $4.21 per MMBTU is adjusted for energy content, transportation fees, and a regional price differential of $0.07 per MCF. The adjusted gas price of $3.01 per MCF is held constant throughout the lives of the properties.

……

our estimates are based on…..and that our projections of future production will prove consistent with actual performance”

http://www.bhp.com/-/media/bhp/documents/investors/reports/2011/2011form20f.pdf?la=en

(Underline by author)

Chesapeake’s documentation before the transaction

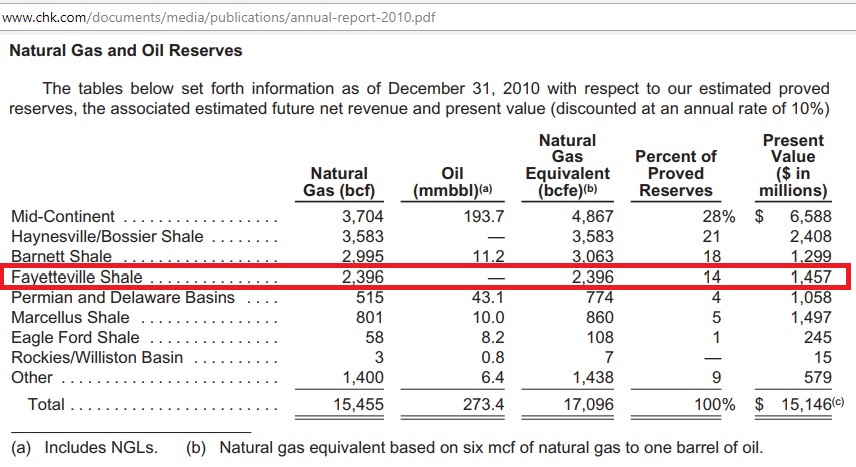

So let’s have a look at what Chesapeake presented to investors:

Fig 11: Chesapeake’s proved reserves in December 2010

http://www.chk.com/documents/media/publications/annual-report-2010.pdf

It is interesting to note that Sewell also participated by 58% in preparing Fayetteville’s reserves for Chesapeake, so BHP did not really independently assess the reserves.

As for the 10 Tcf resources given in the above BHP slide 4 they should actually be in the Chesapeake annual report 2010 for 31 Dec but this document contained only the proved reserves per SEC rules.

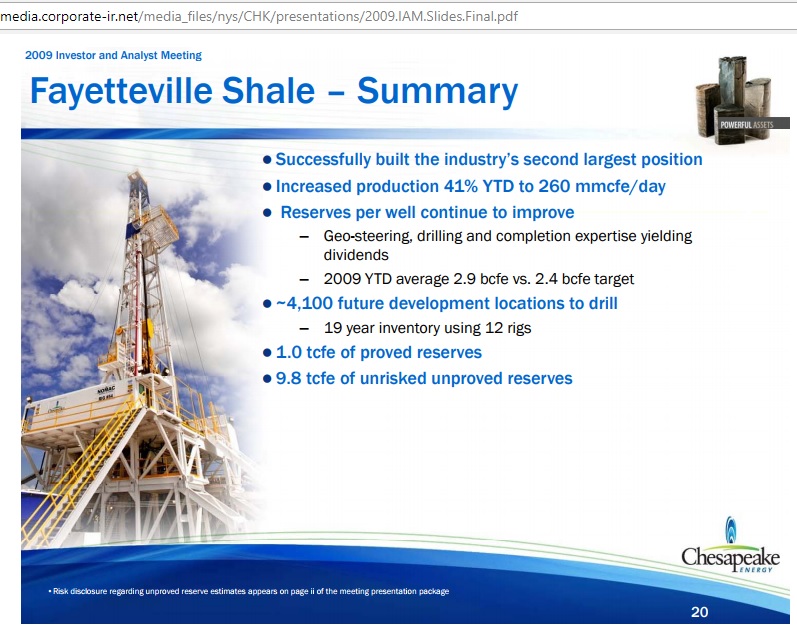

Maybe the number was taken and rounded from Chesapeake’s October 2009 Institutional Investor and Analyst Meeting presentation, slide 20 (9.8 tcfe)

Fig 12: Chesapeake investor presentation Oct 2009

Fig 12: Chesapeake investor presentation Oct 2009

Note that in October 2009 proved reserves were shown as only1 tcf.

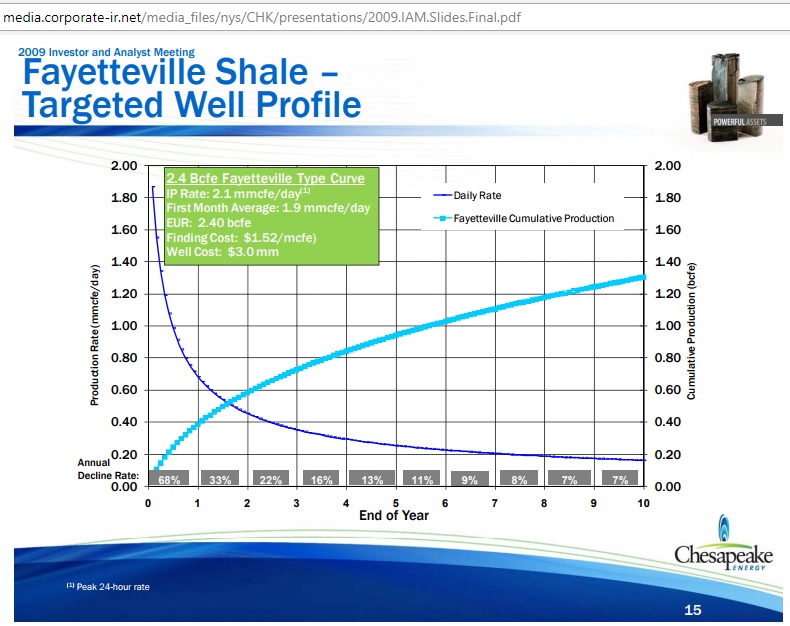

The 9.8 tcfe resource and 4,100 new wells would need an Estimated Ultimate Recovery (EUR) of 2.4 bcfe per well as shown in slide 15

Fig 13: Assumed EUR 2.4 bcfe per well

Fig 13: Assumed EUR 2.4 bcfe per well

http://media.corporate-ir.net/media_files/nys/CHK/presentations/2009.IAM.Slides.Final.pdf

Early warnings

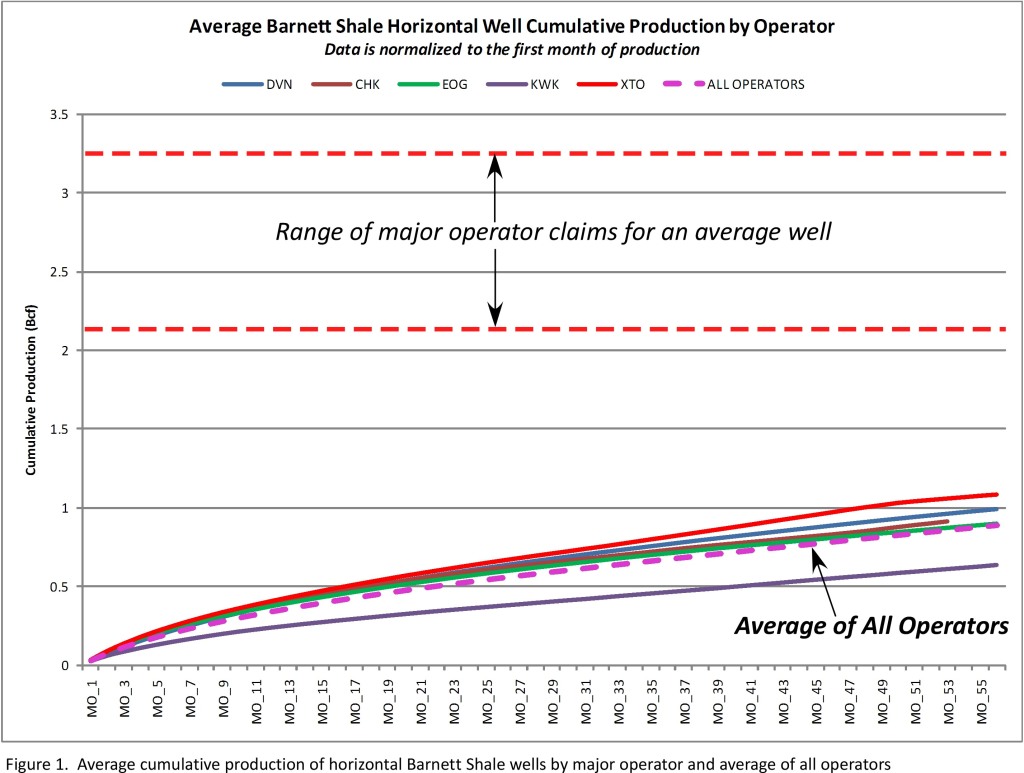

Chesapeake claimed 2.65 bcfe per well in the Barnett shale in the above presentation (slide 10) but in the same year Art Berman, an oil geologist from Houston, published his research on decline rates in shale gas fields: “Facts are stubborn things” on 5/11/2009

Fig 14: Art Berman’s EUR (Estimated Ultimate Recovery) in 2009

Fig 14: Art Berman’s EUR (Estimated Ultimate Recovery) in 2009

“Major operators claim that their average Barnett EUR will reach 2.2-3.3 Bcf/well. Figure 1 shows that those levels of EUR are unlikely to occur in an economically meaningful timeframe based on cumulative production to date.”

http://peak-oil.org/facts-are-stubborn-things-arthur-e-berman-november-2009/

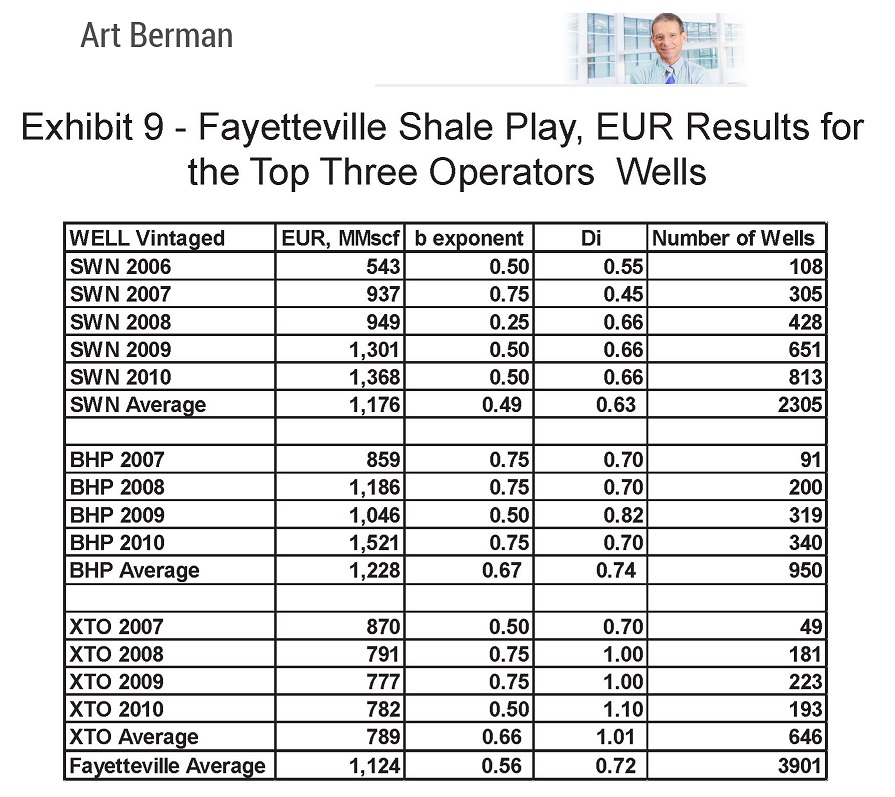

No one listened. In August 2011, a couple of months after BHP acquired Fayetteville from Chesapeake, Art published another analysis “U.S. Shale Gas: Less Abundance, Higher Cost“ in the Oildrum blog. He found that most operators use a single hyperbolic curvature for their production profiles, resulting in low decline rates in later years (up to 50 years) and therefore high EURs. While observations show that decline follows a 2-stage exponential decline with a well life of 12 years and lower EURs.

Fig 15: Timeline of EURs for South Western Energy, BHP and XTO Energy

Fig 15: Timeline of EURs for South Western Energy, BHP and XTO Energy

“Our analysis of shale gas well decline trends indicates that the estimated ultimate recovery (EUR) per well is approximately one-half of the values commonly presented by operators. The average EUR per well for the most active operators is 1.3 Bcf in the Barnett, 1.1 Bcf in the Fayetteville, and 3.0 Bcf in the Haynesville shale gas plays.”

http://www.theoildrum.com/node/8212

Production

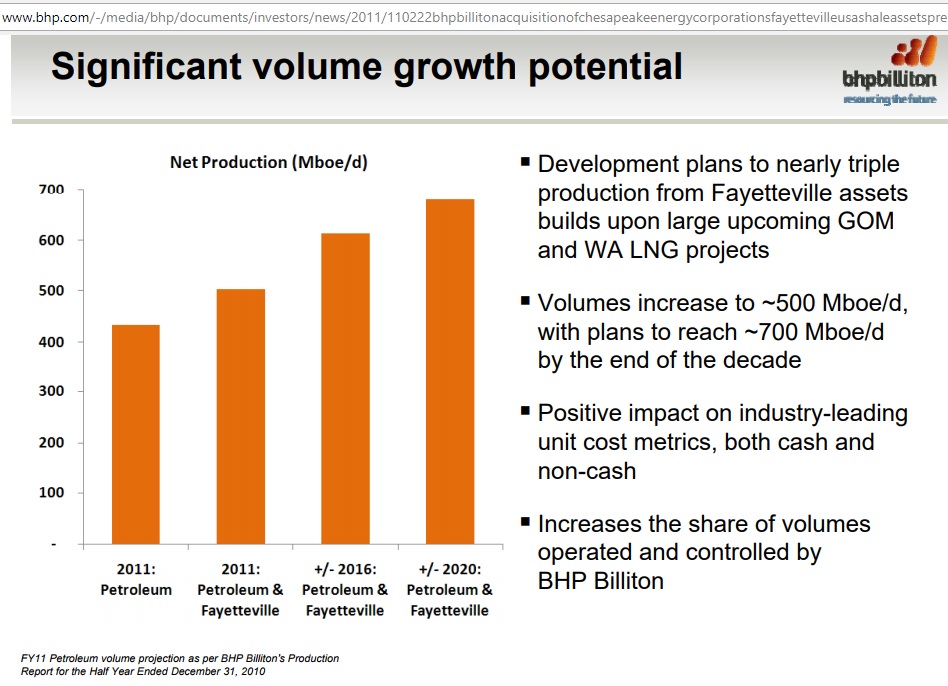

In February 2011, 1 month before the acquisition, BHP promised a tripling of production from Fayetteville:

Fig 16: BHP investor presentation in 2011 on future production volumes

Fig 16: BHP investor presentation in 2011 on future production volumes

http://www.bhp.com/-/media/bhp/documents/investors/news/2011/110222bhpbillitonacquisitionofchesapeakeenergycorporationsfayettevilleusashaleassetspre.pdf

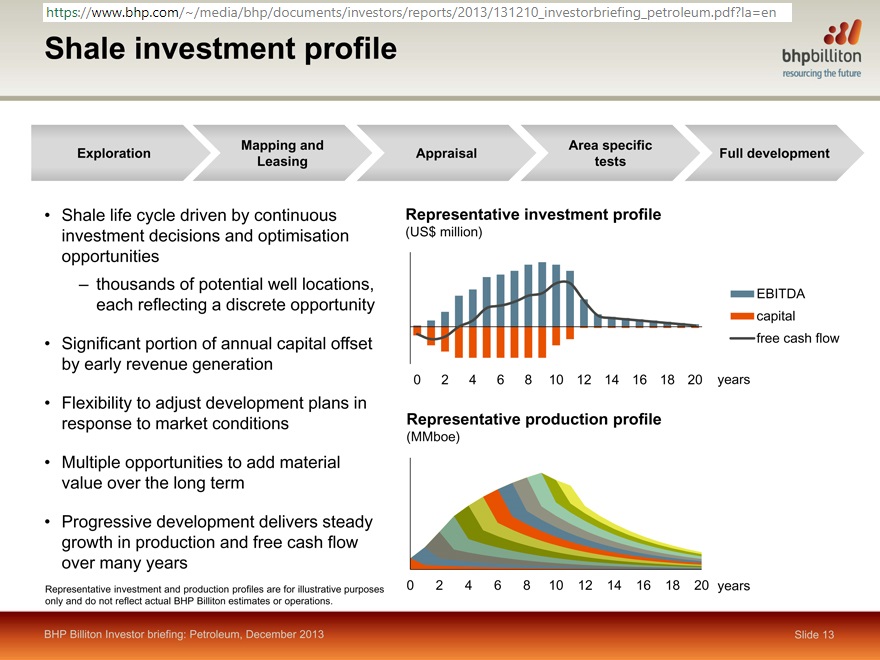

2 years later, in December 2013, BHP showed a typical shale investment and production profile.

Fig 17: Decline of shale after 10 years

Fig 17: Decline of shale after 10 years

https://www.bhp.com/~/media/bhp/documents/investors/reports/2013/131210_investorbriefing_petroleum.pdf?la=en

It has a lifespan of 20 years but a much reduced cash flow already after 12 years, the period noted by Art Berman above.

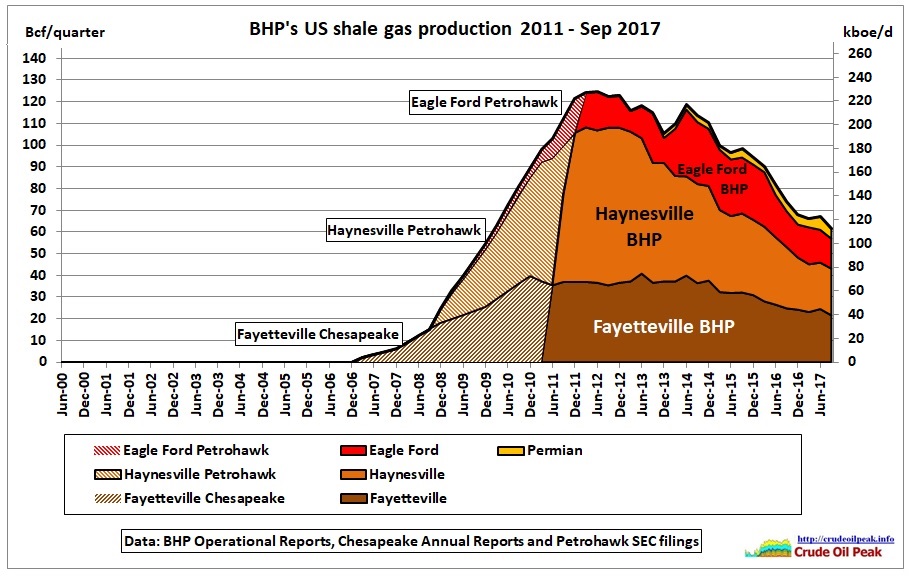

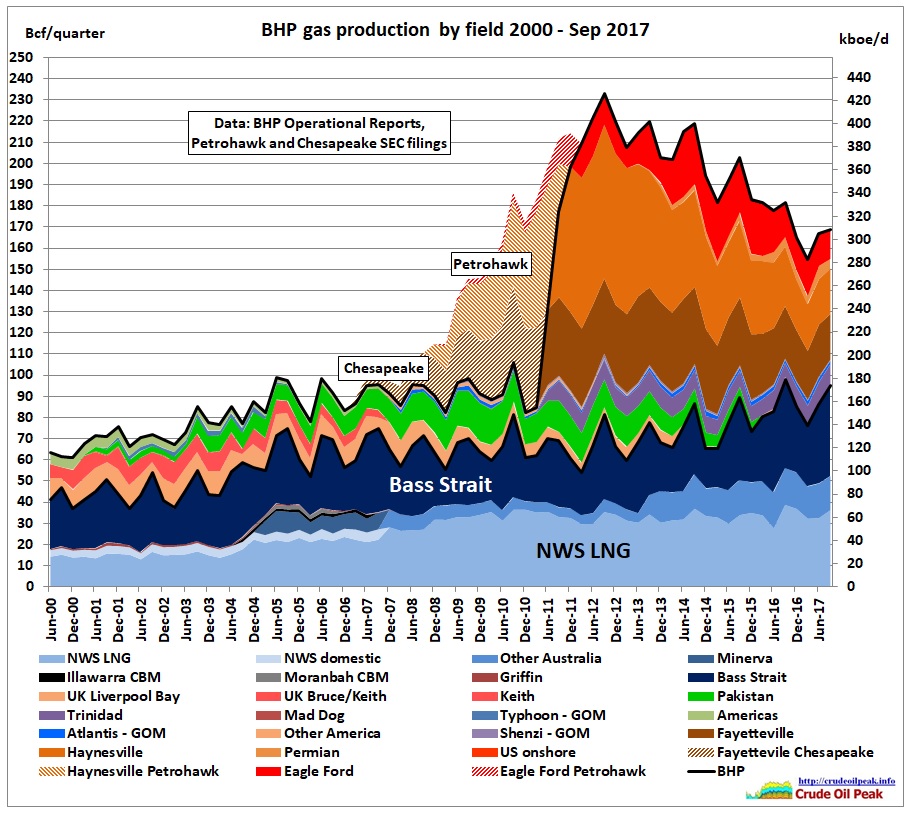

Now let’s look at the actual production statistics:

Fig 18: BHP shale gas production from 4 areas

Fig 18: BHP shale gas production from 4 areas

The hatched areas show the production in these gas fields before the BHP acquisition, from Chesapeake and Petrohawk.

It is clear that BHP bought Fayetteville and Haynesville just as gas production was peaking.

Fig 19: BHP’s total gas production

Fig 19: BHP’s total gas production

The acquisitions were meant to allow BHP to overcome stagnating gas production elsewhere.

Outlook

22/8/2017

“One of the features of shale, which I think we have grown to like a bit less with time,” is that “you have to continue to invest to actually maintain the value of those businesses,” Mackenzie said

http://www.naturalgasintel.com/articles/111478-bhp-actively-marketing-permian-haynesville-eagle-ford-fayetteville

Conclusion:

BHP’s acquisition of the Faytteville shale gas is a clear case of shale hype which has gripped the US oil industry, investors, banks and all those who continue to build oil and gas dependent infrastructure under the assumption that there will be a continuing shale revolution.

We also see that problems have come long before the US gas peak is finally reached. The same applies to oil. Commenters who do not like peak oil and mockingly ask: “Where is the peak? I can’t see it” should open their eyes, look for past peaks in subsystems (companies, countries, basins, regions) and study what the impacts were. That will help them to understand what’s going to happen when we reach the final global peak.