What was done so far

This website contains the relevant reports:

IEA International Energy Program Treaty

https://www.energy.gov.au/iea-international-energy-program-treaty

In July 2012 (under the Rudd government), just months after Australia permanently dropped below the 90 days mark, a report prepared by Hale & Twomey Limited (from New Zealand) was published titled:

National Energy Security Assessment (NESA) Identified Issues –

Australia’s International Energy Oil Obligation

30/7/2012

https://www.energy.gov.au/sites/g/files/net3411/f/nesa-identifed-issues-aust-energy-oil-obligation-2012.pdf

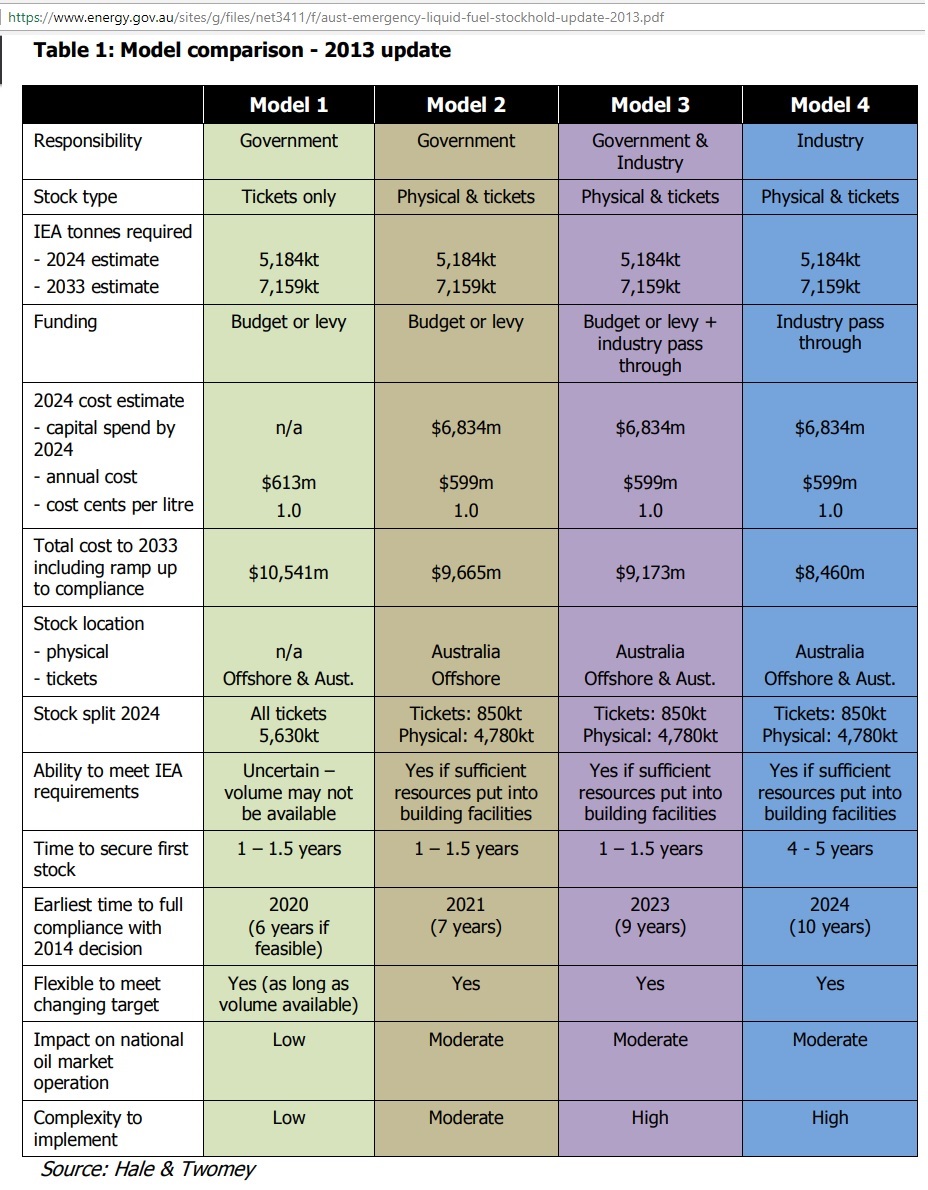

The report proposed 4 models with varying degrees of responsibilities, funding , stock type, location and split

- Model 1: Government responsible for the IEA stockholdings and uses ticket contracts to secure emergency stock above existing commercial stock levels.

- Model 2: Government responsible for the IEA stockholdings and uses both physical stock and tickets to secure emergency stock above existing commercial stock levels.

- Model 3: Combining government responsibility with an industry obligation and using both physical stock and ticket contracts for emergency stock.

- Model 4: There is an industry obligation which will ensure the target can be met with the option to use both physical stock and tickets to meet the obligation.

Tickets are option contracts in which a country or organization purchases an option to buy stock from a stock owner. The stock can only be released in an emergency (declared by the IEA), with the option holder able to buy the stock at market prices. The purchaser of the ticket is able to count the stock as part of its obligation to hold emergency stock and the seller of the ticket is obliged to subtract these ticket sales from their stocks. This is physically monitored by the IEA. When stock owners and purchasers are in different countries these transactions are called bilateral tickets and require government-to-government agreements between both countries that guarantee the purchaser can exercise its options when needed.

The time required for implementation of each of the 4 models: 5-10 years starting in 2012. The report also did some cost calculations: from 0.5 cents/liter (model 1) to 1.4 cents/liter (model 4) in 2016 and 1.1 to 3.1 cents per liter in 2022 (compliance year).

In October 2013, 1 month after Abbott’s government took over, an update of the above report (certainly prepared during the Rudd government) came out.

Australia’s Emergency Liquid Fuel Stockholding Update 2013 – Australia’s IEA Oil Obligation

https://www.energy.gov.au/publications/australias-emergency-liquid-fuel-stockholding-update-2013-australias-iea-oil-obligation

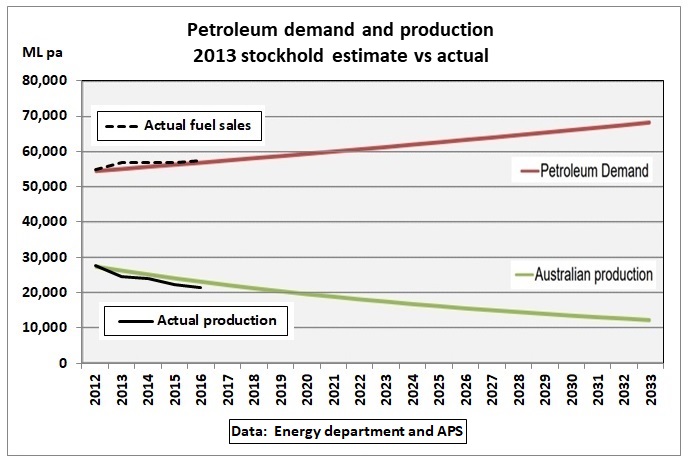

This update estimated a widening gap between petroleum production and demand in order to calculate IEA stockholding requirements.

Fig 12: Trend estimate (2013) of petroleum production and demand with 2016 actuals added by author

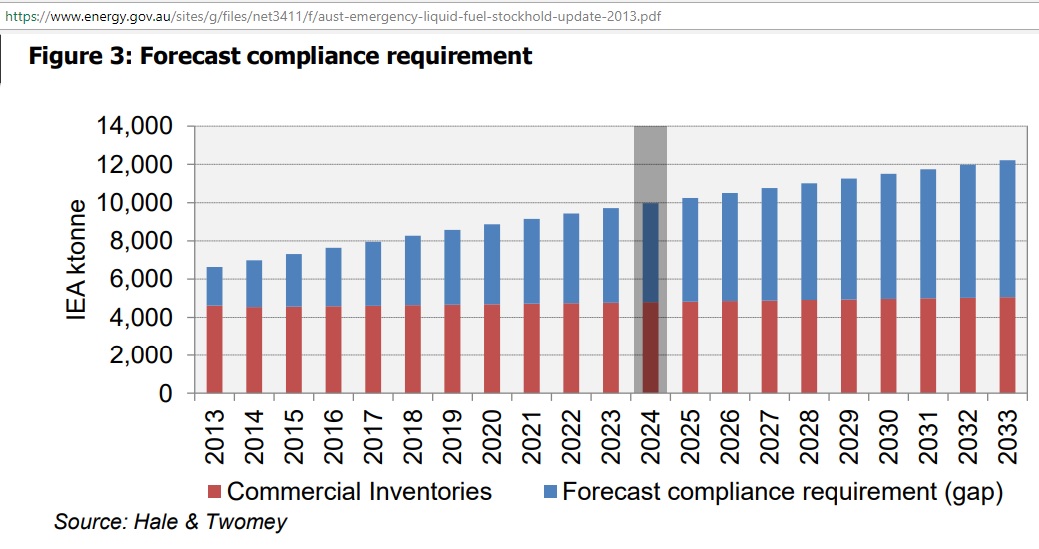

The above gap was used to calculate future petroleum stock requirements:

Fig 13: Commercial and emergency stock requirements. Target year moved to 2024

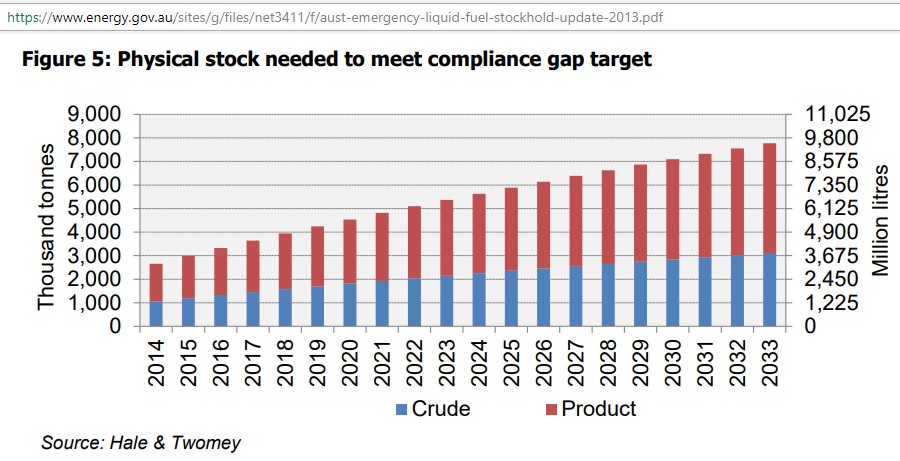

Fig 14: Crude and product split

The 2013 stockhold report is based on the closure of the Kurnell and Clyde refineries but mentions that products would be 70% of total stocks if the Geelong refinery (120 kb/d) shuts down. Instead, the Bulwer refinery in Brisbane (102 kb/d) closed down.

The quantity of petroleum products in stock increases more than that for crude as Australia’s refining capacity is capped and demand for products is assumed to grow.

To give an idea about the magnitude of this job look at a tank farm in Rotterdam:

Fig 15: Tank farm with 1.6 million m3 capacity (10 million barrels)

http://www.odfjell.com/Terminals/RotterdamTerminalNetherlands/otr/Documents/Odfjell%20Terminals%20Brochure.pdf

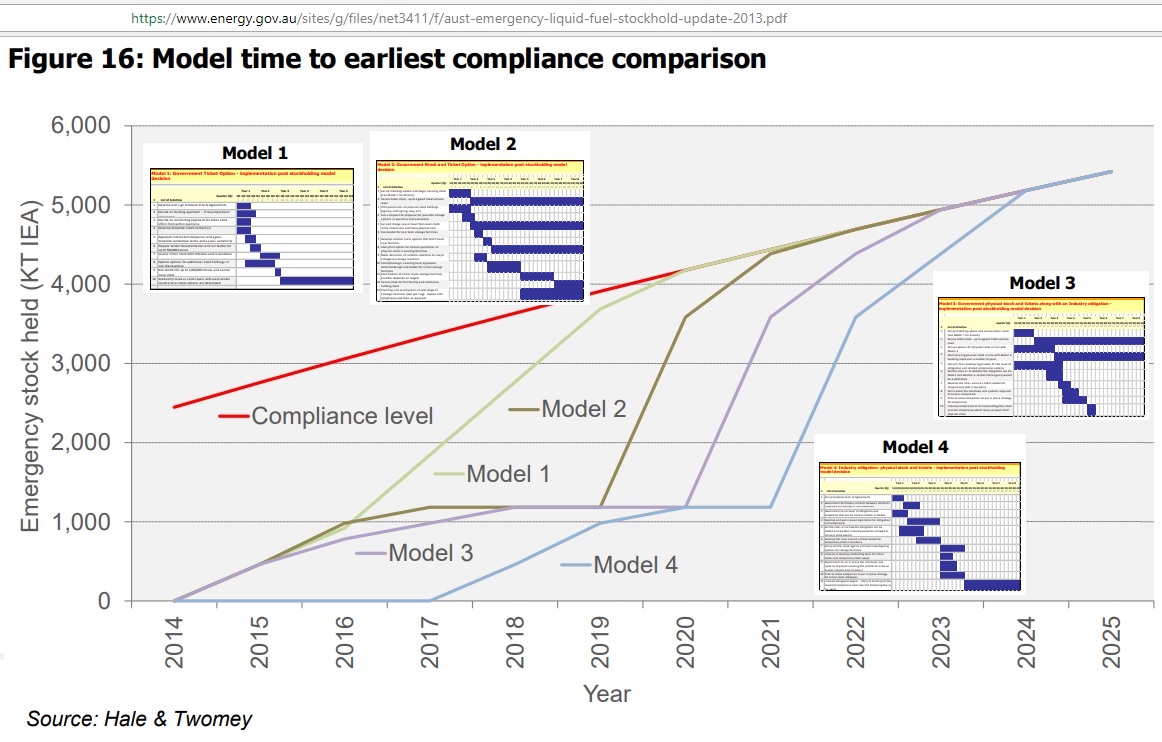

Just to bring Australia to the 2016/17 compliance level 4/1.6 = 2.5 tank farms of the above size would have to be built. We see the problem gets bigger and bigger over time. The 10 year implementation period of the 2012 report has been moved by 2 years into the future:

Fig 16: 4 different Implementation paths towards emergency stock compliance

The model bar charts have been inserted by the author for illustration purposes to show the detailed work of Hale and Twomey’s research.

Fig 17 shows the updated assessment of various models up to 2024

In model 1 the Australian government hopes to buy 5,630 Kt of tickets with the objective to shift the whole problem of building additional stock capacity onto other countries.

In model 2 the Australian government has to build 4,780 Kt of capacity either in Australia itself or overseas and buy tickets for 850 Kt

In model 4 the responsibility for emergency stocks rests entirely with the petroleum industry

Model 3 is somewhere in between model 2 and 4

In any event, if the emergency stock is to be approved by the IEA, it has to be demonstrated that additional physical storage has been built, and these are huge projects.

Fig 17: Scope of 4 models as updated in 2013

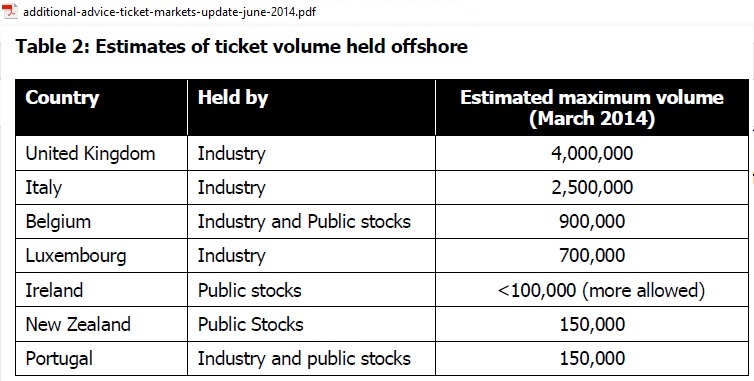

How does the proposal from Fig 17 compare to other countries?

Fig 18: Tickets held by other countries in tons

https://www.energy.gov.au/sites/g/files/net3411/f/additional-advice-ticket-markets-update-june-2014.pdf

Only UK comes close in volumes, also an oil producer which turned into a net importer after its oil production peaked.

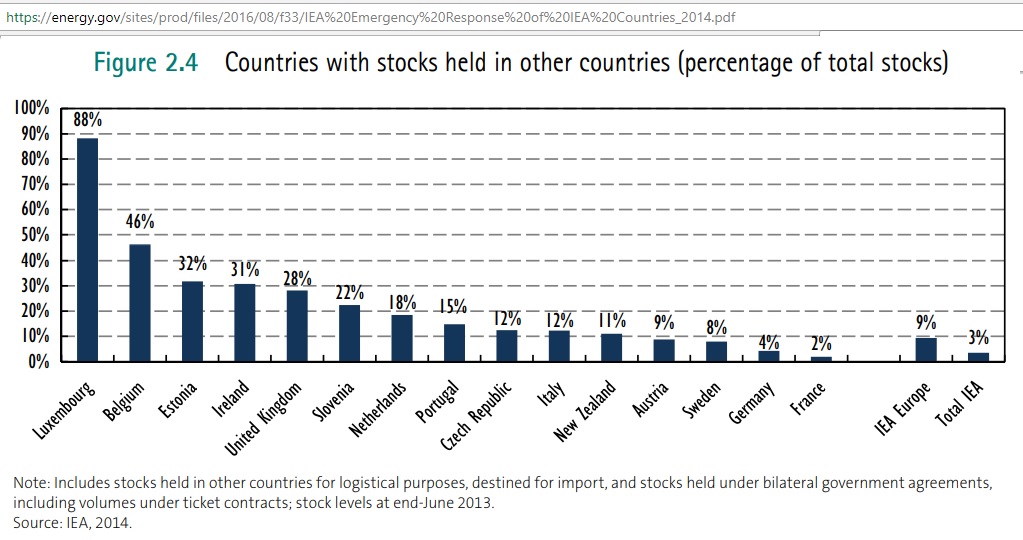

Fig 19: Percentages of oil stocks held in other IEA countries

Fig 19: Percentages of oil stocks held in other IEA countries

So for a country to hold around 50% of its oil stocks in other countries would be extraordinary, especially when considering Australia’s remote location. Most countries (except NZ) in the above chart would have access to their ticket stock in close geographic proximity.

Fig 20: IEA member countries

https://assets.geoexpro.com/uploads/60f15009-2e22-4a2d-ae19-5a300db75b8f/iea_1130x486.jpg

{kind=link}

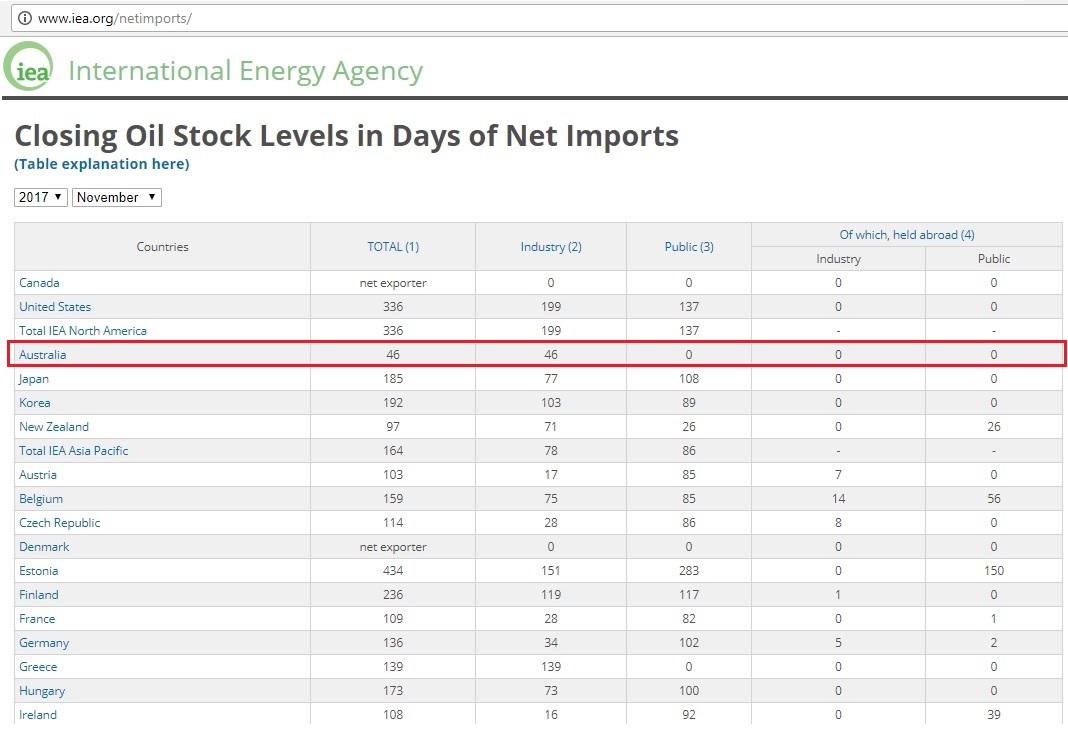

Fig 21: Excerpt from IEA’s stock level table http://www.iea.org/netimports/

Where is Australia now?

In negotiations with the IEA, the Australian government agreed in June 2016 to following measures:

- the introduction of mandatory reporting of Australian Petroleum Statistics from January 2018

- the purchase of 400 kilo tonnes of oil tickets in 2018-19 and 2019-20 to enable Australia to contribute to an IEA collective action if needed. Tickets are used by some IEA members to supplement in-country stocks to meet their 90 day requirement and can be used to contribute towards collective action in the event of an oil supply disruption

- a return to full compliance with the IEA stockholding obligation by 2026. This will include diplomatic engagement to expand the international ticket market in the Asia-Pacific region, and ongoing investigation into the potential for emergency liquid fuels stockholdings to be established in Australia and overseas

- establishment of an Energy Security Office [in July 2016] within the Department of the Environment and Energy

https://www.energy.gov.au/iea-international-energy-program-treaty

On item 2, legislation was passed in both the House of Reps and the Senate to authorize the government to implement the purchase of tickets

LIQUID FUEL EMERGENCY AMENDMENT BILL 2017

11/9/2017

The Liquid Fuel Emergency Amendment Bill 2017 (the Bill) enables the Australian Government to enter into commercial oil stockholding contracts, with either foreign or Australian entities. These contracts include purchasing rights to access oil stocks, also known as ‘ticketing’.

This amendment is required to provide the legislative authority for the spending of funds on oil stockholding contracts, for the purpose of the principles confirmed by the High Court in Williams v Commonwealth (No 2) (2014) 252 CLR 416.

The Australian Government plans to purchase 400 kilotonnes of offshore tickets in the 2018-19 and 2019-20 financial years. This initial purchase of tickets is part of the first phase of Australia’s return to compliance with the IEA’s 90-day oil stockholding obligation. The ticketing contracts will be supported by government-to-government level arrangements or treaties with the host country, a requirement of the IEA.

That’s the 1st phase. If the Australian government continues at the ticket buying speed of 200 Kt pa it is easy to calculate how many decades the remaining phases will take.

And get this: the government intends to buy tickets in Asia (in the hope the IEA will approve it). There does not seem to be any commitment to start building additional physical tank farm infrastructure in Australia as only “investigations” in the “potential” are promised until 2026.

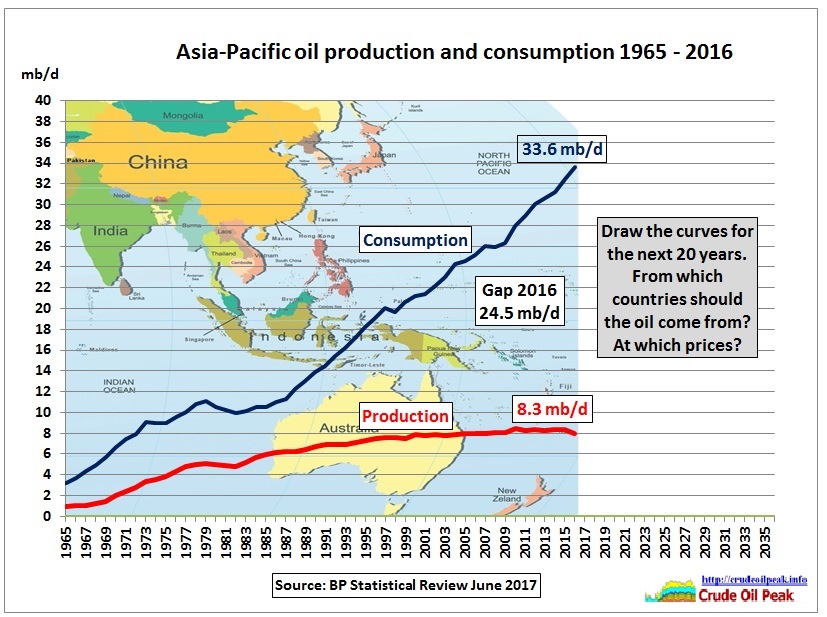

This timid approach is fundamentally flawed. First, oil production in the Asia Pacific has peaked so the problem of imports will become acute in the not too distant future.

Fig 22: AP oil production and consumption (BP Statistics)

Fig 22: AP oil production and consumption (BP Statistics)

Secondly, the likely crises which would require to draw on emergency stocks would be along the oil trading route Japan/Korea – South China Sea – Singapore, threating the very shipping lanes emergency stock from Asia would be using.

Not to mention that Asia itself is highly dependent on oil from the Middle East so any crisis there may cause Asian ticket partners to renege on their contracts. When writing this post:

Eleven Chinese warships reportedly sailed into the East Indian Ocean this month, amid a constitutional crisis and state of emergency in the Maldives.

21/2/2018

http://www.abc.net.au/news/2018-02-21/chinese-warships-enter-east-indian-ocean-amid-maldives-tensions/9469836

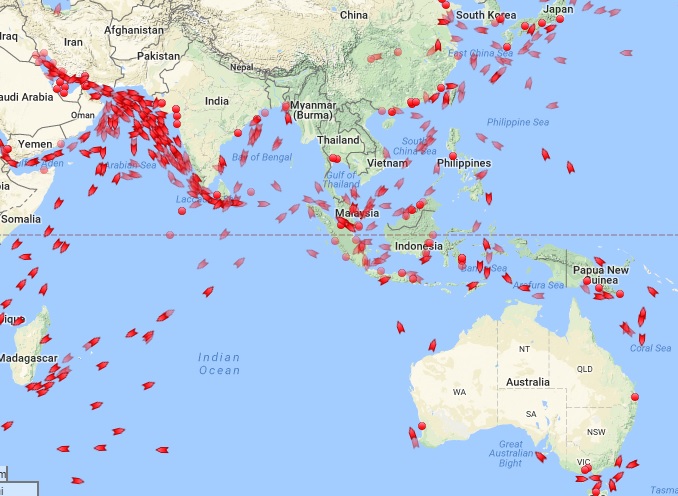

Fig 23: Tanker traffic

Fig 23: Tanker traffic

Conclusion:

With each oil stock report Australia’s conveniently self-defined compliance window of 10 years is moved 2 years into the future. One wonders when the IEA will be running out of patience. More importantly, Australia may be running out of time as the number of unsolvable conflicts in the Middle East and in Asia accumulates. And US shale oil will be peaking, too. We don’t know when that will happen, but it will happen. Australian energy bureaucrats and their political masters seem to be too complacent to prepare for these events.

Related posts:

12/8/2017 Almost half of Australia’s petrol, diesel and jet fuel imports come from South Korea and Japan

http://crudeoilpeak.info/almost-half-of-australias-petrol-diesel-and-jet-fuel-imports-come-from-south-korea-and-japan

23/6/2017 Australia’s oil stock coverage on record low

http://crudeoilpeak.info/australias-oil-stock-coverage-on-record-low

29/4/2017

South Korea’s oil trade under threat

http://crudeoilpeak.info/south-koreas-oil-trade-under-threat

14/4/2017

Australia more vulnerable than ever to fuel import disruptions

http://crudeoilpeak.info/australia-more-vulnerable-than-ever-to-fuel-import-disruptions

12/1/2016 No glut in Australian petroleum inventories

http://crudeoilpeak.info/no-glut-in-australian-petroleum-inventories