Exxon Mobil’s Melbourne refinery is closing and will be converted into a fuel import terminal. The Australian public broadcaster has found the right title for its article:

Australia loses another oil refinery, leaving our fuel supply vulnerable to regional crises

11/2/2021

https://www.abc.net.au/news/2021-02-11/australia-loses-another-oil-refinery-risking-fuel-supply/13139648

Fig 1: Exxon-Mobil Altona refinery in Melbourne

Fig 1: Exxon-Mobil Altona refinery in Melbourne

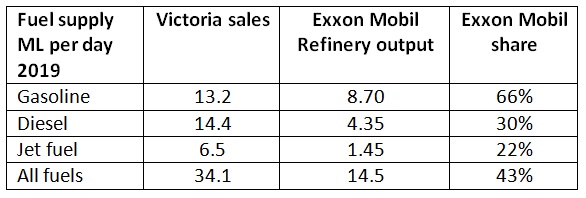

The refinery has a capacity of 86 kb/d, around 10% of Exxon Mobil’s Asia Pacific capacity.

Fig 2: Exxon Mobil’s refineries in Asia Pacific

Fig 2: Exxon Mobil’s refineries in Asia Pacific

“The Altona refinery produces up to 14.5 million litres of refined products per day.

Petrol represents approximately 60 percent of production [8.7 ML/d], with diesel representing a further 30 percent [4.35 ML/d] and jet fuel around 10 percent [1.45 ML/d]. The percentage of each product depends on the type of feedstock used – different types of crude oil, for example, will produce more or less LPG from the refining process.

Around 90 percent of products are transported by pipeline from the refinery to Mobil’s Yarraville terminal and other industry terminals for distribution by road.

The refinery supplies feedstock for the nearby Altona chemical complex, which in turn supplies feedstocks to a number of petrochemical manufacturing plants at Altona. These plants produce the raw material from which a multitude of consumer products are made.”

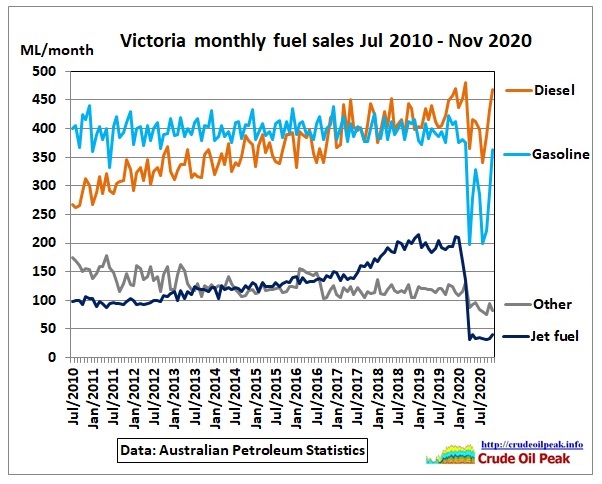

How much is that compared to Victoria’s fuel sales?

Fig 3: Victoria’s petroleum sales by product

Fig 3: Victoria’s petroleum sales by product

Between 2010 and December 2019 Victoria gasoline sales were practically flat at 400 ML/month or 13.2 ML/day. In contrast, Diesel sales increased by a whopping 5.5% pa from a trend average of 290 ML/month in July 2010 to 440 ML/month or 14.4 ML/day by end 2019. Jet fuel sales increased from 100 ML/month in 2010/11 to 200 ML/month or 6.5 ML/day in 2018/19 (jump due to international flights)

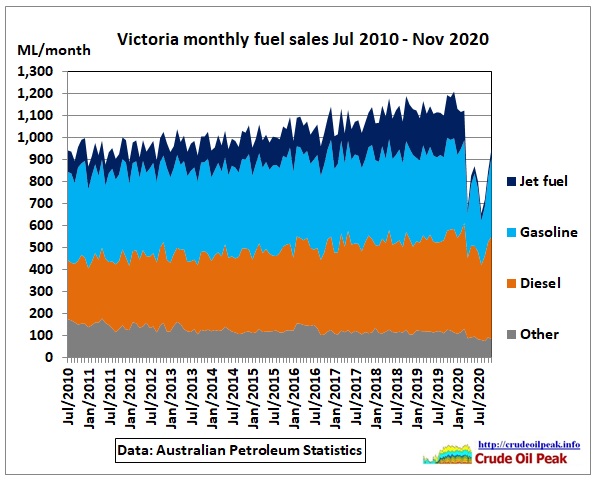

Let’s stack it all up:

Fig 4: Total Victoria fuel sales

Fig 4: Total Victoria fuel sales

10 Feb 2021

“ExxonMobil has imported crude from destinations including West Africa and Azerbaijan for the Altona refinery in recent months. The refinery also runs crude produced by the Gippsland Basin Joint Venture (GBJV) operated by ExxonMobil in a 50:50 partnership with UK-Australian resources firm BHP. GBJV produced around 25,000 b/d of crude and condensate in July-December last year.”

https://www.argusmedia.com/en/news/2185554-exxonmobil-australia-to-shut-90000-bd-altona-refinery?backToResults=true

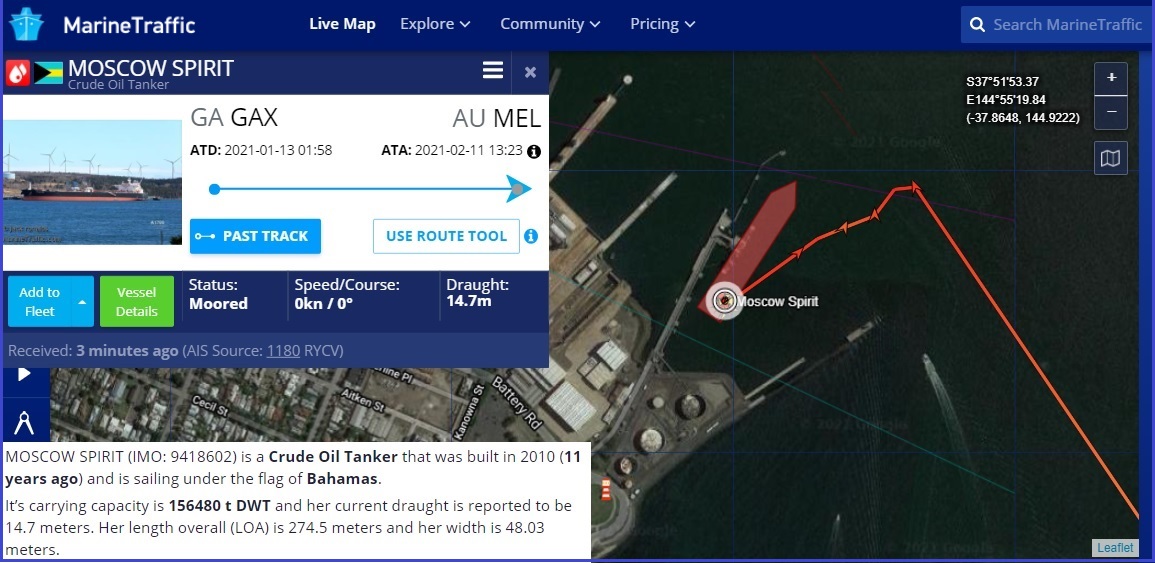

Let’s see how crude oil supplies from West Africa work. While writing this article MOSCOW SPIRIT (Suezmax, Teekay, Bahamas) is in town with crude oil from GA GAX

Using MarineTraffic https://www.marinetraffic.com

Fig 5: Crude oil tanker at Melbourne’s Gellibrand pier with pipeline to Altona

Fig 5: Crude oil tanker at Melbourne’s Gellibrand pier with pipeline to Altona

So where is GA GAX? It’s a “crude oil terminal” in Gabon, but not what you think:

Fig 6: GAMBA mooring offshore Gabon

Fig 6: GAMBA mooring offshore Gabon

https://www.marinetraffic.com/en/ais/details/ports/21495

Would Melbourne motorists have any idea the crude oil supply for their petrol would come from this?

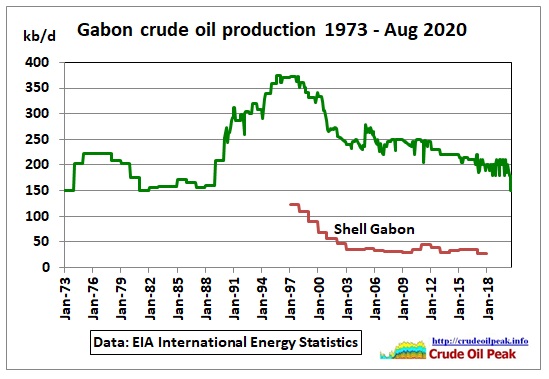

Nor would they know (or being told by the government or media) that Gabon’s oil production peaked long time ago.

Fig 7: Gabon’s crude oil production peaked long ago

Fig 7: Gabon’s crude oil production peaked long ago

Not only Gabon’s oil production, but all of Africa’s production has peaked

5/2/2021

Peak oil in Africa (part2): Export zero sum game

https://crudeoilpeak.info/peak-oil-in-africa-part-2-export-zero-sum-game

19/1/2021

Peak oil in Africa part1: OPEC quotas Jan 2021

https://crudeoilpeak.info/peak-oil-in-africa-part1-opec-quotas-jan-2021

As Fig 7 shows, Shell was once involved in Gabon but:

Shell divests Gabon onshore interests

24 Mar 2017

https://www.shell.com/media/news-and-media-releases/2017/shell-divests-gabon-onshore-interests.html

China’s CNOOC Acquires Shell’s Interests in Offshore Gabonese Blocks

27 Nov 2019

“Royal Dutch Shell Plc has transferred its 75% operated interest in exploration blocks BC9 and BCD10 located off the coast of Gabon to CNOOC Africa Holdings Ltd., a wholly-owned subsidiary of Chinese state-owned oil company CNOOC Ltd. Previously, in March 2017, Shell had entered into a transaction with Assala Energy Holdings Ltd., a portfolio company of The Carlyle Group, for the sale of all of its onshore oil & gas assets in Gabon, for a total consideration of US$587.0 million. Shell’s withdrawal from the two offshore blocks completes its exit from Gabon.”

https://www.finbrook.com/news/chinas-cnooc-acquires-shells-interests-in-offshore-gabonese-blocks

So well done, Exxon Mobil, to have secured this crude cargo from Gabon. But it won’t last long. 1 mill barrels of a SUEZMAX tanker will most probably yield 170 ML of fuels, not even the equivalent of 2 weeks of Altona’s requirements.

https://energyeducation.ca/encyclopedia/In_a_barrel_of_oil

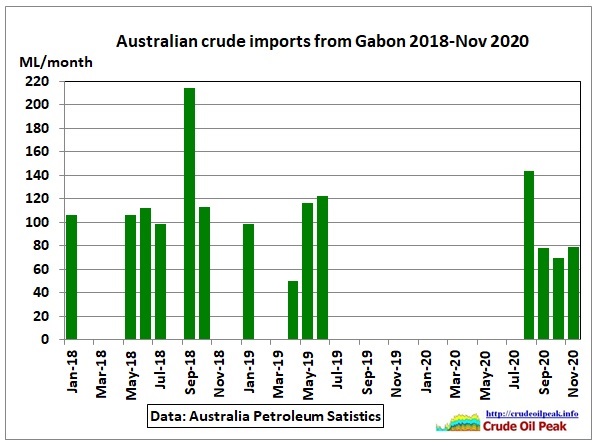

Australian refineries started to import crude oil from West Africa (Gabon and Congo) in 2011. There was a drop in imports after the first 3 refineries closed (Clyde, Kurnell, Bulwer). They then bounced back, followed by a steady decline.

Fig 8: Australian imports from Gabon showing a big gap in 2019/20

Fig 8: Australian imports from Gabon showing a big gap in 2019/20

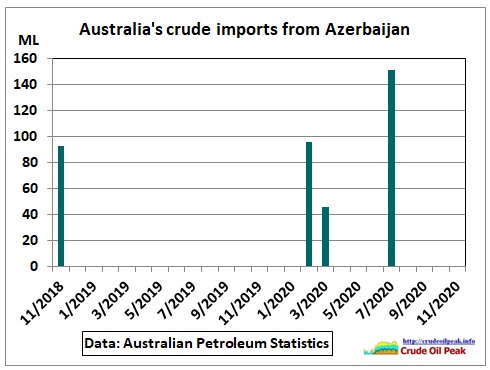

And how about Azerbaijan? Australia imported oil from there in only 4 months during the last 2 years

Fig 9: Australian crude imports from Azerbaijan Nov 2018-Nov 2020

Fig 9: Australian crude imports from Azerbaijan Nov 2018-Nov 2020

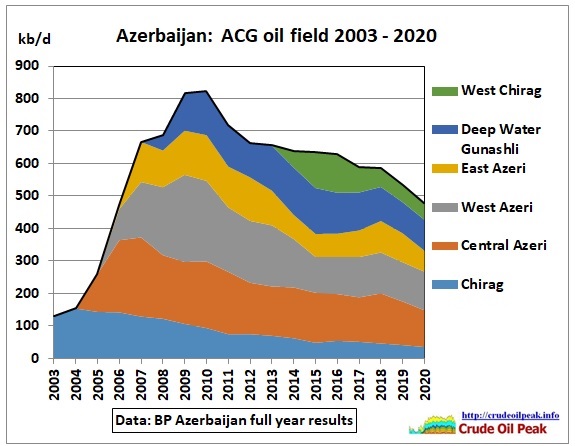

Nevertheless, it is interesting to look at Exxon Mobil’s activities in Azerbaijan. According to the 2019 Financial and Operating Review Exxon Mobil holds a 7% working interest in the ACG (Azeri-Chirag-Guneshli) field with a net liquids production of just 13 kb/d.

Fig 10: Azerbaijan’s ACG oil field in the Caspian

Fig 10: Azerbaijan’s ACG oil field in the Caspian

https://www.bp.com/en_az/azerbaijan/home/news/business-updates/2020-full-year-results.html#accordion_1

After this short excursion into peak oil let’s go back to Exxon Mobil’s refineries.

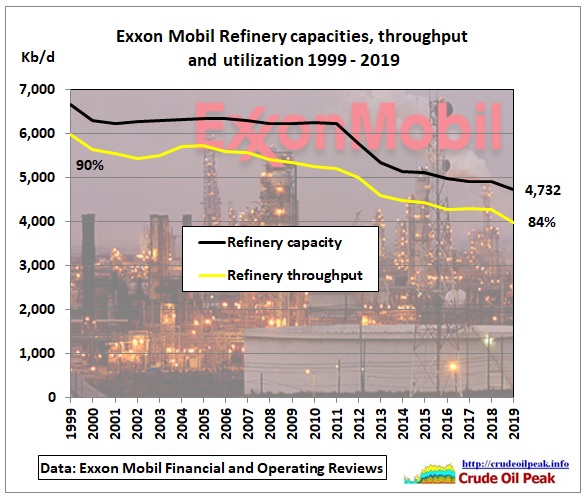

Fig 11: Exxon Mobil refinery capacities and utilization

Fig 11: Exxon Mobil refinery capacities and utilization

Refinery capacities were reduced from 6,700 kb/d to 4,700 kb/d over 20 years and utilization went down to 84%.

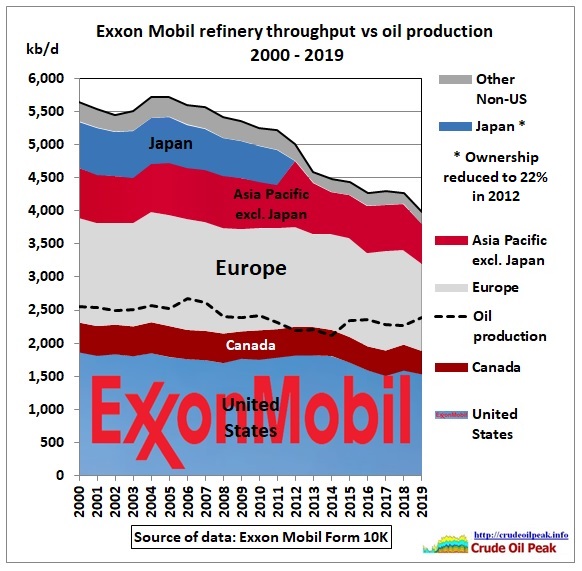

Fig 12: Exxon Mobil’s refinery throughput

Fig 12: Exxon Mobil’s refinery throughput

Exxon Mobil’s global refinery throughput declined by 24% since 2011, Asian throughput by almost 50%. Consequently, product sales went down, but stabilized 2014.

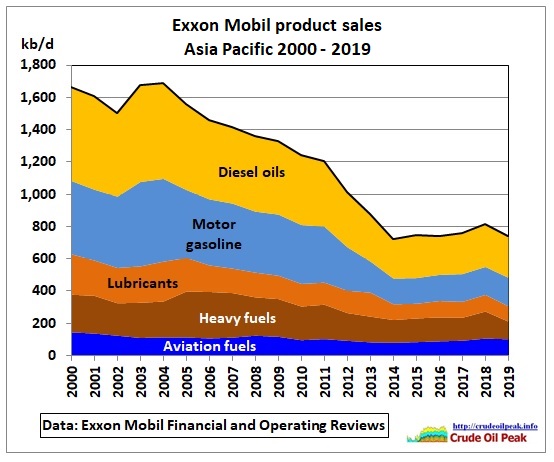

Fig 13: Exxon Mobil’s fuel sales in Asia

Fig 13: Exxon Mobil’s fuel sales in Asia

Historic reminder:

10 Jan 2014

“Almost 300 Mobil outlets were sold to 7-Eleven in 2010, under a deal that was expected to precipitate ¬ExxonMobil’s exit from all downstream operations in Australia.

But the two companies surprised the market on Thursday when they announced Mobil – which continued to supply fuel to 7-Eleven after the sale – would have its branding returned to shopfronts throughout 2014.”

https://www.afr.com/companies/mobil-brand-back-at-the-petrol-pumps-20140110-iyarg

Production

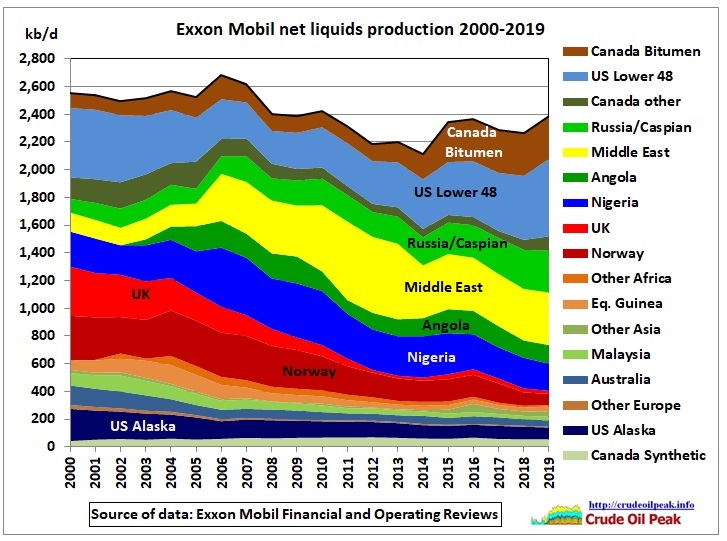

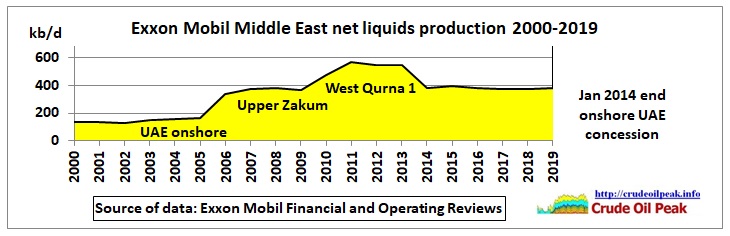

Fig 14: Exxon Mobil net liquids production

Fig 14: Exxon Mobil net liquids production

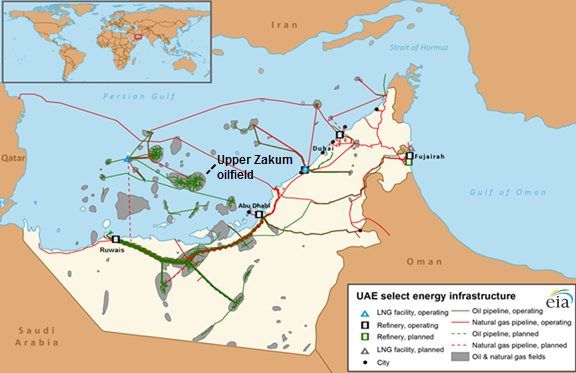

The production peak in 2006 was caused by Exxon Mobil acquiring a 28% share of the Upper Zakum oil field in the United Arab Emirates, north of Abu Dhabi.

Fig 15: Upper Zakuum oil field (artificial islands)

Fig 15: Upper Zakuum oil field (artificial islands)

https://www.eia.gov/todayinenergy/detail.php?id=23472

Fig 16: Exxon Mobil in the Middle East (West Qurna in Iraq)

Fig 16: Exxon Mobil in the Middle East (West Qurna in Iraq)

Historic explanation:

ExxonMobil will not renew bid for Abu Dhabi’s historic onshore concession

5/5/2014

ExxonMobil has reportedly not bid for the renewal of Abu Dhabi’s historic onshore concession.

The American major was alone among the legacy partners to decline to bid, according to a report published on Monday by Petroleum Intelligence Weekly, an industry news source. Exxon and partners Total, BP and Royal Dutch Shell lost their 75-year rights to the emirate’s oldest producing fields in January, when the Second World War-era contract expired.

https://www.thenationalnews.com/business/exxonmobil-will-not-renew-bid-for-abu-dhabi-s-historic-onshore-concession-1.243579

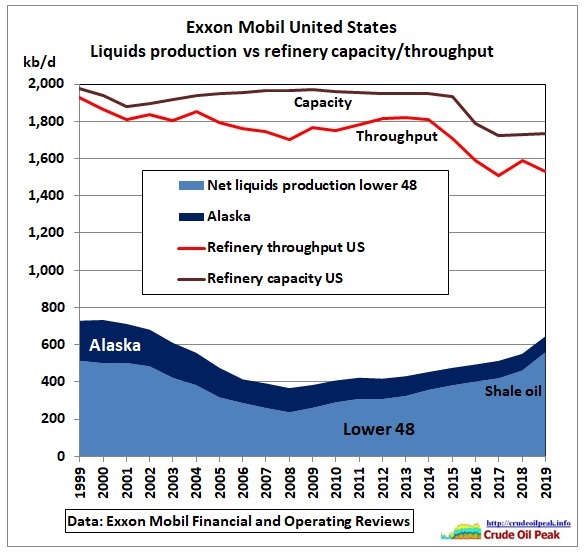

.. Fig 17: Exxon Mobil’s oil production and refineries in the US

Fig 17: Exxon Mobil’s oil production and refineries in the US

Although Lower 48 production is 9% higher than in 1999 due to shale oil, Alaska’s terminal decline did not result in total US production to be higher in 2019 than 20 years ago.

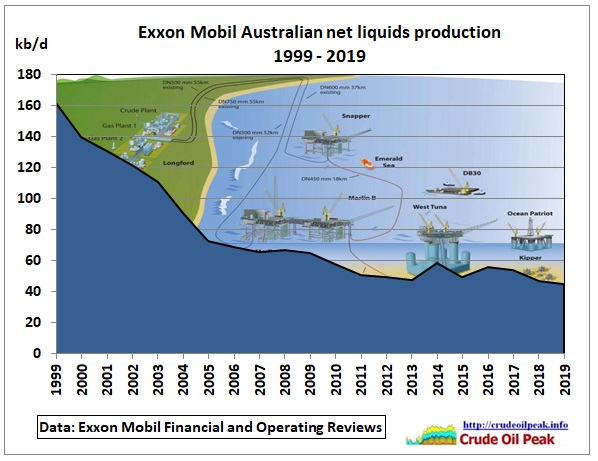

How about Exxon Mobil’s oil production in Australia (Bass Strait)? It has been going down over the last 20 years although decline rates are lower now.

Fig 18: Exxon Mobil’s net liquids production in Australia

Fig 18: Exxon Mobil’s net liquids production in Australia

Conclusion:

Due to the underlying global decline wedge Exxon Mobil’s acquisitions in the Middle & Russia and production increases in shale oil and tar sands could bring back production just to levels seen 10 years ago.

Exxon Mobil’s global refinery throughput of around 4 mb/d exceeds its own net liquids production of 2.4 mb/d by around 70% which means 3rd party oil has to be bought on the world market to fill tanks and distillation towers.

Related post:

14/11/2020

Australia’s BP Kwinana refinery closure: peak oil context

https://crudeoilpeak.info/australias-bp-kwinana-refinery-closure-peak-oil-context

The next post will be an update on Australia’s oil vulnerability