This article is an update to a previous post:

8/11/2022 Only 3-4 years to replace/save 45% of Australian diesel imports?

http://crudeoilpeak.info/only-3-4-years-to-replace-save-45-of-australian-diesel-imports

It incorporates the recently released Defence Strategic Review.

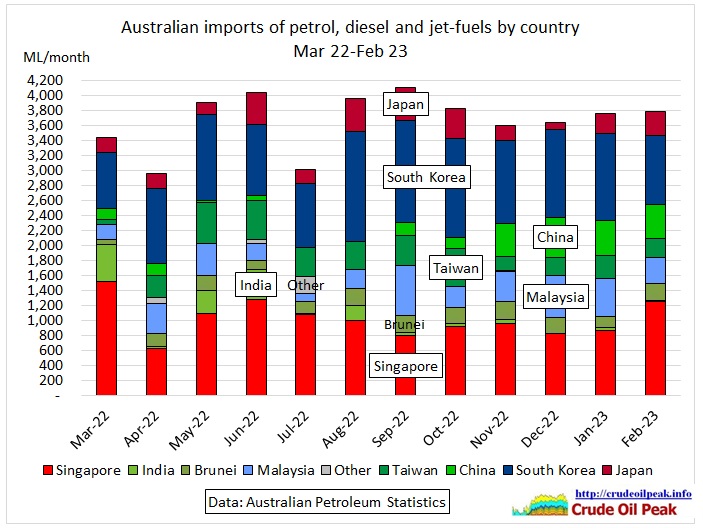

Fig 1: Australian fuel imports by country (4,000 ML/month = 830 kb/d)

Fig 1: Australian fuel imports by country (4,000 ML/month = 830 kb/d)

In ABC TV’s Sunday program “Insiders” on 30 Apr 2023, David Speers interviewed Defence Minister Richard Marles

SPEERS: So, the Defence Strategic Review says we can no longer rely on a 10 year warning period for any conflict. It says defence planning needs to focus on a 3 year period. What risks do we face in the next 3 years?

MARLES: Well, David, I think the risks that we are facing around the world right now is a global rules based order, which is under as much threat or stress that’s been at any point. We obviously see that in Ukraine, but we also see it in our own region, in places like the South China Sea. This is being accompanied by the biggest conventional military buildup that the world has seen since the end of the Second World War.

That obviously has an implication for our strategic landscape, but we’ve also changed. We are much more reliant upon our economic connection with the world. In the early 1990s, our trade as a percentage of our GDP was around 32 per cent. It’s now in 2020, was up to 45 per cent.

And there’s a physical dimension to that economic connection. Most of our liquid fuels now almost all come from overseas. Back in the nineties, we used to do it all onshore. In fact, most comes now from just one country, and that’s Singapore. So, the threat is not that we’re about to be invaded, but our exposure to economic coercion, and to coercion from an adversary is greater and the potential for that coercion going forward is much more significant. And that’s where the threat lies and that’s why we need to reposture for that (so in the next three years the worry is our trade routes, our fuel supplies could be blocked by China) [deleted].

Fig 2: Screen shot with automated youtube transcript

Fig 2: Screen shot with automated youtube transcript

The sentence on China blocking fuel supplies was removed from these videos [apparently not meant for public consumption]:

Economic coercion the biggest threat facing Australia, says Defence Minister, Insiders, ABC News

30/4/2023

https://www.youtube.com/watch?v=CIpQKpRSJJE

ABC Insiders iview

https://iview.abc.net.au/video/NC2309V012S00

The interview continues:

SPEERS: So, in the next three years, the worry is our trade routes, our fuel supplies could be blocked by China?

MARLES: Well, first, it’s not just the three years- it is that, but I think it’s beyond that. So, we are thinking about this over the next three, the next ten years and beyond. But the point that we’re really making is that when you look at the way in which great power contest is playing out, and particularly in our region, you look at that military build up and you look at our exposure to that through a much greater economic connection to the world, we are much more vulnerable to coercion than we’ve ever been before.

https://www.minister.defence.gov.au/transcripts/2023-04-30/television-interview-insiders

Let’s go through some of the statements in this interview:

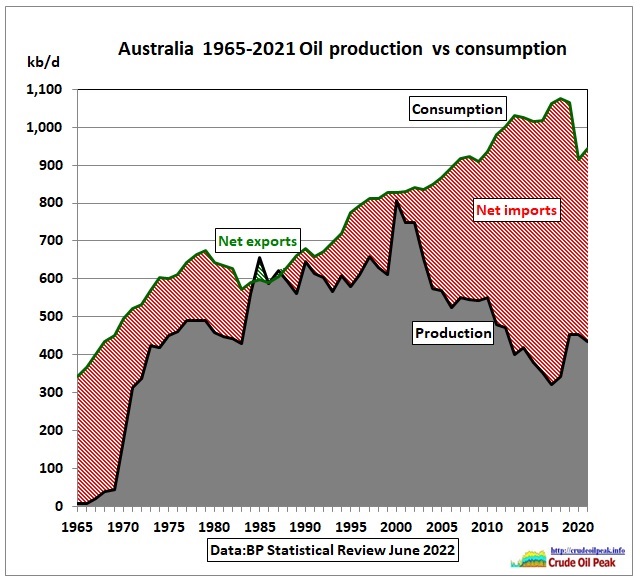

(1) “Back in the nineties, we used to do it all onshore”

Yes, that’s called peak oil.

Fig 3: Peak oil in Australia in 2000, under Howard’s watch

The time to get away from oil was under Prime Minister Howard. Being an energy and climate agnostic, he wrote in his 2004 energy white paper that alternative transport fuels were not needed. At that time these would have been CNG/LNG and rail electrification. Instead, he started LNG exports on the west coast, copied by his successor Rudd on the east coast. 80 mt pa of Australian LNG exports is the equivalent of 80 mt LNG x 8 mb oil equivalent = 640 mb or 1.7 mb/day, more than sufficient to cover 1.1 mb/d. The CO2 is in the atmosphere anyway but without benefits to the Australian transport sector.

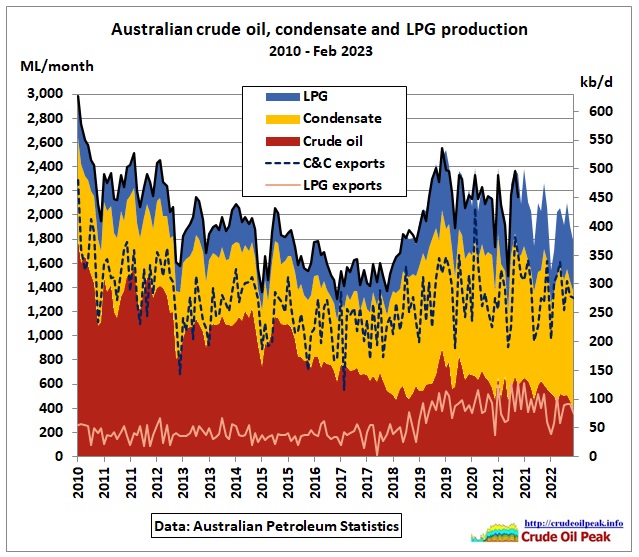

In Fig 3, the recent uptick in oil production is from condensate and LPG, mainly coming from offshore gas fields:

Fig 4: Crude, condensate and LPG production

Fig 4: Crude, condensate and LPG production

Almost all of these liquids are exported, just like LNG. Crude is exported because it may not be the type of oil needed by Australian refineries and because many were shut down anyway with only 2 remaining in operation. Condensate (associated with LNG production) is exported because Australia has no condensate splitter. There would be 20% diesel in condensate, good for essential transport of agricultural products and emergency services. In 2010 I proposed a condensate splitter to then Resource Minister Martin Ferguson at a Community Cabinet Meeting in Epping/Sydney but I was told that we can always buy oil. Most of the LPG is also exported from the west coast while it is imported on the east coast. This is more economic. We see here that financial considerations override energy security objectives.

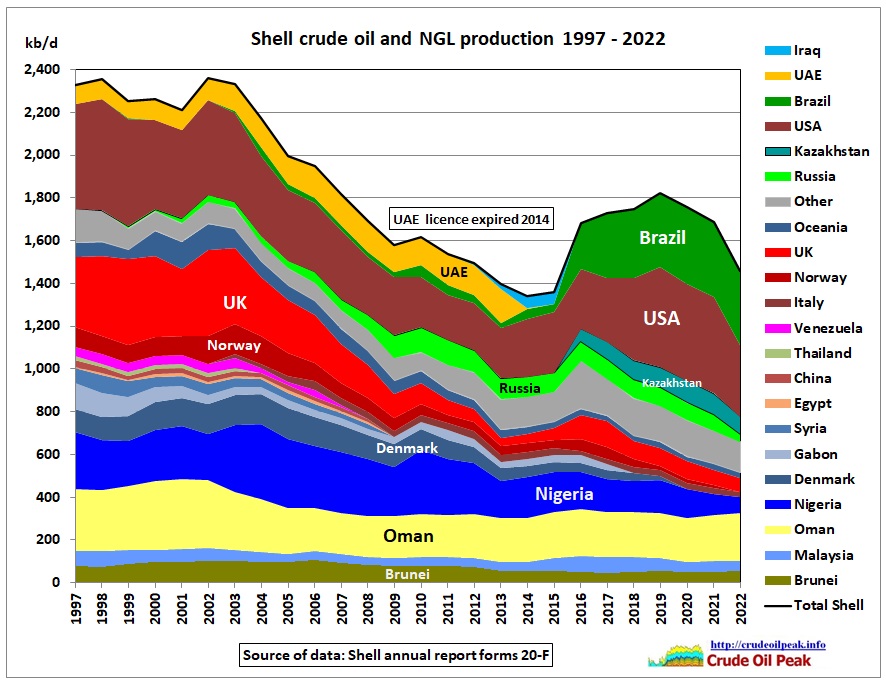

Australian refineries closed because of their small size and low complexity index compared to overseas refineries and because of peak oil experienced by international oil companies. The following graph shows the example of Shell. Look at the years 2011 and 2014 when Shell closed Clyde and sold Geelong to Viva.

Fig 5: Shell peak oil

Fig 5: Shell peak oil

13/4/2011 Australia’s fuel import vulnerability increases as Sydney’s Clyde refinery is closing

http://crudeoilpeak.info/australias-fuel-import-vulnerability-increases-as-sydneys-clyde-refinery-is-closing

23/2/2014 Geelong refinery sold as Shell’s oil production continues to decline

http://crudeoilpeak.info/geelong-refinery-sold-as-shells-oil-production-continues-to-decline

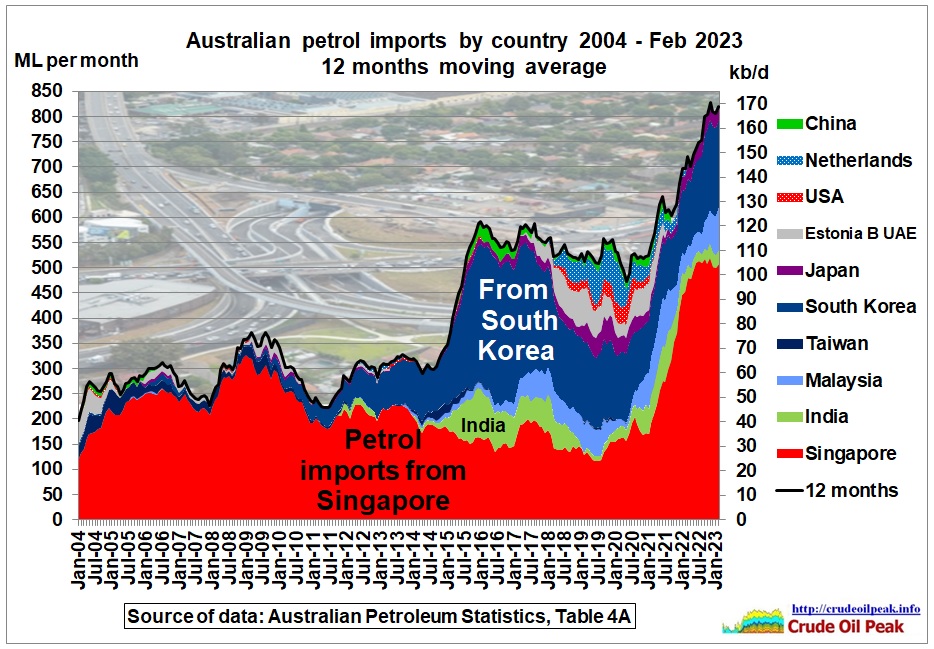

(2) “…In fact most [of our liquid fuel] comes now from just one country and that’s Singapore”

That statement is only correct for petrol:

Fig 6: Australian petrol imports by country

Fig 6: Australian petrol imports by country

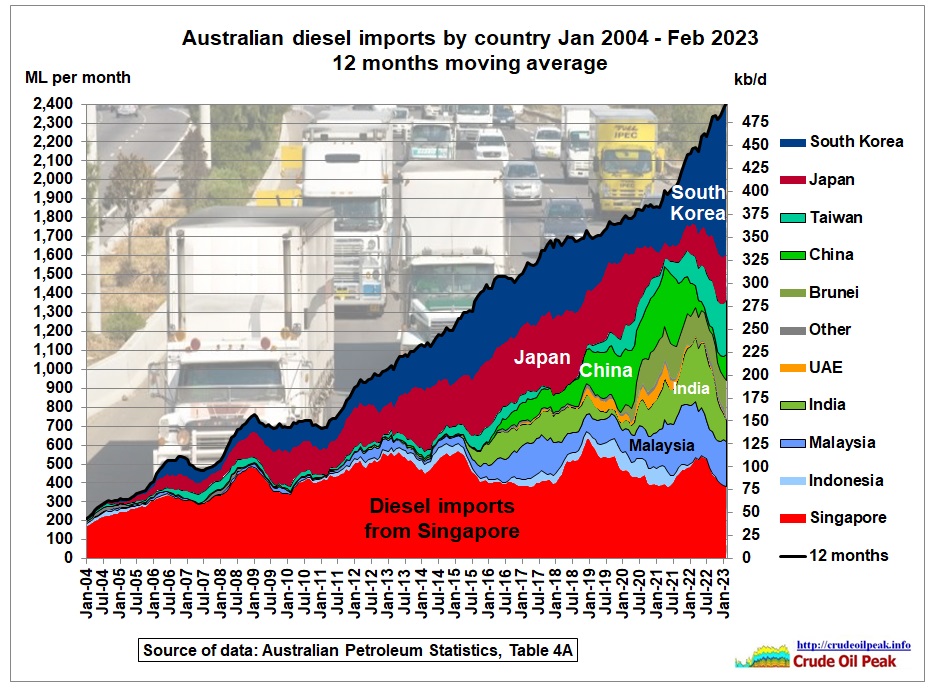

But it is not correct for diesel, on which Australia’s whole economy runs:

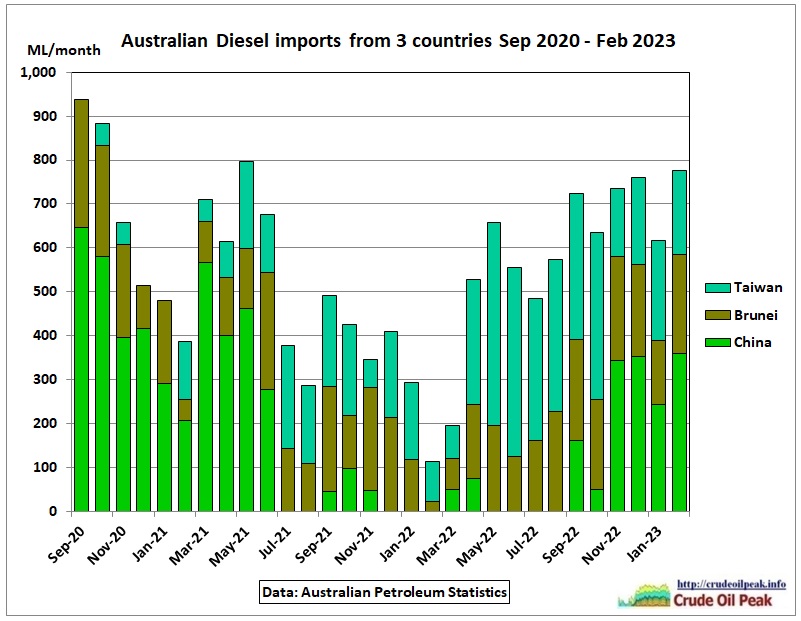

Fig 7: Australian Diesel imports by country

Fig 7: Australian Diesel imports by country

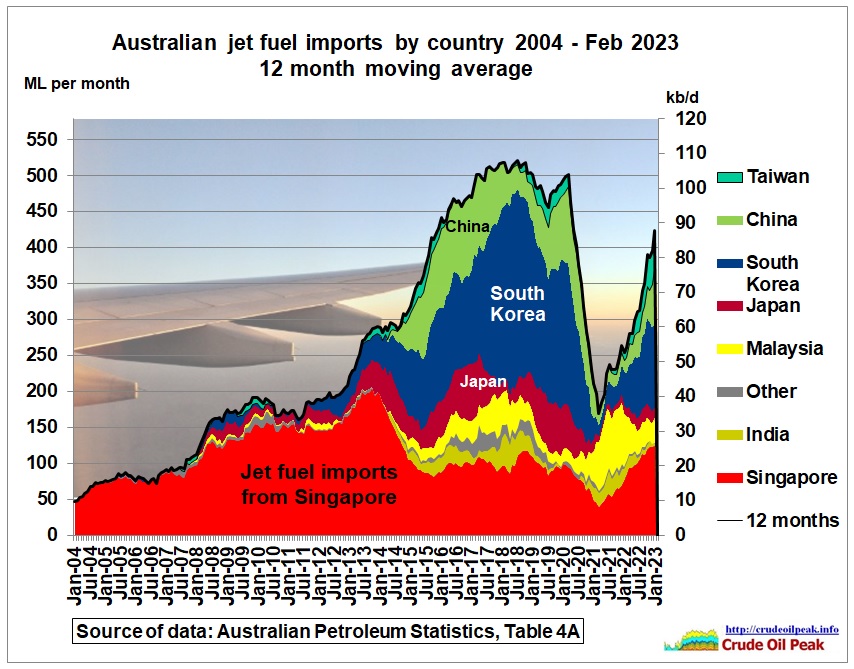

Fig 8: Australian jet fuel imports by country

Fig 8: Australian jet fuel imports by country

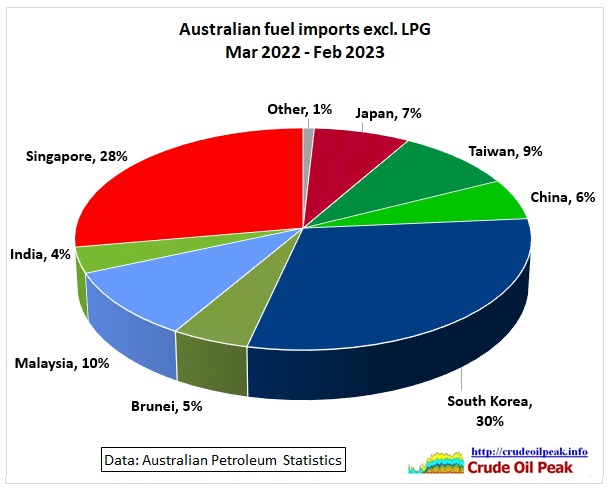

All together now for the last 12 months:

Fig 9: Australian fuel imports by country

Fig 9: Australian fuel imports by country

We see that Singapore – which is considered by the Australian public as a safe country to import fuel from – supplies ‘only’ 28 % of all fuels. Of course Singapore has to import crude oil but that would come via the Indian Ocean, not the South China Sea. We could add Malaysia because the refineries and oil ports (Melaka, Port Dickson, Pengerang) are located near to Singapore, making it 38% from these 2 countries. However, Malaysian oil production has peaked:

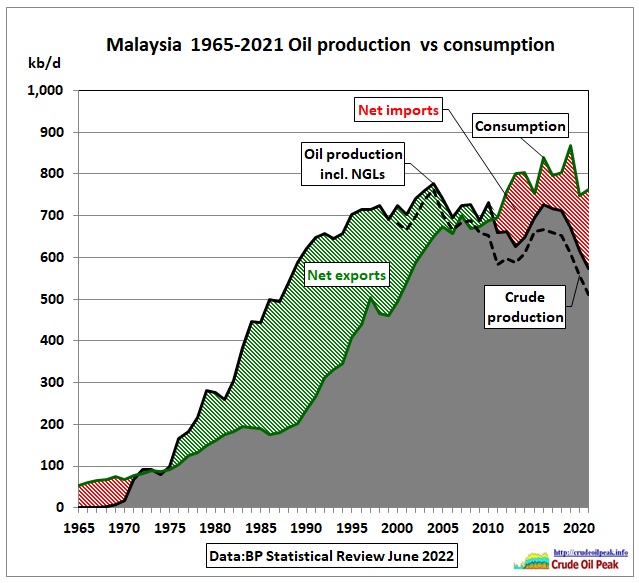

Fig 10: Malaysian oil production has peaked (BP Stat. Review data)

Let’s get some details on Malaysia’s crude oil production:

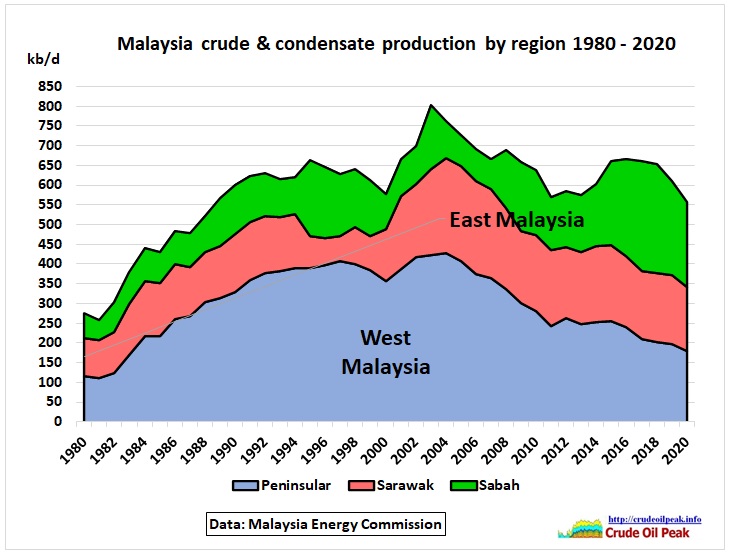

Fig 11: Malaysian crude oil production by region

Fig 11: Malaysian crude oil production by region

https://meih.st.gov.my/home

West Malaysia has definitely peaked (in 2004) at 430 kb/d followed by an average annual decline rate of 5.1%. Sarawak offshore (Bintulu – Miri) peaked a year later but declined at only 2.3 % pa.

It should also be remembered that large exploration and production blocks in both Sarawak’s and Sabah’s offshore fields lie within China’s 9-dash line and 4 Sha claims (Spratley islands).

https://www.rfa.org/english/news/china/malaysia-southchinasea-01182022151031.html

The peaking of course means it will get harder to import both crude oil and fuels from Malaysia.

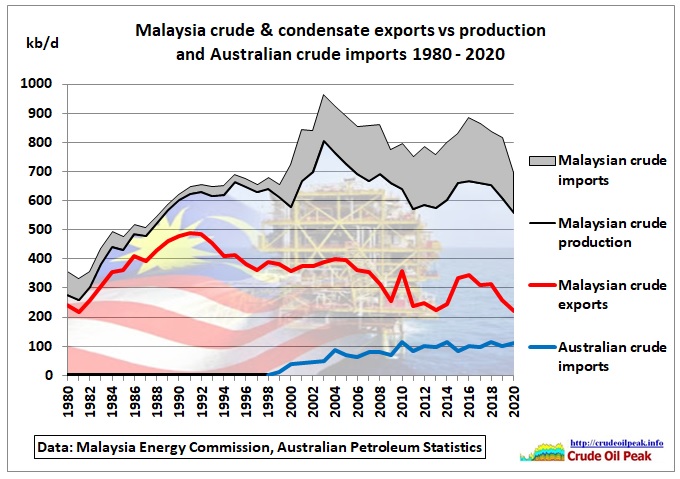

Fig 12: Australian crude imports from Malaysia vs total Malaysian exports

Fig 12: Australian crude imports from Malaysia vs total Malaysian exports

Despite declining production and exports, Australia was able to maintain crude imports at around 100 kb/d up to 2020. This is the latest year for which oil statistics from the Malaysia Energy Commission are available. What must have helped are special commercial deals between Viva Energy’s Geelong refinery and Shell which is active in Sarawak and Sabah. https://www.shell.com.my/about-us/what-we-do/shell-in-malaysia.html

Brunei is sandwiched in East Malaysia with a new Chinese refinery as was shown in this post:

25/3/2021 Brunei peak oil – golden opportunity for China’s Belt and Road Initiative

https://crudeoilpeak.info/brunei-peak-oil-golden-opportunity-for-chinas-belt-and-road-initiative

The concern from Fig 9 is that 57% of Australia’s fuel imports in the last 12 months have come from north of Singapore, including Brunei.

Imports of crude oil

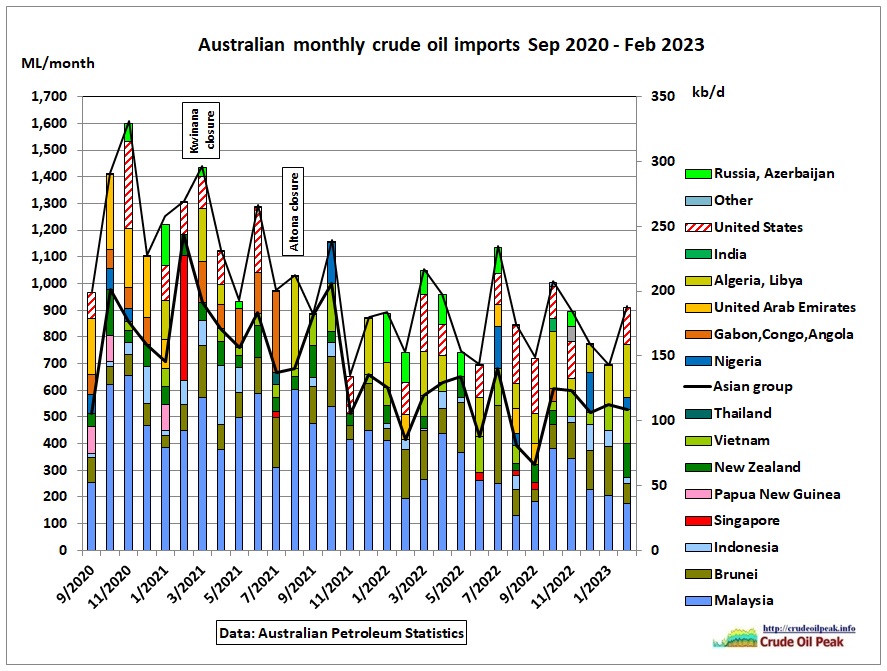

With the closing of Australian refineries and the peaking of oil production in various oil export countries, the geographic mix of Australian crude imports has fundamentally changed.

Fig 13: Australian crude imports

Fig 13: Australian crude imports

In general, Australian crude imports are more robust than fuel imports because they do not depend on supply chains passing through the South China Sea

Fig 14: Month-by-month crude imports

Fig 14: Month-by-month crude imports

Crude imports from Malaysia are on a declining trend since end 2020

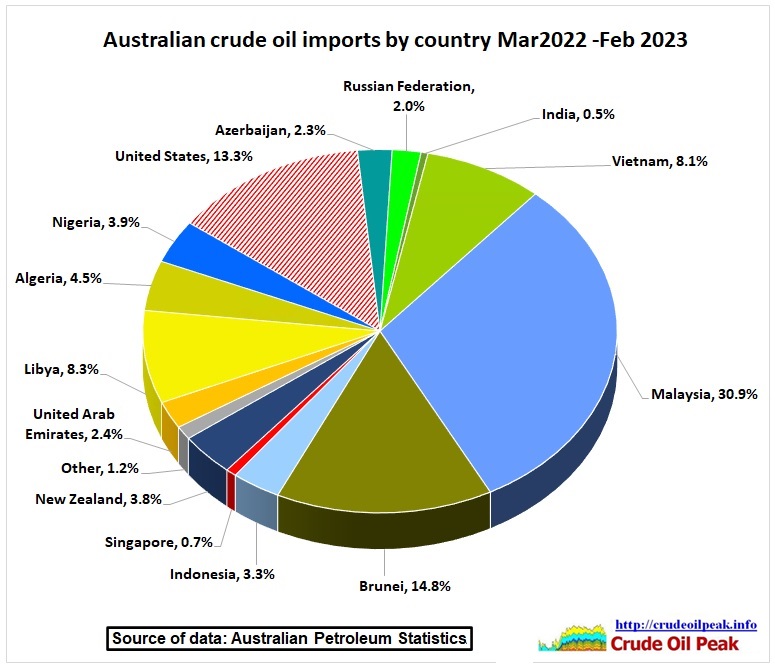

Fig 15: Crude import shares by country (last 12 months)

Fig 15: Crude import shares by country (last 12 months)

Following crude imports would be vulnerable: Vietnam, Brunei and part of Malaysia (from Sarawak and Sabah)

Australian Strategic Defence Review

This review published on 24 Apr 2023 was overseen by former Defence Minister Stephen Smith (2010-2013)

‘Worst I have ever seen’: Major review of Australia’s defence force launched amid growing security threats

3 Aug 22

The review, the first since 2012, will be led by retired Air Chief Marshal Sir Angus Houston, a former Chief of the Australian Defence Force (ADF), and former Labor defence minister Stephen Smith.

https://www.sbs.com.au/news/article/worst-i-have-ever-seen-major-review-of-australias-defence-force-launched-amid-growing-security-threats/i7liw0m3a

Stephen Smith is known to the author as someone concerned with oil supplies (short encounter with him and Beazley in the Imax theatre in Sydney in 2007).

Excerpts from the Defence Review relevant to the above Ministerial statement:

(A) Planning periods

1.19 Instead of a 10-year warning time, the Review has identified three distinct time

periods for Defence planning:

• the three-year period 2023-2025 (for those matters which must be prioritised and addressed urgently);

• the five-year period 2026-2030; and

• the period 2031 and beyond.

(B) On fuels and energy security

our commitments to increasing output of domestically produced renewable energy, improving our domestic fuel reserves, and establishing a civil maritime strategic fleet.

National Defence requires a re-posturing of Defence, particularly an enhanced network of bases, ports and barracks across northern Australia. Comprehensive upgrade works on these bases must commence immediately, and fuel storage and supply issues should be rectified.

Resilience requires the ability to withstand, endure and recover from disruption.

Resilience makes Australia a harder target and less susceptible to coercion.

Critical requirements include:

• an informed public;

• national unity and cohesion;

• democratic assuredness;

• robust cyber security, data networks and space capabilities;

• supply chain diversity;

• economic security;

• environmental security;

• fuel and energy security;

• enhanced military preparedness;

• advanced munitions manufacturing (especially in long-range

• guided weapons);

• robust national logistics; and a national industrial base with a capacity to scale.

Chapter on Fuel (page 77)

10.16 Addressing vulnerabilities, particularly where there are single points of failure and inadequate capacity in key domestic distribution routes, is essential.

A variety of alternative supply and storage back-up options needs to be developed to provide a more robust fuel posture.

Recommendation:

• A whole-of-government Fuel Council should be established as soon as possible with representatives from relevant departments and industry to deliver resilient national fuel supply, distribution and storage.

(C) On China

A stable relationship between Australia and China is in the interests of both countries and the broader region. Australia will continue to cooperate with China where we can, disagree where we must, manage our differences wisely, and, above all else, engage in and vigorously pursue our own national interest.

Australia’s strategic circumstances and the risks we face are now radically different. No longer is our Alliance partner, the United States, the unipolar leader of the Indo-Pacific. Intense China-United States competition is the defining feature of our region and our time. Major power competition in our region has the potential to threaten our interests, including the potential for conflict. The nature of conflict and threats have also changed.

Regional countries continue to modernise their military forces. China’s military build-up is now the largest and most ambitious of any country since the end of the Second World War. This has occurred alongside significant economic development, benefiting many countries in the Indo-Pacific, including Australia.

This build-up is occurring without transparency or reassurance to the Indo-Pacific region of China’s strategic intent. China’s assertion of sovereignty over the South China Sea threatens the global rules-based order in the Indo-Pacific in a way that adversely impacts Australia’s national interests. China is also engaged in strategic competition in Australia’s near neighbourhood.

https://www.defence.gov.au/about/reviews-inquiries/defence-strategic-review

The Review does not mention China blocking Australia’s fuel supplies nor even details on the conflict with Taiwan.

But Australia’s national interest requires securing fuel supplies from Asia as shown in Figs 6-8 and Fig 13. To visualize the fuel supply chain, this pic shows a tanker from Taiwan’s MAILIAO port (on the west coast)

Fig 16: Tanker A LEOPARD at Sydney’s Gore Cove terminal end December 2022

Fig 16: Tanker A LEOPARD at Sydney’s Gore Cove terminal end December 2022

Pic taken by author from a ferry

While writing this article, ARIZONA LADY was approaching Sydney. The recent port calls in Taiwan tell you the story:

Fig 17: ARIZONA LADY recent port calls in Brisbane, Taiwan and Newcastle

Fig 17: ARIZONA LADY recent port calls in Brisbane, Taiwan and Newcastle

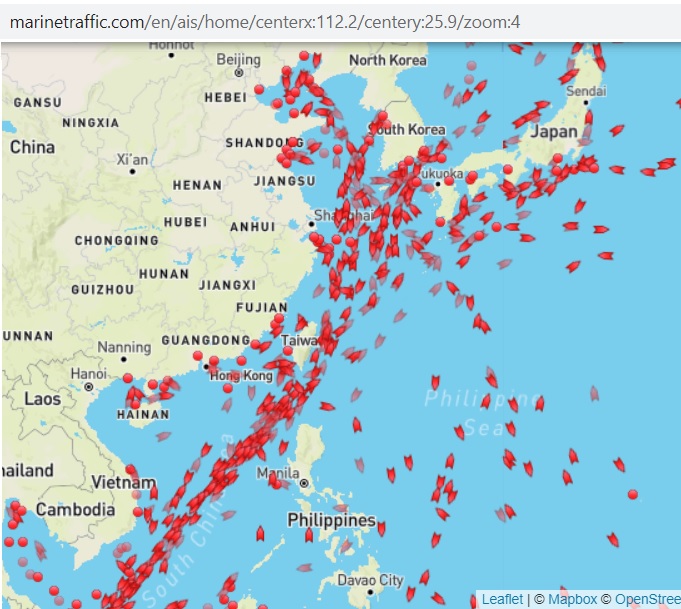

The map below shows that many crude oil tankers going north and fuel tankers going south sail east of Taiwan.

Fig 18: Tanker traffic from https://www.marinetraffic.com/

Fig 18: Tanker traffic from https://www.marinetraffic.com/

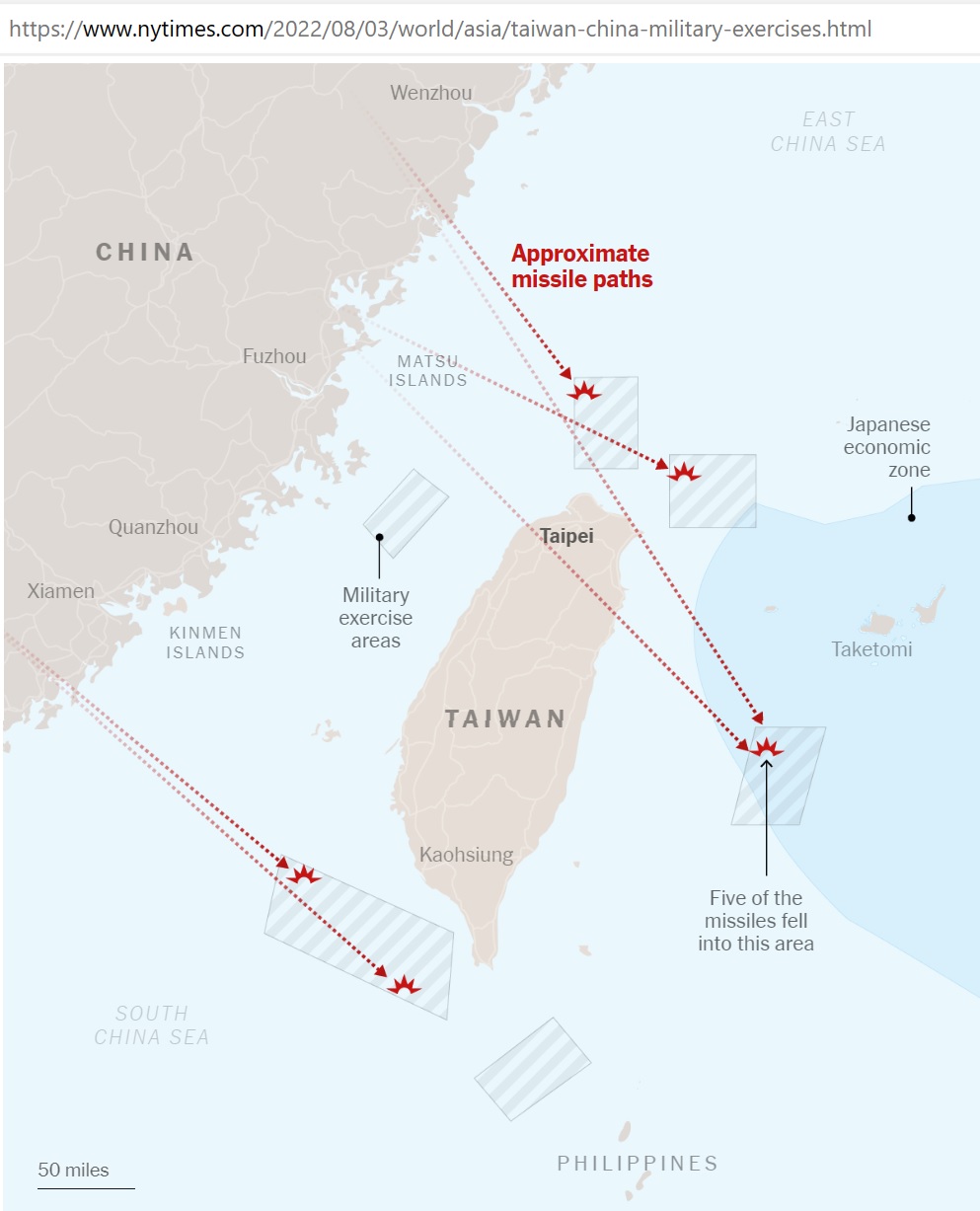

That is a problem because Chinese missiles have already hit this area in August 2022.

Fig 19: Chinese missile paths

Fig 19: Chinese missile paths

Chinese Missiles Strike Seas Off Taiwan, and Some Land Near Japan

3 Aug 22

https://www.nytimes.com/2022/08/03/world/asia/taiwan-china-military-exercises.html

Naval exercises of the PLA also took place in April 2023 east of Taiwan, also in Japanese waters.

Fig 20: Locations of aircraft carrier Shandong south of Miyako island

Fig 20: Locations of aircraft carrier Shandong south of Miyako island

(Map from Joint Staff Office of Japan’s Ministry of Defense)

U.S., Chinese Aircraft Carriers Operating Near Taiwan, Chinese Carrier Shandong Launched 80 Fighter Missions in Weekend Drills

10 Apr 2023

https://news.usni.org/2023/04/10/u-s-chinese-aircraft-carriers-operating-near-taiwan-chinese-carrier-shandong-launched-80-fighter-missions-in-weekend-drill

While writing this article:

China’s aircraft carriers play ‘theatrical’ role but pose little threat yet

5 May 2023

https://www.reuters.com/world/chinas-aircraft-carriers-play-theatrical-role-pose-little-threat-yet-2023-05-05/

Immediate media response:

China’s Shandong aircraft carrier group collaborates with Rocket Force, land-based aviation forces in 1st far sea exercise

7 May 2023

The Shandong aircraft carrier group of the Chinese People’s Liberation Army (PLA) Navy recently wrapped up its first far sea exercises in the West Pacific, in which it collaborated with the Rocket Force, land-based aviation forces and other surface combat units beyond the first island chain, as more details emerged to refute foreign media claims that Chinese carriers play only a “theatrical” role.

https://www.globaltimes.cn/page/202305/1290247.shtml

Fig 21: Diesel imports from China, Taiwan and Brunei

Fig 21: Diesel imports from China, Taiwan and Brunei

Let’s go through some scenarios:

(a) Blockade around Taiwan. This would not be specifically targeted at Australia but would reduce fuel imports (-9%)

(b) Due to the presence of China’s navy, tankers start to avoid the area, impacting China’s crude oil imports. China would stop fuel exports including Australia (-6%)

(c) Fights begin to break blockade including military action east of Taiwan. Tankers will divert away from the area, travelling longer distances to and from South Korea and Japan, impacting on 37% of Australian fuel imports. As a minimum, there will be delays in deliveries. Also, for the same volume of oil per month, more tankers are needed, leading to other problems depending on how far tankers would have to get around the area.

The Energy Market’s Next Crisis: Oil Tanker Shortages

14 Sep 2022

The war in Ukraine and the EU’s response to it have already livened up the global tanker market considerably – and with it, freight costs for hydrocarbons.

Few tankers have been built in the past few years, and since this is not something the industry can reverse overnight, supply will probably remain tight, pushing the cost of transporting oil and fuels higher.

https://oilprice.com/Energy/Energy-General/The-Energy-Markets-Next-Crisis-Oil-Tanker-Shortages.html

(d) Due to tanker shortages, China’s own oil imports get delayed requiring it to redirect fuel exports from its refinery in Brunei. Australia would suffer another -5% reduction in fuel imports. Up to this point not a single missile would have hit a tanker but 20% of Australia’s fuel imports would have gone and 37% of fuel imports would be delayed, with sharply increased transport costs.

An invasion of Taiwan with navy battles would be too hard to consider.

Of course, China itself would have to secure their oil imports:

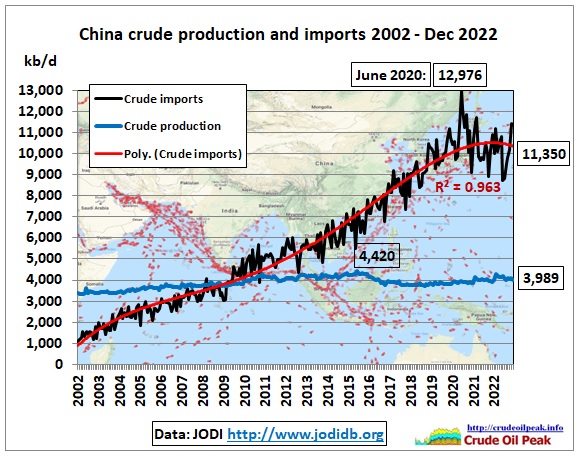

Fig 22: Chinese crude imports vs stagnating domestic production

Fig 22: Chinese crude imports vs stagnating domestic production

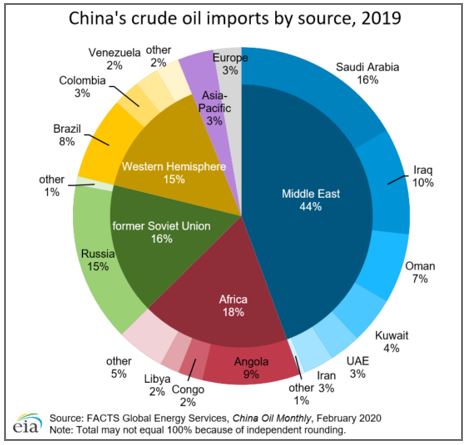

Fig 23: China’s crude imports by origin

Fig 23: China’s crude imports by origin

An article from the Centre on Global Energy Security (Columbia University) discusses a China energy import interdiction scenario. These are the main points:

• China is a major energy importer so a reduction of its energy imports will have reverse effects on markets than what is happening now with Russia.

• It is not clear what energy suppliers to China would do as their economies are exposed to these exports.

• Western based private oil and gas companies could use force majeure clauses to terminate sales in a war situation.

• Sanctions on shipping companies and insurance providers would be imposed in the same way as is now the case with Russia.

• China sits on a crude oil storage worth 100 days, a short time compared to potentially longer wars like we see in Ukraine.

• Removing China’s crude imports would have impacts similar to the early stages of Covid (oil price drops)

Potential Energy Challenges from a China-Taiwan Conflict Scenario

25 Jan 2023

A material number of current energy exporters might not embargo China in a major conflict, like a confrontation with Taiwan. But if such a conflict were to lead to a broader interdiction of energy imports to China, it would have considerable impacts on the Chinese economy—each year the country’s energy posture risk has been increasing. A full interdiction of seaborne energy imports into China could translate roughly to a 17 percent hit to China’s GDP, based on the energy intensity of the country’s economy and its import volumes, with significant impacts on the transportation, mining, and other sectors heavily dependent on oil and natural gas. And the amount of reduced China crude demand that this would cause could impact global crude markets more than the world experienced during the COVID market disruption, straining energy exporting nations in the process.

https://www.energypolicy.columbia.edu/publications/potential-energy-challenges-from-a-china-taiwan-conflict-scenario/

A full scale war around Taiwan would require tankers travelling in convoys like in WW2 over the Atlantic, accompanied and protected by naval forces. In this case, the whole South China Sea would have to be circumvented.

Consequences

If there is indeed only a 3 year window for fuel supply disruptions, there is no way that the introduction of EVs, electric buses and trucks will have proceeded sufficiently to make any material difference. For 20 years too many wrong decisions have been made. This cannot be corrected. The only thing which can be done is to not make the situation worse:

- Reduce immigration to a minimum because additional migrants will consume more fuels, especially urban elites

- Do not approve new oil consuming projects and structures like road tunnels, tollways, freeways and airports

- Prepare to bail out Transurban with more than $30 bn debt

For Sydney:

- Seriously think what to do with the works already done for the Western Sydney Airport

- Stop building the Metro tunnel to that airport

- Stop building the West Metro tunnel in Sydney which has the only function to serve new apartment towers, already vulnerable to volatile power generation. This tunnel could become a mushroom candidate in case of diesel shortages. It will be more important to use scarce diesel supplies for emergency vehicles, in agriculture, to transport food and other vital goods and for important energy projects like Snowy2

- Keep Sydney Trains in good working order. Do not convert the Bankstown line to a metro.

The proposed Fuel Council must immediately define and/or update priorities for fuel rationing. All State and Federal budgets must be reviewed and revised to minimise fuel consumption in the next 3 years.

Related posts:

13/4/2023

Australian jet fuel imports from China surge in 4 months to January 2023

http://crudeoilpeak.info/australian-jet-fuel-imports-from-china-surge-in-4-months-to-january-2023

5/8/2022

Australian diesel imports from Taiwan May 2022

http://crudeoilpeak.info/australian-diesel-imports-from-taiwan-may-2022

25 May 2022

Australian fuel import bill going sky-high

https://crudeoilpeak.info/australian-fuel-import-bill-going-sky-high

Australian Oil Stocks Consumption Cover

22 Mar 2022

https://crudeoilpeak.info/australian-oil-stocks-consumption-cover

9/12/2021

Australia crude oil import vulnerabilities Sep 2021 data

http://crudeoilpeak.info/australia-crude-oil-import-vulnerabilities-sep-2021-data