The IEA warns:

The prospect of large-scale disruptions to Russian oil production is threatening to create a global oil supply shock. We estimate that from April, 3 mb/d of Russian oil output could be shut in as sanctions take hold and buyers shun exports.

https://www.iea.org/reports/oil-market-report-march-2022

Are we prepared?

Covid has just taught us a lesson how vulnerable our supply chains can be. Empty shelves in shopping centres could also have been caused by diesel shortages.

Therefore, most important are diesel stocks. It’s not looking good.

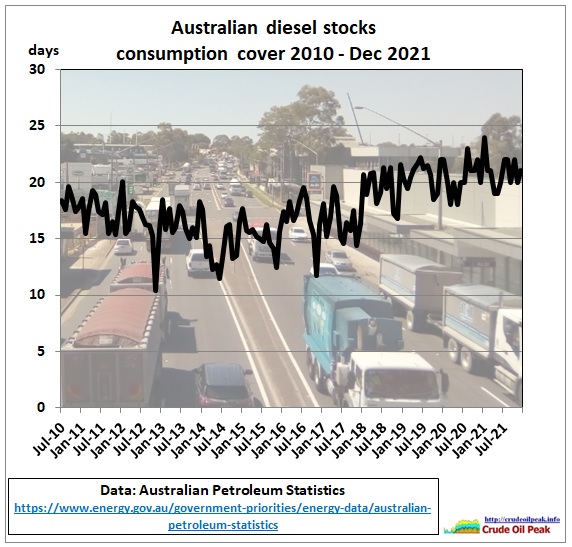

Fig 1: Diesel stocks will last just 3 weeks (table 7)

Fig 1: Diesel stocks will last just 3 weeks (table 7)

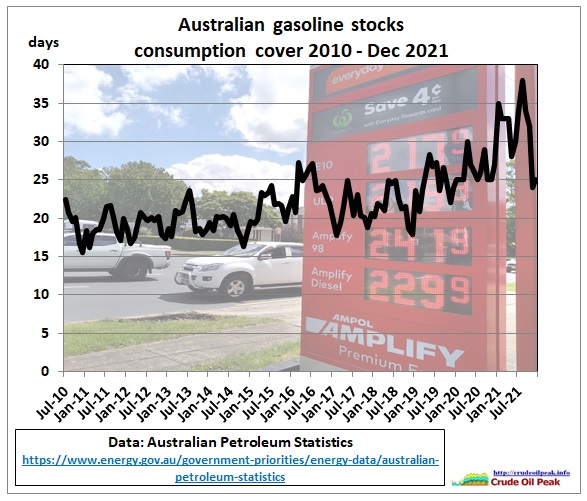

Fig 2: Gasoline stocks are highly variable depending on the arrival of imported cargoes

Fig 2: Gasoline stocks are highly variable depending on the arrival of imported cargoes

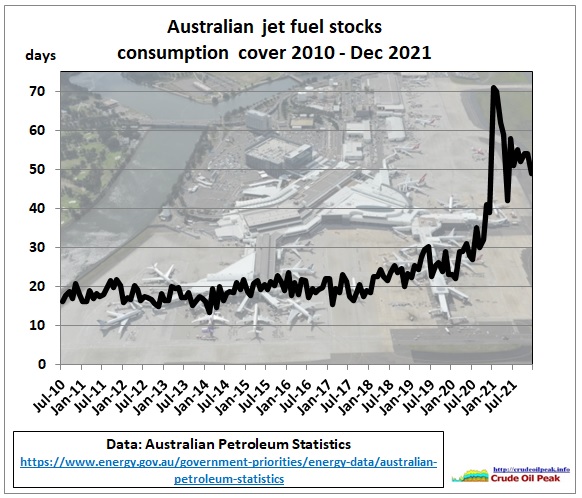

Fig 3: Lower jet fuel consumption during Covid increased coverage

Fig 3: Lower jet fuel consumption during Covid increased coverage

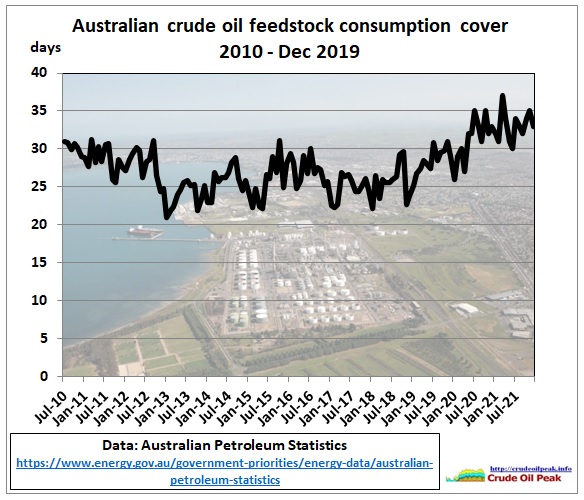

Fig 4: Crude feedstocks at refineries would last around 1 month

Fig 4: Crude feedstocks at refineries would last around 1 month

The increase of the crude consumption cover since 2018 is the result of both increasing feedstock and declining refinery input requirements due to closing refineries.

So we need to look at the actual volumes:

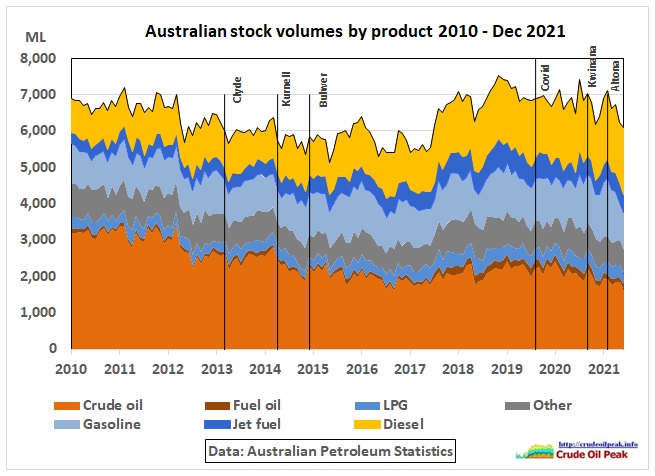

Fig 5: End of month stock volumes for crude and petroleum products

Fig 5: End of month stock volumes for crude and petroleum products

2021 averages:

Crude oil: 1,900 ML (trend down), gasoline: 1,300 ML, diesel: 1,700 ML

Crude stocks went down as was to be expected. These were replaced by increasing product volumes as previous refiners converted their crude storage to import terminals for products. On balance, however, total stock volumes are not higher than a decade ago.

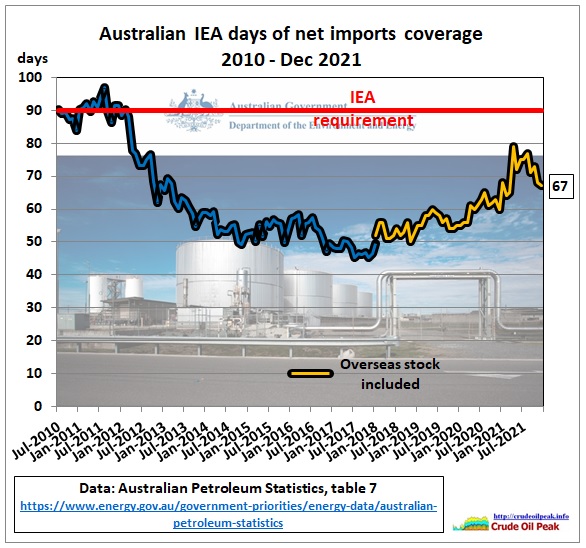

Instead of a consumption coverage, the IEA compares stocks to imports:

Fig 6: Net oil imports coverage as defined by the IEA

Fig 6: Net oil imports coverage as defined by the IEA

Liquid Fuel Security Review

Interim report

April 2019

“To date, the Government has chosen not to invest in domestic stock holdings. Building stocks is expensive regardless of whether they are industry-mandated or government-owned stocks. Australia’s own domestic production is reducing and our demand continues to grow. If there is greater transparency and oversight, Australians could have more confidence in the market. Industry and government could better respond to emerging supply issues which means less stock is required to effectively manage supply. The more information available to both buyers and sellers, the more likely the market will act more efficiently which may increase competition. Fuel companies each have a strong economic incentive to manage their own supply chain, no one has oversight of the whole market. Even with work under way for this review it is difficult for government to see the full picture of fuel supplies in Australia.” p 2

“….Australia’s domestic refinery capacity has reduced in response to oversupply in the global market; it is questionable whether large new oil refineries in Australia could be economically viable…” p 4

https://www.energy.gov.au/sites/default/files/liquid-fuel-security-review-interim-report.pdf

No. Refinery capacity was reduced because IOCs faced peak oil:

Australia’s BP Kwinana refinery closure: peak oil context

14 Nov 2020

https://crudeoilpeak.info/australias-bp-kwinana-refinery-closure-peak-oil-context

There was a change in the government’s thinking:

Australia to boost fuel security and establish national oil reserve

22 April 2020

https://www.minister.industry.gov.au/ministers/taylor/media-releases/australia-boost-fuel-security-and-establish-national-oil-reserve

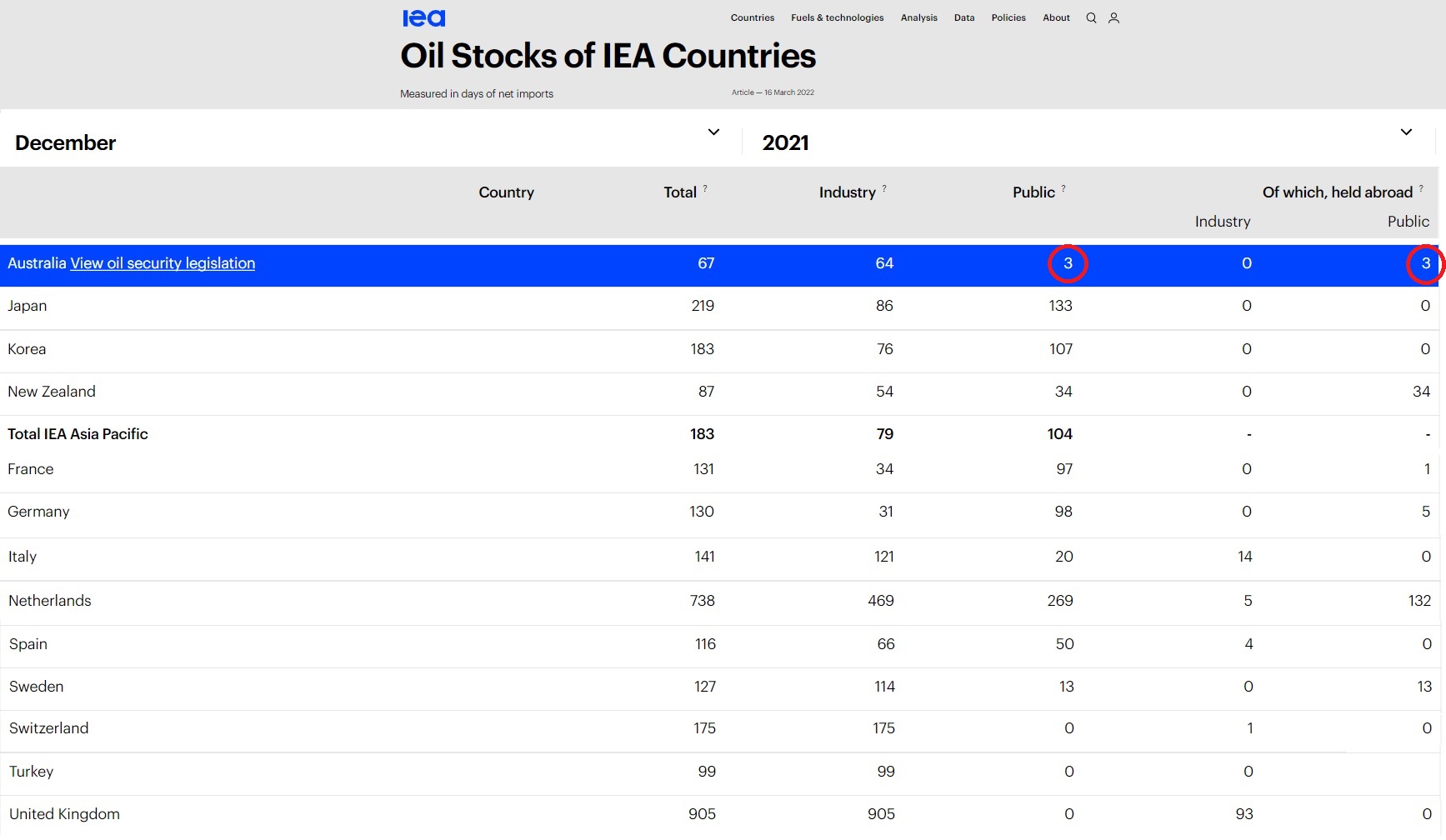

This crude oil reserve is included in the above graph (yellow line) but how much is it? 1.7 million barrels. 3 DAYS!!! It’s on the IEA website:

Fig 7: Australia’s public reserve: 3 days worth of oil for local refineries

Fig 7: Australia’s public reserve: 3 days worth of oil for local refineries

https://www.iea.org/articles/oil-stocks-of-iea-countries

FUEL SECURITY ACT 2021 (NO. 65, 2021)

30 June 2021

6 The Secretary notifies entities from time to time of the quantity of stocks of the MSO (Minimum stockholding obligation) product they are required to hold. The Secretary determines the quantity in accordance with the rules.

The rules in turn must provide for quantities to be determined by reference to a target number of days decided by the Minister. In deciding the target, the Minister must have regard to the emergency reserve commitment within the meaning of Article 2 of the International Energy Agreement (among other matters).

http://classic.austlii.edu.au/au/legis/cth/num_act/fsa2021173/

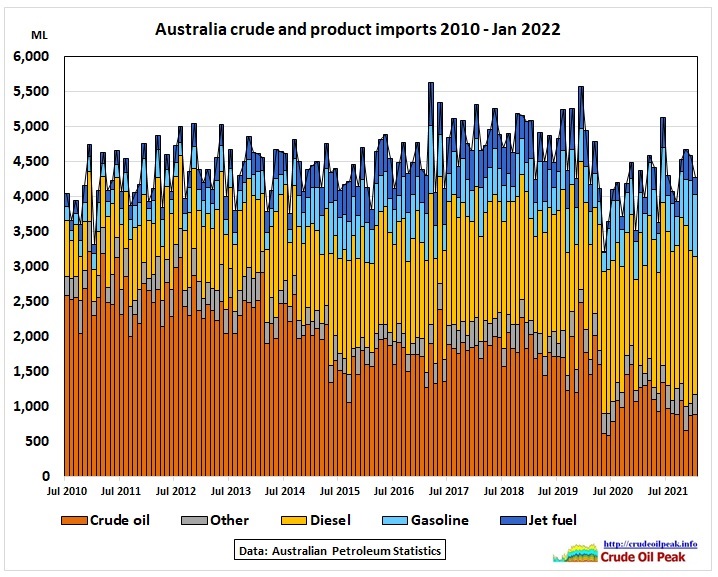

So let’s have a look at crude and product imports.

Fig 8: Crude and product imports

Fig 8: Crude and product imports

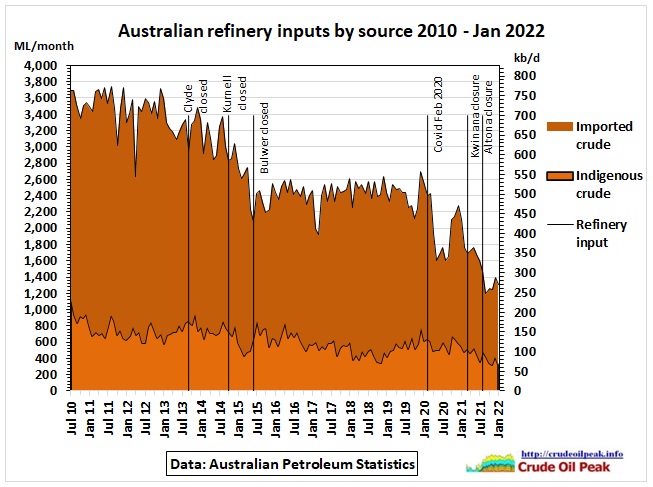

Fig 9: Imported and indigenous crude as refinery input

Fig 9: Imported and indigenous crude as refinery input

The percentage of indigenous crude usage has not changed and is around 25%.

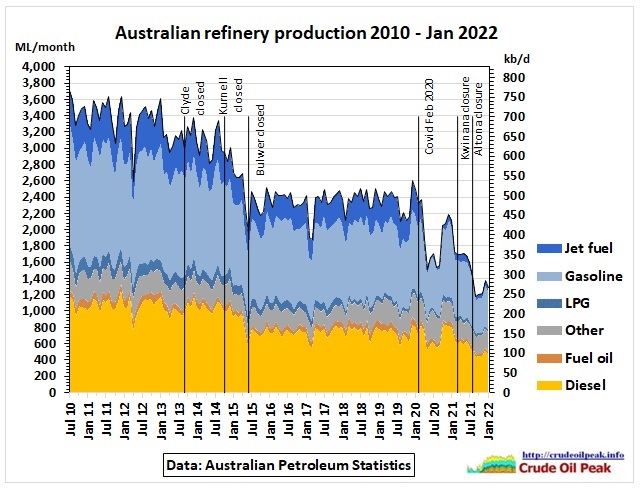

Refinery output by fuel

Fig 10: Over 10 years 2/3 of refinery output disappeared. Only 2 refineries remain

Fig 10: Over 10 years 2/3 of refinery output disappeared. Only 2 refineries remain

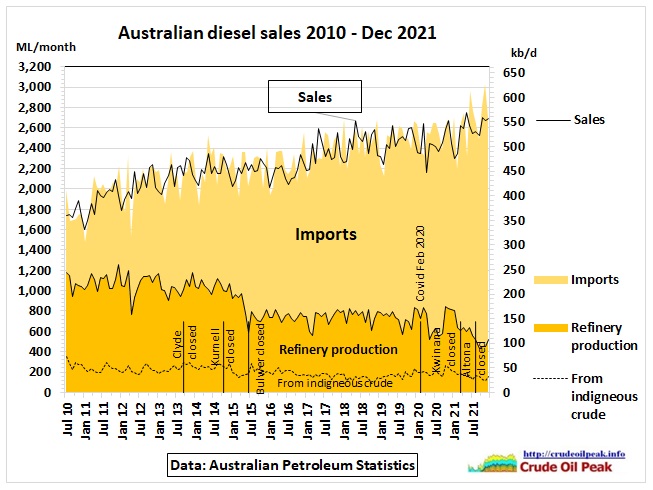

Fig 11: Diesel sales recovered after the Covid lockdowns

Fig 11: Diesel sales recovered after the Covid lockdowns

Note that indigenous crude is blended with imported crude at the ratio of around 1:3. In the above graph diesel from indigenous crude does not mean that this diesel can be refined from only indigenous crude.

Boosting Australia’s Diesel Storage Program

11 Jan – 3 Mar 2021 Grant applications

Provide matched funding to industry to construct new diesel storage that will result in an

estimated 780ML of additional diesel storage being kept onshore (no less than 20 megalitres in additional storage of diesel fuel at any individual site). This quantity is estimated to

be required for industry to meet the proposed minimum stockholding obligation by 2024.

Increasing Australia’s resilience through additional onshore diesel storage AU$260m

https://business.gov.au/grants-and-programs/boosting-australias-diesel-storage-program

Successful applicants:

73 ML $33m Qube Holdings Limited, Port Kembla Diesel Storage Project NSW

126 ML $33m Stolthaven Australia Pty Ltd, Diesel Fuels Storage Program – Stolthaven Newcastle

2 x 30 ML $17.13m Park Pty Ltd, Park Fuels: Port Kembla and Newcastle NSW

80 ML $30m Airport Development Group Pty Limited, Top End Diesel Storage Program NT

80 ML $28m Terminals Pty Ltd, Diesel Storage Expansion at Pelican Point (Adelaide) Terminal SA

90 ML $33m Viva Energy Refining Pty Ltd, Geelong Refinery Strategic Diesel Storage VIC

60 ML $26.97m Ampol Limited, Newport Diesel Storage Project VIC

100 ML $25.5m Coogee Chemicals Pty Ltd, Kwinana ADO Strategic Storage (KASS) WA

110 ML $33m Qube Holdings Limited, Lumsden Point Diesel Storage and Import Terminal WA

. https://www.vivaenergy.com.au/energy-hub/strategic-supply-and-storage

https://www.vivaenergy.com.au/energy-hub/strategic-supply-and-storage

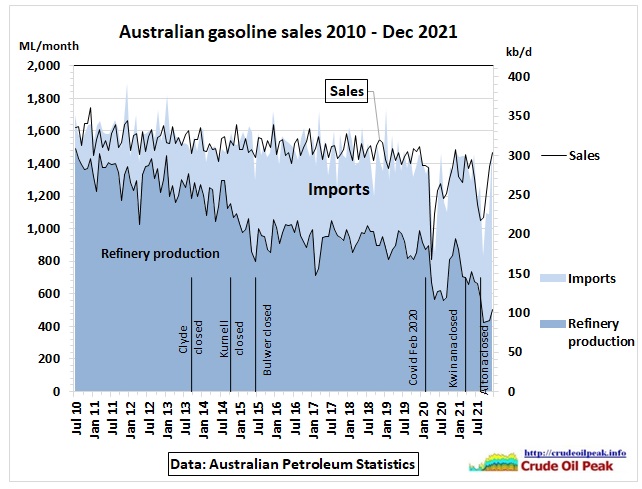

. Fig 12: Gasoline sales were on a 1.3% pa decline path before Covid

Fig 12: Gasoline sales were on a 1.3% pa decline path before Covid

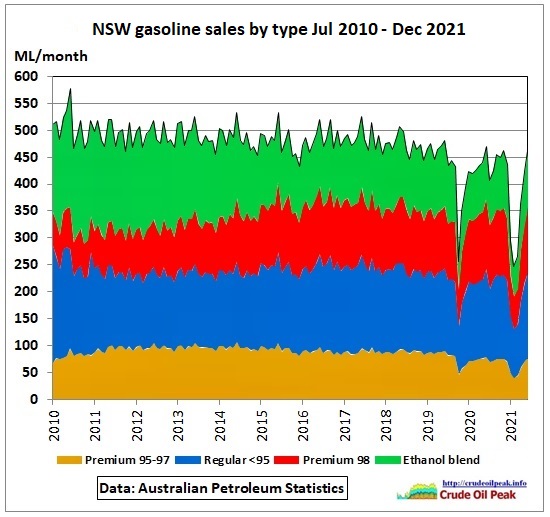

Fig 13: NSW gasoline sales by type: ethanol blend went down by 30%

Fig 13: NSW gasoline sales by type: ethanol blend went down by 30%

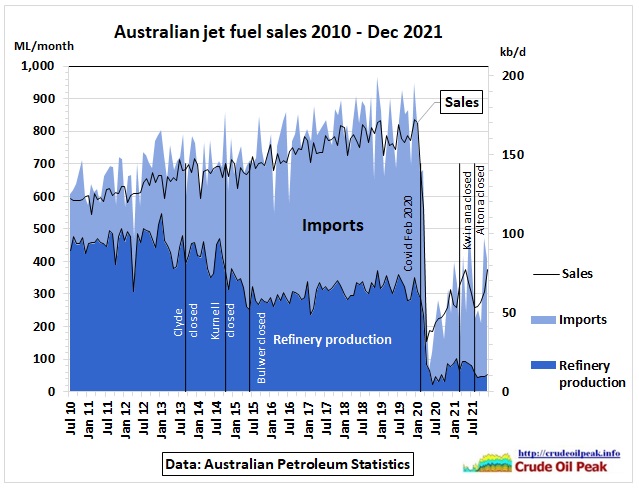

Fig 14: Jet fuel sales collapsed when the Wuhan virus hit

Fig 14: Jet fuel sales collapsed when the Wuhan virus hit

Summary:

Total stock volumes have not changed over a decade. The share of crude oil stocks has declined to around a quarter as a result of closing refineries. Therefore, product stocks have become very important.

Consumption coverage changes from month to month depending on the arrival of tankers but is around 1 month for crude and gasoline with a minimum of 24 days. The lowest coverage is for diesel with 21 days. The diesel storage program will increase this also to 1 month