U.S. Gathers the Most Air Power in the Mideast Since the 2003 Iraq Invasion

18 Feb 2026

U.S. is ready to strike Iran but President Trump hasn’t yet decided to do so

https://www.wsj.com/world/middle-east/u-s-gathers-the-most-air-power-in-the-mideast-since-the-2003-iraq-invasion-98ced89f

The 5 OPEC countries which are considered in this post are: Saudi Arabia, United Arab Emirates, Kuwait, Iraq and Iran. Data from the latest OPEC annual Statistical Bulletin 2025 cover the period 2012-2024.

https://www.opec.org/annual-statistical-bulletin.html

Qatar, Bahrain and Oman are not included in the ASB statistics.

Crude oil and Condensate only. Petroleum products are not included.

Fig 1: Crude and condensate exports from 5 OPEC countries

Fig 1: Crude and condensate exports from 5 OPEC countries

Total exports were almost 15 mb/d with China getting the biggest share (32%), followed by OECD Asia Pacific (21%), Other Asia (17%) and India (13%). This means that 83% of these exports go to Asia. Exports to OECD Europe and Americas have been in decline since 2017.

Now let’s look at more details of Fig 1:

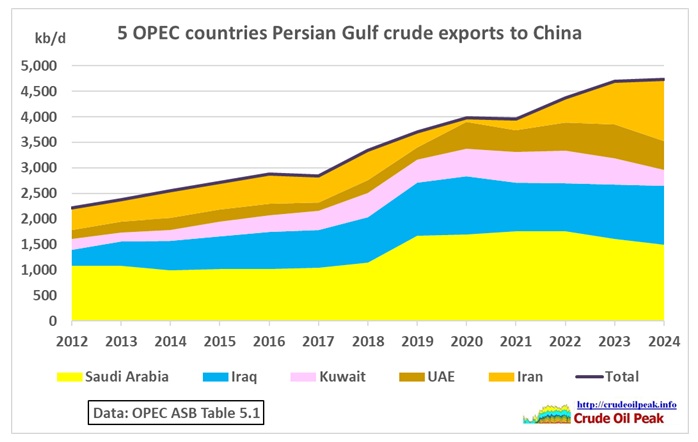

Fig 2: Crude exports to China: 4.7 mb/d in 2024

Fig 2: Crude exports to China: 4.7 mb/d in 2024

This graph represents the red area (32%) in Fig 1. We see that exports from Saudi Arabia and Iraq did not change much since 2019 and that recent growth has come entirely from Iran.

We keep the scale on the left hand side at 5 mb/d so that the oil flows in the following figures are comparable

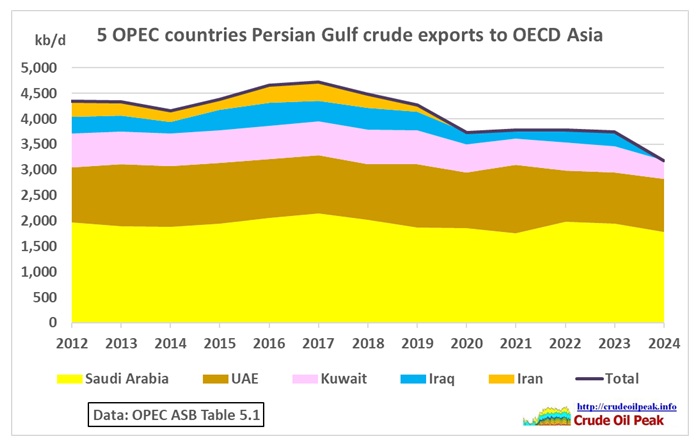

Fig 3: Crude exports to OECD Asia: 3.2 mb/d in 2024

Fig 3: Crude exports to OECD Asia: 3.2 mb/d in 2024

OECD countries in Asia include Japan, South Korea, Australia and New Zealand. This graph represents the light blue area (21%) in Fig 1. We can see that these countries have phased out imports from Iran completely in 2020.

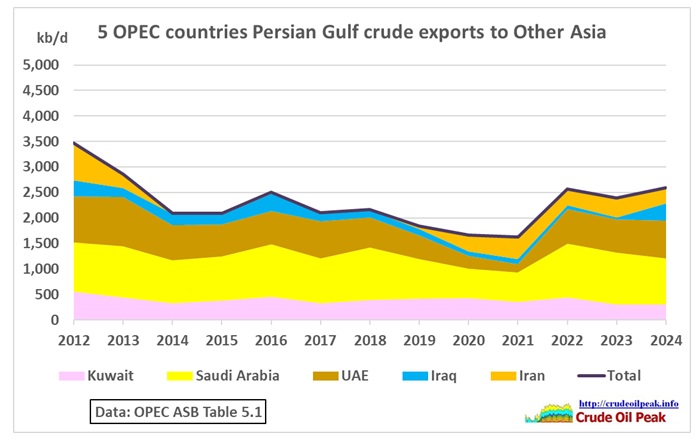

Fig 4: Crude exports to Other Asia: 2.6 mb/d in 2024

Fig 4: Crude exports to Other Asia: 2.6 mb/d in 2024

Other Asia includes Thailand, Vietnam, Malaysia, Singapore, Indonesia, Philippines and Pakistan. It represents the grey area (17%) in Fig 1.

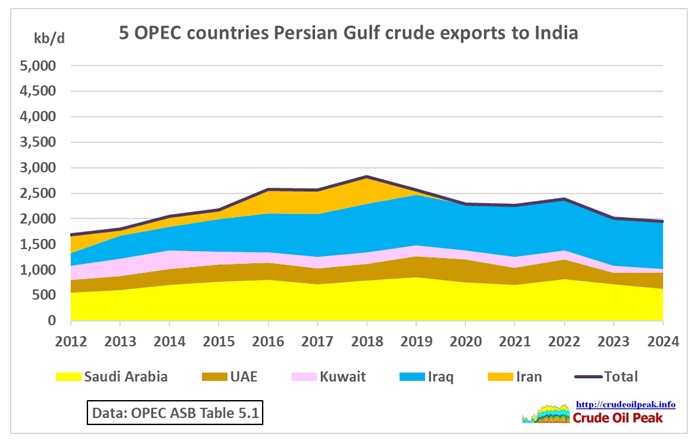

Fig 5: Crude exports to India: 1.9 mb/d in 2024

Fig 5: Crude exports to India: 1.9 mb/d in 2024

This graph shows the details for the green area (13%) in Fig 1. Exports from Iraq increased but exports from Iran ended in 2020.

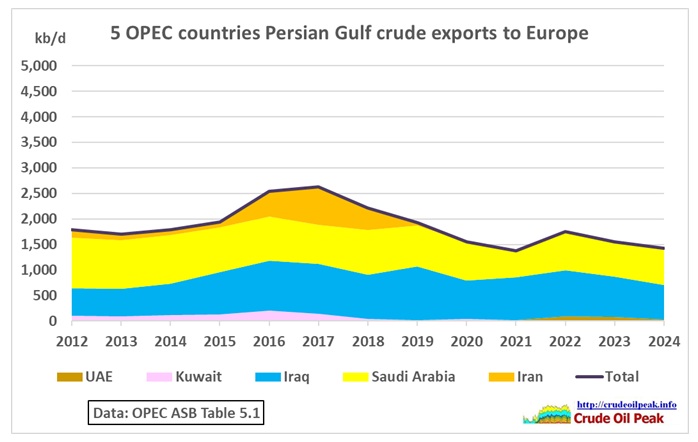

Fig 6: Crude exports to OECD Europe: 1.4 mb/d in 2024

Fig 6: Crude exports to OECD Europe: 1.4 mb/d in 2024

This is the dark blue area (10%) in Fig 1. These exports are dominated by Saudi Arabia and Iraq. Iranian exports lasted only for 4 years after the JCPOA (Iran nuclear deal) was agreed upon.

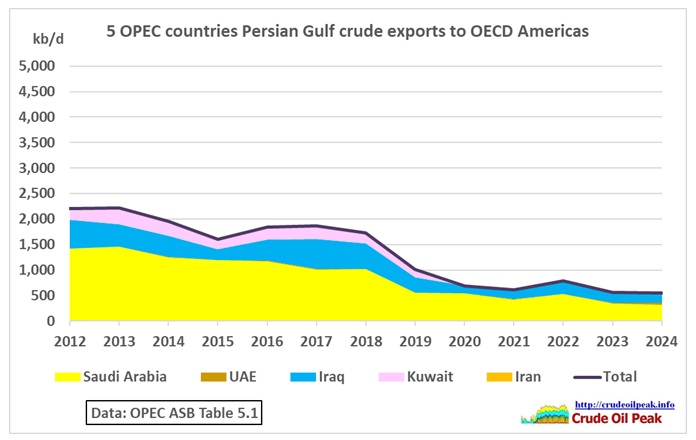

Fig 7: Crude exports to OECD Americas: 0.5 mb/d in 2024

Fig 7: Crude exports to OECD Americas: 0.5 mb/d in 2024

Crude exports to OECD Americas declined over 12 years

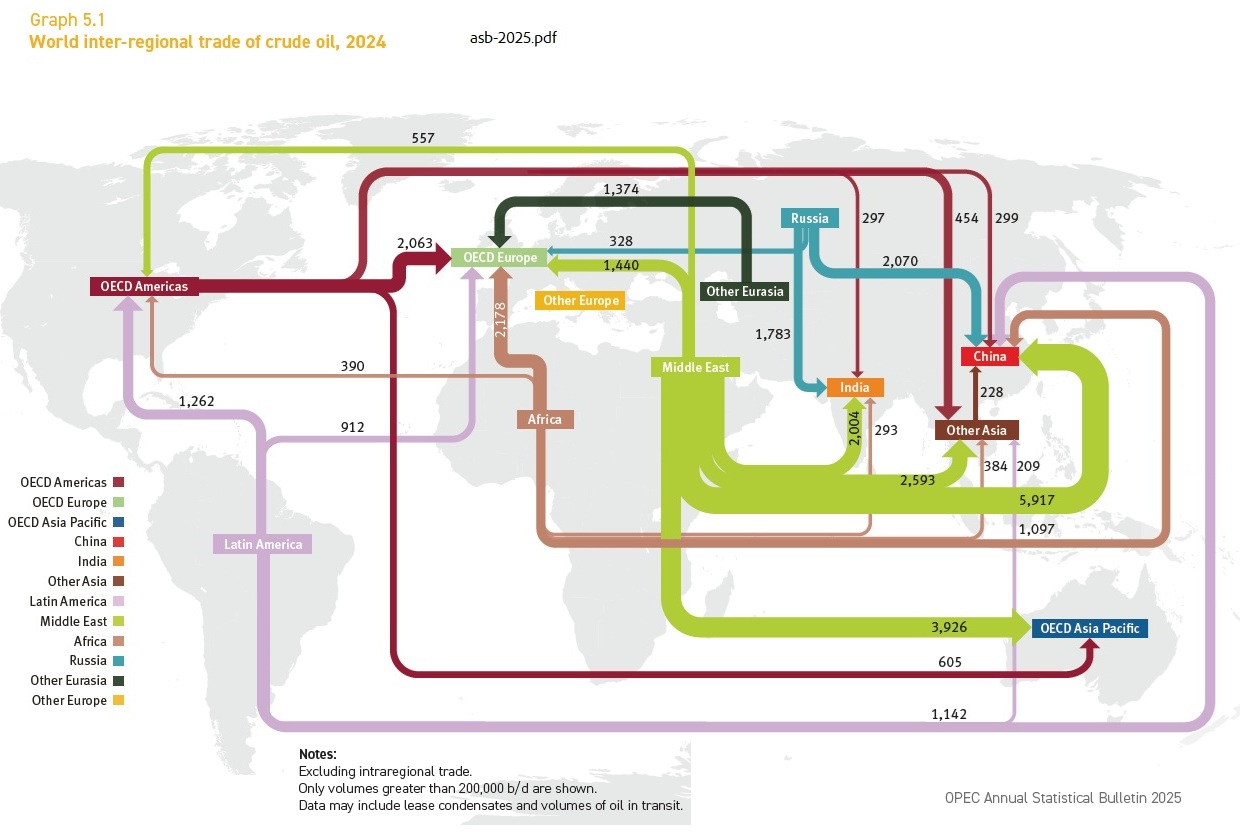

Fig 8: Global crude oil flows

Fig 8: Global crude oil flows

Asia is absolutely dependent on OPEC oil from the Middle East

Part 2

By exporting country

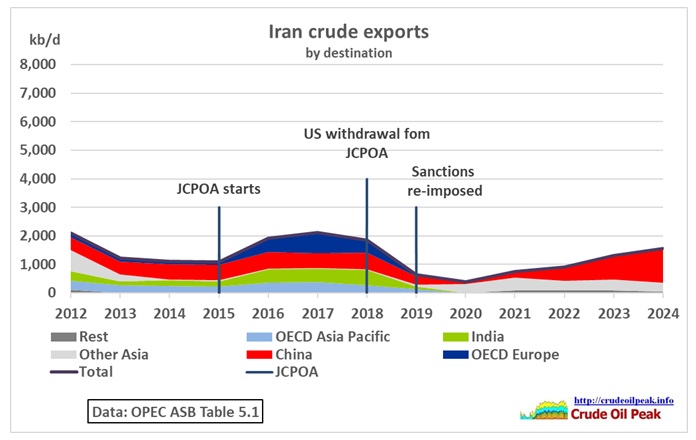

Fig 8: Crude exports from Iran

Fig 8: Crude exports from Iran

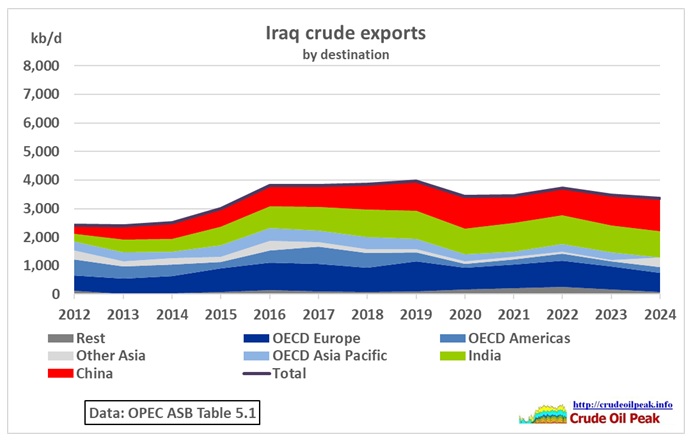

Fig 9: Crude exports from Iraq

Fig 9: Crude exports from Iraq

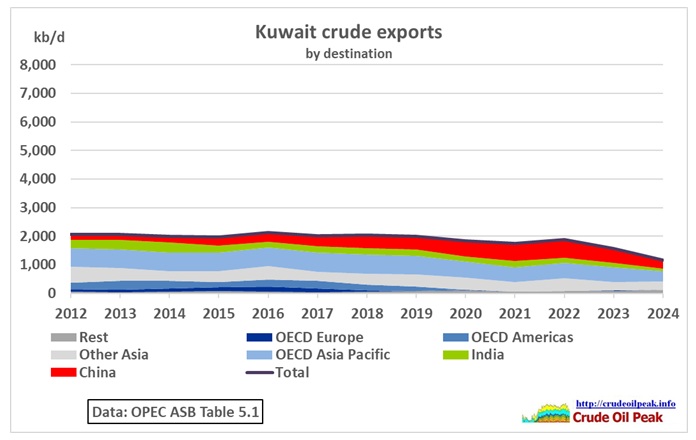

Fig 10: Crude exports from Kuwait

Fig 10: Crude exports from Kuwait

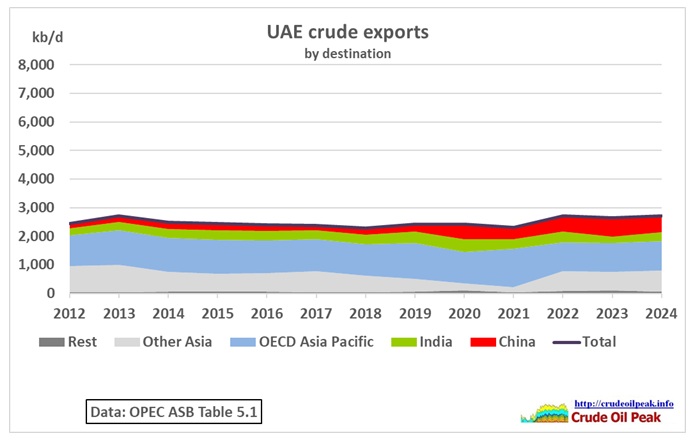

Fig 11: Crude exports from UAE

Fig 11: Crude exports from UAE

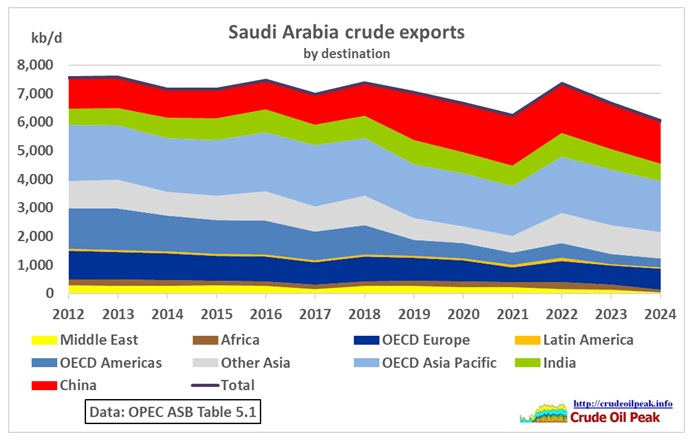

Fig 12: Crude exports from Saudi Arabia

Fig 12: Crude exports from Saudi Arabia

Related post:

1/10/2019

The Attacks on Abqaiq and Peak Oil in Ghawar

http://crudeoilpeak.info/the-attacks-on-abqaiq-and-peak-oil-in-ghawar

Alternative routes to the Strait of Hormuz

16 June 2025

Saudi Arabia and the UAE have some infrastructure in place that can bypass the Strait of Hormuz, which may somewhat mitigate any transit disruptions through the strait. The pipelines do not typically operate at full capacity, and we estimate that about 2.6 million b/d of capacity from the Saudi and UAE pipelines could be available to bypass the Strait of Hormuz in the event of a supply disruption.

Saudi Aramco operates the 5 million-b/d East-West crude oil pipeline, which runs from the Abqaiq oil processing center near the Persian Gulf to the Yanbu port on the Red Sea. Aramco temporarily expanded the pipeline’s capacity to 7.0 million b/d in 2019 when it converted some natural gas liquids pipelines to accept crude oil. In 2024, Saudi Arabia pumped more crude oil through the East-West pipeline to avoid the shipping disruptions around the Bab al-Mandeb.

![]()

The UAE also operates a pipeline that bypasses the Strait of Hormuz. This 1.8 million-b/d pipeline links onshore oil fields to the Fujairah export terminal in the Gulf of Oman. In 2024, crude oil and condensate volumes originating in the UAE and traversing Hormuz were 0.4 million b/d less than in 2022 because refinery upgrades allowed more heavy crude oil to be refined locally. These upgrades also allowed the UAE to increase exports of its lighter crude oil grades, and use of the pipeline to the Fujairah export terminal increased. Increased use of the pipeline for day-to-day operations has limited the excess capacity available to reroute additional volumes around the Strait of Hormuz.

Iran inaugurated the Goreh-Jask pipeline and the Jask export terminal on the Gulf of Oman (avoiding the Strait of Hormuz) with a single export cargo in July 2021. The pipeline’s effective capacity remains around 300,000 b/d. However, during the summer of 2024 Iran exported less than 70,000 b/d from ports (Bandar-e-Jask and Kooh Mobarak) using the Goreh-Jask pipeline and stopped loading cargoes after September 2024.