Update with data 2023

.

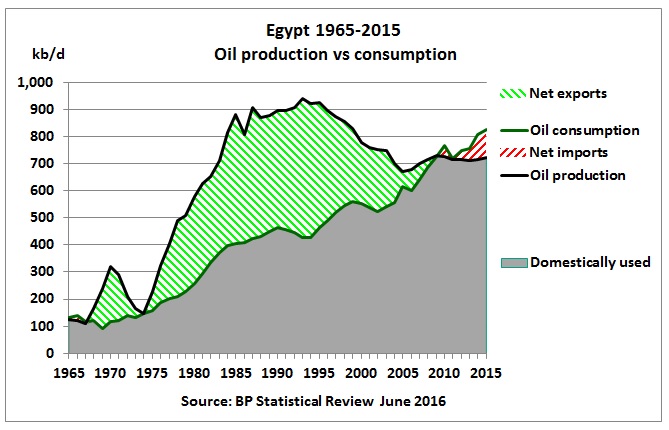

Update June 2016

Updated with data from BP Statistical Review June 2015

Updated June 2014 with data from BP Statistical Review 2014

Updated June 2014 with data up to December 2013

Data from: http://www.eia.gov/cfapps/ipdbproject/iedindex3.cfm?

Updated August 2013

Daily gas production/consumption

3/8/2013

Qatar has dispatched a tanker carrying liquefied natural gas (LNG) it is donating to Egypt, Qatar’s official news agency, QNA, said yesterday, the first of five shipments Doha has promised the troubled country which is struggling to meet its energy needs http://www.gulf-times.com/qatar/178/details/361607/qatar-sends-lng-aid-to-egypt

6/7/2013

Egypt’s future crude oil import requirements for 3 population scenarios  http://crudeoilpeak.info/egypts-future-crude-oil-import-requirements-for-3-population-scenarios

http://crudeoilpeak.info/egypts-future-crude-oil-import-requirements-for-3-population-scenarios

4/7/2013

2/3 of Egypt’s oil is gone 20 years after its peak

http://crudeoilpeak.info/23-of-egypt%e2%80%99s-oil-is-gone-20-years-after-its-peak

Updated June 2013

Egypt Struggles to Pay Oil Bill

October 3, 2012 Industry executives estimate that the government is $6 billion to $7 billion behind in payments to the companies for oil and natural gas they have produced and delivered to the state-owned Egypt General Petroleum Corp. “The burden has become very high on the Egyptian government,” said Magdi M. Nasrallah, a professor at the Department of Petroleum and Energy Engineering at American University in Cairo, and a consultant to energy companies operating in Egypt. “It has become dangerous because Egypt is buying the share of the joint ventures at international prices and selling this share on at subsidized prices.” http://www.nytimes.com/2012/10/04/world/middleeast/egypt-struggles-to-pay-oil-bill.html?pagewanted=all&_r=1&

2012

http://www.energianews.com/newsletter/files/cf2ce782c2dfad78f0cebfd40f8c8d8f.pdf

http://www.energianews.com/newsletter/files/cf2ce782c2dfad78f0cebfd40f8c8d8f.pdf

..

The situation is well described in Apache’s annual report 2012

page 7 Our operations in Egypt are conducted pursuant to production-sharing agreements in 23 separate concessions, under which the contractor partner pays all operating and capital expenditure costs for exploration and development. Development leases within concessions generally have a 25-year life, with extensions possible for additional commercial discoveries or on a negotiated basis, and currently have expiration dates ranging from five to 25 years. A percentage of the production on development leases, usually up to 40 percent, is available to the contractor partners to recover operating and capital expenditure costs, with the balance generally allocated between the contractor partners and Egyptian General Petroleum Corporation (EGPC) on a contractually defined basis. page 8: Oil from the Khalda Concession, the Qarun Concession, and other nearby Western Desert blocks is sold to third parties in the Mediterranean market or to EGPC when called upon to supply domestic demand. Oil sales are exported from or sold at one of two terminals on the northern coast of Egypt. Oil production that is presently sold to EGPC is sold on a spot basis priced at Brent with a monthly EGPC official differential applied. Apache purchases multi-year political risk insurance from the Overseas Private Investment Corporation (OPIC) and other highly rated international insurers covering a portion of its investments in Egypt. In the aggregate, these insurance policies, subject to the policy terms and conditions, provide approximately $1 billion of coverage to Apache for losses arising from confiscation, nationalization, and expropriation risks, with a $263 million sub-limit for currency inconvertibility.  http://www.apachecorp.com/investors/annual_report.aspx The IMF aks for a reduction in subsidies http://www.imf.org/external/np/exr/countryfacts/egy/ 2010 IMF report: http://www.imf.org/external/pubs/cat/longres.aspx?sk=23796.0 From the EIA:

http://www.apachecorp.com/investors/annual_report.aspx The IMF aks for a reduction in subsidies http://www.imf.org/external/np/exr/countryfacts/egy/ 2010 IMF report: http://www.imf.org/external/pubs/cat/longres.aspx?sk=23796.0 From the EIA:  ..

..  ..

..  Despite all the problems, Egypt exported 114 kb/d of crude oil

Despite all the problems, Egypt exported 114 kb/d of crude oil  http://www.eia.gov/countries/cab.cfm?fips=EG

http://www.eia.gov/countries/cab.cfm?fips=EG

Egypt’s crude oil production peaked 1995/96 and declined since then. Natural gas liquid production added from 2005 could not offset that decline. Total petroleum consumption increased by around 3% pa since then which required imports of crude and finished petroleum products. Egypt is now a net importer of both crude oil and finished petroleum products:

Egypt’s crude oil production peaked 1995/96 and declined since then. Natural gas liquid production added from 2005 could not offset that decline. Total petroleum consumption increased by around 3% pa since then which required imports of crude and finished petroleum products. Egypt is now a net importer of both crude oil and finished petroleum products:  Data for the above graph are from: http://www.eia.gov/cfapps/ipdbproject/iedindex3.cfm

Data for the above graph are from: http://www.eia.gov/cfapps/ipdbproject/iedindex3.cfm  This production profile is from the Energy Institute in UK: http://www.energyinst.org/home See also from Energy Files: http://www.energyfiles.com/imagesforecasts/egypt.11.jpg http://www.energyfiles.com/afrme/egypt.htmlSumed Pipeline

This production profile is from the Energy Institute in UK: http://www.energyinst.org/home See also from Energy Files: http://www.energyfiles.com/imagesforecasts/egypt.11.jpg http://www.energyfiles.com/afrme/egypt.htmlSumed Pipeline

{kind=link}

The Sumed pipeline runs 200-miles from Ain Sukhna on the Gulf of Suez to Sidi Kerir on theMediterranean. The Sumed’s original capacity was 1.6 million bbl/d, but with the completion of additional pumping stations, capacity has increased to 2.34 million bbl/d according to industry press. The pipeline is owned by the Arab Petroleum Pipeline Company (APP), a joint venture between EGPC (50 percent), Saudi Aramco (15 percent), a consortium of Kuwaiti companies (15 percent), the International Petroleum Investment Co of Abu Dhabi (15 percent), and Qatar (5 percent). According to APEX, oil flows through the Sumed pipeline in 2009 were 1.1 million bbl/d. This is down considerably from 2008 levels of 2.1 million bbl/d which can also be attributable to the oil market dynamics mentioned above. Closure of the Suez Canal and the Sumed Pipeline would divert tankers around the southern tip of Africa, the Cape of Good Hope, adding approximately 6,000 miles to transit time. http://www.eia.doe.gov/cabs/Egypt/Full.html————–

Egypt expects to up energy subsidies, maintain food subsidies

25/1/2011 Egypt is expected to spend LE 67.6 billion on petroleum subsidies by the end of the current financial year According to Beltone, food subsidies amount to around 4 percent of total spending, with wheat’s share at 3 percent, compared to energy subsidies, which represents more than 15 percent of total government spending and around 65 percent of total subsidies. She said that more funds for food subsidies should be raised by reducing energy subsidy spending. But talk about reductions in government energy subsidies which has come up over the past year has evaporated on now only appear to be increasing as world oil prices rise. Abdulla Ghorab, CEO of the Egyptian General Petroleum Corporation (EGPC), said that Egypt’s energy subsidy is expected to reach LE 86.8 billion for fiscal 2011/12 following a meeting with Minister of Petroleum, Sameh Fahmy earlier this week, according to the state-run Al-Ahram daily. http://www.masress.com/en/dailynews/127139 ====== related links ========== Impact on agriculture http://crudeoilpeak.info/egypt-diesel-shortages 31/1/2011 Egypt – the convergence of oil decline, political and socio-economic crisis http://crudeoilpeak.info/egypt-the-convergence-of-oil-decline-political-and-socio-economic-crisis