Update with 2023 data

Update July 2017

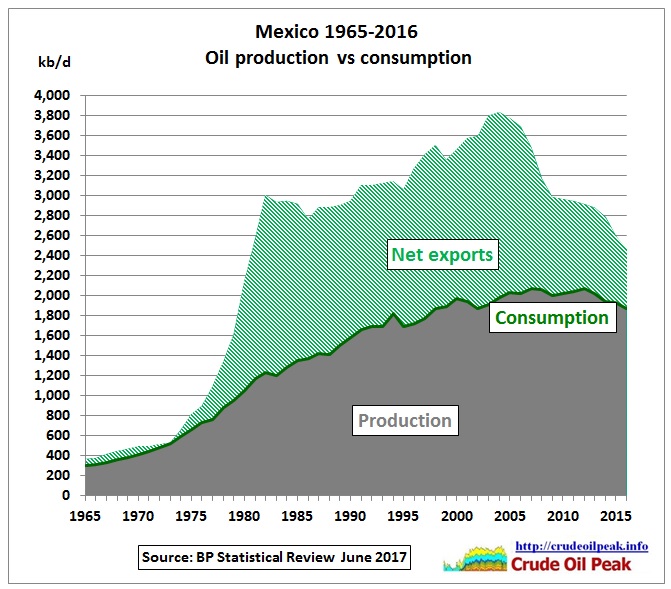

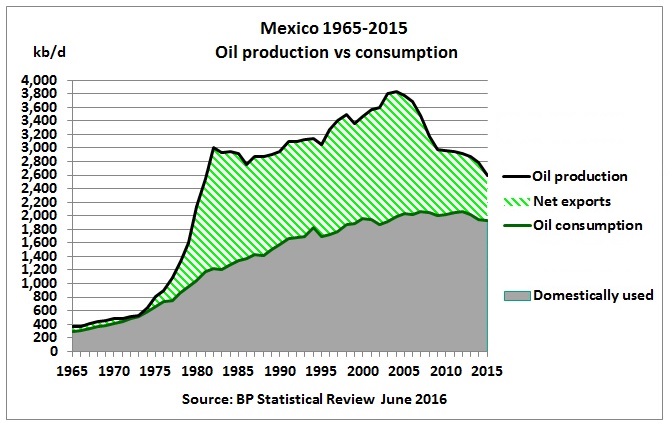

Using data from BP Statistical Review

Update May 2017

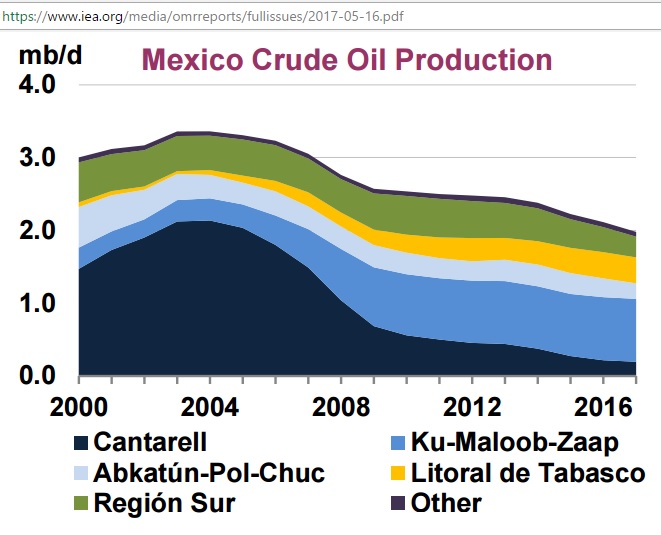

https://www.iea.org/media/omrreports/fullissues/2017-05-16.pdf

Update January 2017

Looting and riots erupt in Mexico as gas prices spike 20 percent in one weekend as the government stops regulating oil prices

5/1/2017

http://www.dailymail.co.uk/news/article-4089408/Mexican-president-defends-gas-price-hike-protests-spread.html

October 2016

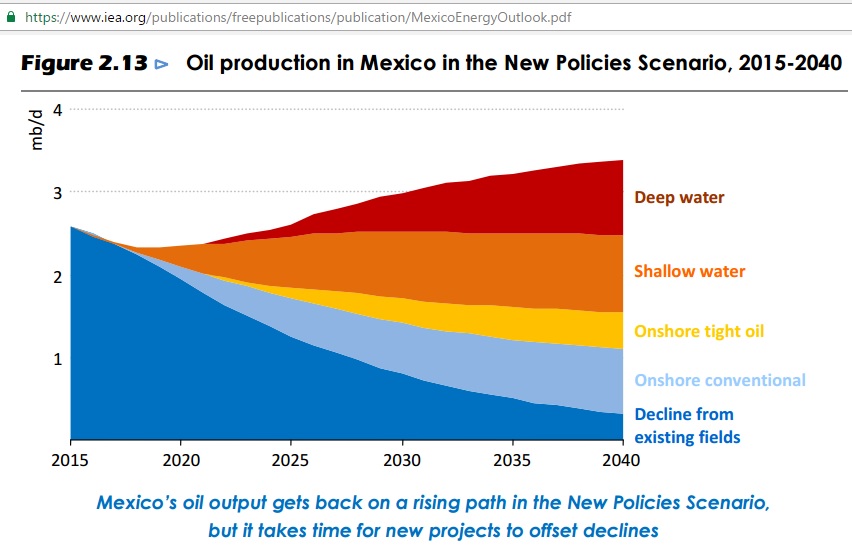

https://www.iea.org/publications/freepublications/publication/MexicoEnergyOutlook.pdf

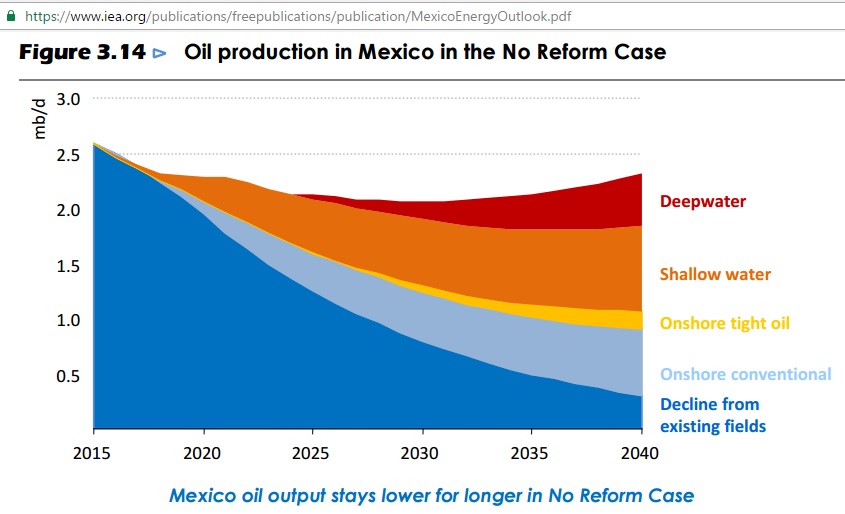

This Scenario is much more optimistic than the WEO 2014 (Fig 3.13 below). It assumes that Mexico’s oil industry reform is fully implemented.

Pemex reform bills were introduced in August 2014

https://www.brookings.edu/articles/mexicos-energy-reforms-become-law/

The IEA explains:

“The difference in projected oil production between the New Policies Scenario and the No Reform Case widens steadily over the period to 2040, by which time it exceeds 1 mb/d (2.3 mb/d versus the 3.4 mb/d reached in the New Policies Scenario) (Figure 3.14). The divergent trajectories take some time to become apparent, reflecting the lead times of the projects that are awarded in the New Policies Scenario but that fail to proceed in the No Reform Case. The key difference between the two trajectories is the amount of capital available for the upstream investment. In the New Policies Scenario, investment (and technology) comes from many sources. In the No Reform Case, the more limited capital available to PEMEX (especially in the current period of lower oil prices) needs to be spread over a wide range of assets, including capital-intensive deepwater projects. The company continues to do a commendable job (as it has done, for example, in exploring the deepwater Perdido area in the northern Gulf of Mexico), but the amount of upstream activity is significantly lower.”

Leftist Candidate Could Threaten Pemex Reforms.

12/8/2016

“A firebrand leftist who twice narrowly missed becoming Mexico’s president is riding high with a fresh bid for election in 2018, vowing to upend a landmark energy sector opening championed by President Enrique Pena Nieto”

http://www.maritime-executive.com/article/leftist-candidate-could-threaten-pemex-reforms

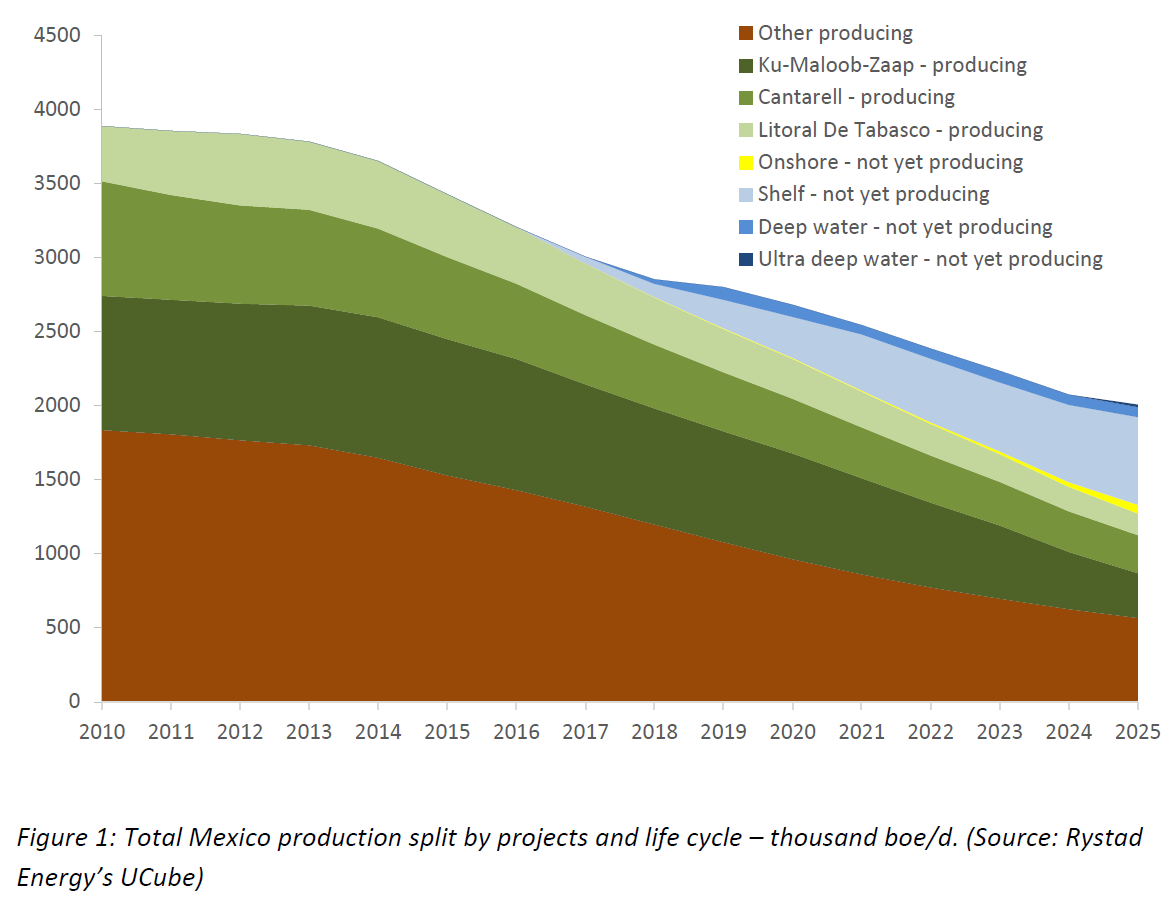

Both IEA scenarios are quite different from the Rystad graph shown below. The only agreement is on decline in producing fields.

June 2016

March 2016

Estimate from Rystad

“Figure 1 shows Mexico’s production, split by projects, life cycle and onshore/offshore from 2010 to 2025. Production is in decline, a trend driven mainly by the country’s supergiant offshore oil fields, Ku-Maloob-Zaap, Cantarell and Litoral De Tabasco. From 2016 and onwards, production is expected to continue declining, but at a slower pace, thanks to substantial contribution from the new discoveries in the Litoral De Tabasco (Xikin, Esah and Batsil) and Cantarell (Cheek), infill drilling at Ku as well as the deepwater project Lakach. ”

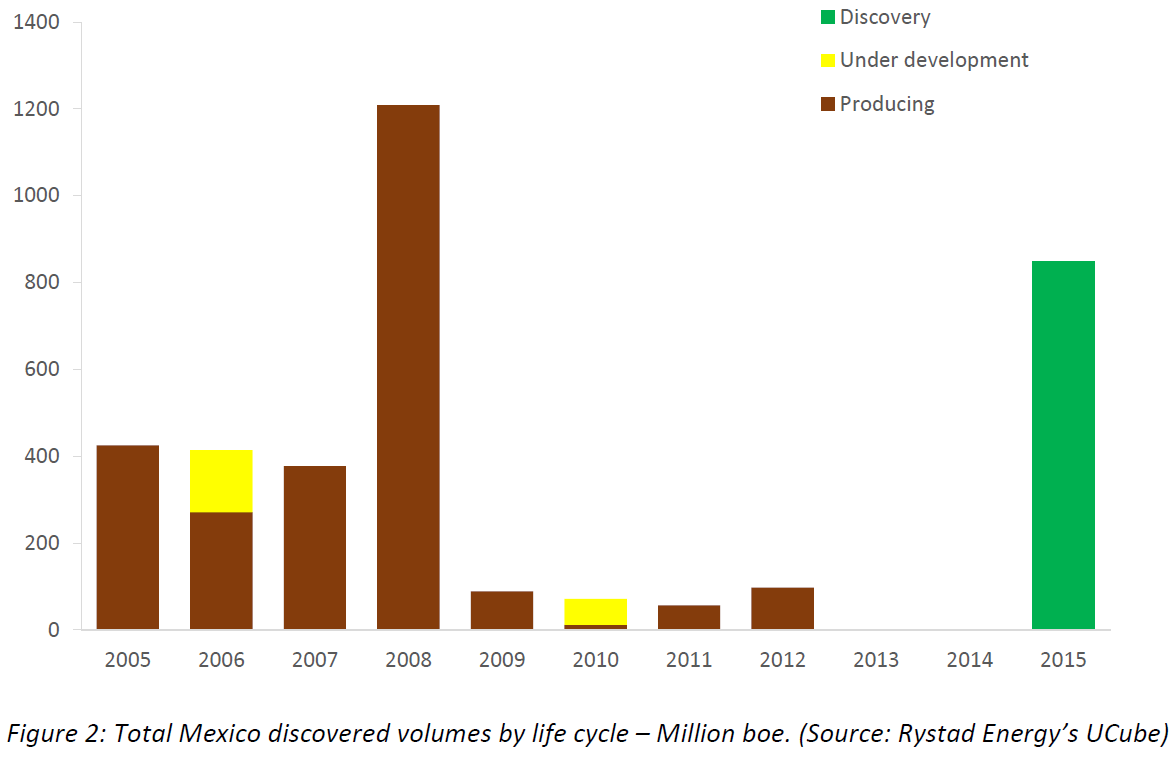

Figure 2 shows the discovered volumes for Mexico from 2005 to 2015. The year with the highest discovered volumes in the last decade was 2008. Two major discoveries, Ayatsil-Tekel and Tsimin (Litoral De Tabasco), make up around 60% of the 2008 discovered resources. After three years of low exploration success, Pemex discovered the deep water Kunah, Trion and Puskon fields in 2012. None of these discoveries, however, are expected to be put into production before 2025 and are not considered to be commercial at the current oil price forecast (and are not shown in Figure 2).

http://www.rystadenergy.com/NewsEvents/PressReleases/are-mexicos-2015-discoveries-enough

January 2016

http://www.eia.gov/todayinenergy/detail.cfm?id=24112

http://www.eia.gov/todayinenergy/detail.cfm?id=24112

November 2014

http://www.worldenergyoutlook.org/weo2014/

June 2014

December 2013

Data from here: http://www.eia.gov/cfapps/ipdbproject/iedindex3.cfm?

.

http://docs.dpaq.de/5859-the_missing_piece_unlock_103265274.pdf

June 2013

February 2012

Mexico: time for action

2010

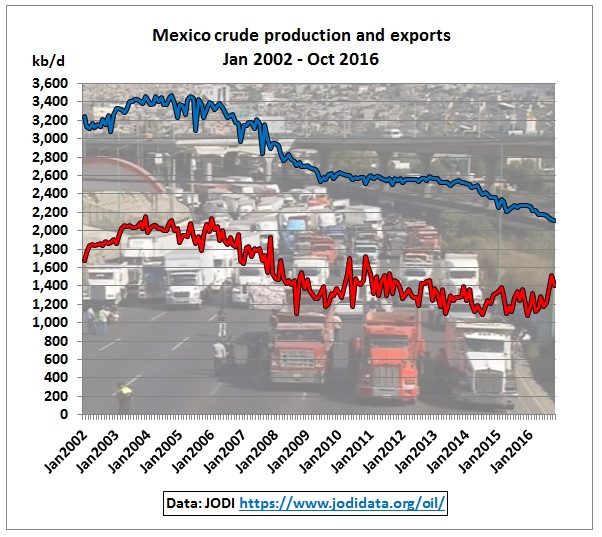

Crude oil exports declined by 800 Kb/d between 2004 amd 2009, mainly caused by the peaking of the Cantarell field

Source of data: http://www.eia.gov/cfapps/ipdbproject/iedindex3.cfm?

Source of data: http://www.eia.gov/cfapps/ipdbproject/iedindex3.cfm?

Heavy Maya crude, around 60% of total Mexican production is exported to the US which has the refining capacity for this oil. More details here:

http://www.eia.gov/cabs/Mexico/Full.html