Fig 1: The conventional crude oil plateau started in 2005

At the end of the high oil price period in June 2014, Virgin Australia had liabilities of $ 4.7 bn. Despite lower oil prices it never got rid of that debt. Instead it increased by another $ 2.1 bn.

Fig 2: Virgin liabilities vs Brent oil price

This post is an update of:

Despite growth in passenger numbers Virgin Australia can’t make money since 2009

12/2/2014 (with data up to 2013)

http://crudeoilpeak.info/despite-passenger-growth-virgin-australia-cant-make-money-since-2009

All airlines are hit by the impact of the Corona virus but Virgin had problems before travel restrictions were introduced. High debt – accumulated over more than 10 years – is among the main reasons why voluntary administration was unavoidable.

Virgin Australia owes almost $7 billion to more than 12,000 creditors

We compare Virgin’s profits and losses with oil prices:

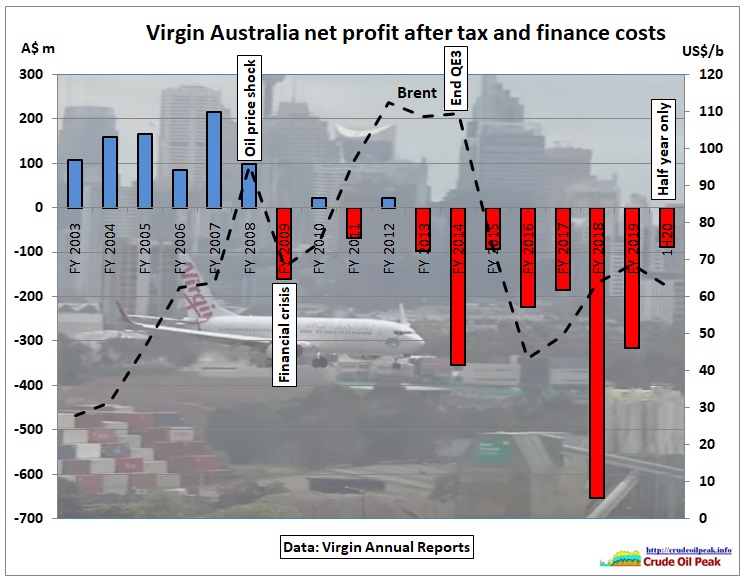

Fig 3: Profit/loss vs Brent oil price FY 2003-FY 2019

It is clear that Virgin went into the red after the oil price shock in 2008.

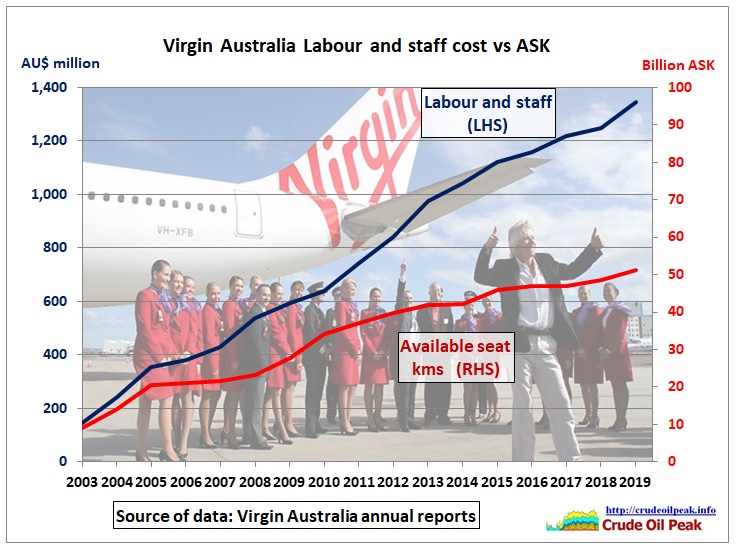

How have Virgin’s losses come about? The next graph shows how operating expenditure consumed the revenue. The 3 main cost components are fuel, airport charges and staff expenses. All have increased over the years, more than the number of available and revenue seat kms.

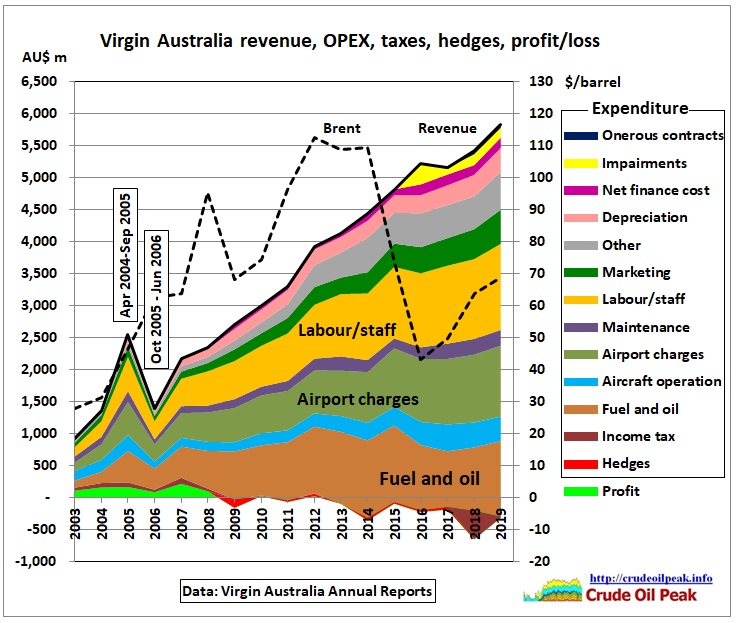

Fig 4: Virgin Revenue, Operating expenditure and profit/losses

Note that the irregularities in 2005/06 were caused by changes in the reporting periods.

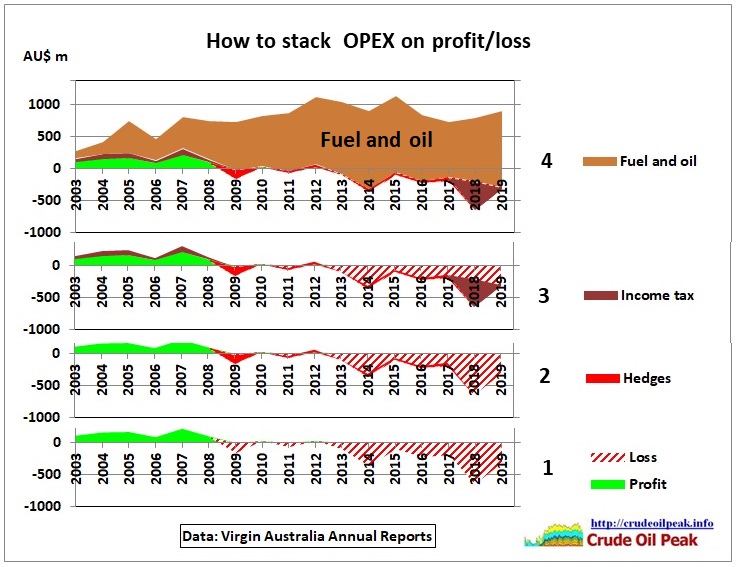

Fig 5: Stacking on negative areas hides the losses

At the bottom we start with profits and losses (1) then stack hedges (2), income tax (3) and fuel (4).

The large loss in 2018 includes a tax expense of $m 452 resulting from a derecognition of deferred tax assets ($m 511) which had accumulated since 2009 (see note B5, Annual Report 2018, p62).

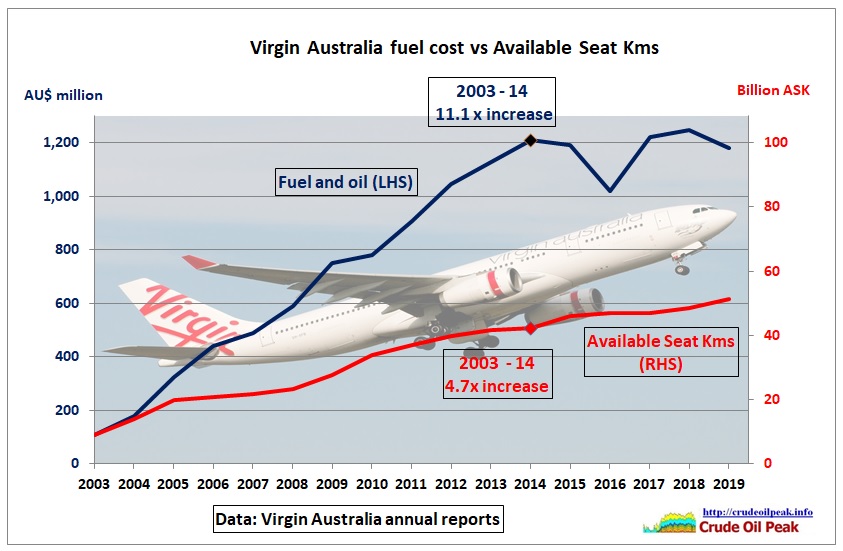

Virgin Blue started in August 2000. A year later, 9/11 rattled the airline industry as passengers feared more hijackings. Virgin benefited from the liquidation of Ansett in 2002 but the competitor Jet Star entered the market in 2003. Then oil prices went up as the North Sea started its inevitable decline and the Iraq war did not stop the crude oil peak in 2005. It was not a good time to start and grow an airline. The following graph shows that fuel costs increased much more than available seat kms right from 2004:

Fig 6: Virgin cost of fuel: up, up and away

From the 2009 annual report

During the year, the net loss arising from fuel hedging activities for the Group was $250.4 million (2008: gain of $93.2 million) as a result of actual fuel prices moving lower than the average hedged price. Of this net amount, a loss of $147.9 million (2008: gain of $74.1 million) represents the effective portion of the hedges which has been recognised in fuel expense, and a loss of $102.5 million (2008: gain of $19.1 million) represents the ineffective portion of the hedges (including changes in option time value) which has been recognised in ineffective and non-designated derivatives expense.

https://www.virginaustralia.com/au/en/about-us/company-overview/investor-information/annual-reports/

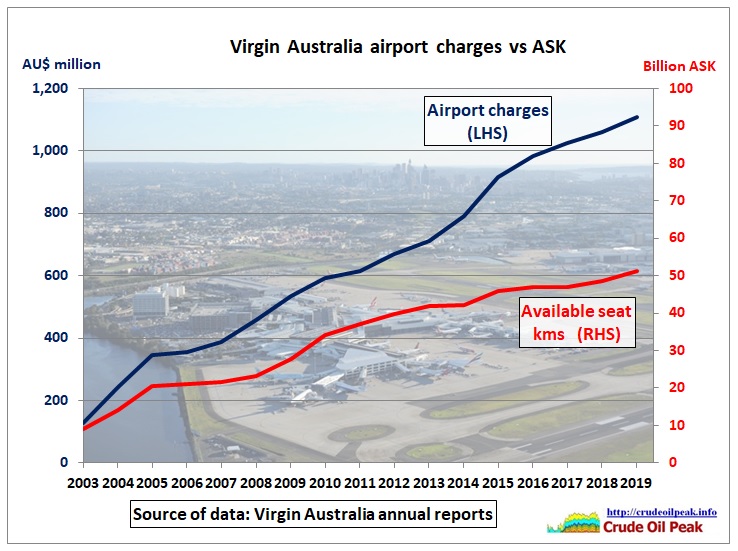

So it’s not just the high cost of fuel but also the volatility of oil prices. There was also a huge gap developing between the growth in airport charges and available seat kms.

Fig 7: An airport boom is not cheap

Qantas, Virgin bosses say lack of monopoly regulation on airports squeezing consumers and airlines dry

19 Sep 2019

The two big airline bosses will visit Canberra on Wednesday to urge Treasurer Josh Frydenberg to regulate airports to stop them charging excessive landing fees.

Virgin chief executive Paul Scurrah said airports have charged his airline an extra $109 million over the last three years. It’s a unicorn,” Qantas chief executive Alan Joyce told AM.

https://www.abc.net.au/news/2019-09-18/qantas-virgin-ceo-airports-monopoly-regulation/11522056

Fig 8: Growth at all cost

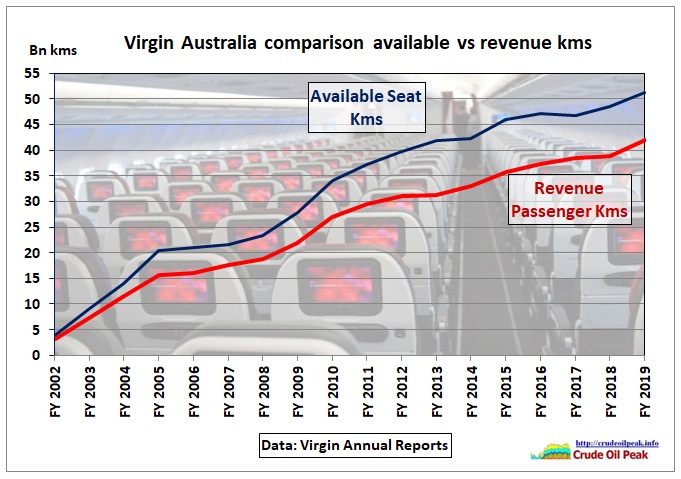

Fig 9: Widening gap between ASKs and RPKs

Apart from the increase in costs, available seats could not be filled. The revenue load factor decreased from 81.3% in 2002 to 75.6% in 2013 but then recovered to 80% in 2018. Jetstar in that year had a load factor of 85%.

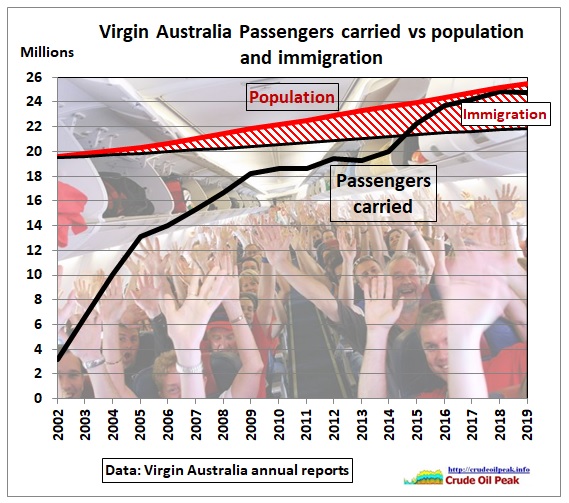

Fig 10: Passenger growth slowed down for 5 years after 2009

The overall growth from 3 million passengers in 2002 to 25 million in 2019 is impressive if not crazy. Every resident takes 1 flight per annum. Population growth was 30%, mainly driven by immigration which fuels travel demand to and from the countries of origin. A continuation of this trend is unsustainable irrespective of the impact of the Corona virus.

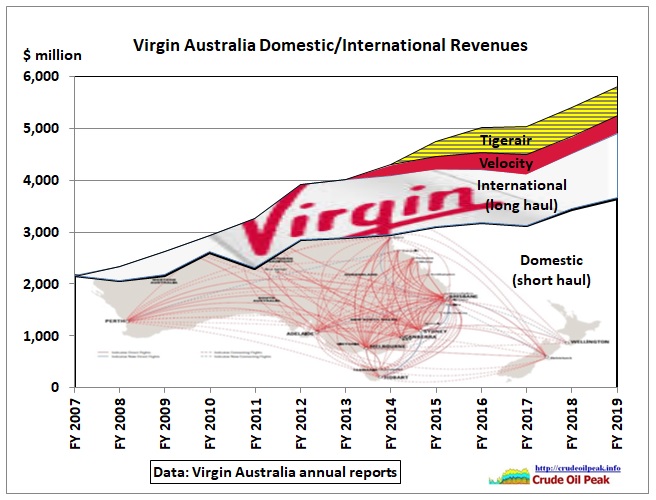

A lot of the passenger growth came from Virgin adding international business to its domestic base.

Fig 11: A risk too big: expanding into international markets in difficult times

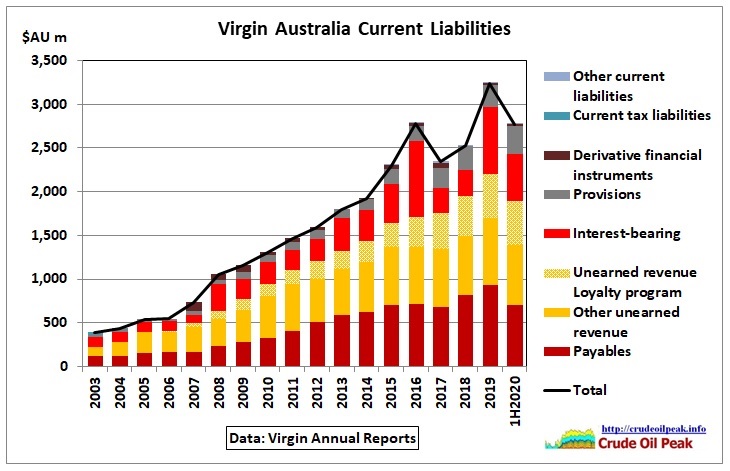

Fig 12: Current liabilities (due in the following financial year)

We see that current liabilities entered into a higher growth path in and after the oil shock year 2008. The growth in unearned revenue is amazing. This comprises revenue from passenger ticket sales received in advance of carriage and is classified as current (tickets are expected to be used within 12 months)

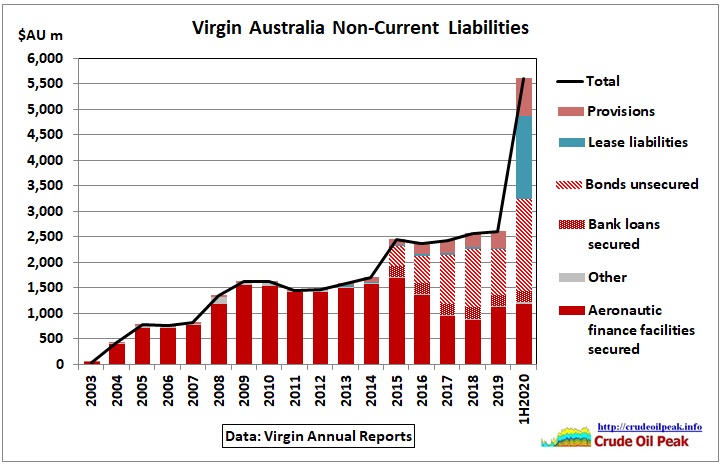

Fig 13: Non-current liabilities

In 2015 Virgin began to issue unsecured bonds, starting with US$300 million in the US bond market, at a fixed interest rate of 8.5%. This was a period in which oil prices had dropped i.a. because QE3 had ended in 2014. These bonds matured on 15th November 2019. They were paid back by newly issued unsecured notes of US$ 425 m to institutional investors.

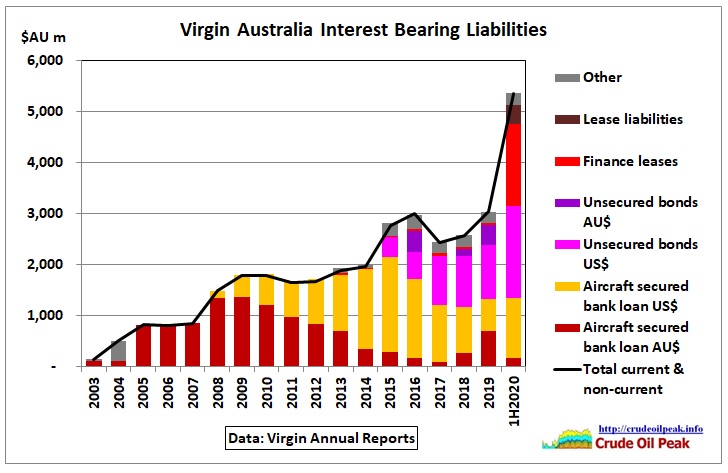

We extract interest bearing liabilities from Fig 12 and Fig 13.

Fig 14: Current and non-current interest bearing liabilities by type

We can see that aeronautic finance facilities more than doubled in 2008, in line with the growing fleet (see Fig 15). AU $ denominated bank loans were then replaced by US$ loans. In 2015, unsecured bonds were introduced.

The last half yearly report notes:

“Bonds – unsecured

During the half year ended 31 December 2019, the Group issued AU$325 m of unsecured notes in the Australian retail market and US$ 425 m of unsecured notes to institutional investors. The proceeds of these bonds were primarily used to acquire the non-controlling interests in Velocity Frequent Flyer Holdco Pty Ltd and for the repayment of a US$ 400 m bond during the period.”

So debt was rolled over and increased into more risky areas.

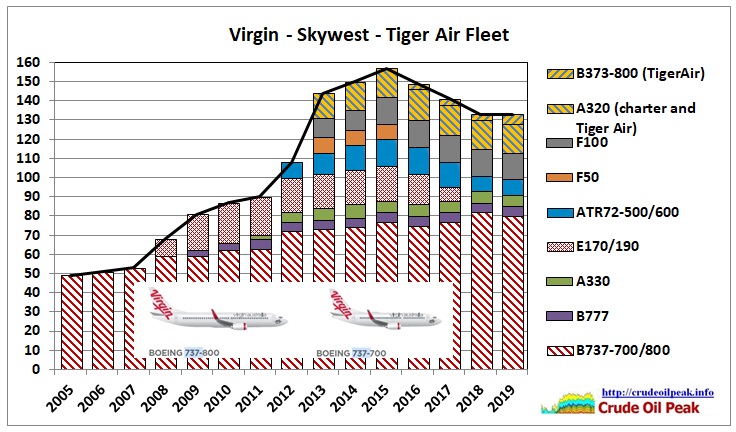

Fig 15: History of Virgin’s fleet

In 2006, Virgin ordered 20 Embraer E-Jets from Brazil. This was a time when peak oil research was intensifying. The Australian Senate conducted an inquiry into oil supplies in that year.

The Embraer jets were sold just 10 years later, to cut costs.

In 2013, during the high oil price period brought about by the so-called US shale oil revolution, Virgin acquired the fleet from Skywest (Perth), increasing its regional and FIFO capacity during the mining construction boom. That came to an end when oil prices dropped after the world economy could no longer afford high oil prices. At the same time US refineries could no longer absorb the extra light US shale oil which ended up in inventories.

No guidance from Australian governments

In June 2004, Prime Minister Howard had written in his totally flawed energy white paper that there are sufficient global oil supplies for 40 years, the term “sufficient” of course implying that oil prices would not go through the roof as they did.

http://crudeoilpeak.info/critique-of-energy-white-paper-june-2004

At the Sydney Writer’s Festival in July 2008 the future Prime Minister Tony Abbott thought peak oil is an arcane concept:

3/12/2009 New Liberal leader did not know what peak oil is

http://crudeoilpeak.info/new-liberal-leader-tony-abbott-did-not-know-what-peak-oil-is

To be fair, the Rudd government wasn’t better by 1 barrel when refusing to release an internal peak oil report:

24/2/2012 Australian Government kicks own goals in Senate peak oil debate (peaky leaks part 3)

Conclusion:

Imprudent decisions were made more than 15 years ago. The 1st phase of peak oil which started in 2005 (under Howard’s watch) damaged the balance sheet of Virgin Australia. The Corona virus exposed this weakness. The Australian government is reluctant to bail out Virgin in this situation. This is ironic because they asked for it. If successive Australian governments had analysed, understood and accepted peak oil, they would have advised the airline industry (and other oil dependent sectors of the economy including banks) to be careful with their investments and to not assume continuing growth. Then losses could have been minimized.