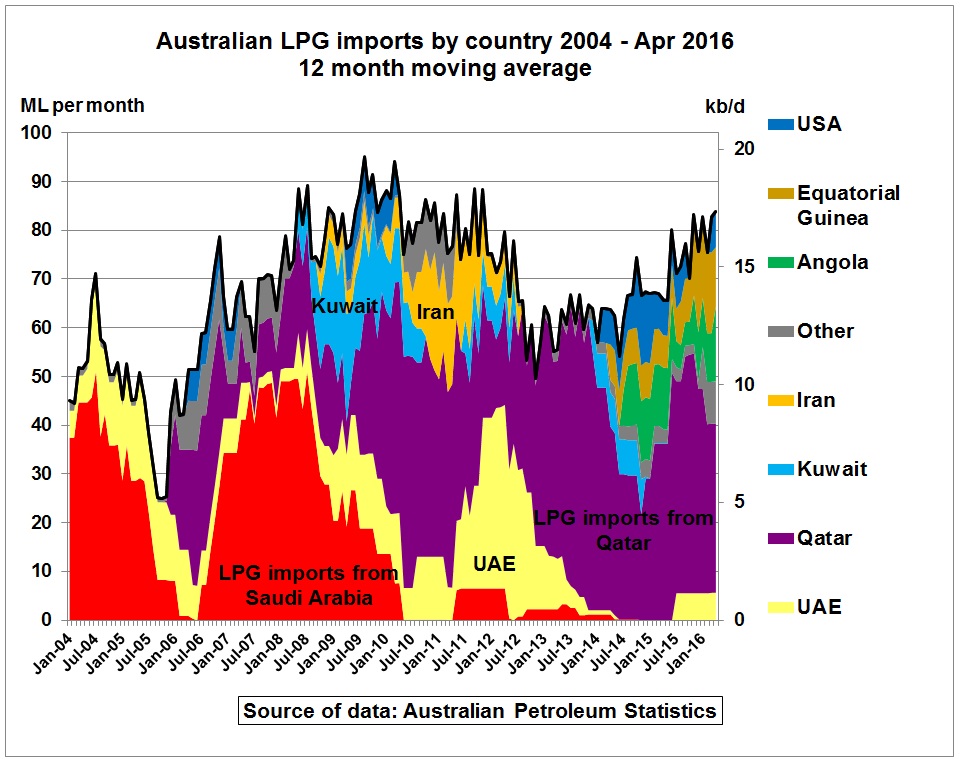

Update July 2016

Update Jan 2014

http://omrpublic.iea.org/omrarchive/21jan2014fullpub.pdf

http://omrpublic.iea.org/omrarchive/21jan2014fullpub.pdf

..

.

http://omrpublic.iea.org/omrarchive/11dec2013fullpub.pdf

The LPG Vehicle Scheme closes on 30 June 2014

http://www.ausindustry.gov.au/programs/energy-fuels/lpgvs/Pages/default.aspx

LPG vehicles

February 2012

industry statistics

Gas Energy Australia and Victorian Automobile Chamber of Commerce

SUBMISSION TO THE PRODUCTIVITY COMMISSION INQUIRY INTO AUSTRALIA’S AUTOMOTIVE MANUFACTURING INDUSTRY

Dec 2013

ABS figures show that in 2001, LPG vehicles made up 2.5% of the light vehicle fleet, peaking at 3.4% in 2010, and declining over recent years to 3.1% in 2013. This has resulted from a reduction in sales of domestically produced factory fitted vehicles and a decline of retrofitted LPG conversions…

The Federal Government’s LPG Vehicle Scheme (LPGVS) (as detailed in section 1.6) is now less effective in encouraging the purchase of new LPG vehicles and LPG aftermarket conversions. Applications received by the Federal Government’s LPGVS in FY12 were 68% below the allocated cap of 25,000, with estimates for the current year likely be 95% below the same cap. In response to this, Recommendation 4 addresses the issue to assist it through the medium term transition process.

The price differential between ULP and LPG more closely correlated with the demand of the LPGVS between 2006 and the early stages of 2009. Despite a relative consistent average price differential over time, there now appears to be consumer disconnect between the price differential and the uptake of the LPGVS, likely based around the relative stability in the ULP price, which is seen as a short term effect.

http://www.pc.gov.au/__data/assets/pdf_file/0012/130503/sub076-automotive.pdf

..

In 2011/12 LPG production was 10% of total liquids production in terms of energy content

.

http://www.caradvice.com.au/15576/lpg-holden-commodore-now-only-400-more/

http://www.caradvice.com.au/15576/lpg-holden-commodore-now-only-400-more/

(1) AERA repor, chapter 3 Oil

http://ga.gov.au/image_cache/GA16759.pdf

The LPG resource data of the AERA report do not differentiate between propane and butane. This would be very important as that will impact on the availability of automotive LPG, which should not contain more than 60% butane in a propane/butane mix[1]. Australia has an excess production of butane. LPG supplies to regional centres (both automotive and domestic) are mostly propane for logistic reasons while some big cities can afford separate storage facilities for propane and butane. Therefore, the total availability of locally produced (naturally occurring) automotive LPG will be limited by the production of propane.

The LPG resource data of the AERA report do not differentiate between propane and butane. This would be very important as that will impact on the availability of automotive LPG, which should not contain more than 60% butane in a propane/butane mix[1]. Australia has an excess production of butane. LPG supplies to regional centres (both automotive and domestic) are mostly propane for logistic reasons while some big cities can afford separate storage facilities for propane and butane. Therefore, the total availability of locally produced (naturally occurring) automotive LPG will be limited by the production of propane.

This issue of propane deficient LPG where excess butane must be exported was mentioned in the 2007 report of the Senate Inquiry on oil supplies on page 104 (items 6.79 and 6.80) but not resolved.[2]

There is also the problem of West coast LPG supply surpluses and East coast shortfalls best described in LPGA’s submission 100 to the Energy White Paper:

“….the Port Botany storage is configured to handle large shipments of propane only…It will seek VLGCs fully loaded with 44 kt of propane…It is more economical to import propane to the east coast from overseas and export both propane and butane produced in the west to international markets” [3]

The appendix 1 of LPGA’s submission contains a list of propane and butane storage facilities. The only sizeable butane storage tanks are in (all refrigerated):

- Port Bonython (SA, 30 kt)

- Westernport (VIC, 55 kt)

- Dampier (WA, 36 kt)

- Kwinana (WA, 15 kt)

This is ABARE’s forecast for LPG dated December 2006[4]

Compare the 1,078 PJ of crude and condensate for 2030 with 400 PJ given in Fig 3.43 of the AERA report and that gives you some idea how reliable the LPG figures would be. Actual LPG production in 2010-11 was 106 PJ, not 142 PJ

http://bree.gov.au/publications/australian-energy-statistics/2013-australian-energy-statistics-data

What’s more, Australia’s capacity for LPG conversions is limited. The automotive industry does not have enough licensed gas mechanics. In 2008:

Queue up for LPG conversions

http://www.carsguide.com.au/site/news-and-reviews/car-news/queue_up_for_lpg_conversion

…

(2) Bill to tax LPG – May 2011

Inquiry into the taxation of alternative fuels bill

http://www.aph.gov.au/house/committee/economics/TaxingFuels/index.htm

Discussion in the House of Reps 2/6/2011

http://www.aph.gov.au/hansard/reps/dailys/dr020611.pdf

Draft Bill

http://www.treasury.gov.au/documents/1944/PDF/Aa_exposure_draft_tax_alt_fuels_bill.pdf

..

..

——————

Related reading:

AIP’s supply reliability[5]

Structure of the Australian petroleum industry[6]

——————

[1] http://www.environment.gov.au/atmosphere/fuelquality/publications/pubs/lpg-fuel-quality-standard-discussion-paper.pdf