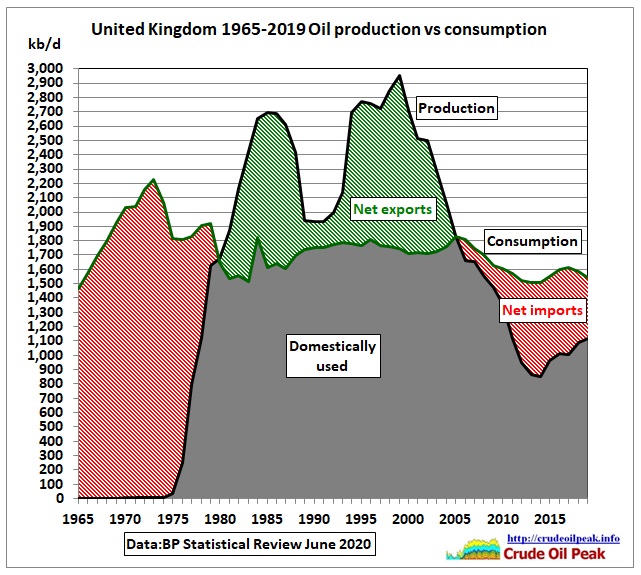

June 2020

Dec 2019

https://www.ogauthority.co.uk/media/6681/uk_oil-gas-rr_2020.pdf

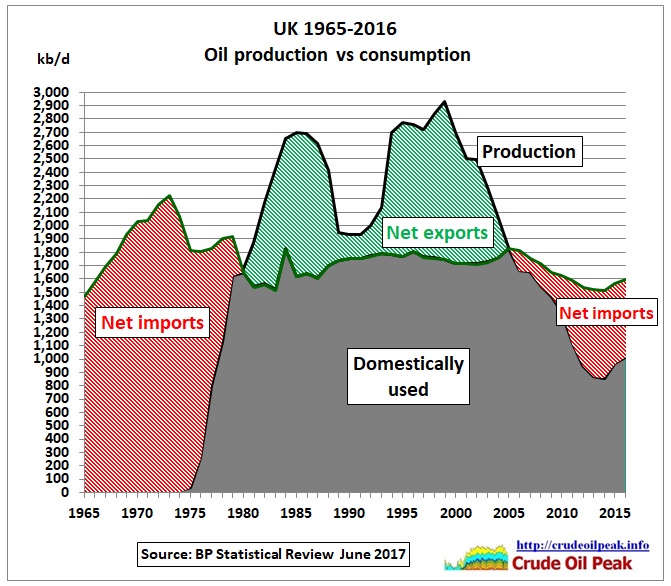

June 2017

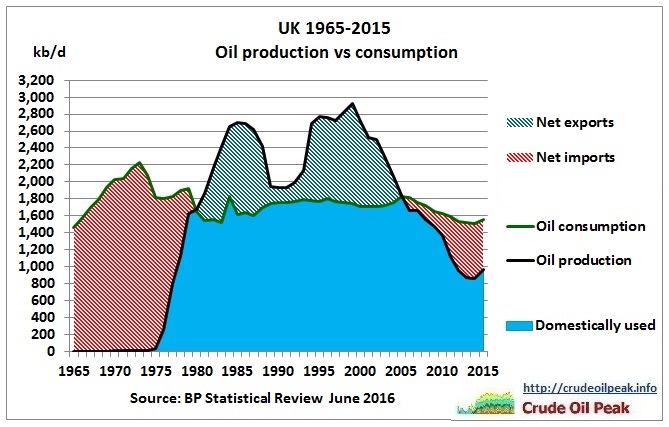

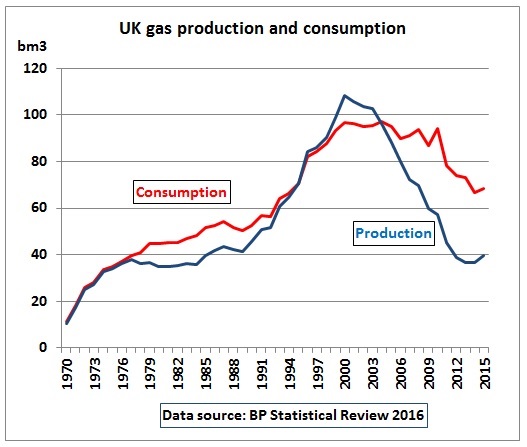

June 2016

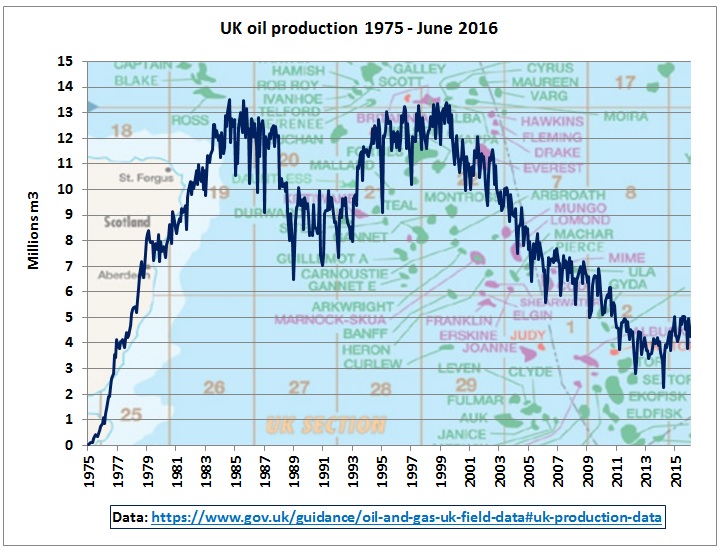

https://www.gov.uk/guidance/oil-and-gas-uk-field-data#uk-production-data

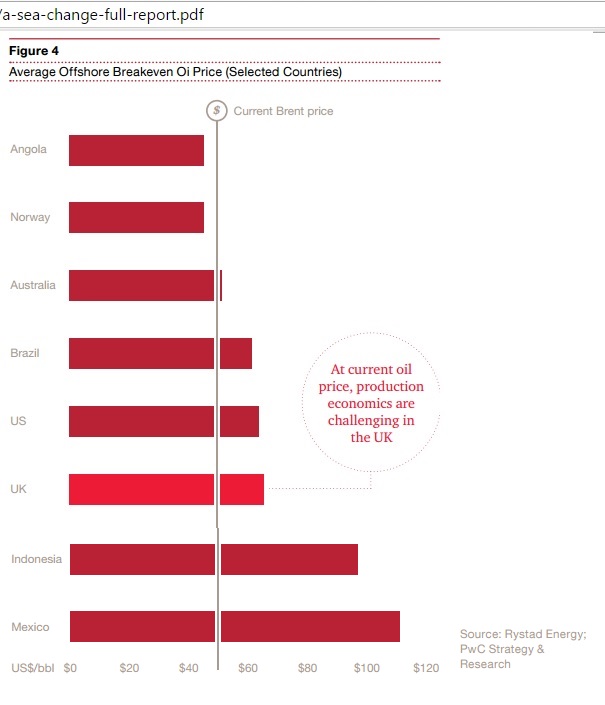

PWC Sea change report

Window of opportunity

Some say there are 24 months to turn around performance. Time is of the essence if a suite of solutions can be deployed to rescue the basin

http://www.pwc.co.uk/seachange

June 2016 BP Statistical Report

..

.

January 2016

http://www.theguardian.com/business/live/2016/jan/25/stock-markets-stimulus-hopes-ftse-oil-live

http://www.theguardian.com/business/live/2016/jan/25/stock-markets-stimulus-hopes-ftse-oil-live

Trade deficit worsened 2 years after the 2nd and last oil peak

October 2015

Endgame for the North Sea?

“Analysis by oil consultancy Wood Mackenzie published last month predicted that 140 of the 330 fields in the UK North Sea may close in the next five years, even if the price of oil returns to $85 a barrel.”

http://www.ft.com/intl/cms/s/0/37da458c-5b7f-11e5-a28b-50226830d644.html#axzz3yLpN8pIP

Low oil price accelerating decommissioning in the UKCS

A high oil price has enabled operators to extend field life and delay decommissioning time and time again on the UK continental shelf (UKCS), however the current low oil price has brought into stark relief that this cannot continue indefinitely concludes a new analysis by Wood Mackenzie. The report, prepared for Offshore Europe 2015, forecasts that while a small number of decommissioning projects have been completed to date, decommissioning activity and spend are forecast to ramp up over the next five years as mature fields are no longer economically viable in a low oil price environment. 140 fields could cease over the next five years

http://www.woodmac.com/media-centre/12529254

September 2014

Scottish independence referendum

26/9/2014

Scots lost out in UK oil and gas endgame

http://crudeoilpeak.info/scots-lost-out-in-uk-oil-and-gas-endgame

https://www.og.decc.gov.uk/pprs/full_production.htm

Crude oil production stacked by start-up year of oil field. Data from here:https://www.og.decc.gov.uk/information

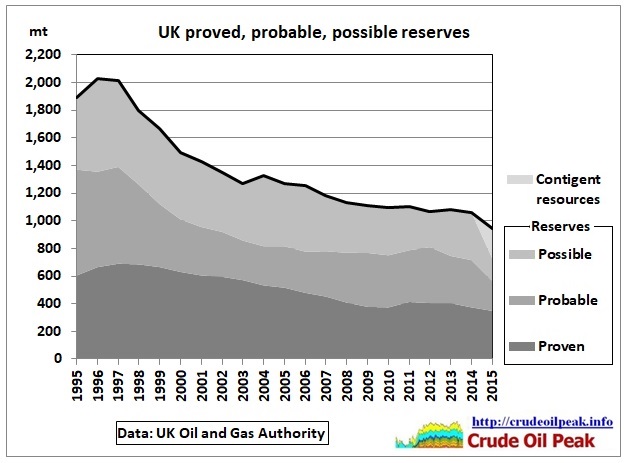

Depletion levels: proven 3383 / 3761 = 90%, proven & probable 3383 / 4152 = 81%

https://www.og.decc.gov.uk/information/bb_updates/chapters/Table4_3.htm

https://www.og.decc.gov.uk/information/bb_updates/chapters/Table4_3.htm

Oil was exported when it was cheap, and is being imported now that it is expensive

http://www.aspo9.be/assets/ASPO9_Wed_27_April_Mauriaud.pdf

From: Cost of energy imports to UK trade balance

http://www.energybulletin.net/stories/2010-10-21/cost-energy-imports-uk-trade-balance

From DECC’s quarterly reports (updated 14/4/2012)

Total indigenous UK production of crude oil andNGLs in the fourth quarter of 2011 was 17.0 per cent lower than a year earlier. This is in-line with the annual change between 2010 and 2011 of 17.4 per cent.

Total indigenous UK production of crude oil andNGLs in the fourth quarter of 2011 was 17.0 per cent lower than a year earlier. This is in-line with the annual change between 2010 and 2011 of 17.4 per cent.

Imports increased by 6.2 per cent and exports decreased by 17.4 per cent to make up for the loss of supply in 2011 Q4. These figures are in-line with the annual changes from 2010 to 2011 for imports (6 per cent increase) and exports (21 per cent decrease).

Refinery production in the latest quarter decreased 3.3 per cent on the same quarter of last year, however in comparison in 2011 refinery production increased by 2.4 per cent compared to 2010.

Refinery production in the latest quarter decreased 3.3 per cent on the same quarter of last year, however in comparison in 2011 refinery production increased by 2.4 per cent compared to 2010.

There have been decreases in production of gas oil and fuel oil, and increases in the production of diesel fuel (DERV) and aviation fuel in both the comparisons between 2011 Q4 and 2010 Q4 and 2011 and 2010.

Overall, imports decreased compared to the same quarter last year, falling by 3.3 per cent, with fuel oils and aviation fuel decreasing. Over the same period exports decreased by 2.0 per cent, with Motor Spirit exports decreasing, although DERV exports increased.

Whilst a net exporter of petroleum products, the UK remains structurally short in diesel road fuel and aviation turbine fuel. Increased production during the last quarter slightly decreased the UK’s import dependence rates for these fuels.

The UK’s overall net import dependence for oil and oil products was 16.4 per cent in the fourth quarter of 2011, with crude oil net import dependence being 45.1 per cent and petroleum products being minus 3.6 per cent (net exports). These figures are broadly in-line with the annual statistics. Crude oil dependence is on an increasing trend as the production from the UKCS declines.

The UK’s overall net import dependence for oil and oil products was 16.4 per cent in the fourth quarter of 2011, with crude oil net import dependence being 45.1 per cent and petroleum products being minus 3.6 per cent (net exports). These figures are broadly in-line with the annual statistics. Crude oil dependence is on an increasing trend as the production from the UKCS declines.

The principal source of the UK’s crude imports is Norway. On the other hand, petroleum products are sourced widely including significant volumes of diesel road fuel from Sweden, and aviation fuel from Kuwait, Qatar, and India.

![]() Total deliveries of key hydrocarbon transport fuels in 2011 Q4 were virtually unchanged when compared to the same quarter last year.

Total deliveries of key hydrocarbon transport fuels in 2011 Q4 were virtually unchanged when compared to the same quarter last year.

In 2011 Q4 deliveries of diesel increased by 1.0 per cent, whilst deliveries of motor spirit decreased by 5.1 per cent. Diesel’s share of road fuels increased further, to another new peak at 61 per cent. On an annual basis diesel increased by 1.2 per cent whilst motor spirit fell by 4.8 per cent.

Deliveries of aviation fuel increased by 5.2 per cent on the same quarter last year, and by 2.3 per cent between 2010 and 2011.

High quality global journalism requires investment. Please share this article with others using the link below, do not cut & paste the article. See our Ts&Cs and Copyright Policy for more detail. Email ftsales.support@ft.com to buy additional rights. http://www.ft.com/cms/s/0/37da458c-5b7f-11e5-a28b-50226830d644.html#ixzz3yLq4EngH

Analysis by oil consultancy Wood Mackenzie published last month predicted that 140 of the 330 fields in the UK North Sea may close in the next five years, even if the price of oil returns to $85 a barrel.