In this part on the budget 2016 series we have a look at the federal revenue:

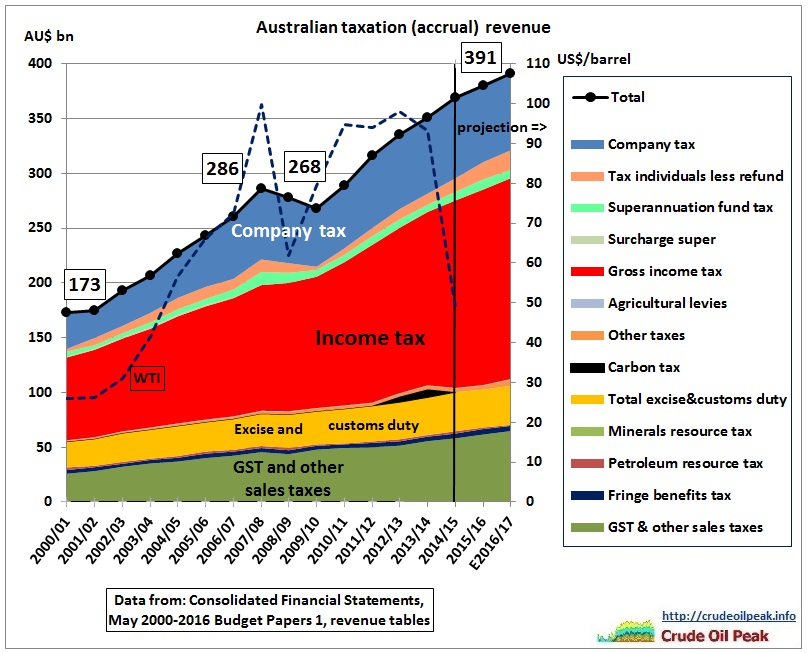

Fig 32: Time series of federal tax revenue

Income tax was growing strongly at 6% pa before the financial crisis, with a peak growth rate of 8.6% in 2004/5 after which high oil prices brought growth rates down. During the critical phase of the GFC growth rates went down to 2% pa to rebound to 9-10 % in 2010-11, possibly as a result of the mining boom.

The carbon tax, which created so many party political conflicts is negligible in the tax scheme of things.

We can clearly see the GFC changed everything, for good:

..

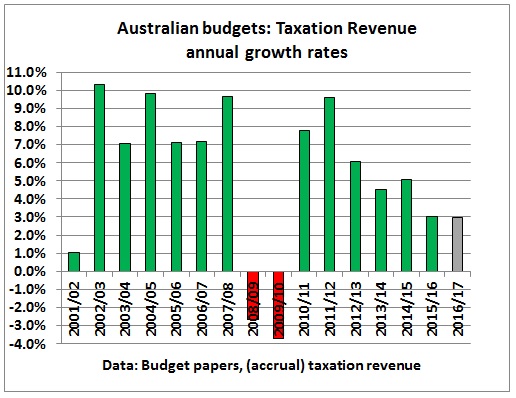

Fig 33: Taxation revenue growth rates

Taxation revenue growth rates after the GFC have been trending downwards. In particular, there is a distinctive kink in the company tax revenue.

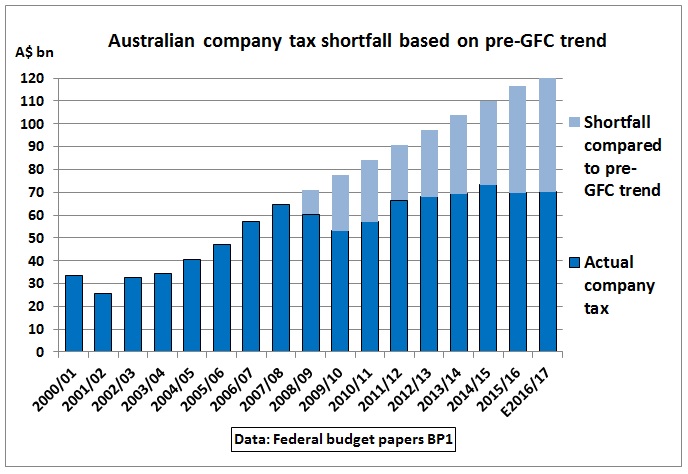

Fig 34: Company tax shortfall

The light blue columns show expected company tax revenue using pre-GFC trends. They amount to a total of $286 bn which is 81% of the accumulated $355 bn of the cumulative (negative) cash-balance up to 2017.

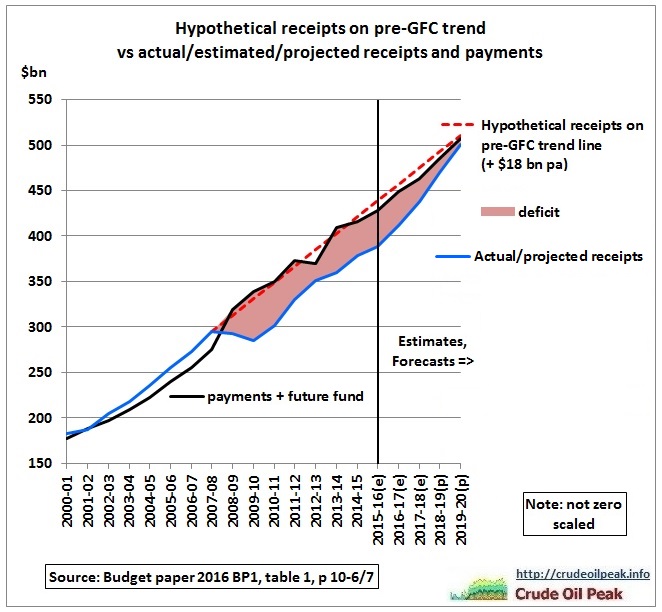

Fig 35: Budget deficit and pre-GFC trend

The graph shows the budget deficit in relation to receipts, payments (including to future fund) and hypothetical receipts based on a linear pre-GFC trend.

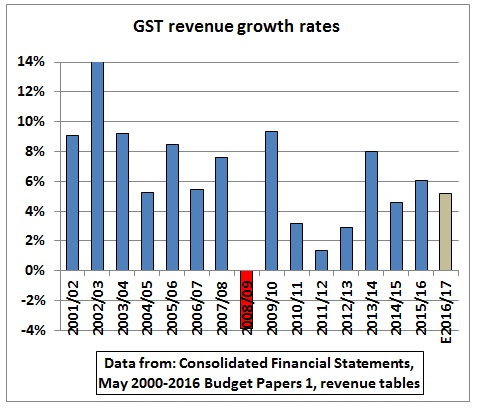

GST

Fig 36: GST revenue growth rates

Average GST revenue growth before GFC: 8.5%, after GFC 4.5% (excluding rebound year 2009/10)

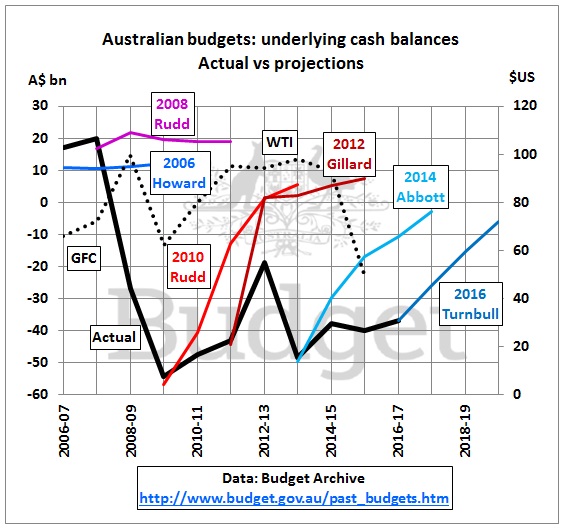

Comparison Budget projections

Now let’s look at the veracity of budget projections in the last 10 years:

Fig 37 Australian budget projections – history

Fig 37 shows that successive governments were too optimistic about bringing the budget back to balance, not to mention that accumulated debt can be paid back.

It is very clear from the above graphs that the budget balance has fundamentally changed after the financial crisis which started in 2008/09. This crisis was caused by the convergence of high debt and high oil prices and triggered by the subprime mortgage crisis in oil dependent US suburbia.

Therefore, in the 2nd half of this post, we’ll analyse the budget papers to see whether oil supplies and oil prices have been adequately considered. We have to go back quite a number of years because wrong assessments outside the budget process have contributed to the problems.

Energy White Paper 2004

The oil related context story to the above graph starts in 2004, when Howard released a completely flawed energy white paper with a statement that there would be sufficient oil supplies for 40 years, result of a naïve calculation dividing reserves by the then current annual production. What matters of course are annual oil flows and these have to be commensurate with the requirements of a growing world economy in EVERY YEAR of the projection period. Oil prices were going up and up at that time which meant that production was NOT sufficient.

Senate Inquiry on oil supplies 2005-2007

In November 2005 a Senate Committee started an inquiry about peak oil concerns. First submissions were received in December 2005

I did submission #69 in February 2006 entitled “Peak oil ante portas”

Budget 2006

As is customary the budget was released in May (2006), prepared by the treasurer Peter Costello and the finance minister Nick Minchin.

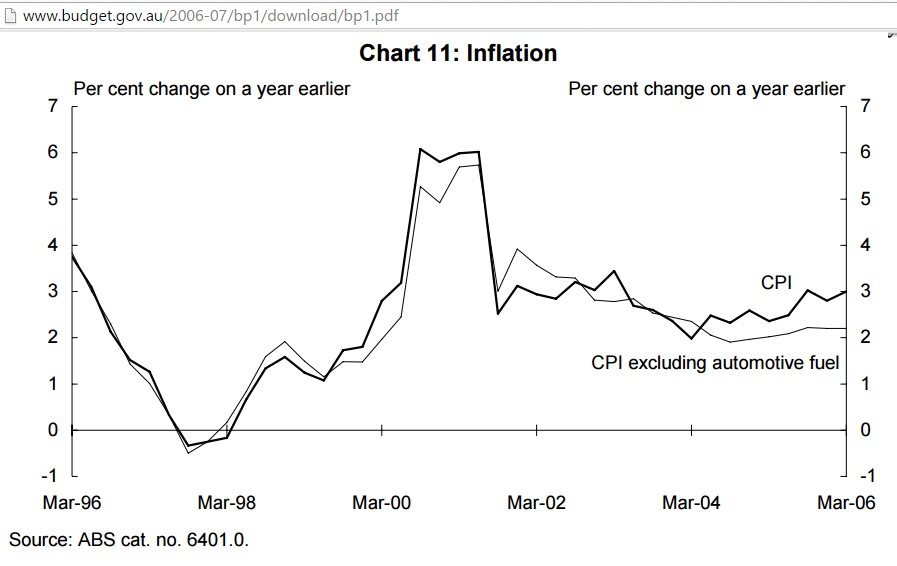

In statement 3, the budget paper calculated that higher fuel prices lifted annual inflation by ¾ of a percentage point above core inflation between 2004 and 2006, but played it down somewhere else in the paper: “In Australia, higher fuel prices also do not appear to have flowed through to broader price inflation.”

Fig 38: Impact of high oil prices on CPI

The budget paper does not worry much about it because it argues that the lesson from the 1970s oil crises was that high oil prices over an extended period of time have a moderating influence on demand. Everything back to normal!

In statement 4, on energy security the paper said: “The world is heavily reliant on energy and, in particular, on the supply of oil. World oil demand is projected to increase by around 45 per cent over the next 20 years. Potential vulnerability is magnified by reliance on supplies from the Middle East, which already accounts for 30 per cent of world production — of which 11 per cent is from Saudi Arabia. This reliance on Middle East sources is projected to rise to 46 per cent by 2030.

Disruptions to oil supplies might arise from conflict involving key energy producers, unfavourable political shifts or major terrorist attacks. Because demand for oil is so unresponsive to price in the short run, disruptions that lead to only modest reductions in world supply could raise oil prices very substantially, at least for some time”

A 45% increase over 20 years means of course there would not be sufficient oil supplies for 40 years at constant production rates as assumed in the 2004 energy white paper. It would “last” for just around 25 years and then drop to zero, an unlikely production profile.

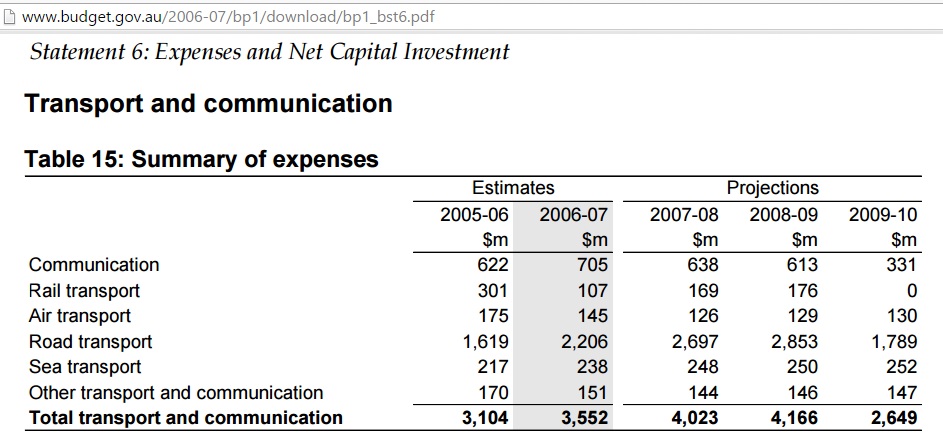

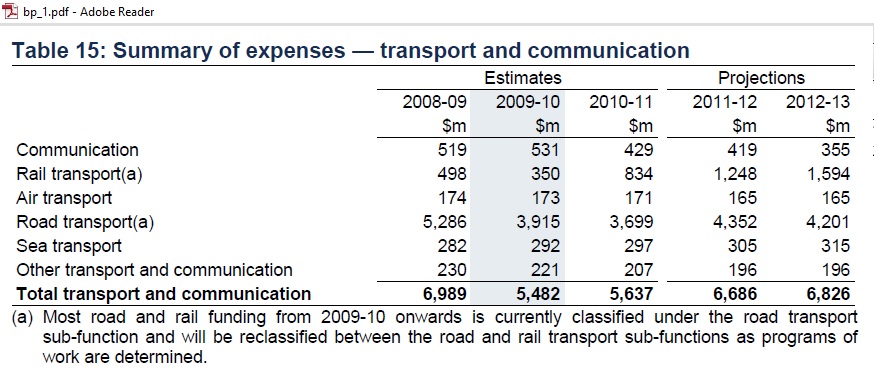

The budget paper deliberations about increasing oil demand and oil vulnerability did not influence at all the way capital investments in table 15 were split up between roads/air and rail infrastructure:

Fig 39: Capital investments in infrastructure

Note rail transport peters out to zero in 2009/10. One would expect more investment in energy-efficient rail if there was an issue with oil vulnerability.

Therefore, what was said in statement 3 and 4 was an academic exercise to calculate some macroeconomic variables without any input into the investment statement.

http://www.budget.gov.au/2006-07/bp1/download/bp1.pdf

Senate Inquiry hearings 2006

In a historic hearing in July 2006 in Sydney Parliament House Dr Ali Samsam Bakhtiari – who had worked with the Iran National Oil Company and who was one of 2 OPEC whistle blowers – held a 3 hr peak oil lecture. The Hansard is here.

Senator Barnaby Joyce, member in Howard’s coalition and now Agriculture Minister had a keen interest in this topic and asked questions on what would be the price for oil. Dr. Bakhtiari replied he could see $100-150 a barrel “not very far into the future” and after that $200-$300 for Arctic oil. Barnaby asked – rather rhetorically but rightly – who could afford to buy $200 oil.

Peak oil denier Nick Minchin 2006

A month later, in August 2006, Nick Minchin went on the record as a peak oil denier in a sitting of the Senate, answering a question without notice on fuel prices (p 26). He thought that high oil prices were caused by under investment in the oil sector in the 1990s when oil prices were low. There would be shale oil – including in Australia itself – which will be commercially feasible to extract at a “certain price”. He saw “significant” growth in the use of LPG and investments in biofuels like ethanol. Ultimately, market forces would “dictate” to move from oil to alternative fuels like hydrogen. No worries.

However, in his earlier 2006 budget paper there was no modelling to show how oil prices and alternative fuels would support the projected GDP growth, not to mention tax revenue. Since 2006, not much has changed in this mindset prevalent among Parliamentarians and bureaucrats.

The Senate Inquiry report came out in February 2007

Saudi oil decline 2005-2007

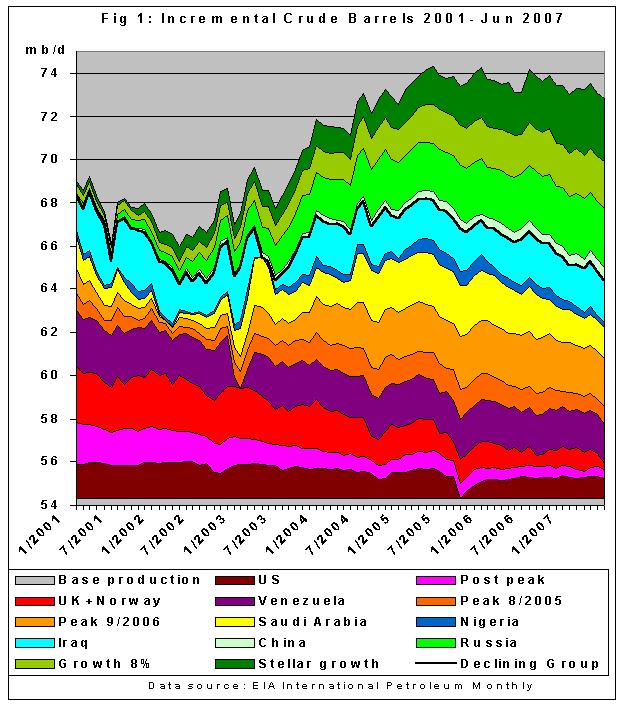

Fig 40: Crude oil production Jan 2001 – Jun 2007

By mid 2007 Saudi oil production had declined to such an extent that it had pulled down the whole global production system. Katrina had brought down US production, too.

The author of this post had a 3-year long exchange of letters with Howard over this topic. At the end in 2007 he advised that he “agrees to disagree”, a useless semantic somersault. It costed Australia dearly.

Rudd’s first budget 2008/09

Rudd came to power in December 2007 with plans for renewable energies but no strategy on oil. The budget paper of May 2008 came right into the eye of the storm of exploding oil prices and a US recession which had started in the 4th quarter of 2007. First news on weak growth of 0.6% from the Commerce Department came out in January 2008.

Australian real gross domestic product growth for 2008-09 was calculated to be 2.75% (down by 0.75% from previous year) assuming an oil price of $115 a barrel. Such high oil prices should have of course been a warning but a medium or long-term analysis of the impact of high oil prices on the financial system and the economy was not done. In relation to oil, treasury was mainly concerned with revenue from excise and cancelled the exemption for condensate. Revenue from the petroleum resource rent tax varied considerably due to falling production and an increase in the deductibility of growing production and exploration cost, often offsetting rising oil prices. As can be seen from Fig 37, Treasurer Wayne Swan thought an underlying positive cash balance can be maintained at A$20 billion pa. Worse still, the budget 2008 ramps up investment in roads and completely neglects rail.

Fig. 41: Infrastructure spending in budget 2008/09

Again we see a complete disconnect between high oil prices and infrastructure decisions.

Only 1 month after this road heavy budget was released we hear Prime Minister Rudd acknowledging in an ABC TV interview:

16/6/2008

KEVIN RUDD, PRIME MINISTER: Kerry, on global oil prices, no one that I can speak to, either within the Government, that is the Treasury who are looking at the long range forecasting here, or abroad, can give you any confidence about where global oil prices will be in three, six, nine, 12 months time.

It is a very murky future that we face. What we do know for a fact is that right now we have the greatest global oil shock in 30 years. We know for a fact that prices are up 400 per cent since the Iraq war, 100 per cent in the last 12 months alone. It’s led to protests and riots in the UK, Spain, France, as well as Indonesia and our own region and South Korea.

KEVIN RUDD: But Kerry, that’s why my responses to many of these questions in parliaments in recent weeks have been framed in terms of

- one, global oil supply, what can be done to boost investment in those countries which are the principal oil exporters? There’s a problem there.

- Two, on the demand side. Global initiatives on energy efficiencies and the huge great push countries of China and India?

- Three, what do you do in terms of energy efficiency in economies like our own? That goes to the whole regime of fuel efficient cars, in particular.

- Four, what do you do in terms of an alternative fuel strategy?

- And five, what do you do in terms of public transport, in order to make it accessible, particularly in our metro areas?

http://www.abc.net.au/7.30/content/2007/s2276494.htm

Assessment of Australia’s Liquid Fuel Vulnerability Nov 2008

Report by ACIL Tasman – commissioned by the Federal Government

http://www.aip.com.au/pdf/ACIL_LFVA_2009.pdf

Causes and Consequences of oil shock 2007/08

A well known analysis in spring 2009 of Hamilton Causes and Consequences of the Oil Shock of 2007–08 found that the US recession was caused by high oil prices coming from strong demand confronting stagnating world production.

Rudd’s 2nd budget 2009/10

This budget paper (May 2009) focuses on the financial crisis without analysing the link to high oil prices as presented in Hamilton’s analysis.

The emergency response to the crisis was the Nation Building Plan

Fig 42: Nation Building Plan expenditure

So the spending over 4 years was $38 bn. The company tax short fall for the same period (Fig 34) was $86 bn.

Following reasons for lower company tax were presented in the budget paper:

- Weakness in the domestic economy

- Lower level of corporate profitability

- Deteriorating world outlook

- Lower equity and commodity prices

- Reduction in investments

- Generally less economic activity

The downturn in company tax is immediately felt as tax is due during the year of income.

And let’s see whether we see Rudd’s expenditure on public transport in the budget paper:

Fig 43: Transport infrastructure in 2009/10 budget

Again rail infrastructure to reduce oil dependency was not shovel ready i.e. the planning was not done after Rudd came to power.

Summary:

Since the financial crisis budget 2008/09 lower company tax is the main reason for Australia’s budget deficit. Every period of high oil prices impacts on the budget negatively. Since the damage of earlier oil price spikes (more debt) is irreversible, lower oil prices do not immediately improve the situation and need time to filter through the economy. However, if oil prices remain at low levels, the oil and gas industry will suffer. The medium to long-term solution to the problem of high oil prices is to get away from oil in the transport sector which requires a rolling rail development and electrification program. When analysing budget papers, there is no evidence that such a program is seen as a priority. Australia remains vulnerable to the next oil price shock.

To be continued.