Australian diesel import update March 2026

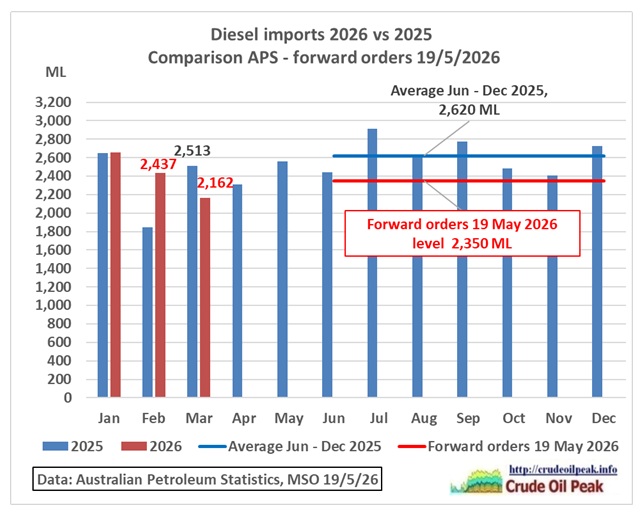

In the previous post it was highlighted that forward diesel orders (19 May 2026) were at 2,350 ML per month. If the geopolitical situation were to continue (optimistic scenario) this level would not be enough to maintain imports achieved in 2024 and 2025. A saving of 10% would be required.

This is an update of graphs with data up to March 2026 from the Australian Petroleum Statistics published last week. March is the first month in which the Iran war impacted on oil flows.

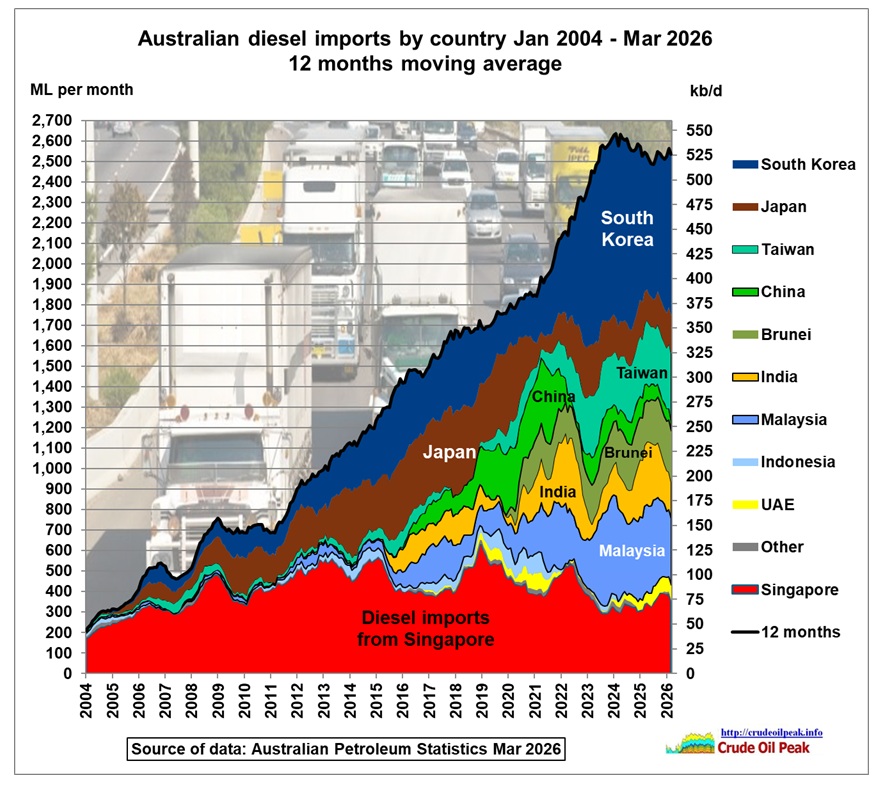

Fig 1: Diesel imports by country of origin

Fig 1: Diesel imports by country of origin

Not much change can be seen in this graph compared to previous graphs because these are 12 months moving averages. So let’s look at the monthly data:

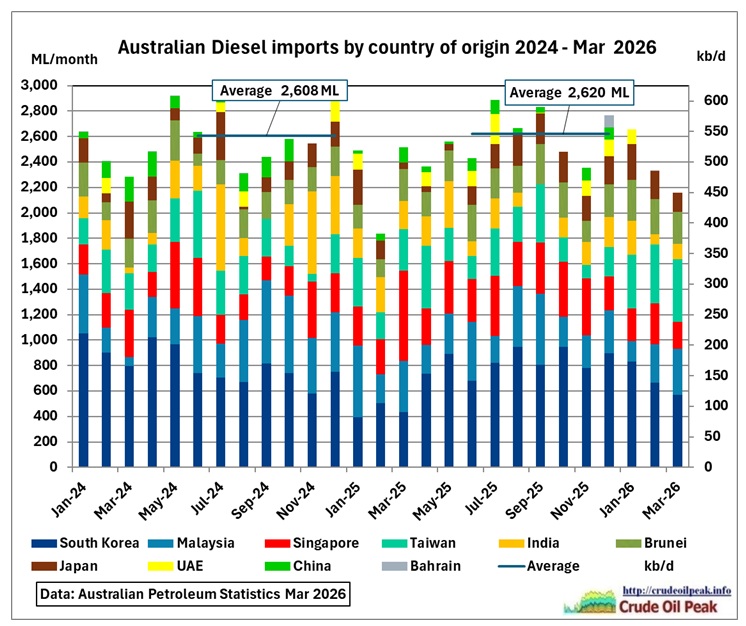

Fig 2: Monthly diesel imports

Fig 2: Monthly diesel imports

Diesel imports already dropped in January-February and then again in March because of the Iran war. There is an annual, seasonal dip in imports in January-February. As Asian refiners are building their own local storage ahead of the spring maintenance period, spot-market export volumes available to international buyers like Australia tighten up. Australian fuel import managers are aware of this cycle. They know that diesel spot-cargoes out of Asia in January/February are expensive. They also have to avoid the domestic holiday port constraints.

As a result, Australian importers minimize their imports during January/February, choosing to draw down the safety stocks they built up locally back in November and December.

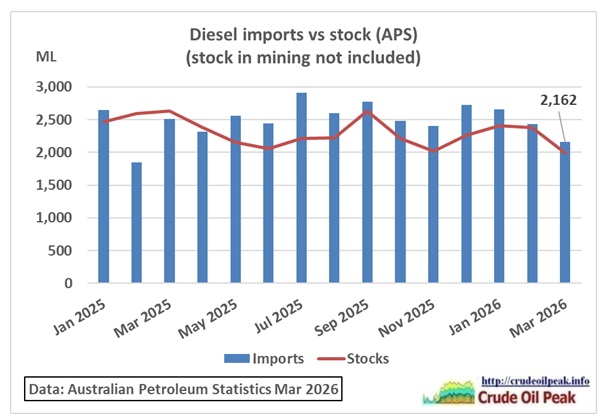

Fig 3: Diesel imports vs stock 2025 – Mar 2026

Fig 3: Diesel imports vs stock 2025 – Mar 2026

Therefore, when the Iran war started 28 Feb, Australia entered March with its imports already sitting at a seasonal structural low.

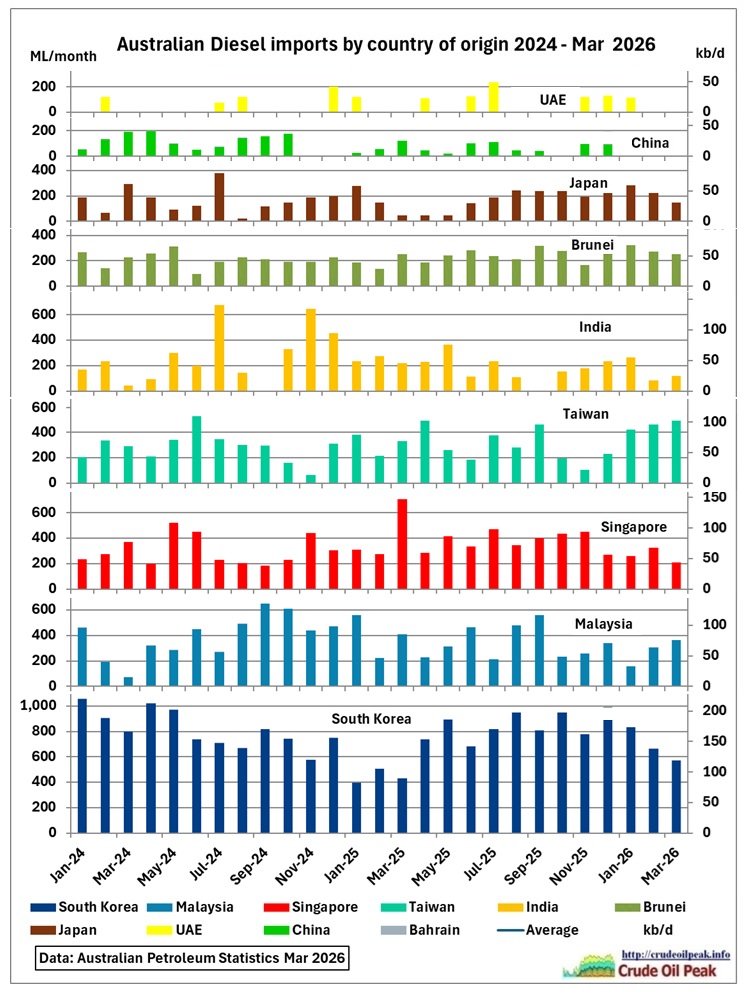

The stacked graph in Fig 2 is not easy to read, so Fig 4 shows imports from each country separately but all together.

Fig 4: Separate import profiles for each country

Fig 4: Separate import profiles for each country

We see that imports from Malaysia, Taiwan and Singapore did not follow that January/February dip in early 2026.

One also has to keep in mind:

Imports are recorded in the calendar month in which the import declarations are first finalised by the DIBP. Normally this is within a few days of discharge of cargo, although, on occasion, there are delays in the finalisation of import declarations. Import declarations can also be finalised before the goods actually arrive to expedite goods movements. For these reasons, recorded imports for a particular month may not necessarily represent declarations lodged, or commodities actually imported, during that month.

The most notable example is petroleum where the value of merchandise imports recorded for a particular month that actually arrived in the same month varies from 80% to 92% (on average 84%).

https://www.abs.gov.au/ausstats/abs@.nsf/Lookup/by%20Subject/5489.0~2015~Main%20Features~Time%20of%20Recording~10015

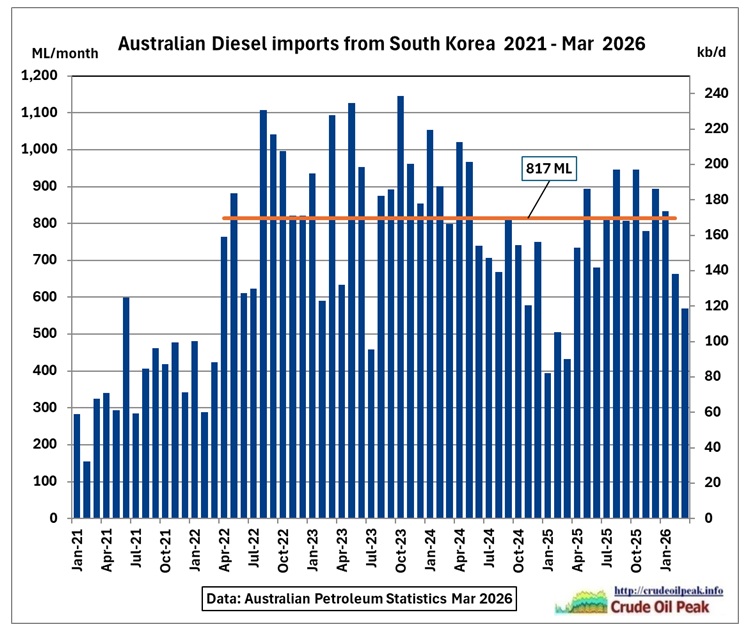

We need to monitor the most important countries like South Korea:

Fig 5: Australian diesel imports from South Korea

Fig 5: Australian diesel imports from South Korea

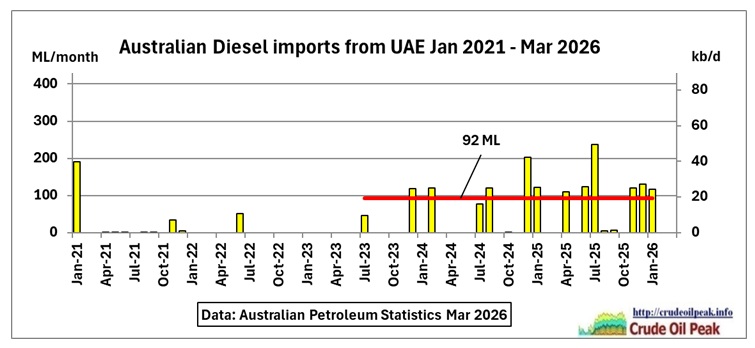

Fig 6: Australia was not much dependent on imports from the UAE which have stopped now

Fig 6: Australia was not much dependent on imports from the UAE which have stopped now

Fig 7: Forward orders (MSO) compared to 2025 imports (APS)

Fig 7: Forward orders (MSO) compared to 2025 imports (APS)

Imports in June – Dec 2025 were 2,600 ML/month while forward orders on 19 May 2026 were only 2,350 ML, a 10 % gap. Expect diesel prices to go up again to cause demand destruction. Or increase forward orders (with a risk premium to be paid by Export Finance Australia – as included in the Budget 2026/27).

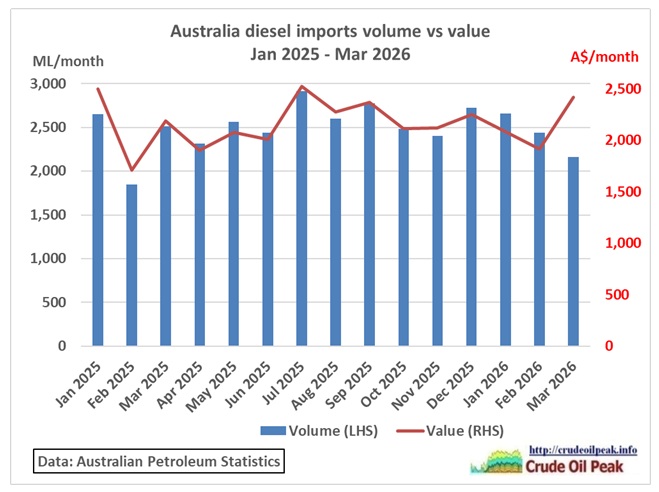

Fig 8: Diesel import volumes vs value

Fig 8: Diesel import volumes vs value

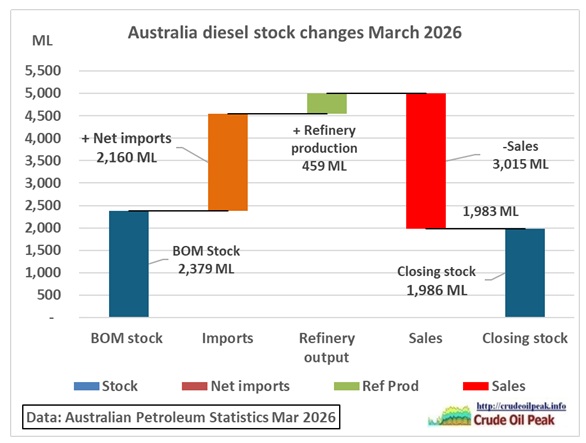

Let’s check the stock balance at the end of March:

Fig 9: Diesel stock change in March 2026

Fig 9: Diesel stock change in March 2026

We have:

Stock EOM February 26………. 2,379 ML

Net Imports March 2026……… 2,160 ML

Refinery production………………. 459 ML

Sales …………………………….-3,015 ML demand much too high (panic sales?)

Balance ………………………….1,983 ML

Stock EOM March 26 ………….1,986 ML

Diff 3 ML

Amazing. The difference is negligible.

13/4/2026

Discrepancies in diesel sales and stocks in the Australian Petroleum Statistics

https://crudeoilpeak.info/discrepancies-in-diesel-sales-and-stocks-in-the-australian-petroleum-statistics

Conclusion:

Under no circumstances must diesel demand be increased. The easiest is to stop planned big diesel intensive projects like in Sydney the Glebe island apartment towers

The NSW State government has hired the public broadcaster ABC News as promoter for a “new suburb” for immigrants. What’s worse, a port with a cement silo would have to be demolished to make room for the apartments. As a result, cement for Sydney would have to be supplied from Newcastle by (diesel) trucks! GOOD LUCK, oil and energy illiterate governments.

The NSW State government has hired the public broadcaster ABC News as promoter for a “new suburb” for immigrants. What’s worse, a port with a cement silo would have to be demolished to make room for the apartments. As a result, cement for Sydney would have to be supplied from Newcastle by (diesel) trucks! GOOD LUCK, oil and energy illiterate governments.

Cement carrier docked at Glebe island to replenish the cement silos there.

Cement carrier docked at Glebe island to replenish the cement silos there.

Other States have similar redundant projects: the Stadium in Hobart and the Olympic Stadium in Brisbane for example. No one has estimated who will be able to afford flying to the end of the world in 2032.

Related post:

Tankers arriving and departing in Sydney

https://crudeoilpeak.info/tankers-arriving-and-departing-in-sydney