In this 3rd post on Australian diesel imports, the focus is on the dependency on Middle East oil as Israel and Iran have started to attack their oil refineries.

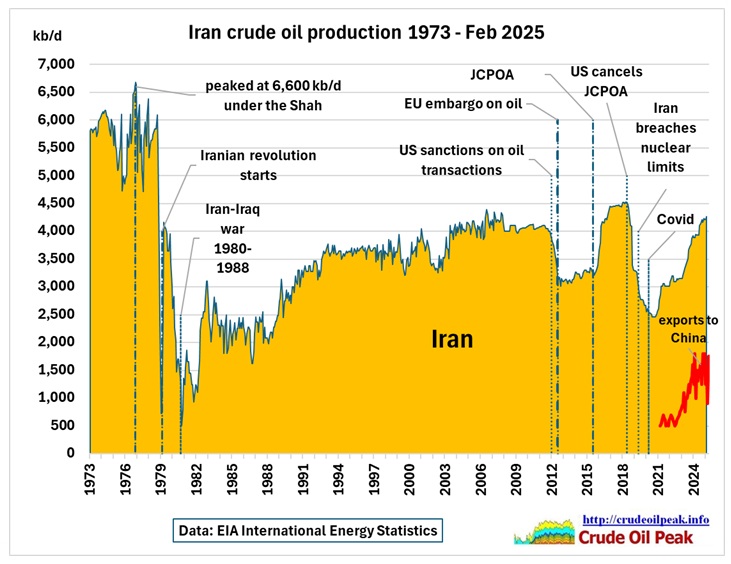

Fig 26: Iran crude oil production since 1973

The problem started decades ago with peak oil in a dictatorship at 6,600 kb/d in the mid 1970s, under the Shah.

Sal Mercogliano in his Youtube Channel describes:

How is Shipping Impacted by an Israel-Iran War?

Trade Through The Strait of Hormuz – History

https://www.youtube.com/watch?v=zfSw4KZXC7M

At the very end of the video: How could Iranians close the Strait of Hormuz?

Attack tankers with gun boats

Limpet mines attacks

Shore-based and ballistic missiles (similar to what Houthis do)

Launch unmanned surface vehicles

Mine the whole Strait – most dangerous

These are scenarios which may happen only at the very end, in a revenge and suicide action by a desperate regime in Tehran.

Fig 27: Tanker traffic in the Persian Gulf and the Strait of Hormuz Jun 2025

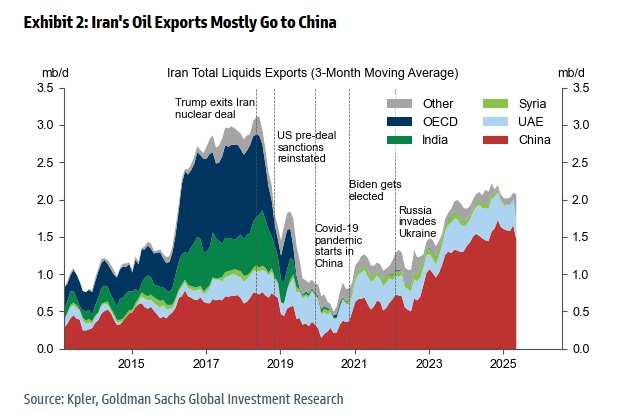

Fig 28: Most of Iran’s oil exports go to China

Fig 28: Most of Iran’s oil exports go to China

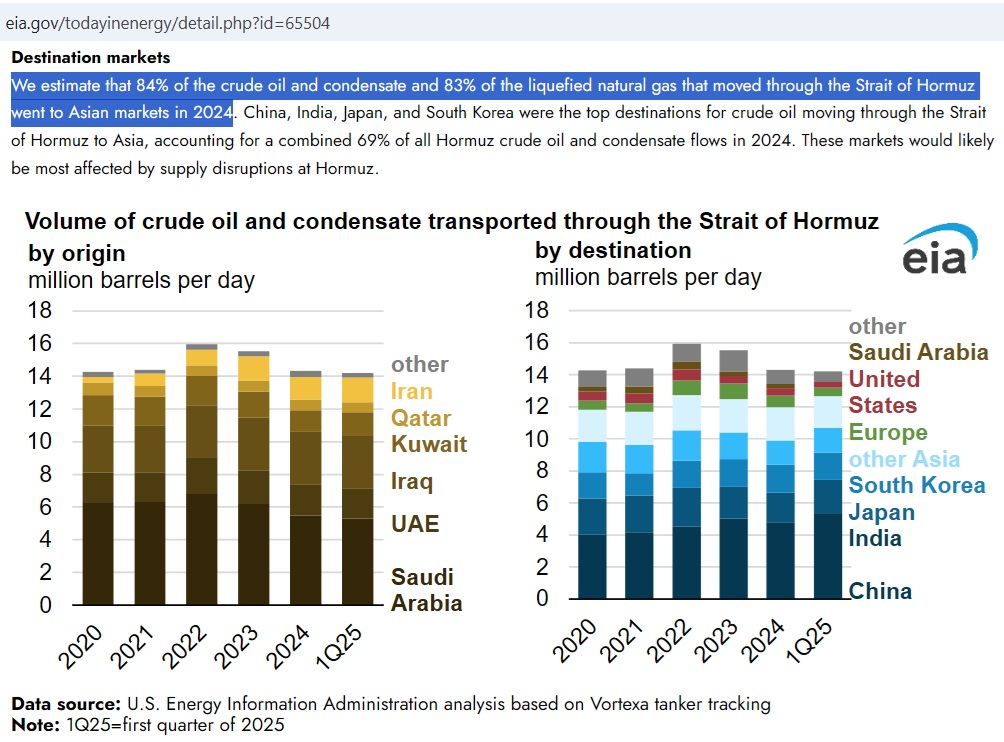

Fig 29: Oil flow through the Strait of Hormuz

16/6/2025

Around 0.5 million b/d transited the strait in 2022 from Saudi ports in the Persian Gulf to Saudi ports in the Red Sea.

https://www.eia.gov/todayinenergy/detail.php?id=61002

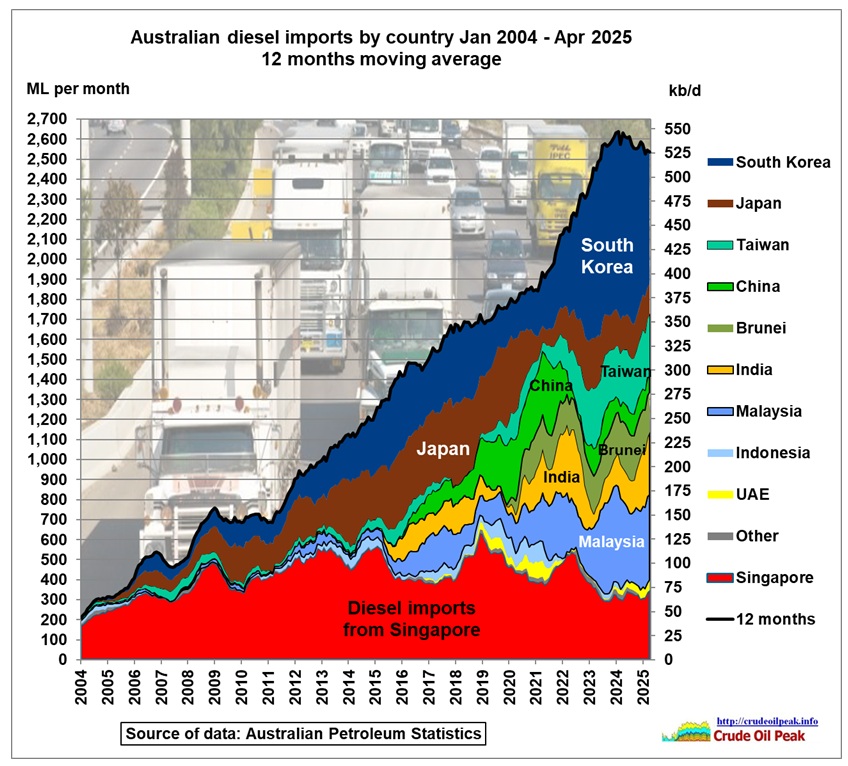

So what does that mean for Australian diesel imports which come from these Asian countries?

Fig 30: Diesel imports 2004 – Apr 2025

Fig 30: Diesel imports 2004 – Apr 2025

https://www.energy.gov.au/publications/australian-petroleum-statistics-2025

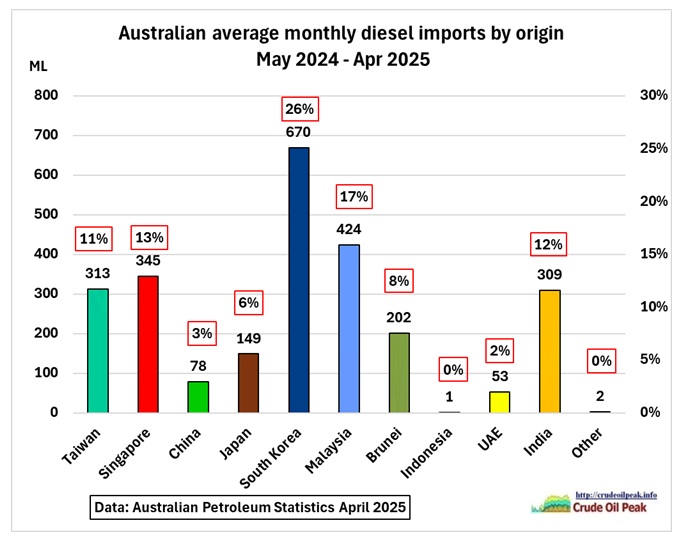

Fig 31: Average diesel imports between May 2024 – Apr 2025

Fig 31: Average diesel imports between May 2024 – Apr 2025

As already shown in Fig 20 (South Korea) and Fig 24 (Japan) in the previous post, these countries depend on crude oil imports from the Middle East at 72% and 90% respectively. We look now at the other countries.

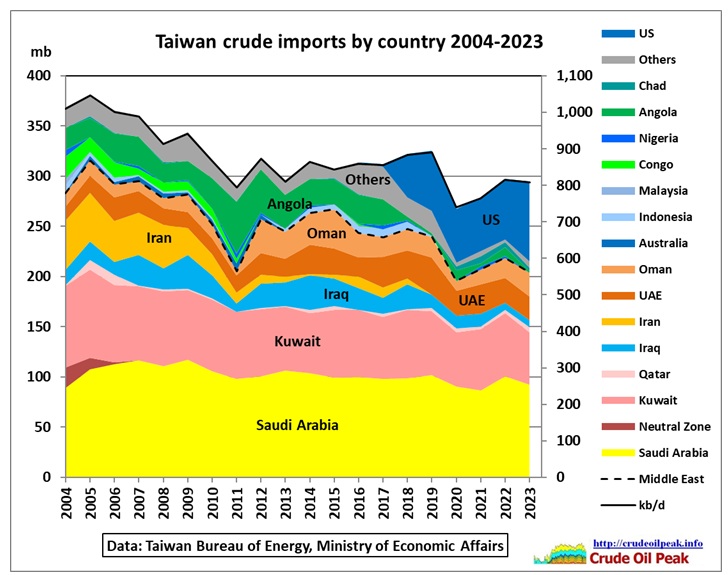

Fig 32: Taiwan’s crude oil imports are ME dependent at 69%

Fig 32: Taiwan’s crude oil imports are ME dependent at 69%

https://www.moeaea.gov.tw/ECW/English/content/SubMenu.aspx?menu_id=1585

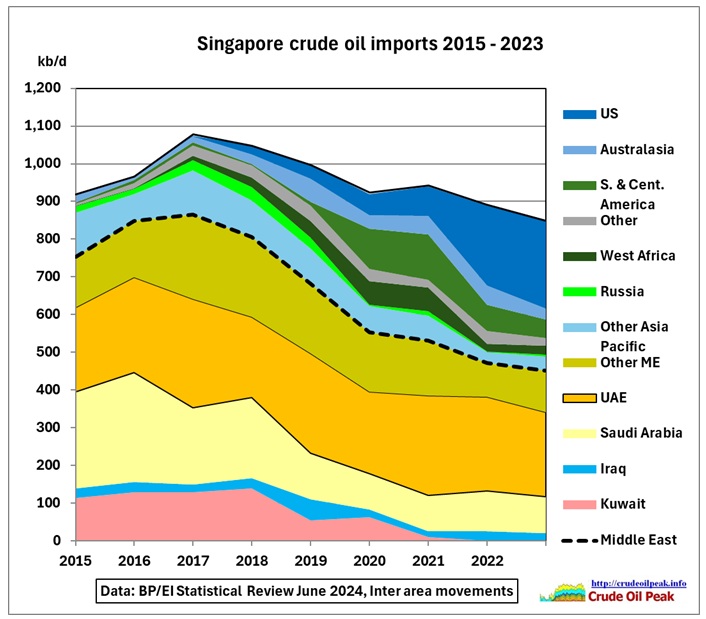

Fig 33: Singapore crude imports by country

Fig 33: Singapore crude imports by country

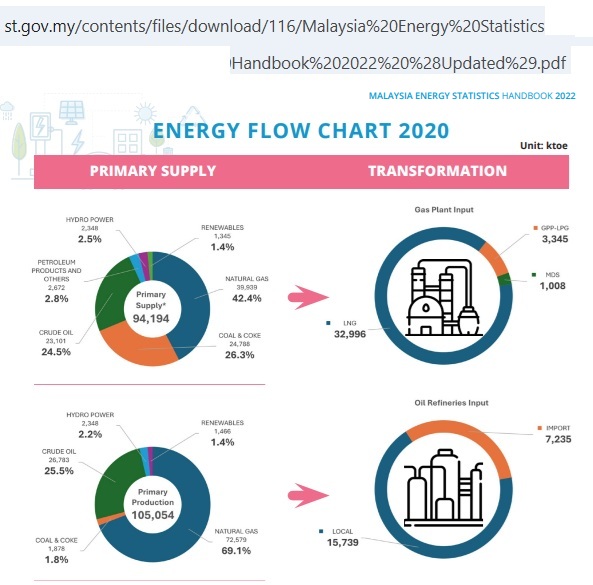

Fig 34: Malaysia’s Energy Flow

Fig 34: Malaysia’s Energy Flow

https://www.st.gov.my/contents/files/download/116/Malaysia%20Energy%20Statistics%20Handbook%202022%20%28Updated%29.pdf

The panel at the bottom right shows oil refineries input dependent on imports at the rate of 7,235/(7,235+15,739)= 31.5%. The Middle East shares of these imports have been calculated with data from the Observatory of Economic Complexity https://oec.world/en

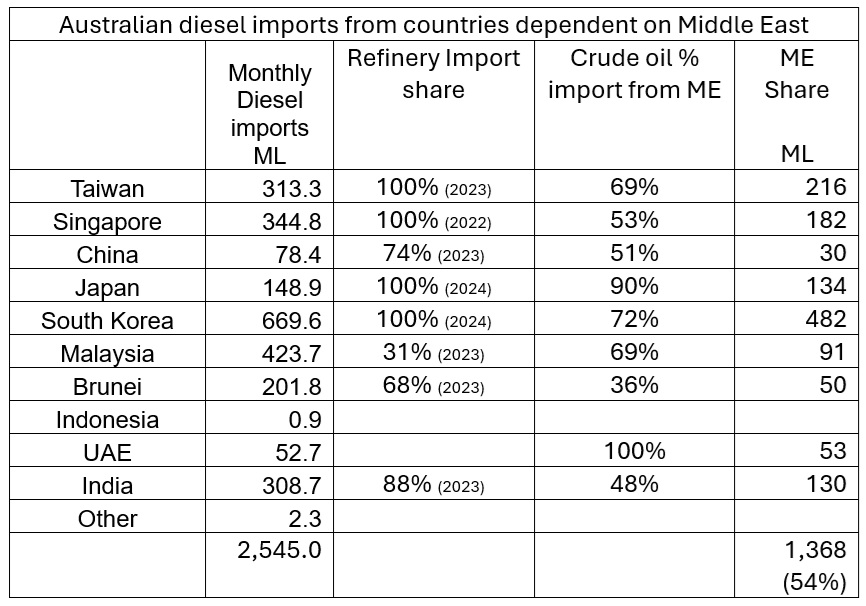

Let’s put all this information in one table and summarize:

Please note that some of the data are from previous years and may have changed by now. What the table suggests however is that around half of Australia’s diesel imports indirectly depend on Middle East oil.

How about Australia’s crude oil imports for the 2 last remaining refineries?

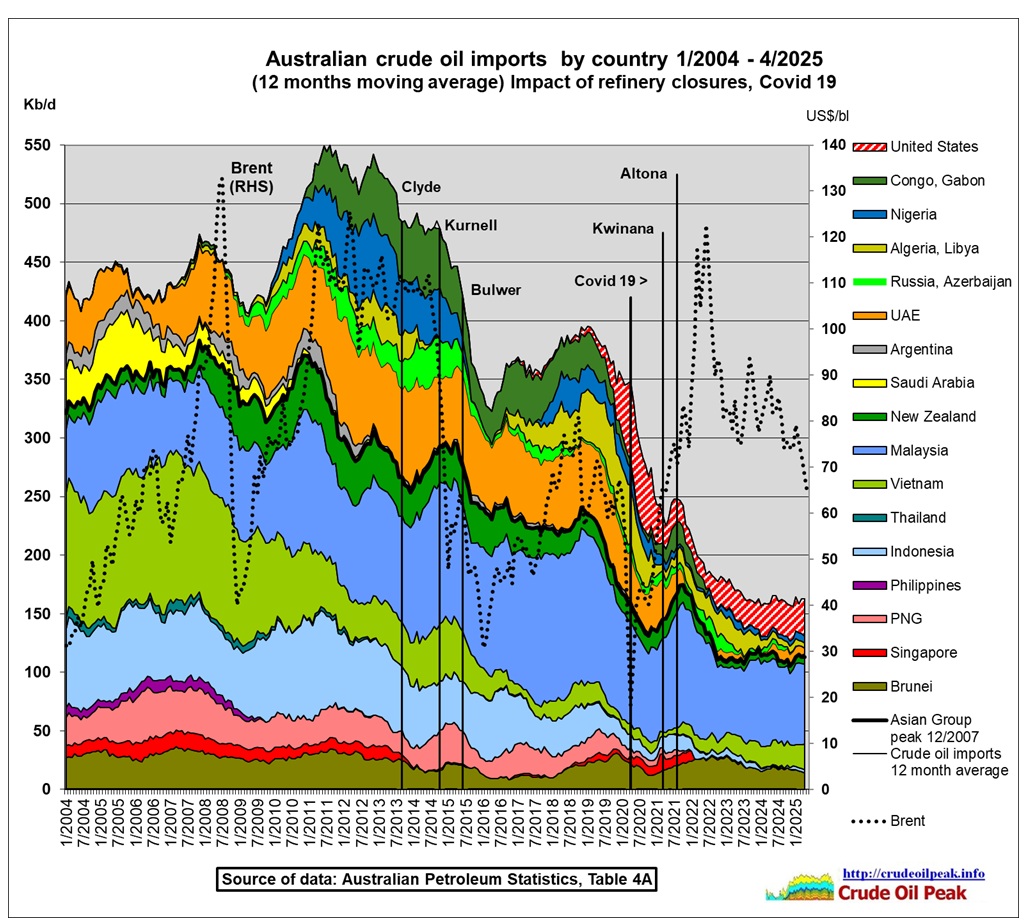

Fig 35: Australian crude oil imports

Fig 35: Australian crude oil imports

Except for occasional imports from the UAE, Australia’s crude imports are not dependent on the Middle East. Traditionally, imports come from neighbouring countries in South East Asia but these declined as crude production in this area peaked around 2001 and Australian refineries started to close down from 2013 onwards. This website followed the shutting down of refineries one by one and how this increased Australia’s oil vulnerability.

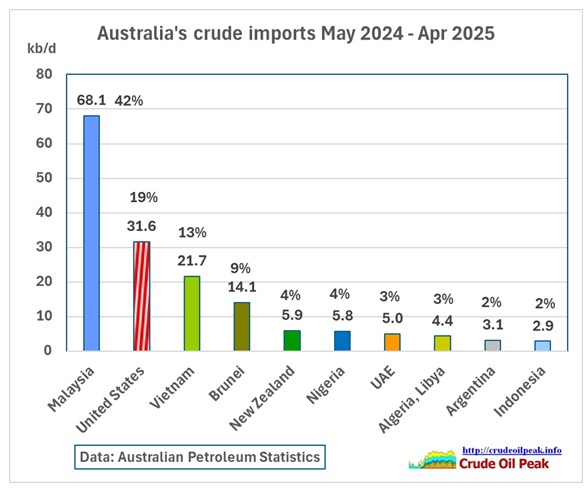

Fig 36: Crude imports in last 12 months

Fig 36: Crude imports in last 12 months

However, Malaysia, Vietnam and Brunei are themselves dependent on crude imports from the Middle East and may be reluctant to export crude to Australia in case of shortages or disruptions. In addition, Australia’s geographic remoteness is not advantageous in spot trading.

Media mis-informs

Australian media have dropped the ball on oil at least 10 years ago which created a deep-seated complacency among the public. The latest examples by the public broadcaster ABC:

Evan Lucas on the Business program on the day the Israel/Iran war started (13/6/25)

Evan Lucas on the Business program on the day the Israel/Iran war started (13/6/25)

“…. the Strait of Hormuz, the reason that’s a massive concern for Europe….”

Half-truth, as if Australia were not impacted.

In the evening news on 14/6/25 it is mentioned that 20% of global oil passes through the Strait of Hormuz but not that 80% goes to Asia.

In the evening news on 14/6/25 it is mentioned that 20% of global oil passes through the Strait of Hormuz but not that 80% goes to Asia.

If ABC TV had bothered to use the simple search word “Hormuz oil flow” it would have immediately come across an earlier version of the above EIA article https://www.eia.gov/todayinenergy/detail.php?id=61002

Conclusion

The time to get away from oil was under John Howard 20 years ago when CNG for urban trucks and LNG for long distance trucks and rail freight could have been introduced as alternative transport fuel instead of exporting gas as LNG. The CO2 is in the atmosphere anyway.

Given the dangerous situation there are only limited options available:

(1) Give up perpetual growth strategies in capital cities

(2) Do not approve big projects with high consumption of diesel during construction

(3) Reduce immigration IMMEDIATELY because the more immigrants come here, the longer the lines at the filling stations and the faster the shelves in shopping centres will empty (remember the Wuhan virus in 2020?)

(4) Educate all politicians, advisors, consultants and journos on oil & energy

Update:

With data up to December 2025

https://crudeoilpeak.info/australias-diesel-import-dependency-on-strait-of-hormuz-is-around-50