Same procedure every Saturday. First, a new chart appears on the DCCEEW website

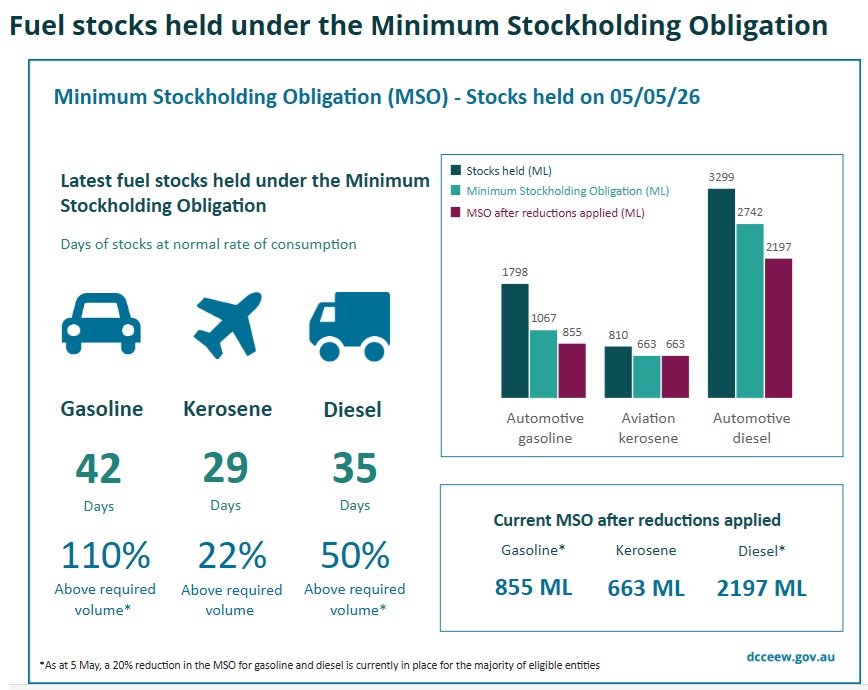

Fig 1: New weekly MSO chart for Tuesday, 28 Apr 2026

Fig 1: New weekly MSO chart for Tuesday, 28 Apr 2026

https://www.dcceew.gov.au/energy/security/australias-fuel-security/minimum-stockholding-obligation/statistics

On this basis we can update our graphs:

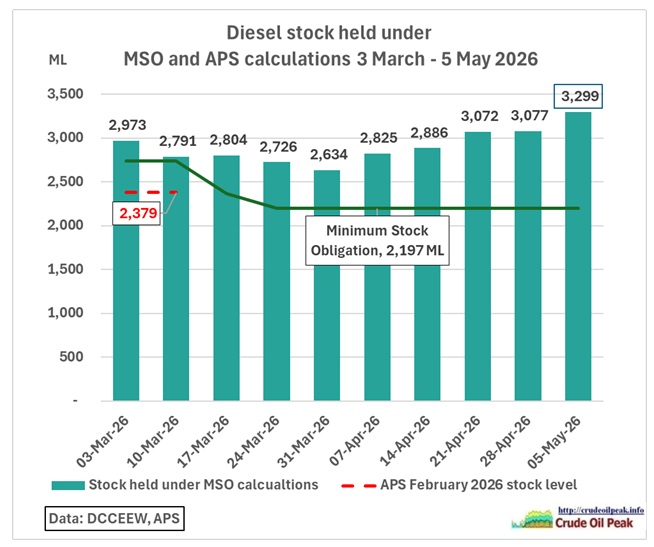

Fig 2: Diesel stock held, MSO requirement and onshore estimate

Fig 2: Diesel stock held, MSO requirement and onshore estimate

Diesel stock has substantially increased since a minimum on 31 March. What is the reason for this? We suspect more tankers on the way and counted in MSO reporting.

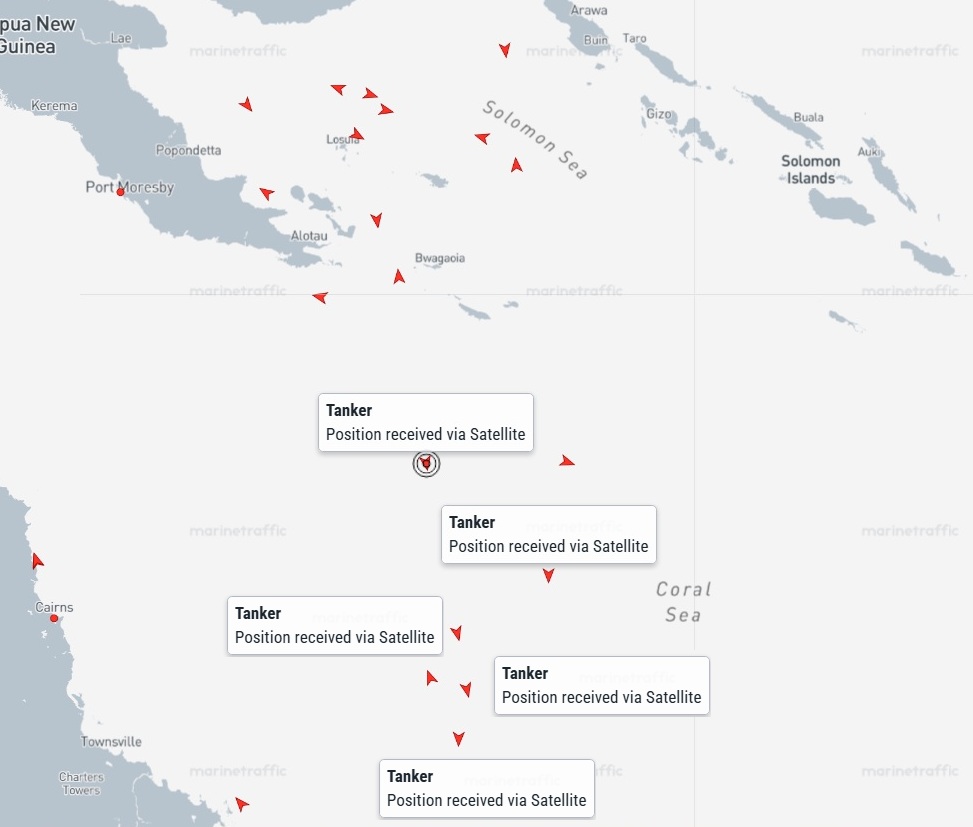

Tankers in Australia’s Exclusive Economic Zone (EEZ) – Coral Sea

Tankers in Australia’s Exclusive Economic Zone (EEZ) – Coral Sea

Tanker arrivals in Sydney are here:

https://crudeoilpeak.info/tankers-arriving-and-departing-in-sydney

So let us try to estimate onshore vs offshore stock. Reliable APS diesel stock levels at the end of February were 2,379 ML. This includes volumes in onshore tank farms and in tankers at ports discharging at or waiting for a berth. Just days later, on 3 March, MSO reporting put stock levels at 2,973 ML and that includes tankers in the 200 nautical mile EEZ zone (370 km). The ratio 2,379/2,973=80% onshore or 20% offshore.

Therefore, In the above graph, we add estimated onshore stock levels (red dashed line). We can see that the MSO was incidentally lowered by a similar amount, also 20%. The reason: although oil companies were technically compliant because their MSO total was above the mandate their physical, pumpable stock onshore was much lower. The government had to realize that the stock on water was not available to supply regional areas, especially in agriculture.

Now, 2 months down the track there is another reason to include onshore diesel in the graphs developed in previous posts. This is the graph in these posts updated with the numbers of Fig 1.

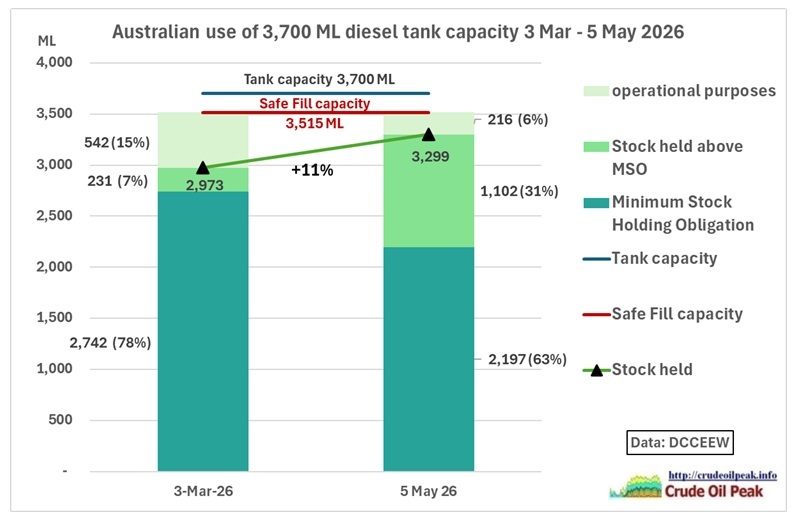

Fig 3: Diesel storage capacity is used up by a whopping 94% (3,299/3,515)

Fig 3: Diesel storage capacity is used up by a whopping 94% (3,299/3,515)

How is that possible? The diesel storage in 90 tanks (of course onshore) is 3,700 ML according to DCCEEW.

Deduct 5% for the unusable bottom of the tank and the top of the tank which is needed for venting and you arrive at 3,515 ML.

Deduct 5% for the unusable bottom of the tank and the top of the tank which is needed for venting and you arrive at 3,515 ML.

The operational volume is 3,515 ML – 2,197 ML (MSO) = 1,318 ML. The stock above the MSO level is shown as 1,102 ML = 84% filled. If these tank farms were really at these high levels, arriving tankers would not normally find empty tanks at ports to unload their fuel. This is logistically unworkable.

We need to understand that “obligated entities” have to report their imports after they have crossed the Australian EEZ boundary. See table in Fig 4 of the previous post

https://crudeoilpeak.info/australia-needs-a-higher-number-of-tankers-to-meet-fuel-import-requirements

or read here directly the legislation:

Fuel Security (Minimum Stockholding Obligation) Rules 2022

Part 2, rule 9

For subparagraph 21(b)(iv) of the Act, the circumstances are:

(a) the vessel is within the outer limits of Australia’s exclusive economic zone; or

https://www.legislation.gov.au/F2022L01450/latest/text

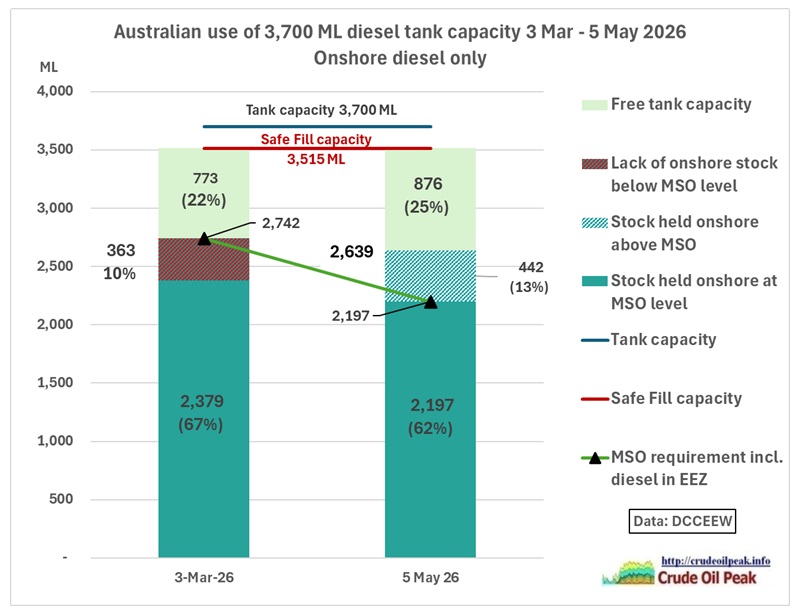

So we have to redo Fig 3 for onshore diesel only:

Fig 4: Use of diesel in onshore diesel farms

Fig 4: Use of diesel in onshore diesel farms

On 3 March, physical stocks were lower than the MSO requirement (including diesel in the EEZ). 2 months later, onshore stocks have improved from 2,379 ML to 2,639 ML (=260 ML equal to 4 Panamax LR1 tankers) after an enormous effort of the oil industry, supported by an unrelenting, international government campaign. Note that current onshore stock of 2,639 ML is still lower than the original MSO.

The operational volume of 1,318 ML would be one third full under the assumption of a 20% offshore ratio. It would be helpful to know operational levels in the main ports of capital cities.

So we can say the increase in diesel stock is caused by more stock in “floating storage” on tankers. Well done! Of course, the Energy Minister should inform the public about how many % of the stock is in onshore tank farms and how many % are offshore. Will any journo ask this question? Let’s see as we come to the 2nd part of the “same procedure”, the press conference, a bit later in the morning:

9 May

9 May

CHRIS BOWEN, MINISTER FOR CLIMATE CHANGE AND ENERGY: Thanks for coming everyone. Today I’m delivering the weekly update on the amount of fuel that we have in Australia and on the way.

….

We have 35 days’ worth of diesel, which is two days more than last week. In fact, that 35 days is the second highest amount of diesel we’ve had in Australia since the minimum stockholding obligation began in 2023.

……………..

We have 55 ships on the water, on the way to Australia, with various types of fuel. That’s one ship less than last week, but entirely in keeping with the sorts of numbers that we’ve been seeing since this international situation began, and in keeping with broader trends.

And we have 4.5 billion litres worth of fuel locked in to be delivered over the next four weeks. That’s half a billion litres more than my report last week.

Again, that’s a good thing. It shows that fuel is continuing to arrive in Australia as expected, and in keeping with the normal sorts of deliveries we would have at this time of year, not impacted by crisis.

We have 2.3 billion litres worth of diesel contracted to be delivered over the next four weeks, 783 million litres of petrol, 450 million litres of jet fuel, and 940 million litres of oil. That’s what makes up that roughly 4.5 billion litres of fuel.

That’s all contracted, locked in to be delivered over the next month.

………..

A one-man press conference in front of his electoral office In Fairfield, Sydney. Was Chris so successful in the past that journos think everything is OK and therefore did not bother to come?

A one-man press conference in front of his electoral office In Fairfield, Sydney. Was Chris so successful in the past that journos think everything is OK and therefore did not bother to come?

….I think we only have questions on the phone today, so over to the telephone.

JOURNALIST: Thank you, Minister. Stephanie from the ABC. This week, the Government announced the $10 billion fuel security package. Has the Government done any modelling on how much this amount could cost motorists at the bowser?

Stephanie Borys, ABC reporter from Canberra

Stephanie Borys, ABC reporter from Canberra

CHRIS BOWEN: Well, the $10 billion is, of course, the total cost of government investment.

What we’ve seen is that we’ve worked closely with industry to ensure that the policy that we’ve brought in is sensibly calibrated.

We do not anticipate any sizeable or meaningful impact on petrol prices, because we’ll work with industry to build the necessary storage.

And, of course, a big part of the announcement was a Federal Government-owned reserve, which won’t have any impact on petrol prices at all.

https://minister.dcceew.gov.au/bowen/transcripts/press-conference-sydney-nsw-7

No impact on petrol prices? Has the government-owned reserve not the function to avoid price spikes in the “next oil crisis”?

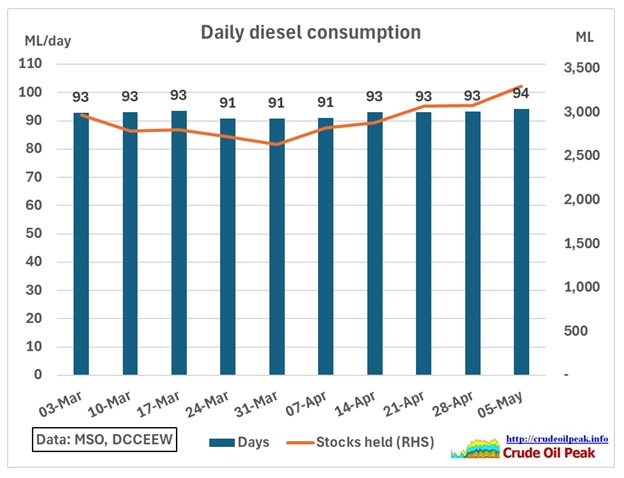

Stocks at 35 days of diesel. So we can calculate daily consumption in ML = stock in ML/days

For sure, the Minister will have taken both onshore and offshore stock:

Fig 5: Daily diesel consumption around 93 ML per day

Diesel consumption did not change much because it is the main fuel used in the economy, not optional. If anything, there was a small dip when stocks were low.

Using the other information in the Minister’s press conference we can now update more graphs:

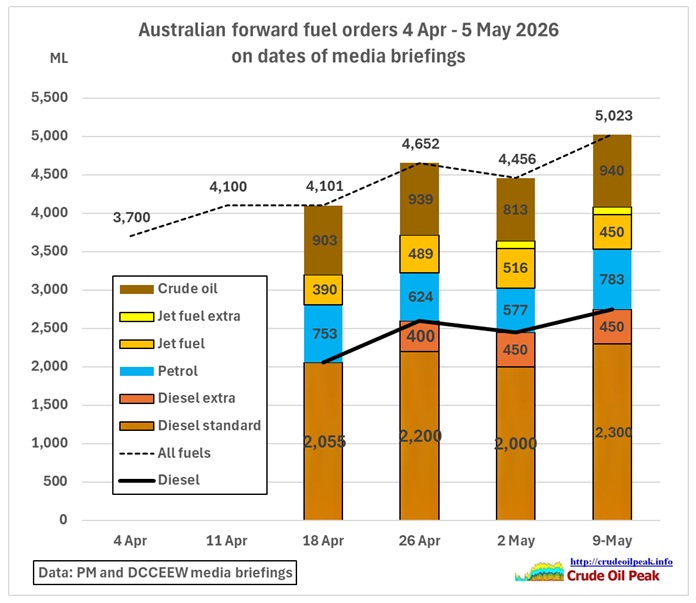

Fig 6: Forward fuel orders by fuel type

Fig 6: Forward fuel orders by fuel type

Diesel orders have slightly increased over 26 April, Petrol orders are up 36% compared to last week and jet fuel orders are struggling at -13%. Crude oil is back to previous levels because that’s what the 2 refineries need.

The $4.5 bn litres are the total 5,023 ML – extra orders of 550 ML = 4,473 ML

Note that no new extra supplies have been added.

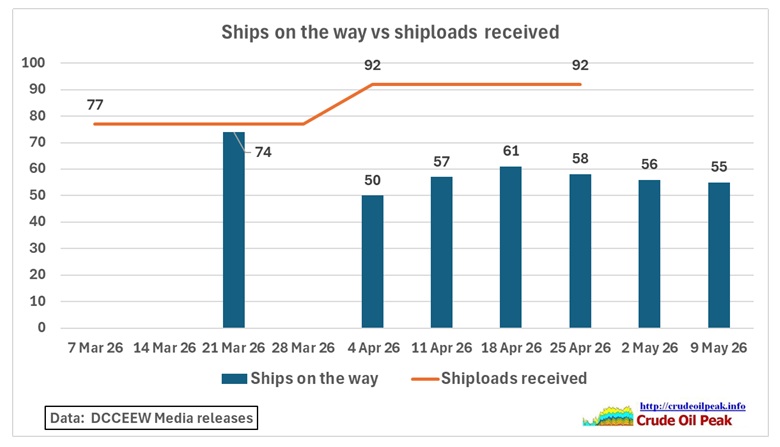

55 ships on the water

Fig 7: Number of ships on the way and shiploads received

Fig 7: Number of ships on the way and shiploads received

What we are not being told is the quantity and type of fuel on order. The number of shiploads was not updated (no 4-week running total).

Extra orders.

In the 10 April press conference:

JOURNALIST: That export finance deal yesterday, can you give us the indication of exactly how much extra fuel will be bought under that?

BOWEN: Well, EFA will update their public register every time that they do a transaction and that will be on the gazette, and obviously I’ll give updates too in my very regular press conferences. What we did yesterday was announce basically the deal with Viva and Ampol so that when they see a spot cargo come up, they can go and secure it. Basically, the arrangement’s already locked in with the EFA. Those spot cargoes come up at very short notice. They can be available for hours – you know, that a ship becomes available for sale, maybe in Korea or Malaysia, and companies have two or three hours to decide whether to buy it. We want them to have the flexibility to go and get that fuel for Australia and for Australians.

https://minister.dcceew.gov.au/bowen/transcripts/press-conference-fairfield-west-new-south-wales

So where is that Gazette? It should be here:

https://www.exportfinance.gov.au/our-organisation/about-us/transaction-register/202526-transaction-register/

When you load the latest PDF file

Commercial Account – Institutional transactions for 1 July 2025 to 14 April 2026

https://exportfinancecdn.azureedge.net/media/dyvaqfla/2026-april-30-transaction-register.pdf

you find no transaction dates and a search for “fuel” “Ampol” or “BP” has no results.

So we have to look at each individual announcement.

1. April 16 (100 ML Diesel): First fuel shipments secured — Initial 100 ML from Brunei/South Korea. https://www.exportfinance.gov.au/newsroom/first-fuel-shipments-secured-under-new-strategic-reserve-powers/

2. April 22 (200 ML Diesel): Securing more fuel and fertiliser — Added 200 ML, bringing the 7-day total to ~300 ML. https://minister.dcceew.gov.au/bowen/media-releases/joint-media-release-securing-more-fuel-and-fertiliser

3. April 24 (100 ML Diesel): Securing more fuel for the regions — Confirmed the total reached 400 ML. April 24 Joint Media Release: Securing more fuel for the regions https://minister.dcceew.gov.au/bowen/media-releases/joint-media-release-securing-more-fuel-regions

4. May 1 (50 ML Diesel + 100 ML Jet): Additional jet fuel and additional diesel secured — Finalised the 450 ML diesel and 100 ML jet fuel (550 ML total). https://www.exportfinance.gov.au/newsroom/additional-jet-fuel-and-additional-diesel-secured/

Conclusion:

Vital data are missing which would allow a full assessment of the current and future situation. Following improvements are necessary:

- In the weekly press conference, the Minister should explain the MSO graph

- Onshore/offshore data must be given

- The EFA website has to include a one-stop article with all rolling updates of named or numbered extra orders

- Consumption data

- Show the stock balance: EOM stock = BOM stock + imports + local refinery production – consumption