In December 2016, OPEC signed an agreement with 10 non-OPEC oil-producing countries to form OPEC+ in response to falling oil prices.

“The joint conference noted that OPEC Member Countries met on 30 November 2016 and decided to implement a production adjustment of 1.2 million barrels a day, effective from 1 January 2017.

Azerbaijan, the Kingdom of Bahrain, Brunei Darussalam, Equatorial Guinea, Kazakhstan, Malaysia, Mexico, the Sultanate of Oman, the Russian Federation, the Republic of Sudan, and the Republic of South Sudan committed to adjust their respective oil production, voluntarily or through managed decline, in accordance with an accelerated schedule. The combined reduction adjustment was agreed at 558,000 barrels a day for the aforementioned producers”

(Equatorial Guinea joined OPEC in May 2017).

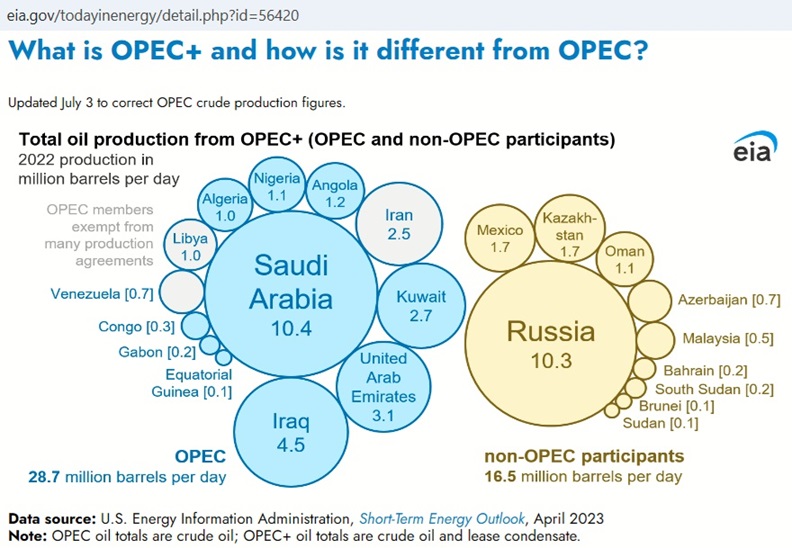

The EIA has this overview of OPEC+ with 2023 production: Fig 1: OPEC+ with original OPEC countries and non-OPEC participants

Fig 1: OPEC+ with original OPEC countries and non-OPEC participants

https://www.eia.gov/todayinenergy/detail.php?id=56420

The current OPEC and Non-OPEC production table was published at the 35th OPEC and Non-OPEC Ministerial Meeting on June 4th, 2023

https://www.opec.org/opec_web/en/press_room/7160.htm

This post is about production from these non-OPEC participants (10 countries)

Fig 2: Crude production of 10 Non-OPEC countries stacked

Fig 2: Crude production of 10 Non-OPEC countries stacked

The Soviet Union collapsed as a result of an energy crisis in the mid 80s. East bloc countries could not be supplied with sufficient quantities of Russian oil and did not have convertible currencies to buy oil on the global market.

4/10/2010 Russia’s oil peak and the German reunification

http://crudeoilpeak.info/russia%E2%80%99s-oil-peak-and-the-german-reunification

Production recovered using western technology.

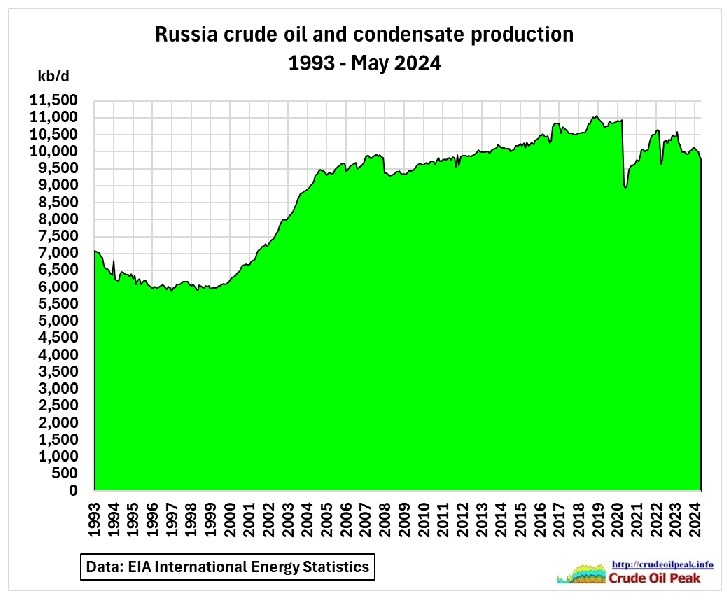

In the above graph Russia dominates (10 mb/d or 61%). The other countries are free riders which already peaked in 2007 at 7.7 mb/d (with a 2nd peak in 2011), in the last 12 months down to 6.3 mb/d (-18%).

Fig 3: Russia crude and condensate production

Fig 3: Russia crude and condensate production

At the end of the 1990s and the beginning of the 2000s, the massive outsourcing of Russian oilfield services to these Western companies led to dramatic increases in productivity. For example, the average Russian oil well increased production from approximately fifty-five barrels per day in 1995 to more than seventy-five barrels by the mid-2000s, a productivity growth of more than one-third. Should Western oilfield services completely depart Russia, this may result in comparable loss in average well productivity and, as a result, overall oil production. There are, however, strong indications that at least some of the Western oilfield-service companies continue to work with the Russian oil industry, reneging on their promises to leave. And of course Russian engineers are hardworking under adverse climatic conditions.

Fig 4: Russian crude oil and NGL production comparison with Rystad forecast

Fig 4: Russian crude oil and NGL production comparison with Rystad forecast

The above graph is superimposing Russian crude and NGL production curves with a Rystad forecast done in 2019 in an article titled “Lack of field sanctioning drives long-term oil production decline in Russia”

28 Feb 2022

Russian oil production update Nov 2021

https://crudeoilpeak.info/russian-oil-production-update-nov-2021

Russia is now a war economy

Military: Putin Issues Conscription Order On Energy Workers

23 Sep 2022

Russian president, Vladimir Putin, has ordered nearly 100% of Russia’s male energy sector employees to present themselves at recruitment offices.

https://www.orientenergyreview.com/oil-and-gas/military-putin-issues-conscription-order-on-energy-workers/?form=MG0AV3

Russian resilience amid sanctions may falter in face of technology gaps: experts

26 Apr 24

Russia has been surprisingly resilient in the face of oil and gas sanctions, but that resilience may not last too long because Russia has not found a market for its fuels as profitable as Europe was and because it lacks some key technology for the sector, experts said April 26.

“When you look under the hood, and you look at the different sub-sectors within the oil and gas industry, you see a surprising level of distress,” Craig Kennedy, an associate at Harvard University’s Davis Center for Russian and Eurasian Studies, said during a webinar hosted by the Center for the National Interest.

https://www.spglobal.com/commodityinsights/en/market-insights/latest-news/electric-power/042624-russian-resilience-amid-sanctions-may-falter-in-face-of-technology-gaps-experts

Russia’s war economy starves crucial oil industry of manpower

6 May 2024

Russia’s oil and gas industry has been crucial for bankrolling the invasion of Ukraine, giving the Kremlin the funds to keep fighting even as the conflict drags on through its third year. But the industry is facing a shortage of manpower as the full mobilization of Russia’s economy for war exacerbates a longstanding demographic crunch.

https://www.bloomberg.com/news/articles/2024-05-06/russia-s-war-mobilization-starves-its-crucial-oil-and-gas-industry-of-manpower

Let’s have a look at the other countries around Russia:

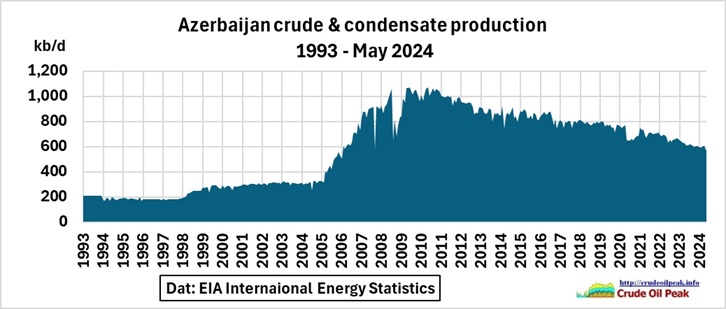

Fig 5: Azerbaijan crude and condensate production

Fig 5: Azerbaijan crude and condensate production

Azerbaijan peaked in 2009-2011 at 1.1 mb/d and has now declined to 0.6 mb/d, a drop by 47%.

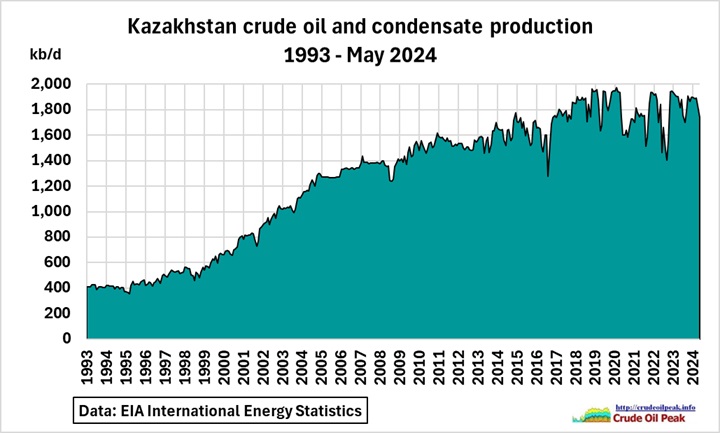

Fig 6: Kazakhstan crude and condensate production

Fig 6: Kazakhstan crude and condensate production

Kazakhstan is at peak for 4 years now (1.97 mb/d in Feb 2020)

And on with Asia:

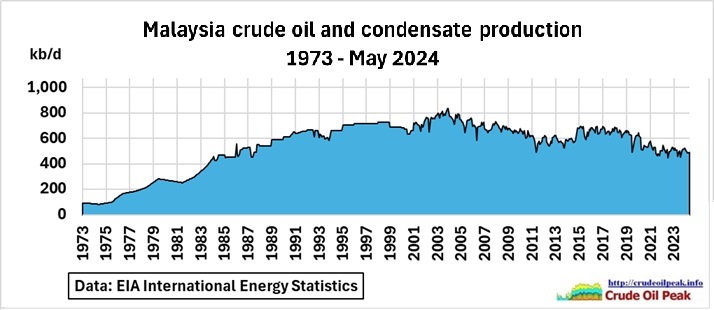

Fig 7: Malaysia crude and condensate production

Fig 7: Malaysia crude and condensate production

Malaysia peaked in 2003 at 840 kb/d. In the last 12 months, production was 500 kb/d, down 40% from the peak.

And to the Americas:

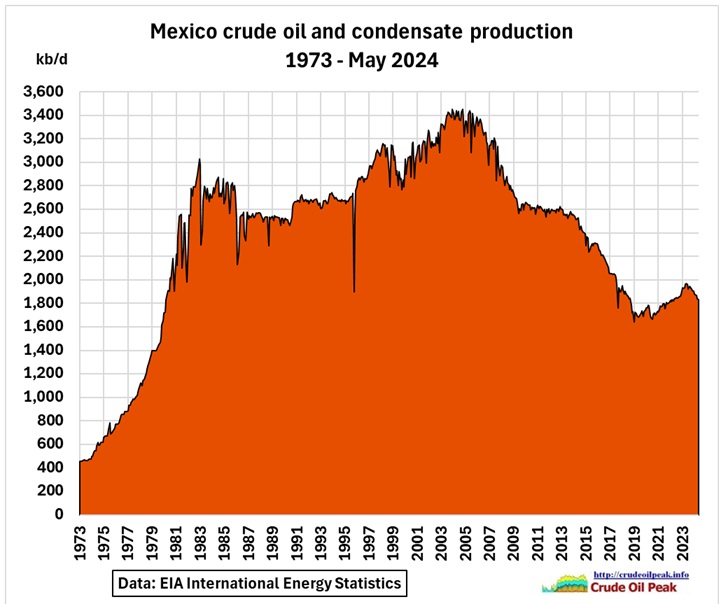

Fig 8: Mexico crude and condensate production

Fig 8: Mexico crude and condensate production

Mexico peaked at 3.4 mb/d in 2003-2004 (Cantarell oil field peak 2.12 mb/d but only 0.16 mb/d in 2022). The decline to 1.9 mb/d (last 12 months) was 45%.

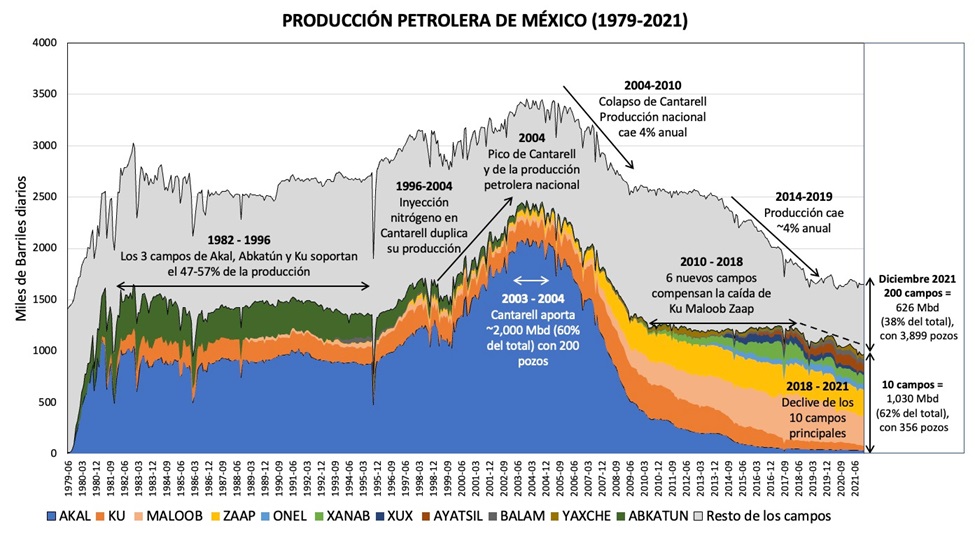

The following graph by the Mexican government https://conahcyt.mx/ shows the production by field up to 2021:

Fig 9: Production profile of 10 big fields and 200 smaller fields (grey area)

https://energia.conacyt.mx/planeas/hidrocarburos/produccion-crudo

CNH (Comision Nacional de Hidrocarburos) has scenarios which show that the uptick of production after 2021 as shown in the EIA data (Fig 7) can be maintained if not slightly improved.

https://hidrocarburos.gob.mx/media/4827/reporte-prospectiva-4to-trim.pdf?formCode=MG0AV3

Peak oil in Mexico has contributed to the migration to the US.

And here 3 countries in a geostrategic location:

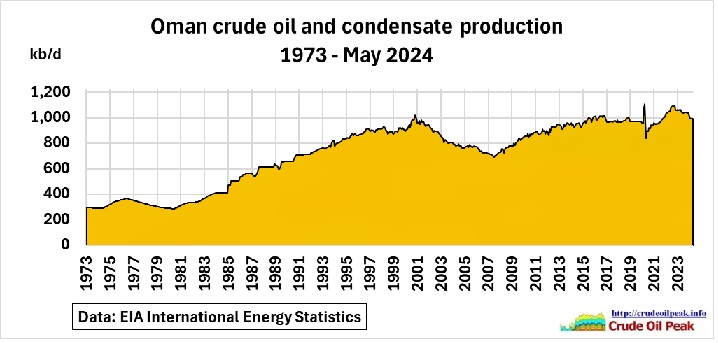

Fig 10: Oman crude and condensate production

Fig 10: Oman crude and condensate production

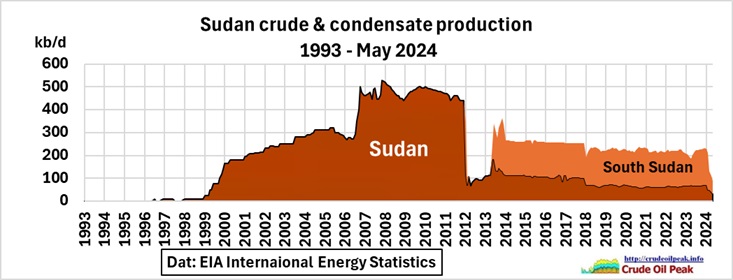

Fig 11: Sudan crude and condensate production

Fig 11: Sudan crude and condensate production

The peak in production 2010 exacerbated the ethnic conflicts between the North (Khartoum) and South Sudan (Juba).

31/5/2011 Sudan’s Nile blend in decline – why we should be concerned

http://crudeoilpeak.info/sudan-nile-blend-in-decline-why-we-should-be-concerned

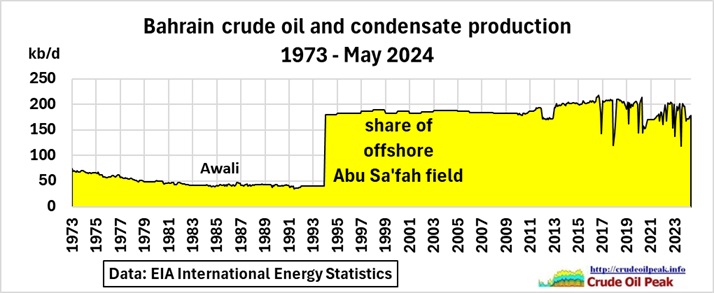

Fig 12: Bahrain crude and condensate production

Fig 12: Bahrain crude and condensate production

To be continued on quotas