Any volunteers?

This is the 2nd post on the best slides shown at the October 2009 ASPO conference

http://peak-oil.org/2009-conference-proceedings/

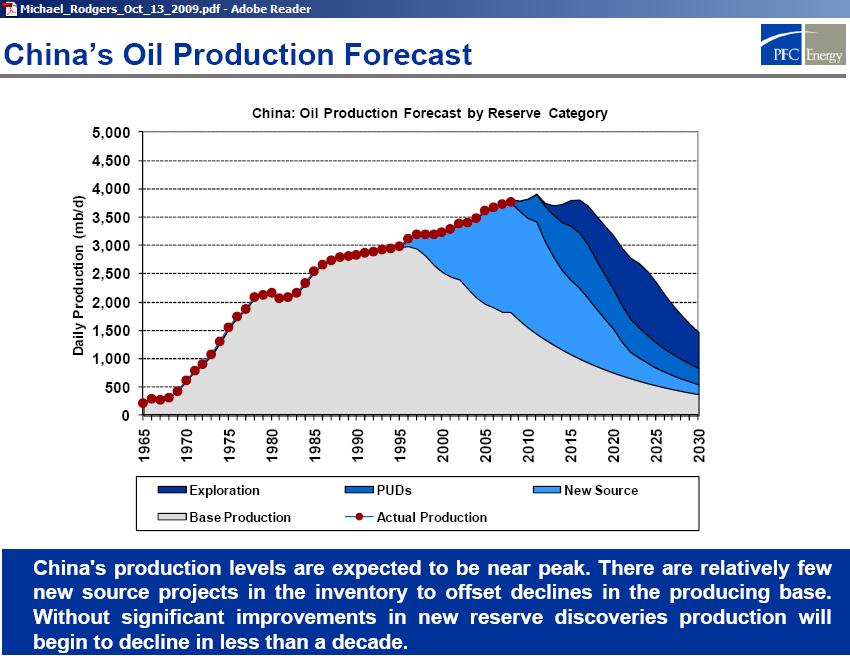

PFC Energy presented a graph showing Chinese oil production arriving at a bumpy production plateau in 2008. The profile is typical for the process of peaking. A majority of mature oil fields peaked around 1997 and is now in irreversible decline. Since then, a new group of fields (light blue) has been aggressively produced, which has lead to the current peak. However, this growth has come at a price. Decline in existing fields is now steeper than before, at around 6% pa. So a new generation of fields has to come on-stream very fast to offset that decline.

PUD=Proved Undeveloped

http://aspo-usa.com/2009presentations/Michael_Rodgers_Oct_13_2009.pdf

PFC Energy writes: “Without significant improvements in new reserve discoveries production will begin to decline in less than a decade”

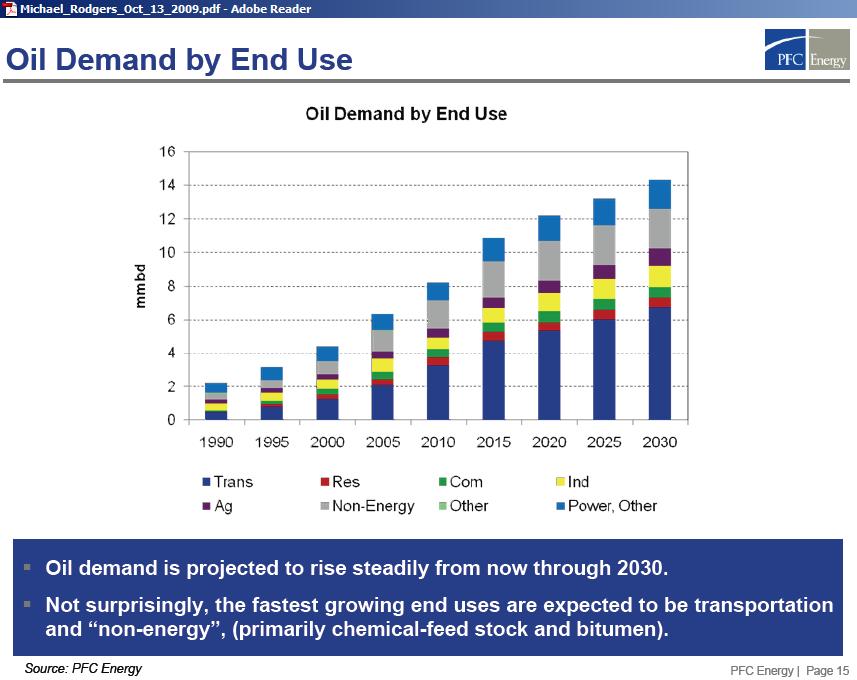

This graph shows Chinese oil demand growing at 3.75% pa over the next 20 years. Around half of the oil is used for transport.

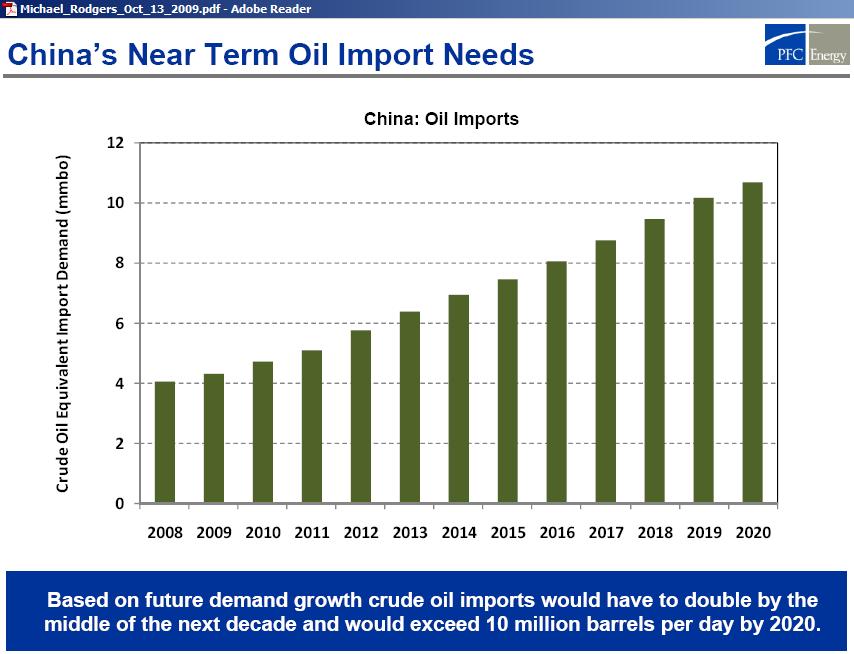

Production on a plateau and rising demand translates into increasing oil import requirements.

PFC Energy: “….crude oil imports would have to double by the middle of the next decade and would exceed 10 million barrels per day by 2020″. So the additional imports would need to be in the order of 6 mb/d by 2020. In another graph of the same presentation PFC expects global crude oil production to be just 3 mb/d higher in 2020 than now. Taken from the graph:

2005: 70.3 mb/d

2010: 72.4 mb/d

2015: 72.9 mb/d

2020: 75.5 mb/d

This means that under the assumption that all additional crude goes to China there is still a shortfall of 3 mb/d. So who is going to save that much to allow China to grow?

http://aspo-usa.com/2009proceedings/Michael_Rodgers_Oct_13_2009.pdf

PFC Energy’s estimate of global crude oil production for 2020 may, however, be too high. In its 2004 presentation to the Centre for Strategic and International Studies

PFC Energy overestimated Russian production by 4.5 mb/d. The crude oil graphs on this web site clearly show that Russia is also on a production plateau. So the savings in the rest of the world to allow China to grow would have to be quite higher than 3 mb/d.

https://www.iea.org/publications/freepublications/publication/WEO_2007.pdf

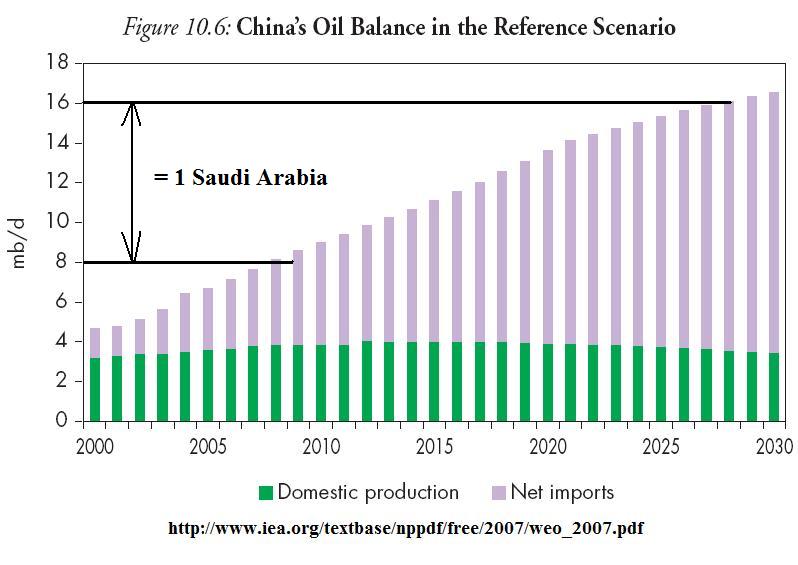

Another view of this problem was shown in the International Energy Agency’s WEO 2007. The IEA also estimates oil import requirements by 2020 to be in the order of 10 mb/d but sees Chinese production after 2020 to decline much more gently than PFC Energy, apparently assuming substantial new discoveries.

In any event, where is one more Saudi Arabia?

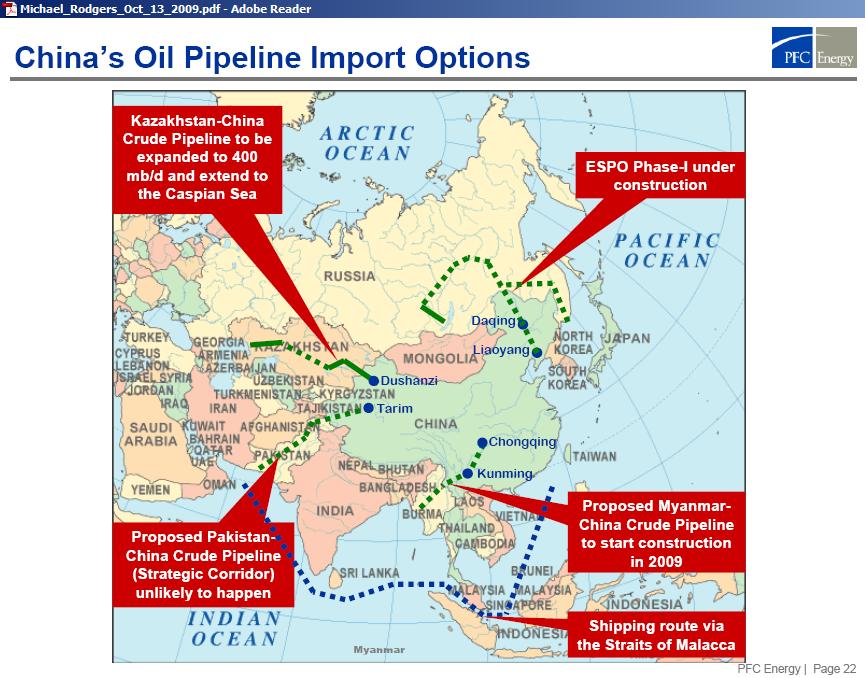

PFC Energy shows the oil import corridors for China:

Apart from the shipping route via Singapore we see 4 pipelines

(1) from Kazachstan

(2) via Pakistan (proposed)

(3) via Myanmar (proposed)

(4) from Russia

Post recreated from http://www.crudeoilpeak.com/?paged=98