3 complacent governments (Howard, Rudd/Gillard, Abbott) released 3 flawed Energy White Papers (2004, 2012 and 2015) which have promoted and facilitated massive LNG export projects on Australia’s West, North and East Coasts. On the East Coast, on-shore coal seam gas is used as feedstock and that has caused a domestic gas crisis as conventional gas production is peaking since 2000, something already Howard knew it would happen. So we have the bizarre situation that Australia plans to build LNG import terminals on the East Coast, for domestic use.

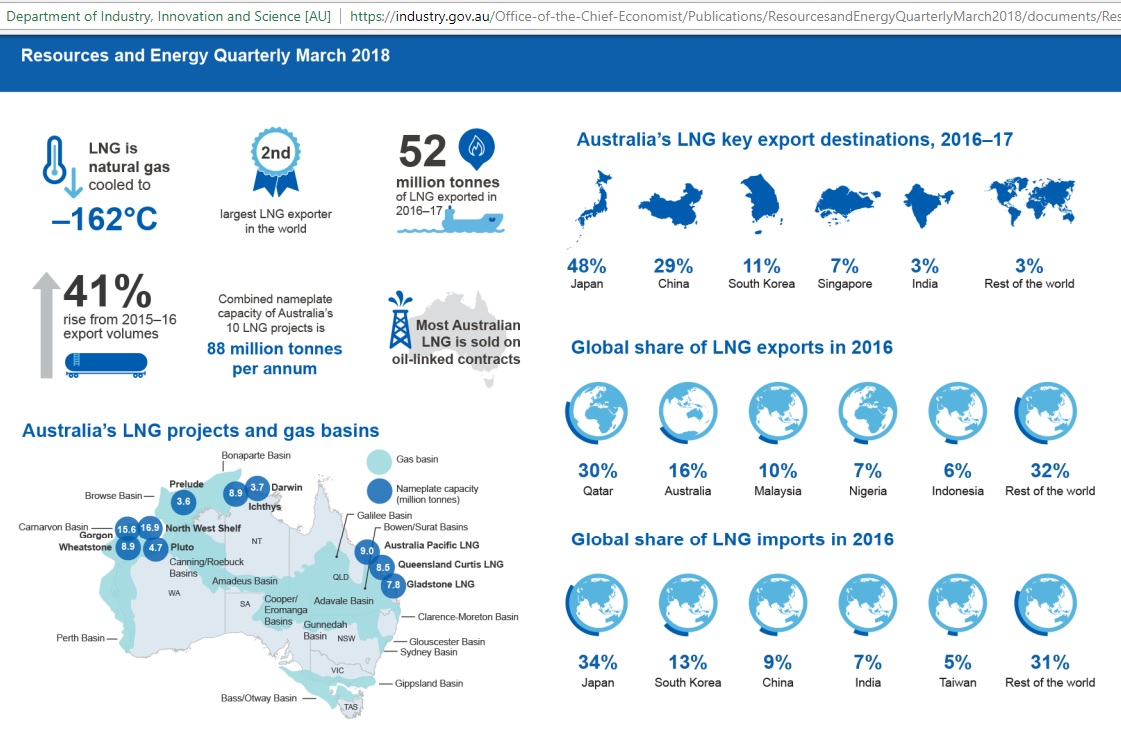

What an embarrassment for a government where the Chief Economist is proud to announce Australia to be the 2nd largest LNG exporter in the world:

Fig 1: Chief Economist’s quarterly report

Fig 1: Chief Economist’s quarterly report

https://industry.gov.au/Office-of-the-Chief-Economist/Publications/ResourcesandEnergyQuarterlyMarch2018/documents/Resources-and-Energy-Quarterly-March-2018.pdf

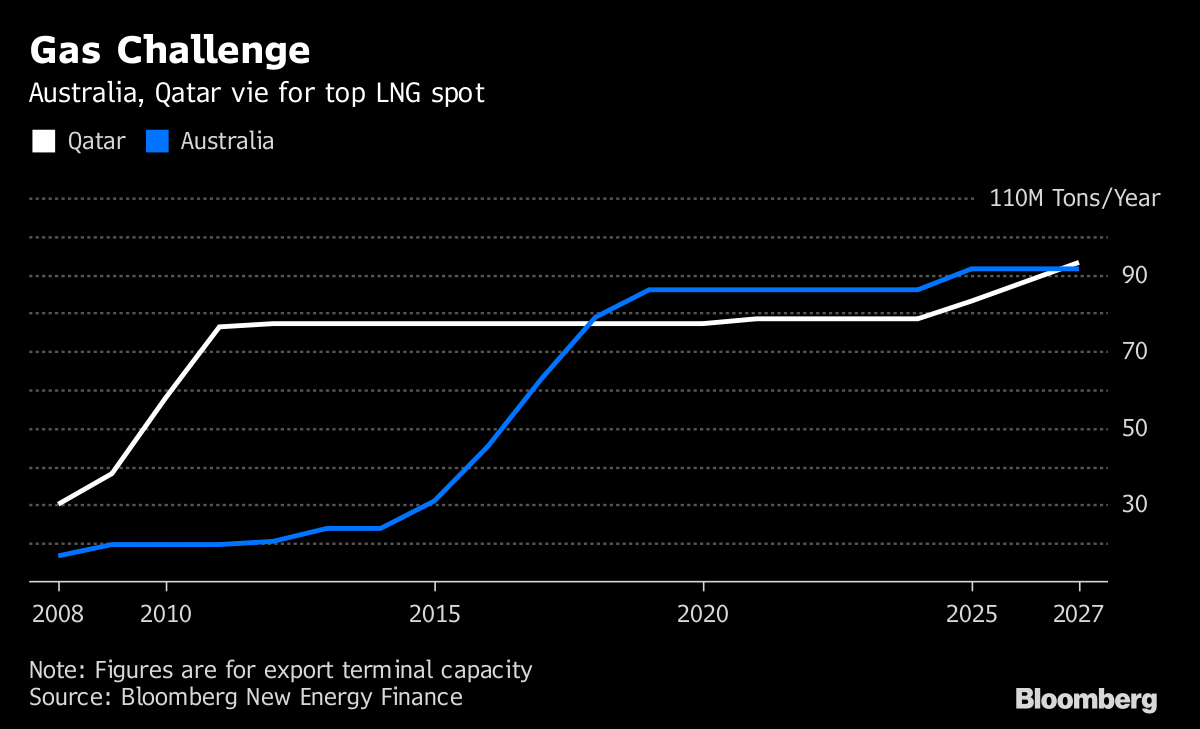

……competing with Qatar and attracting the attention of Bloomberg:

Fig 2: Australia’s LNG exports to challenge Qatar

Fig 2: Australia’s LNG exports to challenge Qatar

To be sure: consultants, financial planners, contractors and gas traders can’t wait to make money from an import terminal. It’s the consumers who will have to pay for the wrong decisions of previous Resource and Energy Ministers.

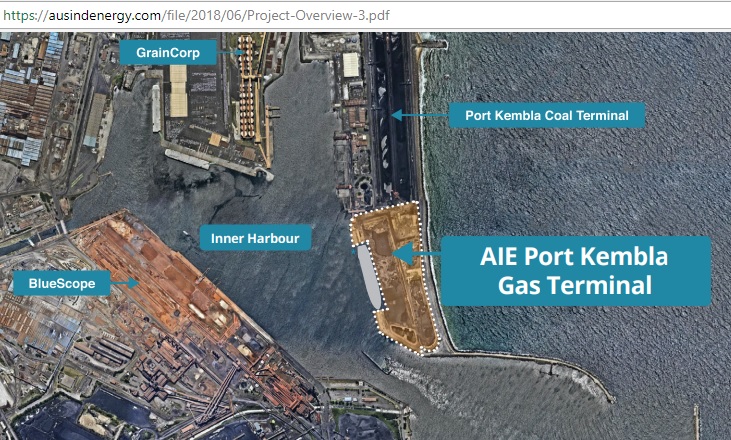

Fig 3: Location for a Port Kembla Gas Terminal 100 PJ pa for 70% of NSW requirements

Fig 3: Location for a Port Kembla Gas Terminal 100 PJ pa for 70% of NSW requirements

https://ausindenergy.com/file/2018/06/Project-Overview-3.pdf

How did it come to this?

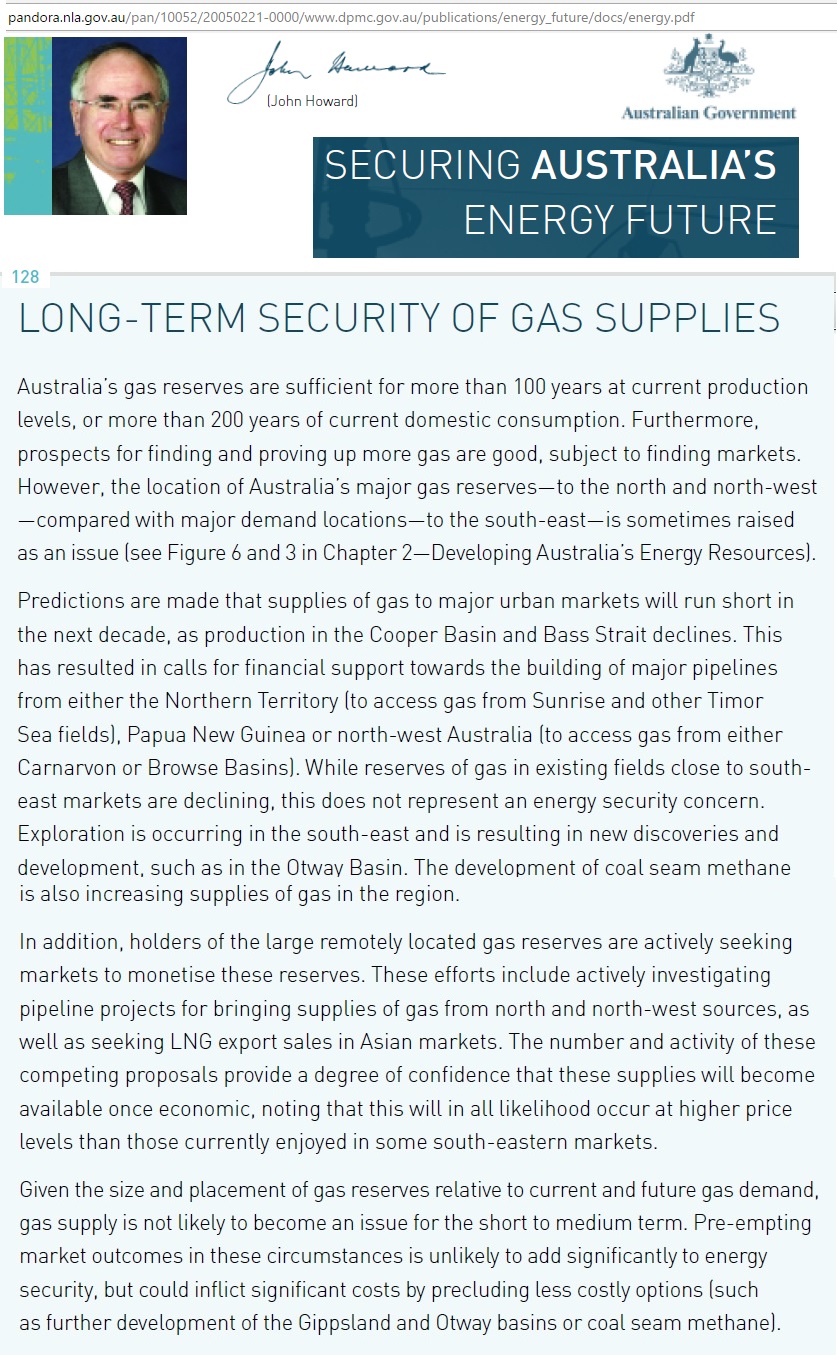

EWP 2004 (Howard government)

Just 14 years ago then Prime Minister Howard wrote a self-content, reassuring chapter on gas in his June 2004 energy white paper (EWP):

Fig 4: Extract from Howard’s energy white paper published in June 2004

Fig 4: Extract from Howard’s energy white paper published in June 2004

http://pandora.nla.gov.au/pan/10052/20050221-0000/www.dpmc.gov.au/publications/energy_future/docs/energy.pdf

We see here the naïve assumption that the “market” will ensure energy security. Note that the expected decline in Cooper and Bass Strait did not cause Howard to take peak conventional gas seriously. He also ignored peak oil in an exchange of letters I had with him. He did not understand that coal seam gas as unconventional gas was fundamentally different from conventional gas. So verbal arguments and untested assumptions were made instead of thorough technical investigations, independent from the wishes of the oil and gas industry. The underlying mindset is complacency. The focus on LNG exports also demonstrates Australia’s quarry mentality.

EWP 2012 (Rudd/Gillard government)

The Rudd/Gillard government which came to power end 2007 lost no time to repeat on the East Coast what Howard had done on the West Coast: massive LNG export projects, this time supplied from coal seam gas, a less profitable business than conventional gas as CSG has no liquids which provide additional revenue. In March 2010, then Resource Minister Martin Ferguson attended in Beijing the signing of an agreement between QCLNG and CNOOC for the supply of 8.5 mt pa of LNG to China.

Fig 5: QCLNG on Curtis Island in Gladstone, Queensland

Fig 5: QCLNG on Curtis Island in Gladstone, Queensland

https://www.gladstoneobserver.com.au

At that time, the Rudd government had no current energy white paper. A public consultation process had started in 2008 (the year of the oil price shock) but was delayed by a carbon pricing debate both within the government and the Parliament. The final EWP, entitled “Australia’s energy transformation” was only released in October 2012.

This follows a typical pattern in Australia where decisions on physical projects are made and later policy papers are cleverly written to confirm they are in line with policies.

Rudd/Gillard’s EWP 2012 was slightly more detailed than Howard’s because in the meantime there were 8 additional years of experience with gas markets. The gas reserves (136 tcf including 33 tcf CSG) were comfortably calculated at an irrelevant 184 years of current production rates.

But first problems emerged with LNG starting to impact on the domestic market:

“Nonetheless, pressures are emerging in the market. Recent floods in Queensland slowed CSG production, and some LNG producers have begun to supplement contracted reserves in the ramp‑up period from conventional supplies in the Cooper Basin (DEEDI 2012). The 2012 Queensland gas market review has pointed to suggestions that some LNG producers may also be building contracted gas positions to preserve options for further LNG train development (DEEDI 2012)” (p 140)

That is the opposite of Howard’s assumption that LNG projects will also increase the availability of domestic gas supplies.

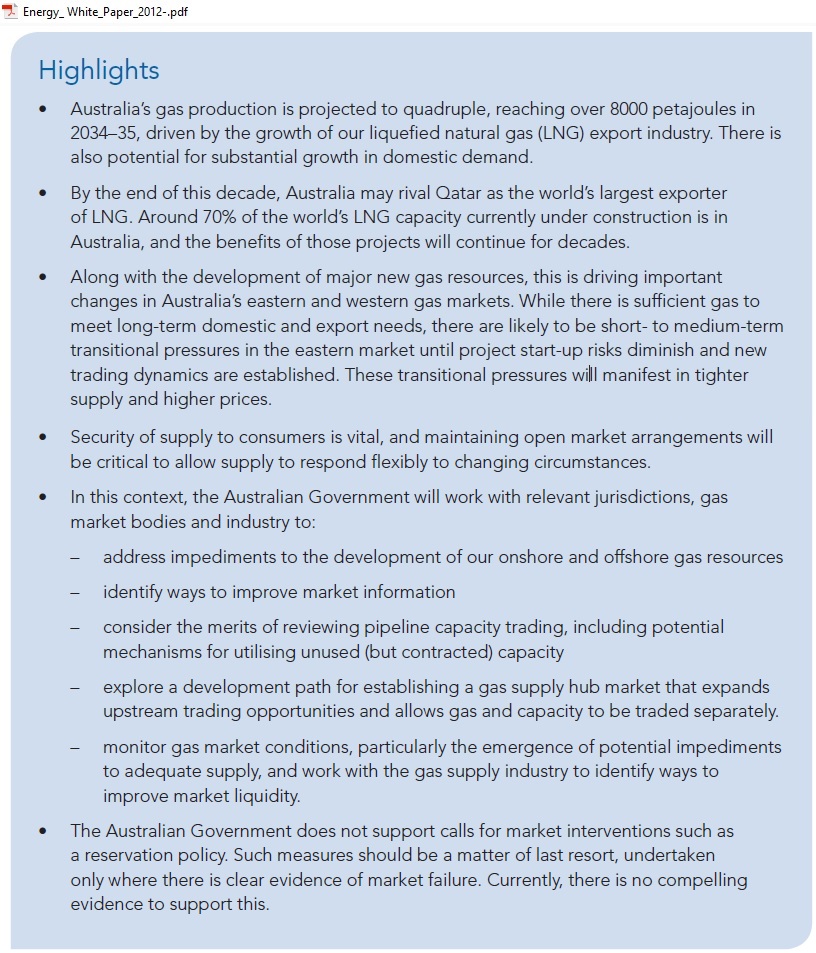

Despite this apparent failure of both the Queensland and Federal governments to keep international and domestic gas markets separate the “policy high lights” in the EWP 2012 recommended not to introduce a reservation policy. Obviously, international investors were given certain promises.

Fig 6: Extract from chapter 9 of the energy white paper 2012

Fig 6: Extract from chapter 9 of the energy white paper 2012

https://www.aip.com.au/sites/default/files/download-files/2017-09/Energy_%20White_Paper_2012-.pdf

Note the embellishing words like “transitional pressures”, “trading dynamics” and “open market arrangements”. No domestic gas demand forecast was done. A statement in the draft EWP 2011 “However, supply is expected to meet aggregate domestic and LNG export demand out to 2031 in all scenarios modelled by AEMO in the 2011 Gas Statement of Opportunities.” was dropped, most likely because that could no longer be guaranteed.

EWP 2015 (Abbott government)

In 2013, Howard’s Resource Minister Ian MacFarlane is back in his job and delivers another energy white paper in April 2015. Here are some extracts which speak for themselves:

“Australia is a growing energy superpower” (p iv)

“Despite cost reductions from the removal of the carbon tax, gas prices are rising as they move toward parity with an international price. This is due to Australia’s increasing links to international gas markets and rising domestic production costs.” (p 3)

“A key to better market outcomes is to limit the role of government in markets.” (p 4)

“Gas reservation is not supported by the Australian Government. Reservation would have negative consequences for the economy. Requiring a proportion of gas production to be reserved for the domestic market would act as a tax on the production of LNG. This would reduce profits from gas production, leading to fewer economic benefits that would not be offset by gains in other sectors of the economy. Less profitable gas production would attract less investment, resulting in reduced gas supply in the longer-term.

Gas reservation is effectively a subsidy to domestic gas users. Artificially low domestic prices do not encourage gas users to use gas more efficiently or encourage innovation in the use of alternative fuels and processes. Ongoing investment in infrastructure that may not be required if users found alternatives to gas or used gas more efficiently is not efficient investment.” (p 20)

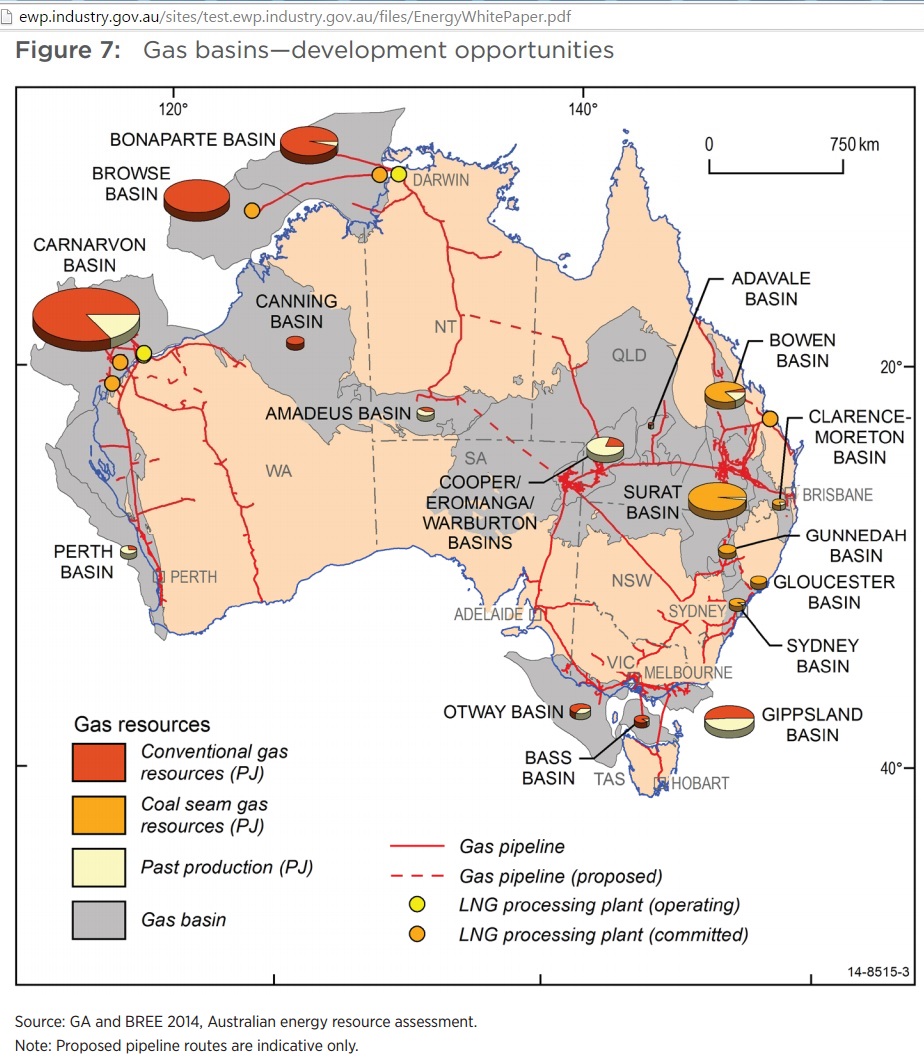

Fig 7: Gas resource map in EWP 2015, p 20

Fig 7: Gas resource map in EWP 2015, p 20

http://minister.industry.gov.au/ministers/macfarlane/media-releases/energy-white-paper-maps-australias-powerful-future

Note that the above map has no numbers attached to the pie charts nor are gas reserves given (different from resources) although the Australian Energy Resource Assessment (AERA) 2014 report has these details on p 82

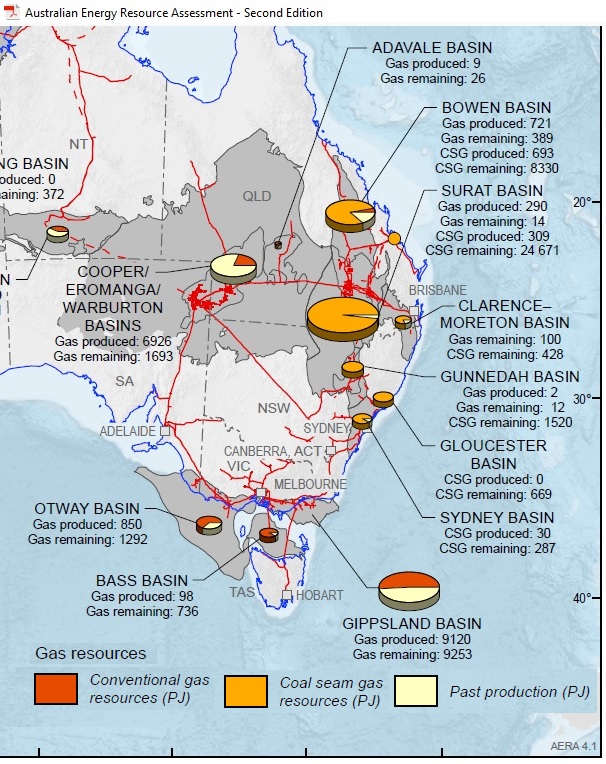

Fig 8: Gas resource map South East Australia

Fig 8: Gas resource map South East Australia

https://arena.gov.au/assets/knowledge-bank/79675_AERA.pdf

From the above we can calculate:

Conventional gas resource depletion in 2014

|

In PJ |

Produced | Remaining Resources | Total Original

Resources |

Depletion level |

| Gippsland | 9,120 | 9,253 | 18,373 | 49.6 % |

| Bass | 98 | 736 | 834 | 11.8 % |

| Otway | 850 | 1,292 | 2,142 | 39.7% |

| Cooper/Eromanga | 6,926 | 1,693 | 8,619 | 80 % |

| All conventional | 16,994 | 12,973 | 29,967 | 56.7% |

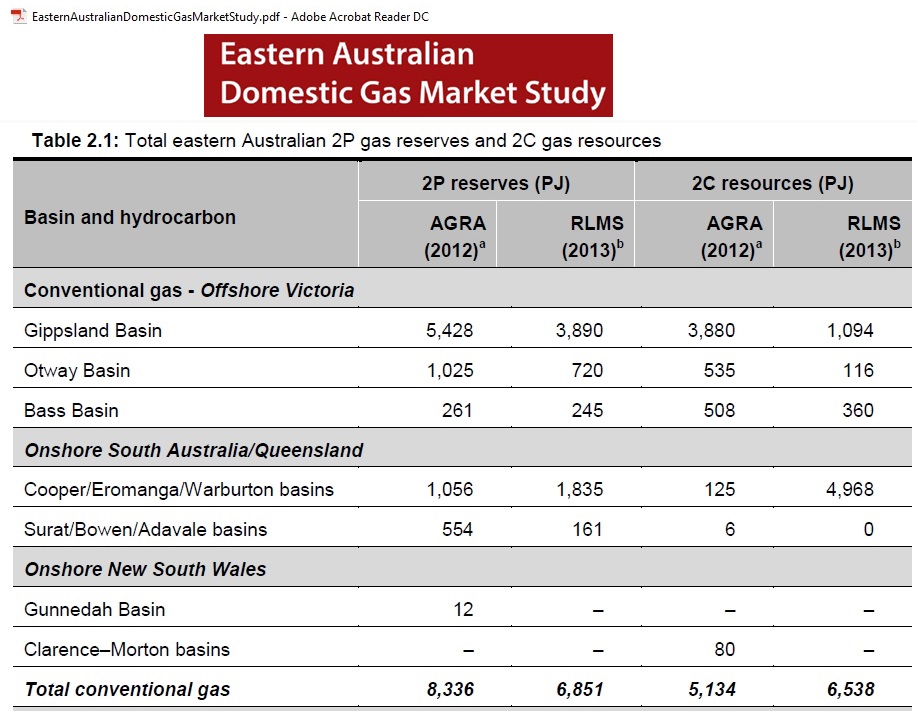

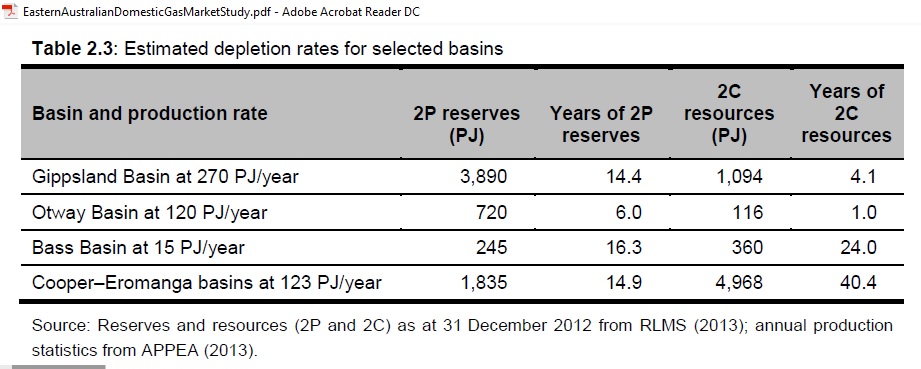

A depletion rate of greater than 50% means that it will be more difficult and costly to produce gas in future. Let’s find out how much of the remaining resources are actually proven and probable (2P) reserves. They can be found in the Eastern Australian Domestic Gas Market Study of the Department of Industry (2014). This report is no longer available on the departmental website but on a parliamentary committee page:

Fig 9: East Coast conventional gas reserves and resources

Fig 9: East Coast conventional gas reserves and resources

There are 2 sources: AGRA (Australian Gas Resource Assessment) and RLMS (Resource and Land Management Services). Their total for 2P and 2C of around 13,400 PJ is the same and also in line with the above table. But there is a big difference in where these resources are. AGRA puts most of them into Gippsland, RLMS into Cooper.

In chapter 4.2 the Domestic Gas Market study asks the question how long gas production will continue.

Fig 10: Estimated reserve/production ratios using RLMS data

Fig 10: Estimated reserve/production ratios using RLMS data

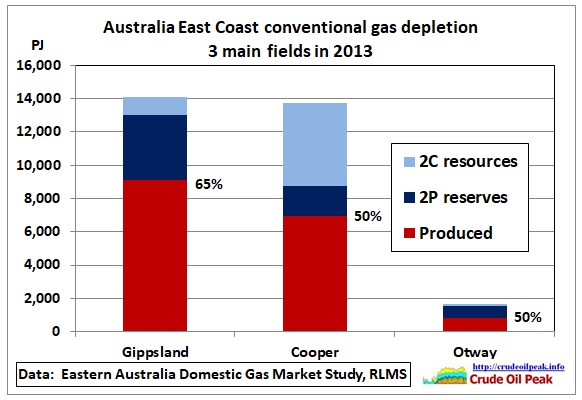

Let’s put that into a graph

Fig 11: Conventional gas depletion on East Coast

Fig 11: Conventional gas depletion on East Coast

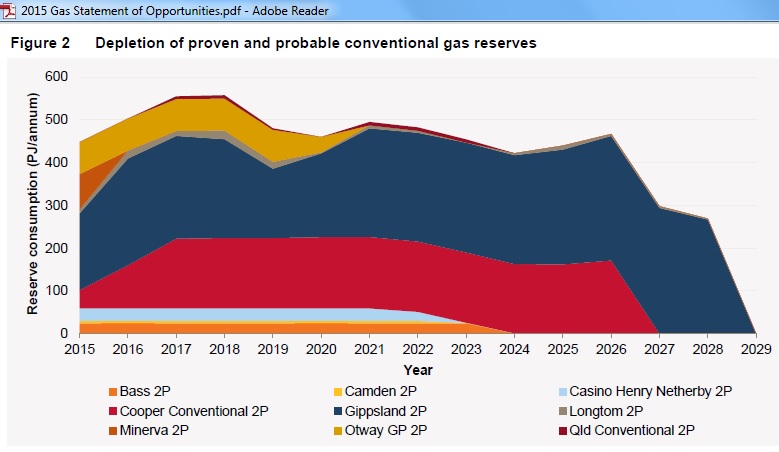

The EWP 2015 did not resolve the resource issues in Fig 8, nor did it inform the reader that 2P reserves will basically be exhausted by the end 2020s as shown in AEMO’s GSOO 2015 which was published in the same month as the WEP 2015.

Fig 12: 2P gas reserve depletion in NSW, SA and Victoria (AEMO GSOO Apr 2015)

Fig 12: 2P gas reserve depletion in NSW, SA and Victoria (AEMO GSOO Apr 2015)

https://www.aemo.com.au/Gas/National-planning-and-forecasting/Gas-Statement-of-Opportunities/2015-GSOO

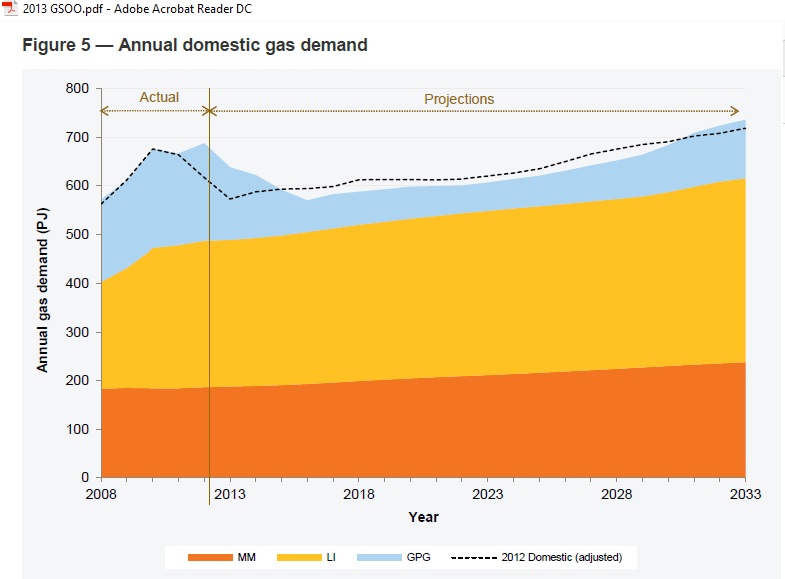

Just like in the previous energy white papers the EWP 2015 did not calculate/update the domestic gas production and consumption balance for the next 15 years, although a consumption graph was available in AEMO’s Gas Statement of Opportunities 2013.

Fig 13: Domestic gas demand

Fig 13: Domestic gas demand

http://www.aemo.com.au/media/Files/Other/planning/gsoo/2013/2013%20GSOO.pdf.pdf

MM=Mass Market (residential and business), LI=Large Industrial (10 TJ/a), GPG=Gas powered generation

The dip in GPG was expected by rising gas prices and lower carbon pricing projections.

Conclusion:

Australia’s energy white papers do not always summarize adequately and timely the research other departments have done on relevant topics. All 3 energy white papers under 3 different governments assumed that the domestic gas market would benefit from developing gas resources for the export market, like bread crumbs falling from the tables of a big feast which was promoted by governments. And we were told governments should stay out of markets. Howard’s energy white paper thought no alternative transport fuels were needed to get away from Australia’s oil dependency. As a result, gas as such an alternative fuel is now being exported from Gladstone in quantities energy equivalent to Australia’s total liquid fuel consumption. The public will become aware of this when it is too late.

Previous posts:

20/10/2017

Australia’s east coast gas crisis will be permanent

http://crudeoilpeak.info/australia-east-coast-gas-crisis-will-be-permanent

27/3/2017

Howard’s energy super power stuck in domestic gas shortages

http://crudeoilpeak.info/howards-energy-superpower-stuck-in-domestic-gas-shortages

7/4/2015

Australia’s alternative transport fuel: The East Coast gas-ship has sailed

http://crudeoilpeak.info/australias-alternative-transport-fuel-the-east-coast-gas-ship-has-sailed