This is part 2 of the series “Can NSW replace Liddell?”

I good test of what will happen when Liddell closes permanently end of April 2023 happened on 6 March 2023 when temperatures in Sydney reached 38ᵒ while 1.000 MW of coal plants were actually offline. We’ll do comparisons to part 1 which described the situation on 20 Feb 2023, a day before the Australian Energy Market Operator (AEMO) warned about reliability risks in NSW in 2023/24 due to the delay in commissioning the Kurri Kurri gas peaking plant.

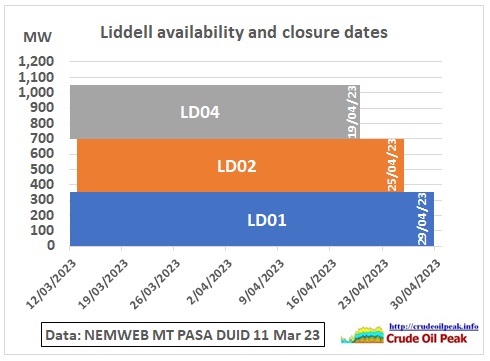

Fig 1: Liddell closing dates

Fig 1: Liddell closing dates

http://www.nemweb.com.au/REPORTS/CURRENT/MTPASA_DUIDAvailability/

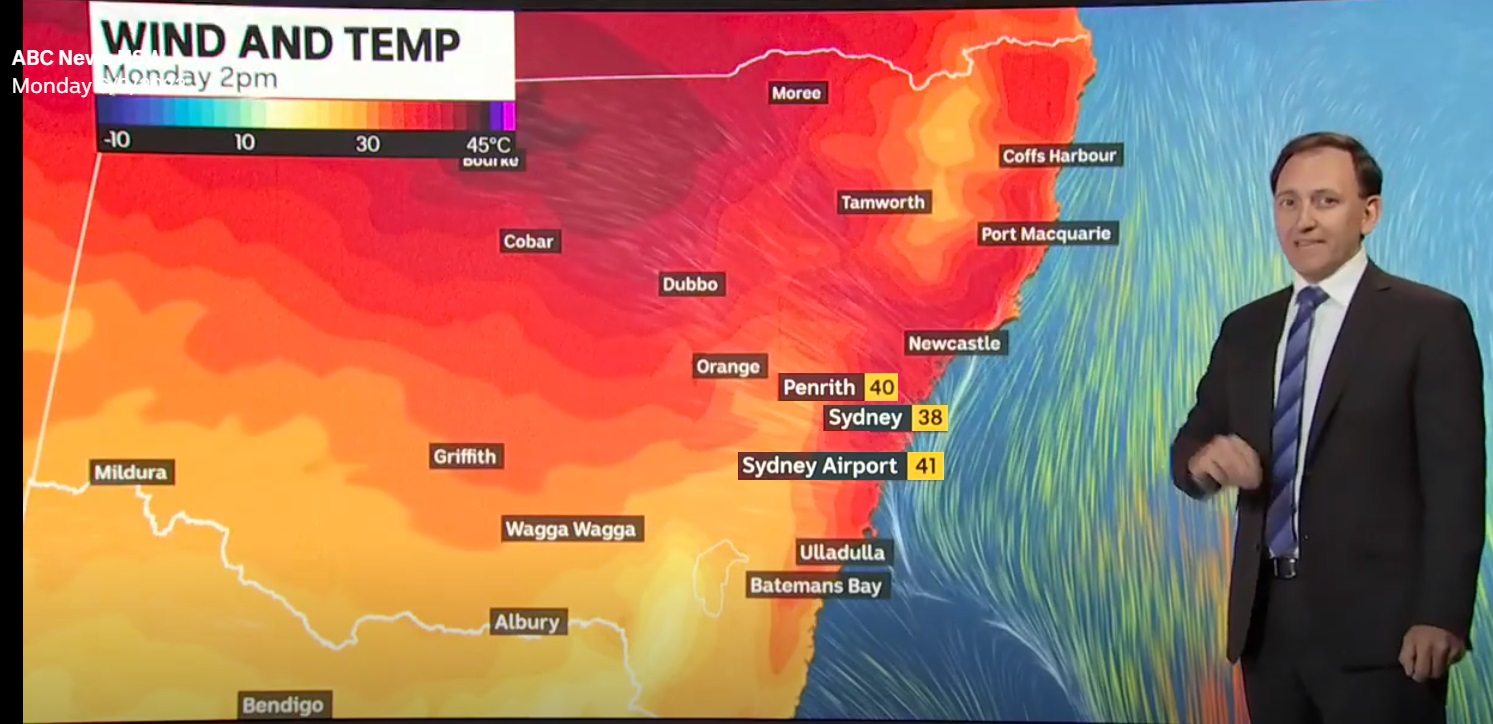

Fig 2: Hot air coming from the North and North-West,

Fig 2: Hot air coming from the North and North-West,

blocking a southerly change

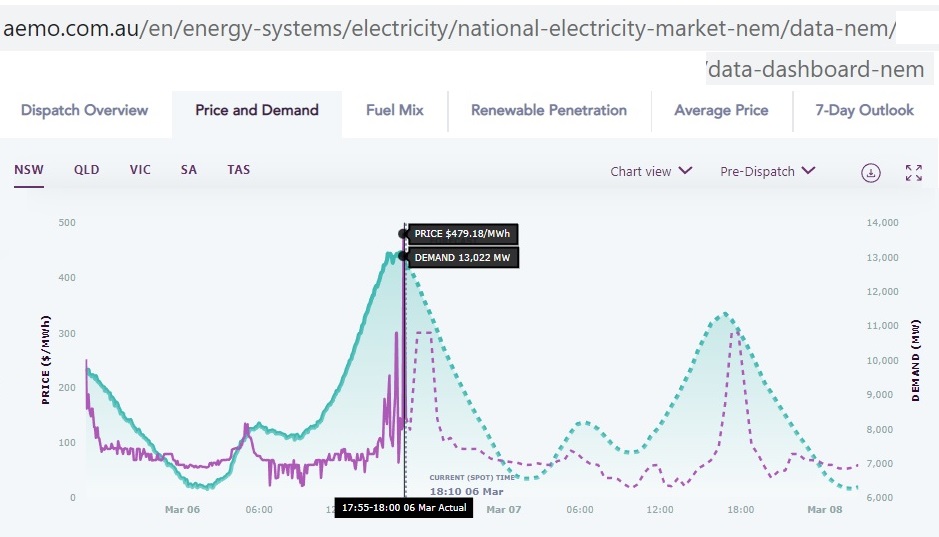

Fig 3: NSW power demand shot up to 13,000 MW at 6 pm

Fig 3: NSW power demand shot up to 13,000 MW at 6 pm

That demand created a price spike of $480/MWh

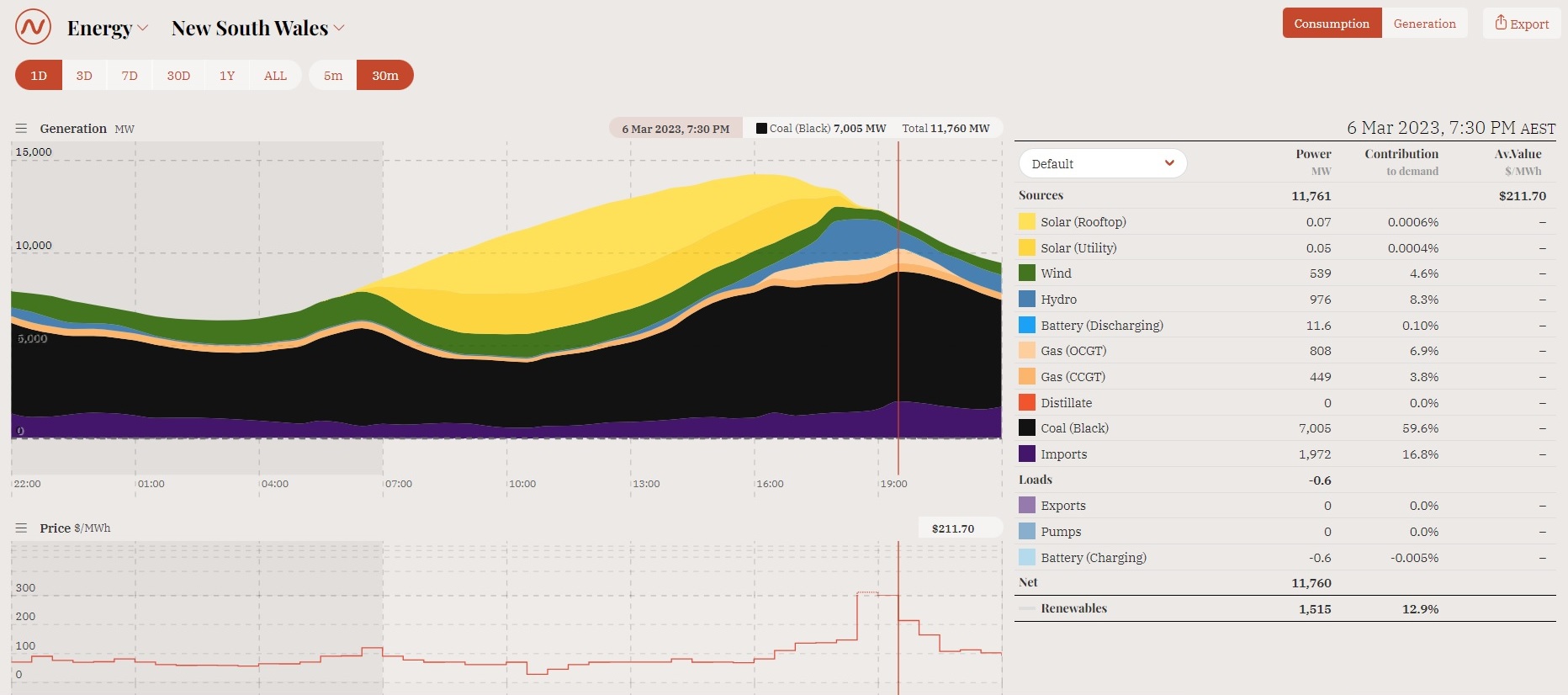

Fig 4: NSW power generation by type of fuel

Fig 4: NSW power generation by type of fuel

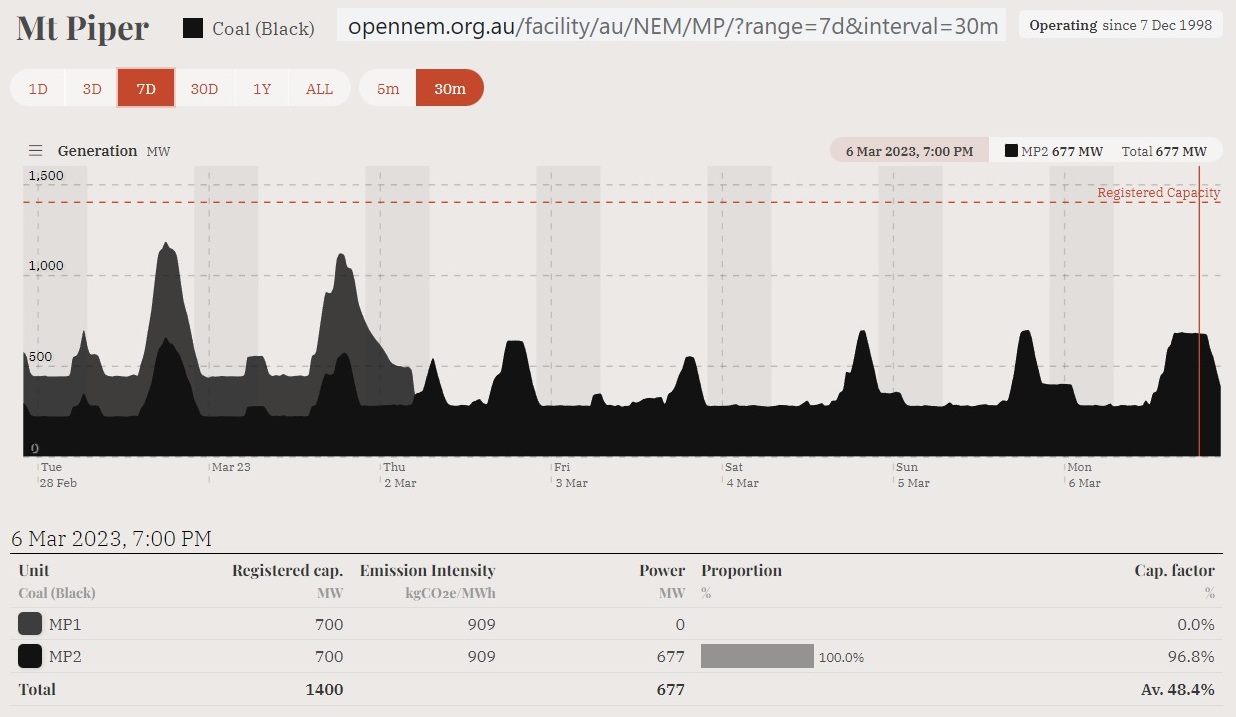

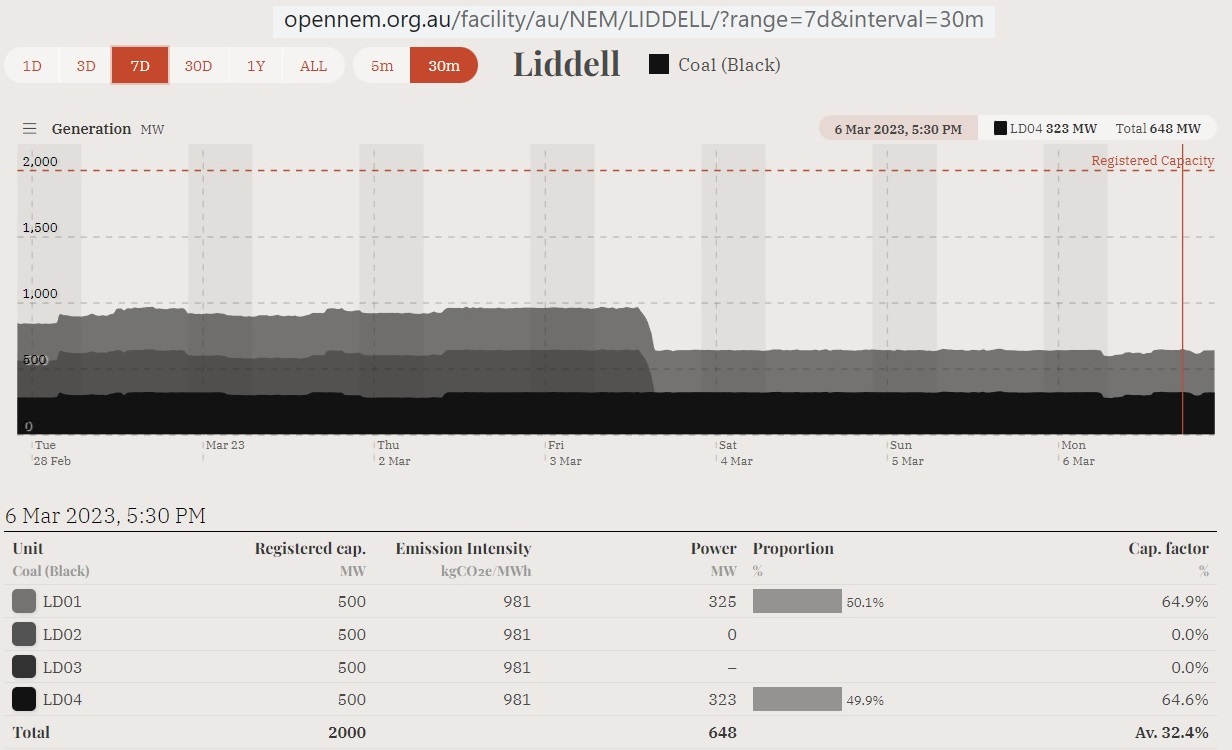

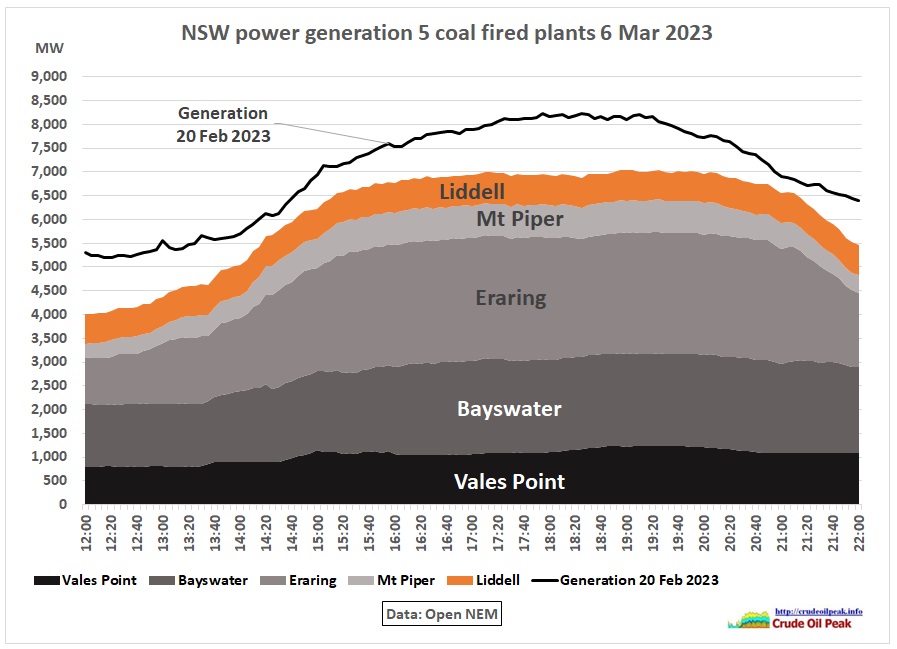

Generation from coal was down to 7 GW. Mt Piper MP1 (680 MW) was out of action since 2nd March and scheduled to come back 24th March. Liddel LD02 (320 MW) stopped working on 3rd March, to come back 13th March. That’s 1,000 MW together. In part 1 we showed that Liddell was normally generating 900 MW.

Fig 5: Mt Piper generation 28 Feb – 6 March 2023

Fig 5: Mt Piper generation 28 Feb – 6 March 2023

Fig 6: Mt Piper w/o MP1 on 6 Mar

Fig 6: Mt Piper w/o MP1 on 6 Mar

Fig 7: Liddell generation 28 Feb – 6 March 2023

Fig 7: Liddell generation 28 Feb – 6 March 2023

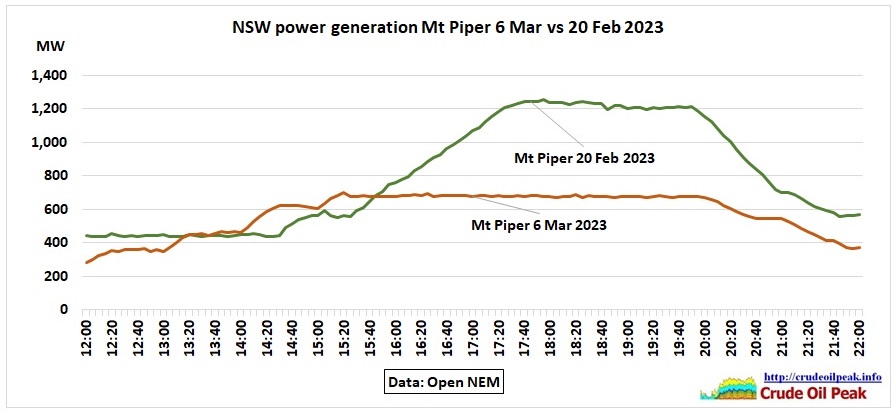

Neither Eraring nor Vales Point went up to their registered capacities (2,880 MW and 1,320 MW respectively) to compensate for the drop in 2 other coal plants.

Fig 8: Eraring and Vales Point on 6 Mar and 20 Feb 23

Fig 8: Eraring and Vales Point on 6 Mar and 20 Feb 23

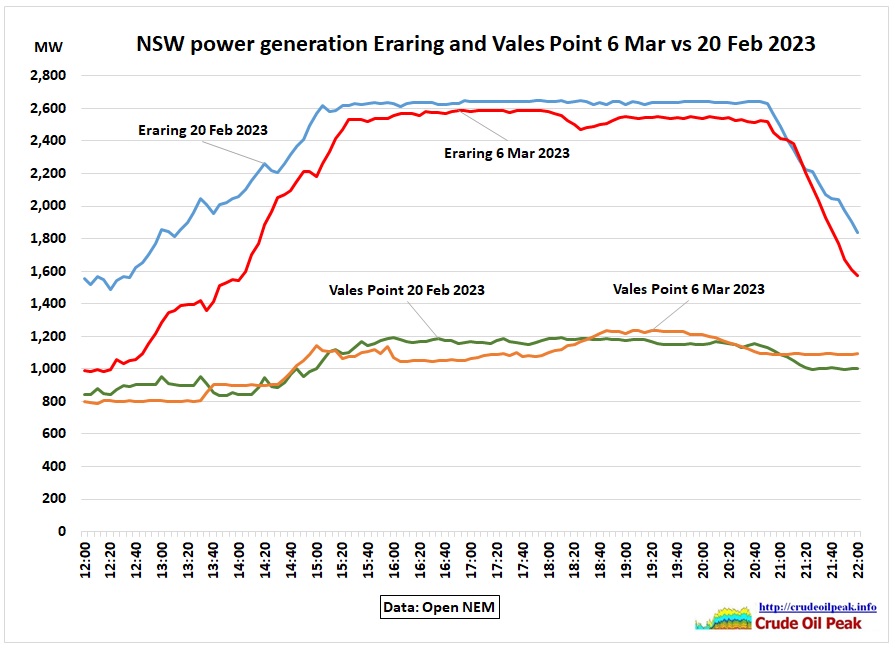

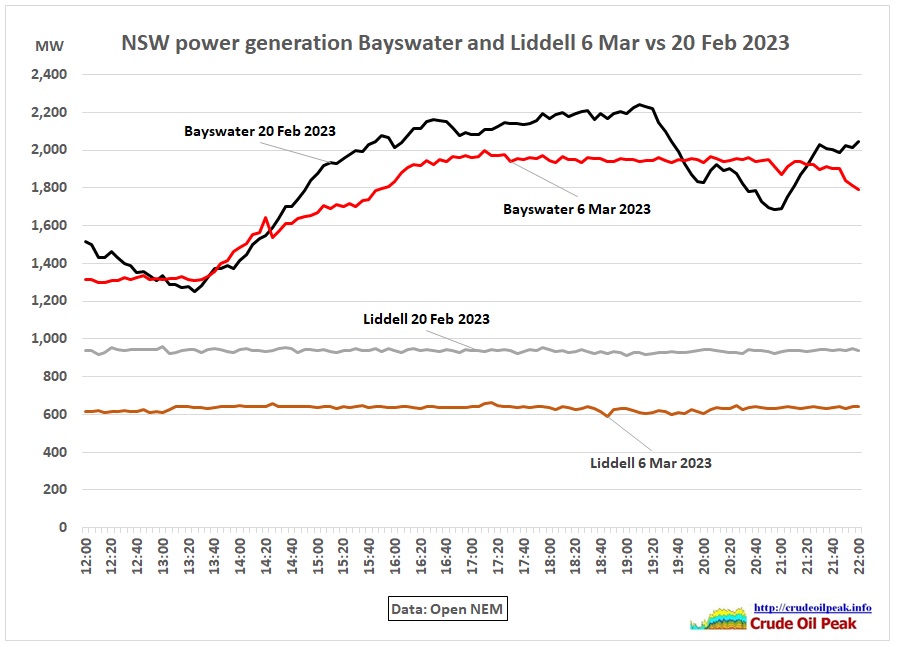

Fig 9: Bayswater and Liddell comparison generation 6 Mar – 20 Feb

Fig 9: Bayswater and Liddell comparison generation 6 Mar – 20 Feb

Bayswater generated less, not more to compensate the loss of LD02 of Liddell which is located nearby.

All together:

Fig 10: Comparison 5 NSW coal plants 6 Mar vs 20 Feb

Fig 10: Comparison 5 NSW coal plants 6 Mar vs 20 Feb

Together, coal generation was flat during the whole afternoon and evening, less peaky than on the 20 Feb.

Impact

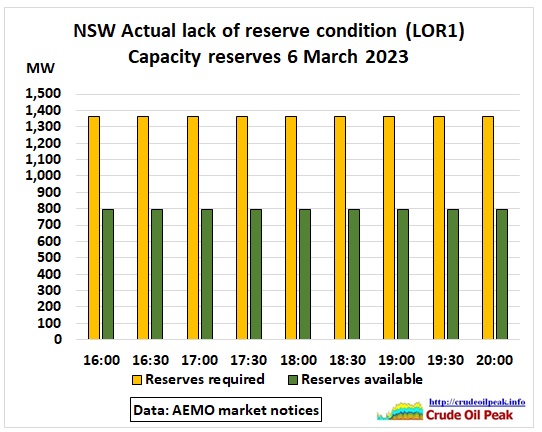

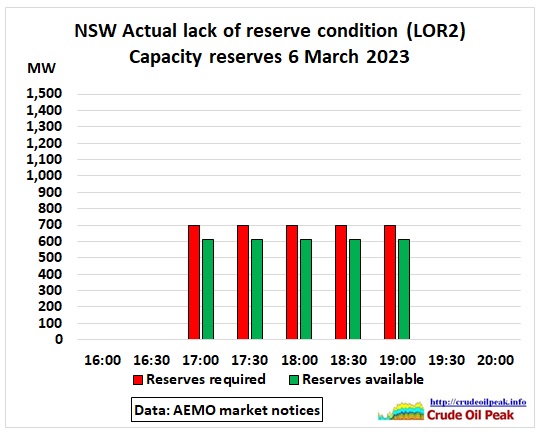

There were 7 forecast LOR1 and LOR2 (lack of reserves) warnings issued in AEMO’s market notices https://aemo.com.au/en/market-notices already 1 day ahead

The forecasts turned into actual LORs:

Fig 11: NSW LOR1 conditions on 6 Mar 2023

Fig 11: NSW LOR1 conditions on 6 Mar 2023

Fig 12: NSW LOR2 conditions on 6 Mar 2023 (notice 106310)

Fig 12: NSW LOR2 conditions on 6 Mar 2023 (notice 106310)

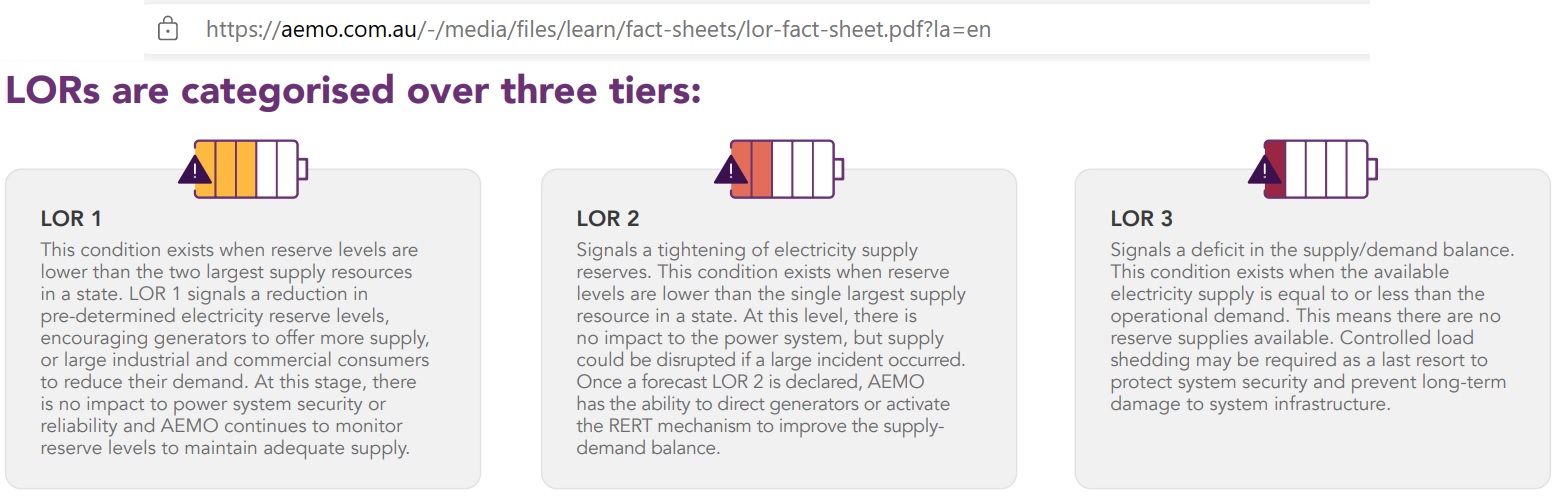

Fig 13: Definitions of LOR1 – LOR3

Fig 13: Definitions of LOR1 – LOR3

https://aemo.com.au/-/media/files/learn/fact-sheets/lor-fact-sheet.pdf

The largest units (registered capacity) are: Eraring 720 MW (4 units), Mt Piper 700 MW (2 units), Bayswater 660 MW (4 units), Vales Point 660 MW (2 units), Loy Yang 560 MW (4 units) and Loy Yang B 500 MW (2 units)

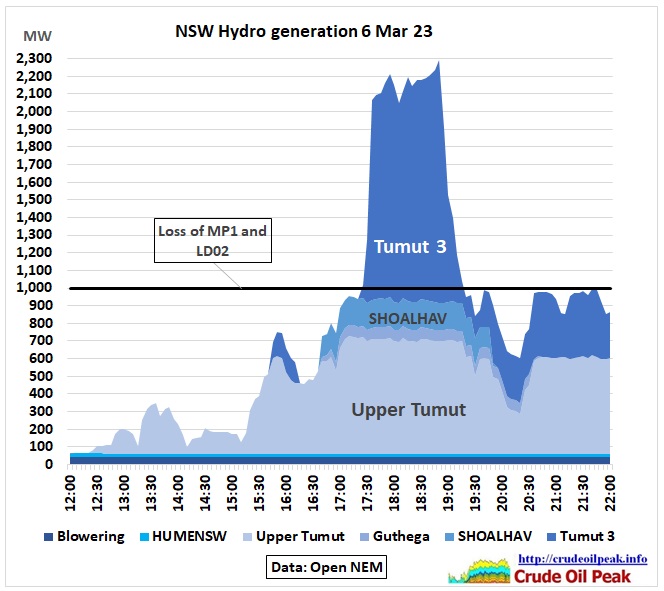

Hydro

Fig 14: Hydro power was 300 MW higher than on 20 Feb

Fig 14: Hydro power was 300 MW higher than on 20 Feb

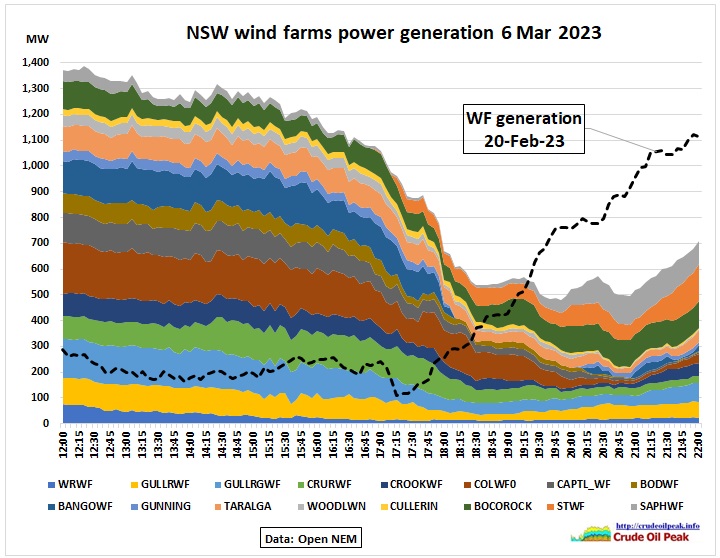

Wind

Fig 15: NSW generation from wind farms 6 Mar vs 20 Feb

Fig 15: NSW generation from wind farms 6 Mar vs 20 Feb

There was more wind on 6 Mar but in the afternoon hrs when solar power declines, wind output also went down – while on 20 Feb it went up.

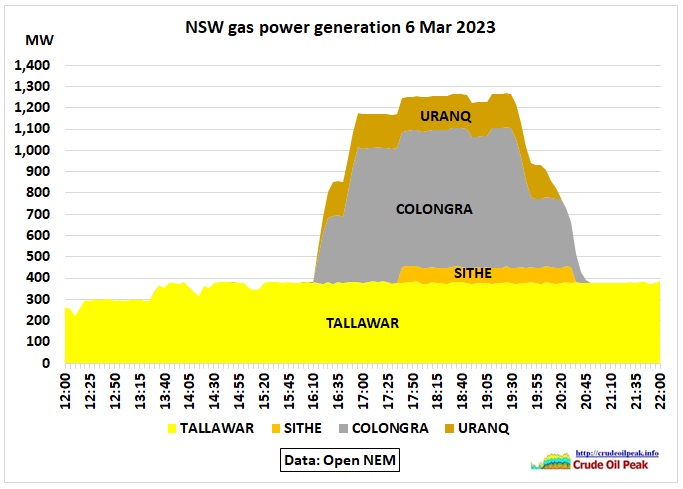

Gas

Fig 16: Power generation from gas on 6 Mar 23

Fig 16: Power generation from gas on 6 Mar 23

Tallawarra started to generate its maximum of 380 MW 4 hrs earlier than on 20 Feb, almost doubling gas consumption.

The Colongra gas peaking plant (4 units) was generating an average of 500 MW during peak hours 16:15 and 20:45 (maximum of 660 MW at 19:30). Part 1 of this post described that the gas storage at Colongra allows only a 5 hrs operation per day at full capacity. This capacity was used at around 80%. https://jemena.com.au/pipelines/colongra-pipeline

Imports

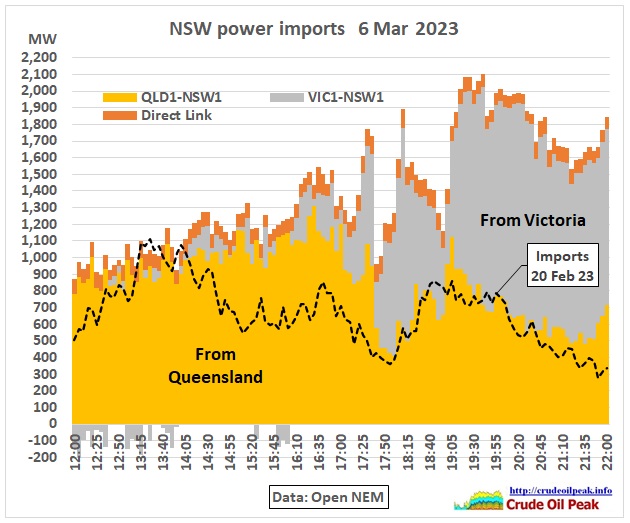

Fig 17: NSW power imports from Queensland and Victoria 6 Mar 2023

Fig 17: NSW power imports from Queensland and Victoria 6 Mar 2023

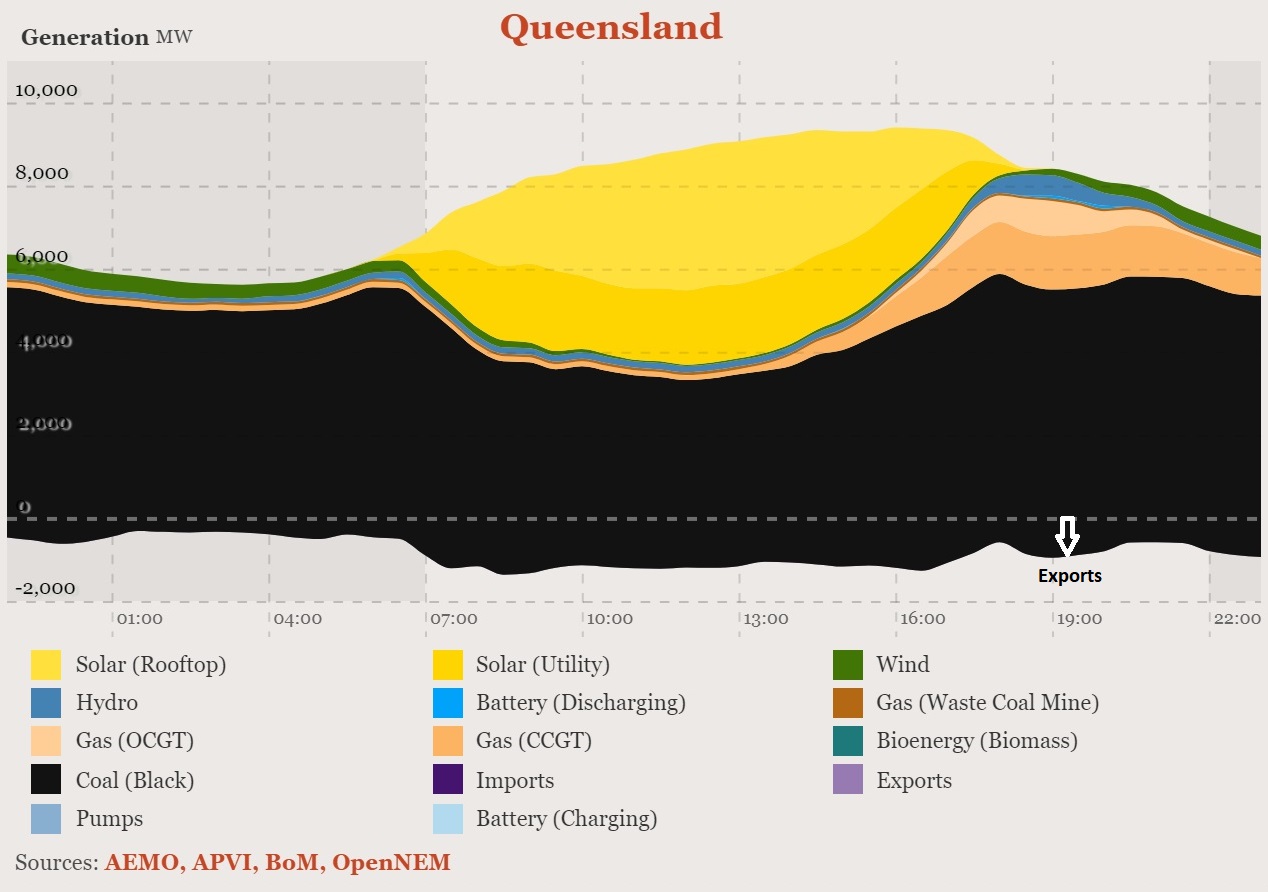

Fig 18: Queensland power generation 6 Mar 2023

Fig 18: Queensland power generation 6 Mar 2023

Coal power was fairly constant at 6,100 – 6,400 MW between 4.30 pm and midnight. But gas power was ramped up to compensate for falling solar power and to maintain exports to NSW after sunset.

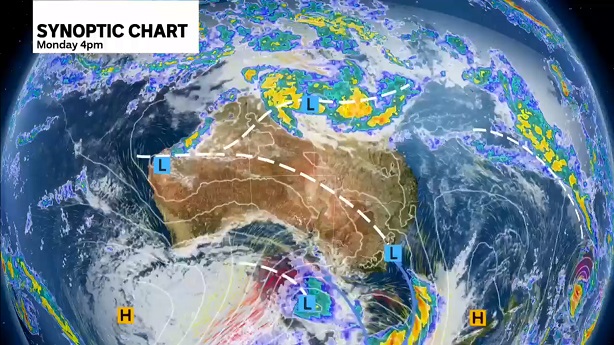

Fig 19: Synoptic chart 6 Mar 23 showing low pressure systems

Fig 19: Synoptic chart 6 Mar 23 showing low pressure systems

with winds turning clockwise, powering Victoria’s wind farms

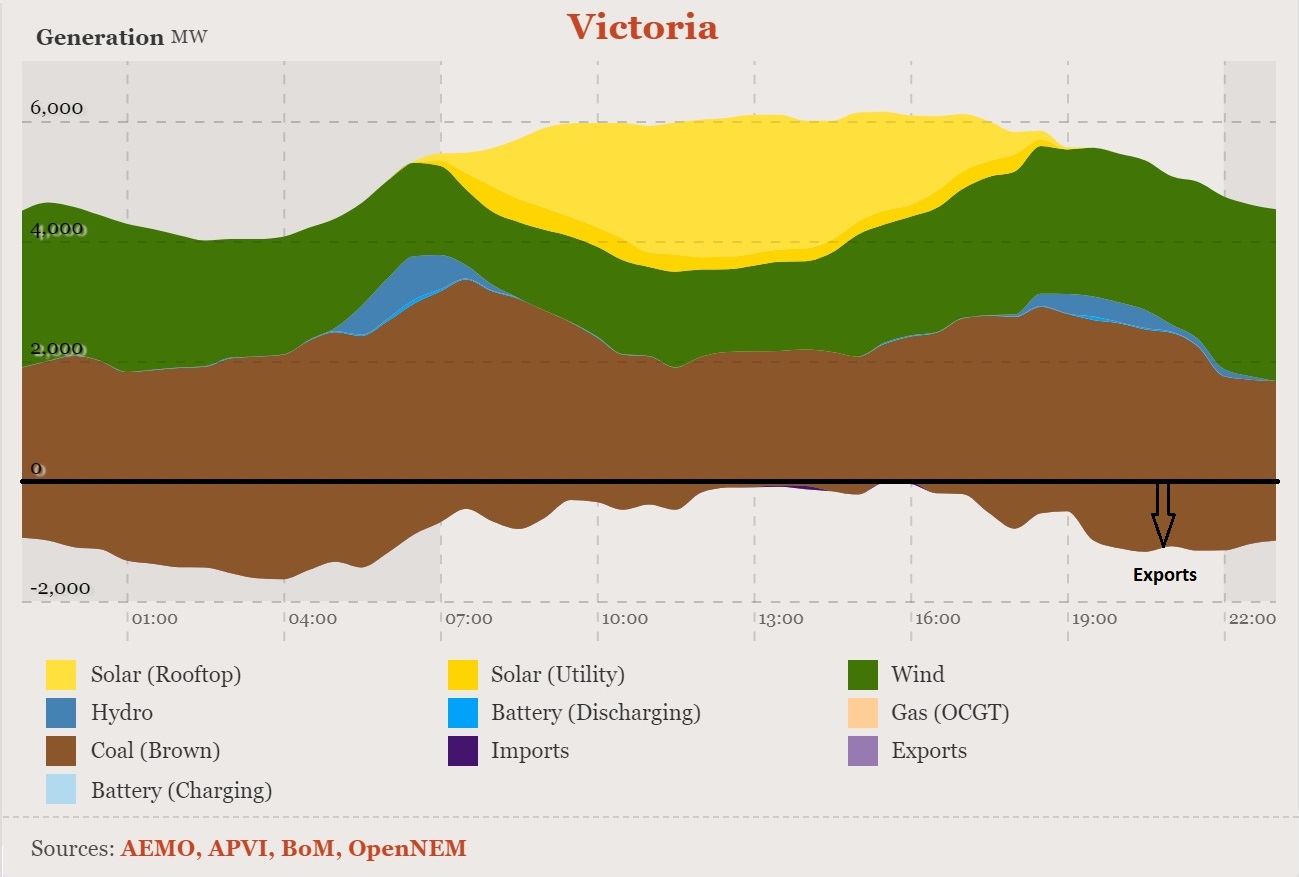

Fig 20: Victoria power generation 6 Mar 2023

Fig 20: Victoria power generation 6 Mar 2023

After sunset, generation was dominated by brown coal and wind (see Fig 19). Almost half of the wind was exported. In the last 30 days there were only 5 days when wind generation was of the same magnitude (-10% to + 20%). On 20 Feb and the 2 preceding days wind output was 70% less.

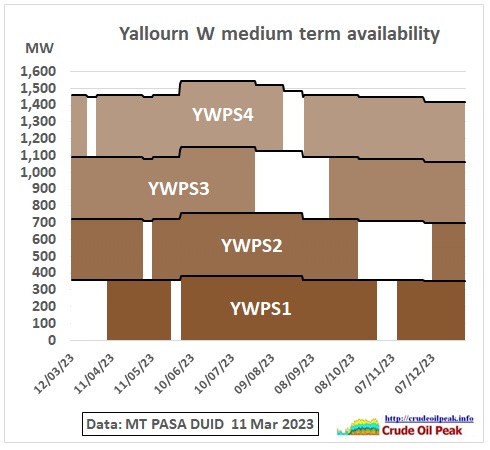

The Yallourn brown coal plant will be closed for maintenance in 2023 as shown in the following graph:

Fig 21: Availability of Yallourn’s 4 units

Fig 21: Availability of Yallourn’s 4 units

http://www.nemweb.com.au/REPORTS/CURRENT/MTPASA_DUIDAvailability/

White areas show planned maintenance periods.

Summary and Conclusion

On 6 Mar 2023, a lack of reserve level LOR2 was observed between 5 pm and 7 pm. Under this condition, a reserve of 600 MW was lower than the largest unit available, namely one of the 4 Eraring units at 720 MW. A failure at that plant or a 4.6% increase of the 13,000 MW demand would have triggered LOR3 (power shortage). This was avoided but only because:

• NSW gas peaking plant Colongra with 500 MW was fired up (and there was sufficient gas)

• NSW hydro power was increased by 300 MW (and dam levels were high enough after 3 La Nina years)

• NSW’s power imports were pushed up to 2,000 MW, drawing on high wind output in Victoria (a level which was available only on 5 days in the last 30 days) and gas generation in Queensland which relies on coal seam gas and has to compete with LNG exports from Gladstone

It is only a matter of time until a combination of less favourable factors will lead to load shedding. Under no circumstances should demand for grid electricity be increased.

Related posts:

8 Mar 2023

Can NSW replace Liddell? (part 1)

http://crudeoilpeak.info/can-nsw-replace-liddell-part-1

7/10/2022

Sale of Vales Point: How will Czech brown coal baron Pavel Tykac with

business registered in Liechtenstein impact on NSW coal and energy markets?

http://crudeoilpeak.info/sale-of-vales-point-how-will-czech-brown-coal-baron-pavel-tykac-with-business-registered-in-liechtenstein-impact-on-nsw-coal-and-energy-markets

14/6/2021

NSW power spot price spikes May 2021 become regular (part 2)

https://crudeoilpeak.info/nsw-power-spot-price-spikes-may-2021-become-regular-part-2

7/6/2021

NSW power spot price spikes May 2021 become regular (part 1)

https://crudeoilpeak.info/nsw-power-spot-price-spikes-may-2021-become-regular-part-1

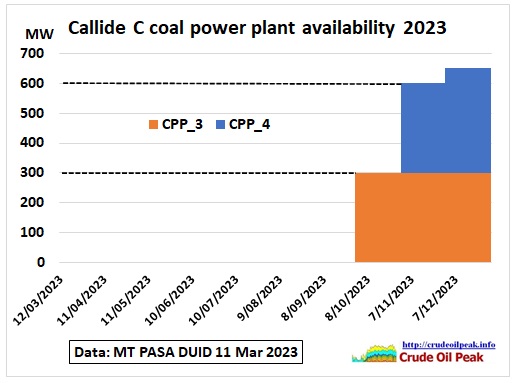

Now Callide C4 which suffered a hydrogen explosion as mentioned in the above post, will not come back until November 2023. Callide C3, which was disabled by the collapse of the cooling system https://www.abc.net.au/news/2022-11-04/callide-power-station-offline-equipment-failures/101615842 may come back in October 2023