This post will show how the Australian government has introduced new dimensions in oil statistics which will hopefully lead to the dawning of the Age of “let the diesel in”.

“When the moon is in the Seventh House” …. Ministerial press releases align with Export Finance Australia (EFA) contracts.

Aquarius (Let the Sunshine in) 1969

https://www.youtube.com/watch?v=06X5HYynP5E

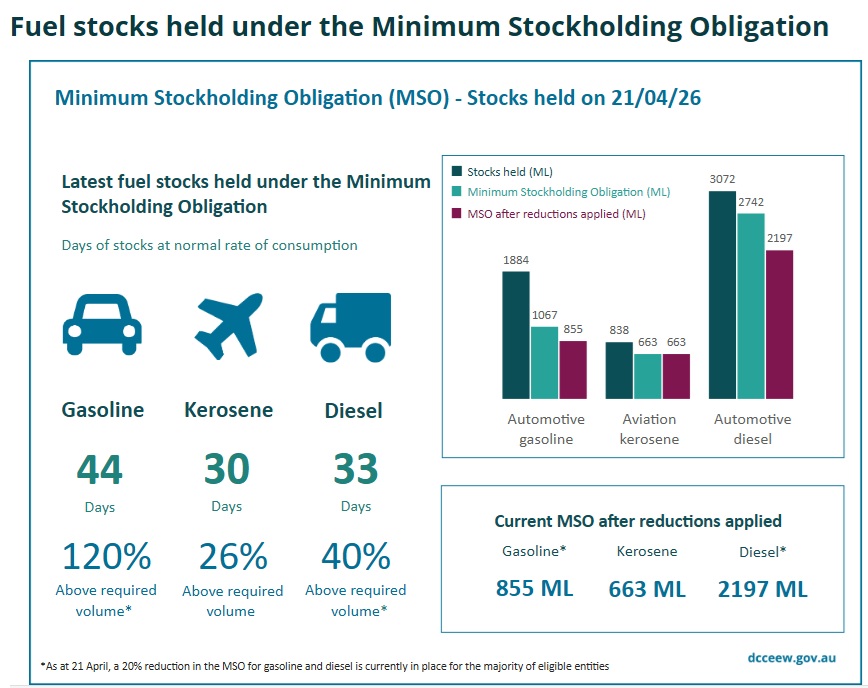

On Sun 26th April the updated Minimum stockholding obligation data for the 21st April came out.

Fig 1: Minimum stockholding obligation dated 21 Apr 2026

Fig 1: Minimum stockholding obligation dated 21 Apr 2026

https://www.dcceew.gov.au/energy/security/australias-fuel-security/minimum-stockholding-obligation/statistics

The interested reader should save these charts because they are overwritten each week. The department does not have a publicly available archive site, one of the drawbacks – which should be corrected.

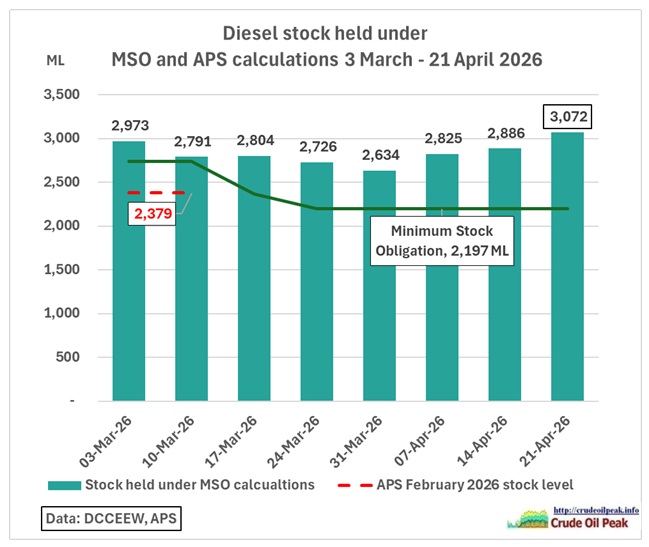

In the following graph it is shown how the MSO diesel stocks evolved, along with the (lowered) MSO and also the diesel stocks as reported in the Australian Petroleum Statistics (APS) for the month of Feb 2026:

Fig 2: Timeline of diesel stocks since 3 Mar 2026

Fig 2: Timeline of diesel stocks since 3 Mar 2026

The publication of the MSO data is usually presented at a media event like this latest:

Press conference, Sydney, New South Wales

26 April 2026

MINISTER FOR CLIMATE CHANGE AND ENERGY, CHRIS BOWEN: I’m pleased to say that Australia’s fuel stocks continue to be very solid. We have 44 days worth of petrol, which is 8 days more than when Iran was first bombed. We have 33 days worth of diesel, which is one day more than when this crisis began. And we have 30 days worth of jet fuel, which is also one day more than the beginning of the war in the Middle East.

I’m also pleased to tell you, there are 58 ships as of last night on their way to Australia with fuel. There have been several of those dock during the week. Last week’s figure was 61 and some of those 58 are expected to dock in Australia as soon as today.

As you know, I also weekly give you an update, give Australians an update on the forward orders for the next four weeks of contracted fuel supplies that will be delivered to Australia. And that is now up to 4.6 billion litres. Last week’s update was 4.1 billion litres and it is up to 4.6 and the increase is primarily diesel, that is up around 500 million litres. We have 2.6 billion litres worth of diesel on the way, on order, contracted for Australia for the next four weeks. 624 million litres of petrol, 489 million litres of jet fuel, and 939 million litres of crude oil, which will then be obviously refined — in our two refineries into refined fuel.

We have, as you know, over the course of the last week, announced 400 million litres of extra diesel, which will arrive during May or the first week of June, which will be extra supply — over and above what normally would have been delivered — just to give us an extra added buffer

https://minister.dcceew.gov.au/bowen/transcripts/press-conference-sydney-new-south-wales-2

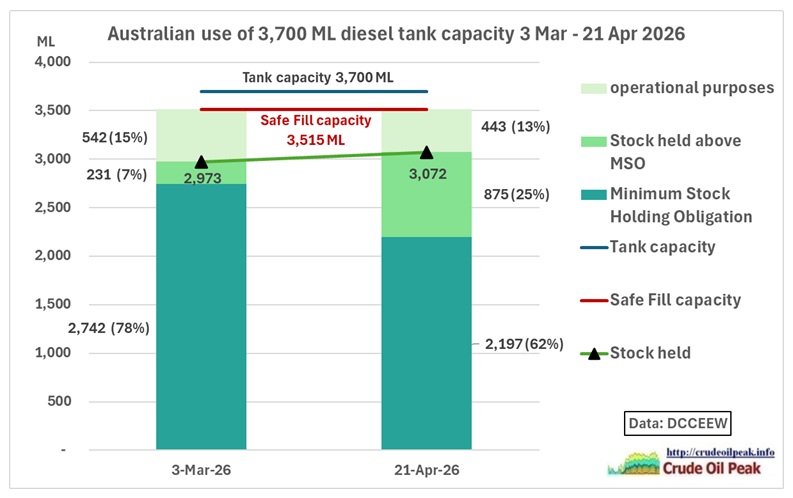

Let’s zoom in on the diesel increase:

Fig 3: The miraculous increase in diesel stock held

Fig 3: The miraculous increase in diesel stock held

The 3,700 ML capacity in 90 diesel terminals is from this 20 March 2026 link: https://minister.dcceew.gov.au/bowen/media-releases/securing-australias-fuel-sovereignty

The physical limit is given by the safe fill capacity of 3,500 ML. The operational window between this capacity limit and the MSO of 2,200 ML is 1,300 ML. It is currently used at (875/(875+443) = 66%, an upper average range. There must always be space in tank farms for arriving tankers for the right type of fuel.

So where is the new dimension of data? It’s forward orders entered into the mix.

We need to understand that we have 5 distinctive diesel flow and stock data sets with different definitions, objectives and political narratives:

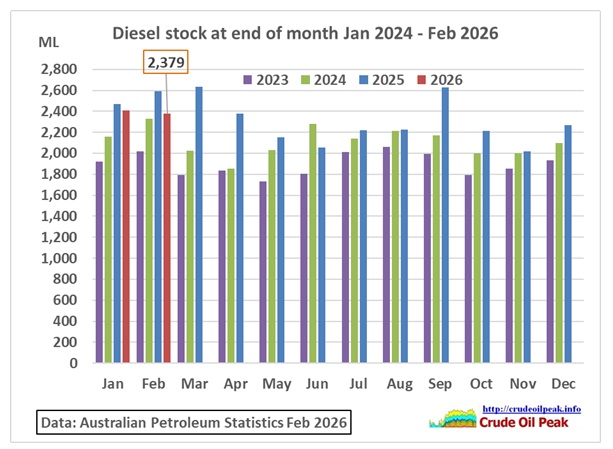

(1) APS stock data until February 2026 of 2,379 ML (latest available data). This includes tank farms onshore and tankers offshore in coastal waters, mainly those waiting at Australian ports and/or moving between these ports. Not included are stocks in mines. This website has extensively used APS statistics for many types of graphs.

Fig 4: Diesel stock in Australian Petroleum Statistics

Fig 4: Diesel stock in Australian Petroleum Statistics

https://www.energy.gov.au/publications/australian-petroleum-statistics-2026

Diesel stock in the first 2 months of 2026 (appr. 2,400 ML) was lower than in 2025 but in both 2024 and 2025 stock went down in March and April.

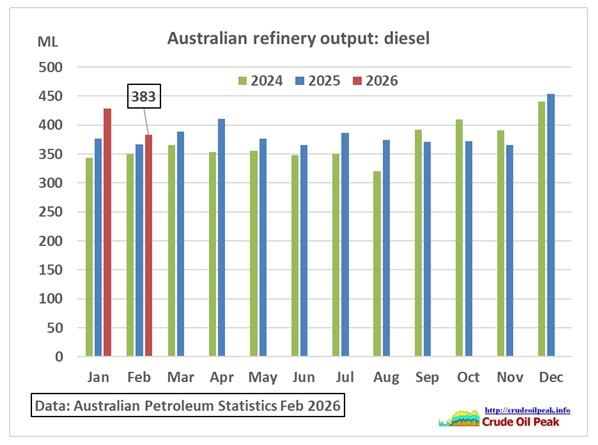

(2) APS domestic average monthly refinery production. We had 390 ML diesel for the 12 month period before Feb 2026

Fig 5: Australian refinery production of diesel

Fig 5: Australian refinery production of diesel

Refinery output has been reduced by the fire in Geelong (-20% diesel = appr. 40 ML per month since 16/4/26). https://www.vivaenergy.com.au/media/news/2026/geelong-refinery-incident-update

So we should expect 390 ML – 40 ML = 350 ML/month for both refineries

(3) Stock data given in weekly Ministerial briefings on minimum stock holdings (MSO). See Fig 2. They also exclude stocks in mines. Note that MSO data in addition to APS data include

all tankers which have entered the EEZ, for example tankers from South Korea passing through PNG and having crossed into the EEZ. Stock on 21 April were 3,072 ML, an increase of 186 ML over the 14 April number and 438 ML over the 31 March number.

(4) Forward orders in various stages of being processed

• contract signed or

• diesel loaded in foreign ports or

• tankers underway OUTSIDE the EEZ

Order book had 2,200 ML of standard orders on 26 April for the next 4 weeks.

And here comes the 5th Dimension:

(5) Extra diesel supplies under the Export Finance Australia (EFA) scheme which works like a hedge fund run by a government insurance. Just as Aquarius transcends the physical, the EFA transcends geography. A tanker doesn’t need to be at a pier to be “security”—it only needs to be a contract in the Minister’s mind.

In fact, the Prime Minister and his Energy Minister are missing no opportunity to announce 100 ML “extra” here and 200 ML “extra” there with so many repetitions that one can easily lose track of which is which but the current sum seems to be 400 ML. Tranche 1, Tranche 2, Tranche 3 etc would have to be introduced to identify these orders.

Let’s put (4) and (5) into a graph:

Fig 6: Forward orders as communicated in press briefings listed below

Fig 6: Forward orders as communicated in press briefings listed below

The fuel data are missing for 4 Apr and 11 Apr, only the totals have been mentioned.

4 April

Press conference, Fairfield West

https://minister.dcceew.gov.au/bowen/transcripts/press-conference-fairfield-west-0

11 April

Press conference in Fairfield West

https://minister.dcceew.gov.au/bowen/transcripts/press-conference-fairfield-west-new-south-wales-0

18 April

Press Conference in Sydney

https://www.pm.gov.au/media/press-conference-sydney-30

26 April

Press conference, Sydney, New South Wales

https://minister.dcceew.gov.au/bowen/transcripts/press-conference-sydney-new-south-wales-2

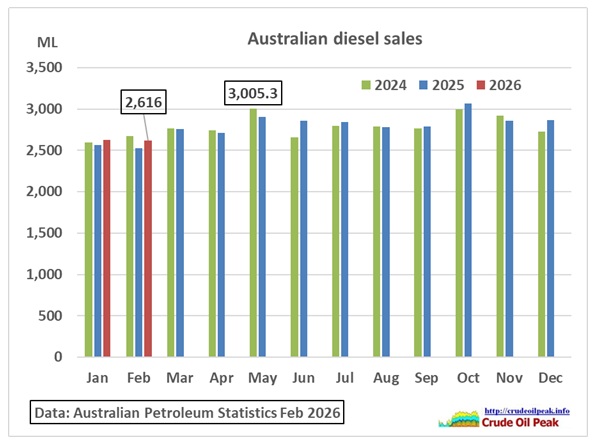

If 2,600 ML are turned into imports and adding 350 ML refinery output we get almost 3,000 ML of diesel supply. That is pretty much the demand Australia had in May of the years 2024 and 2025.

Fig 7: Australia diesel sales

Fig 7: Australia diesel sales

So, if the government wants “sympathy and trust abounding” there needs to be better transparency and verifiable book keeping.

The first contract signed under strategic reserve powers was on 16 April and could therefore not have reached the EEZ by 21 April. Unless diesel consumption went down (which would explain stock increasing) we can suspect that at least the 1st tranche forward order with VIVA Energy (100 ML) was added to the MSO defined stock. The 5th Dimension at work?

Concluding recommendations for the Department of Energy:

- Redesign the webpage https://www.dcceew.gov.au/energy/security/australias-fuel-security/minimum-stockholding-obligation/statistics. This page should contain a scrollable list of separate posts, one for each weekly MSO report

- Include in each MSO post a link to the related media event on the PM or DCCEEW website

- Name each “extra” diesel supply so it can be easily identified, like tranche 1,2,3…

- Design a new bar chart with these tranches and the progress made in turning the orders into physical imports

- Show the numerical links between the 5 data streams and reconcile them

Previous post:

18/4/2026

Australian diesel stocks stabilized mid April 2026

https://crudeoilpeak.info/australian-diesel-stocks-stabilized-mid-april-2026

Related posts:

22/4/2026

Alan Kohler’s diesel Armada has hit Sydney

https://crudeoilpeak.info/alan-kohlers-diesel-armada-has-hit-sydney

Update of tanker arrivals

https://crudeoilpeak.info/tankers-arriving-and-departing-in-sydney

Earlier posts:

13/4/2026

Discrepancies in diesel sales and stocks in the Australian Petroleum Statistics

https://crudeoilpeak.info/discrepancies-in-diesel-sales-and-stocks-in-the-australian-petroleum-statistics

10/4/2026

How much fuel does Australia get from Singapore?

https://crudeoilpeak.info/how-much-fuel-does-australia-get-from-singapore