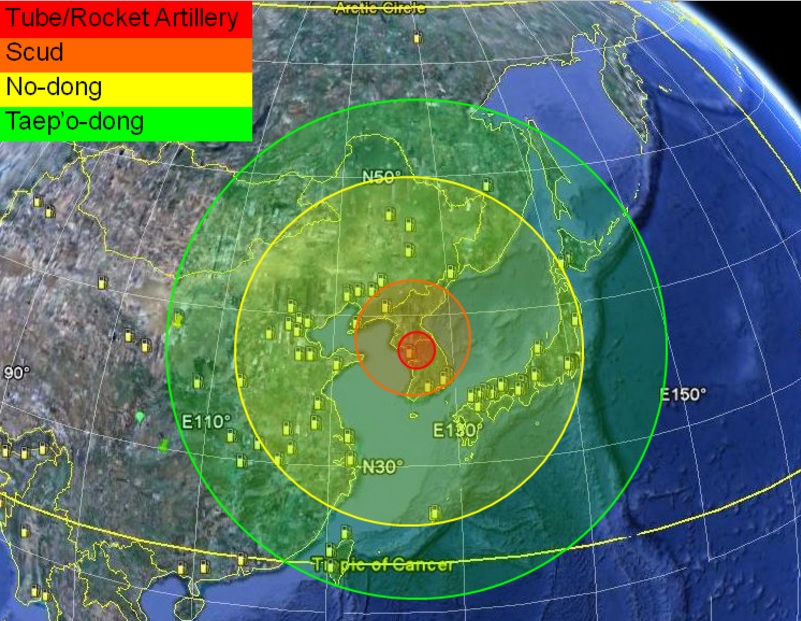

In 2010 the China Sign Post blog published an article entitled “Playing with fire. Potential impact of a North Korean threat to South Korean oil refineries”, showing following map:

Fig 1: Range of North Korea’s missiles in 2010

Fig 1: Range of North Korea’s missiles in 2010

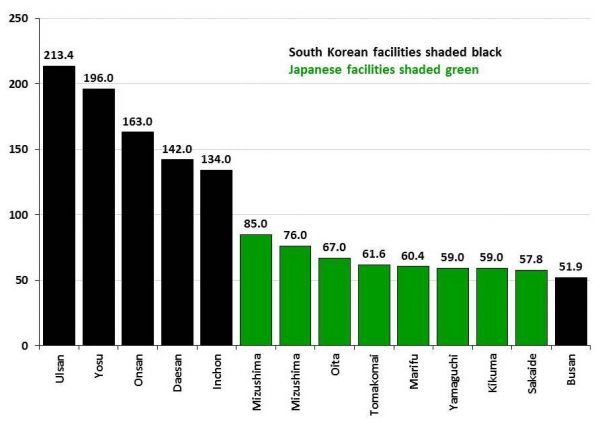

The article ranked the vulnerability of South Korean and Japanese refineries to a North Korean attack, dependent on distance, location and capacity.

Fig 2: Vulnerability ranking of South Korean and Japanese refineries

http://www.chinasignpost.com/2010/11/29/playing-with-fire-potential-impact-of-a-north-korean-threat-to-south-korean-oil-refineries/

The above article was updated in 2013 when tensions were also very high:

“Ballistic missiles with a circular error of probability of several hundred meters such as North Korea’s No-dong would have a good chance of scoring a hit against a refinery, whose processing units, storage tanks, and other infrastructure can occupy an area of multiple square kilometers. An added bonus from Pyongyang’s perspective is that a missile hit on critical parts of a refinery could put the plant out of commission for at least several months.

Based on the latest missile data from Jane’s and other sources, South Korea’s entire refining capacity of approximately 2.8 million bpd lies within range of North Korean Hwasong 6 and 7 and No-dong missiles, while Japan’s 4.7 million bpd of capacity lies fully within the range envelopes of the No-Dong 1 and 2, Musudan, Taepo-dong, and KN-08 missiles.”

http://www.chinasignpost.com/2013/04/14/playing-with-fire-round-2-north-koreas-potential-missile-threat-to-asian-oil-refining-infrastructure/

That was in 2013. Fast forward to March 2017.

Fig 3: North Korean Scud missile drill

10 March 2017

This time, North Korea launched four “extended-range” Scud missiles that are capable of flying up to 620 miles. The map showed all four missiles landing on an arc that stretched down to the Marine Corps Air Station near Iwakuni, Japan. Once again, the North Korean statement doesn’t leave much to the imagination: “Involved in the drill were

{kind=link}

Hwasong artillery units of the KPA (Korean People’s Army) Strategic Force tasked to strike the bases of the U.S. imperialist aggressor forces in Japan in contingency.”

https://www.yahoo.com/news/north-korea-practicing-nuclear-war-144440547.html

This post is not about war scenarios but oil flows.

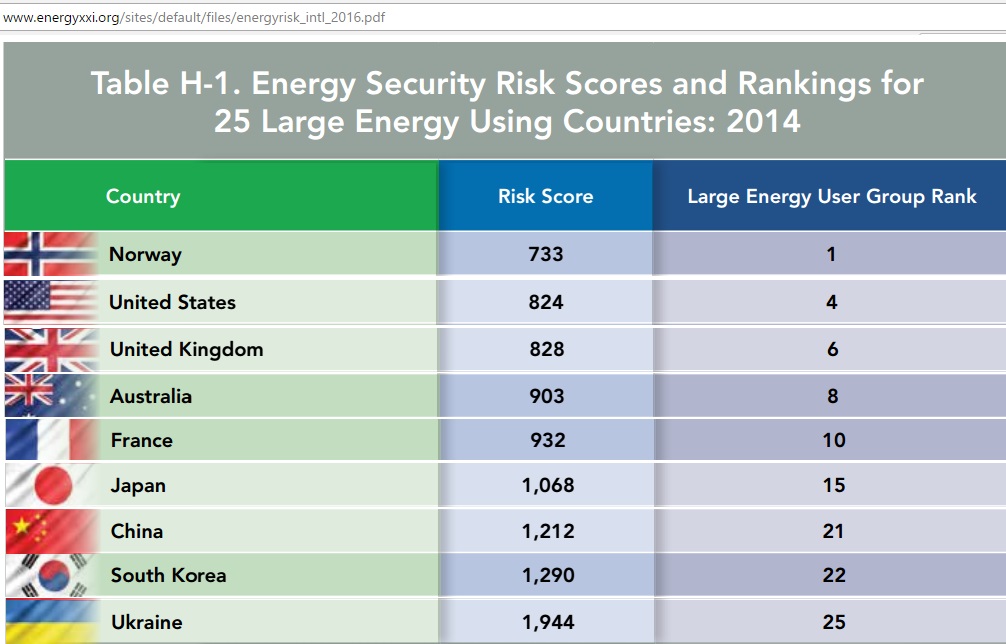

Even under normal circumstances South Korea’s energy security is not very high in comparison to other countries. An assessment of risks for 25 countries undertaken by the US Chamber of Commerce (Institute for 21st Century Energy) in 2015 had South Korea at the 3rd lowest level. The following table shows the composite risk score based on 7 main risk groups including fuel imports, energy expenditure, price and market volatility, energy use intensity, electric power sector, transportation sector and the environment for 9 selected countries (Norway with the highest and Ukraine with the lowest).

Fig 4: Energy security risks for 9 selected countries (excerpts)

Fig 4: Energy security risks for 9 selected countries (excerpts)

http://www.energyxxi.org/sites/default/files/energyrisk_intl_2016.pdf

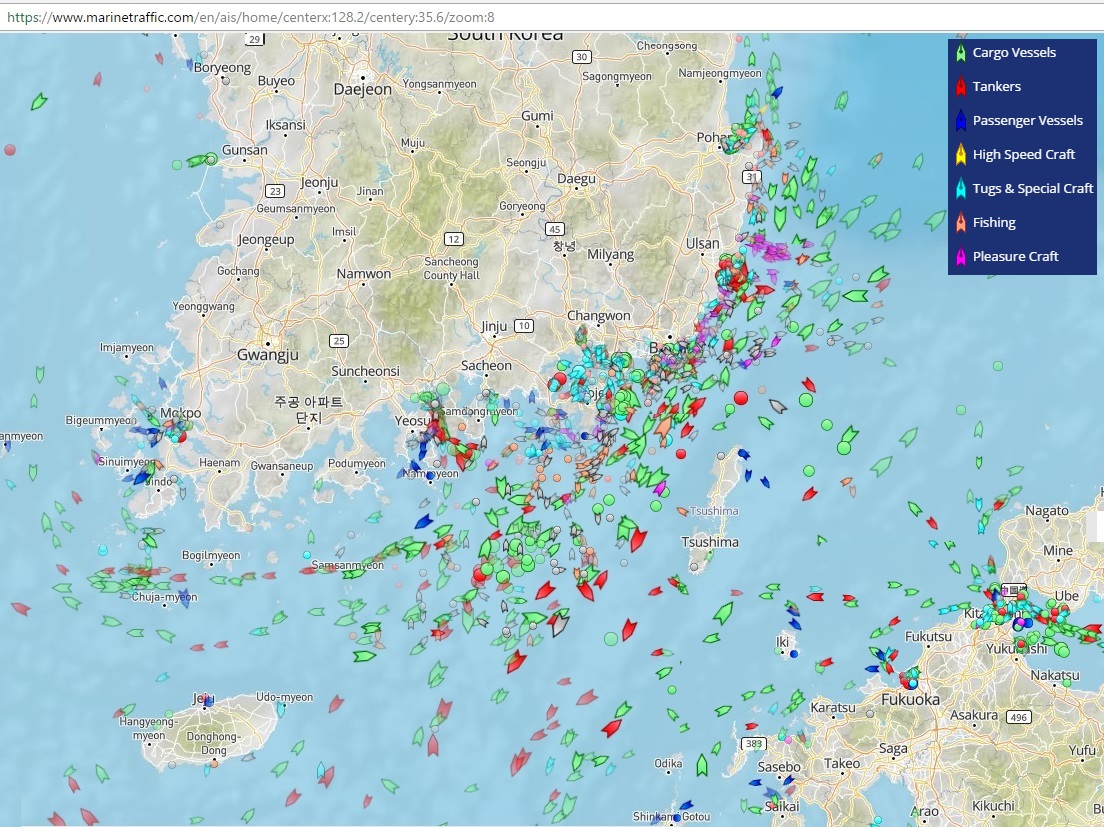

Fig 5: Marine traffic (tankers in red) between South Korea and Kyushu (Japan)

https://www.marinetraffic.com/en/ais/home/centerx:127.9/centery:34.3/zoom:8

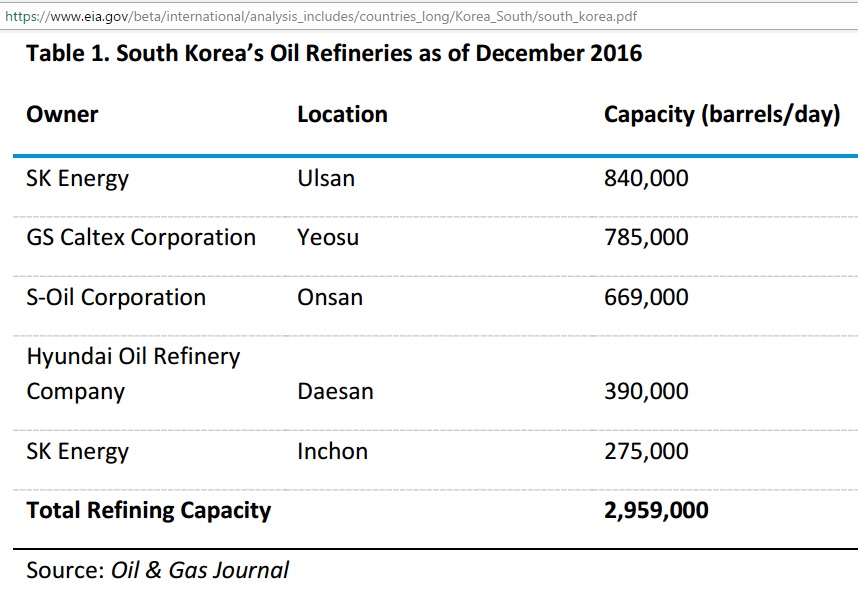

Refineries

This is a list of South Korean refineries

Fig 6: South Korean refineries and capacities

https://www.eia.gov/beta/international/analysis_includes/countries_long/Korea_South/south_korea.pdf

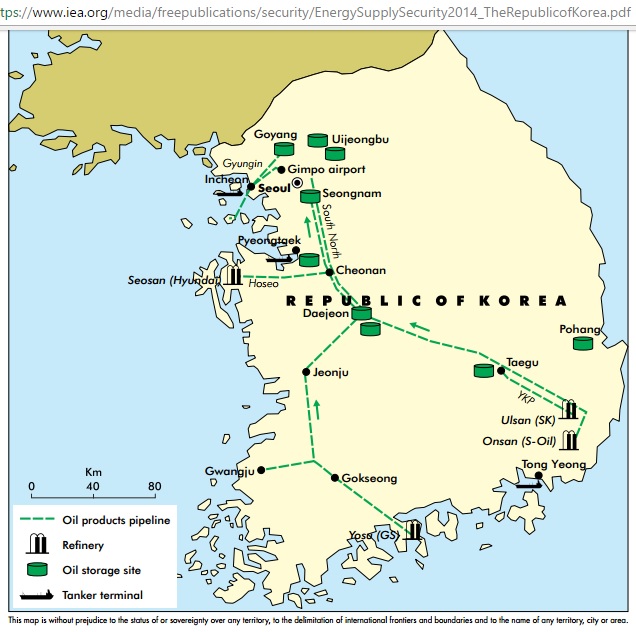

Fig 7: Location of refineries

https://www.iea.org/media/freepublications/security/EnergySupplySecurity2014_TheRepublicofKorea.pdf

Note that the Incheon refinery is within North Korean artillery range.

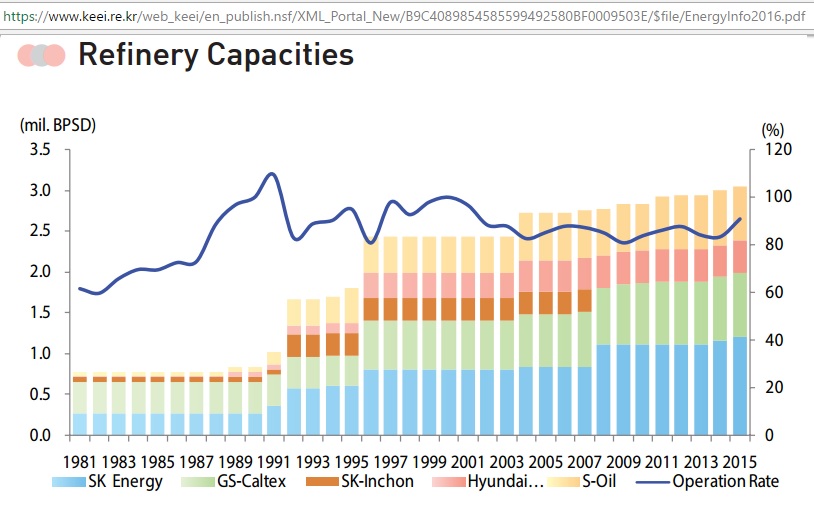

South Korea built up its refinery capacities systematically over the last 25 years.

{kind=link}

Fig 8: South Korean refinery capacities – timeline

Fig 8: South Korean refinery capacities – timeline

https://www.keei.re.kr/web_keei/en_publish.nsf/XML_Portal_New/B9C4089854585599492580BF0009503E/$file/EnergyInfo2016.pdf

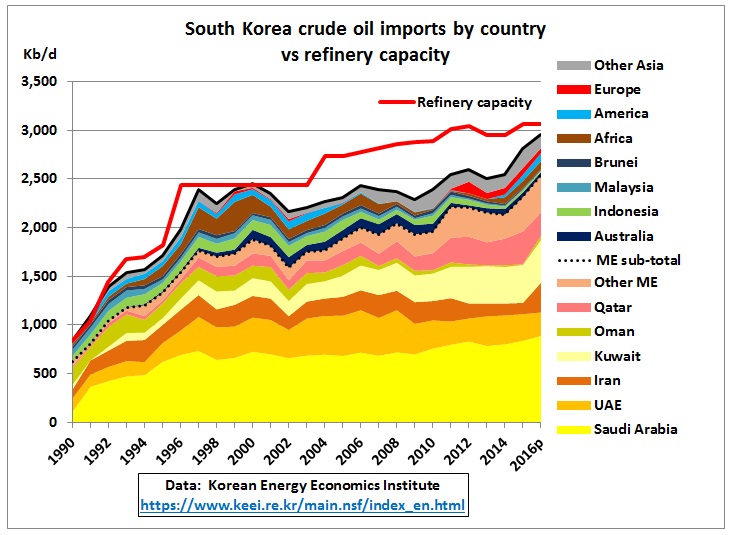

Imports

Where does the crude oil come from for these refineries?

Fig 9: South Korean crude oil imports by country

Fig 9: South Korean crude oil imports by country

https://www.keei.re.kr/main.nsf/index_en.html

The dependency on Middle East oil (under dotted line in above graph) since 2008 is around 85% .

Condensate splitter capacity is 485 kb/d (converting condensate to naphtha for petrochemical use)

Hyundai Oilbank 110 kb/d

Hanwha Total (Daesan) 150 kb/d

SK Energy (Incheon) 140 kb/d

S-Oil (Onsan) 85 kb/d

http://af.reuters.com/article/commoditiesNews/idAFL4N18Z3HG

This is important as US shale oil contains a lot of condensate.

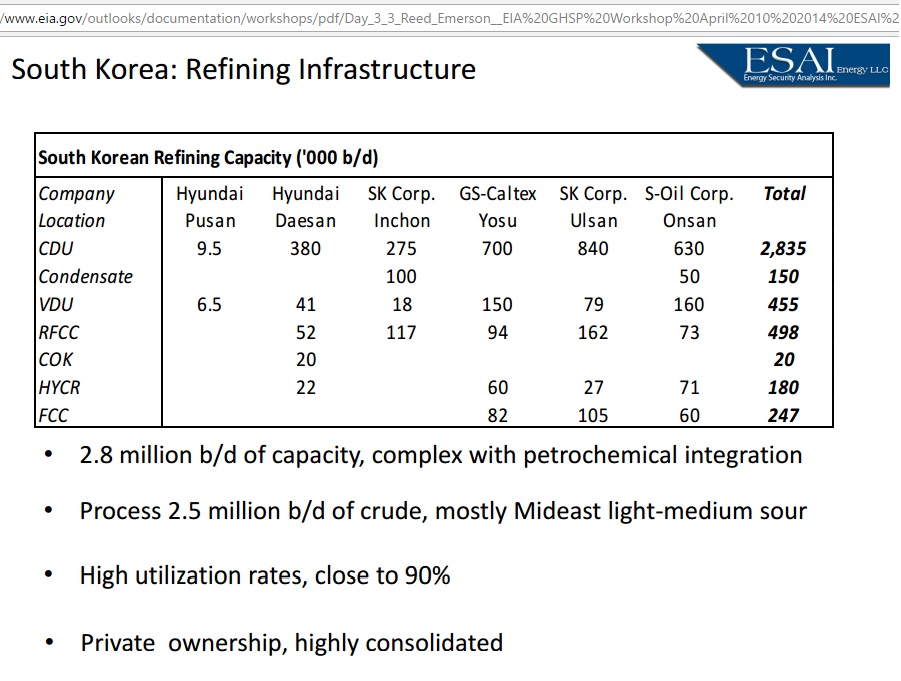

Fig 10: South Korean refinery capacity by type

https://www.eia.gov/outlooks/documentation/workshops/pdf/Day_3_3_Reed_Emerson__EIA%20GHSP%20Workshop%20April%2010%202014%20ESAI%20Energy%20-%20Copy.pdf

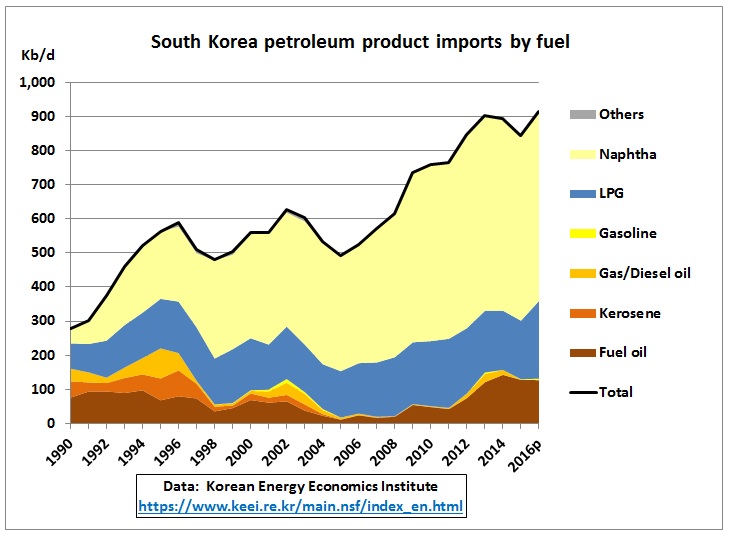

The petro-chemical integration we can see from the type of product imports, mainly Naphtha:

Fig 11: South Korea’s petroleum product imports by fuel

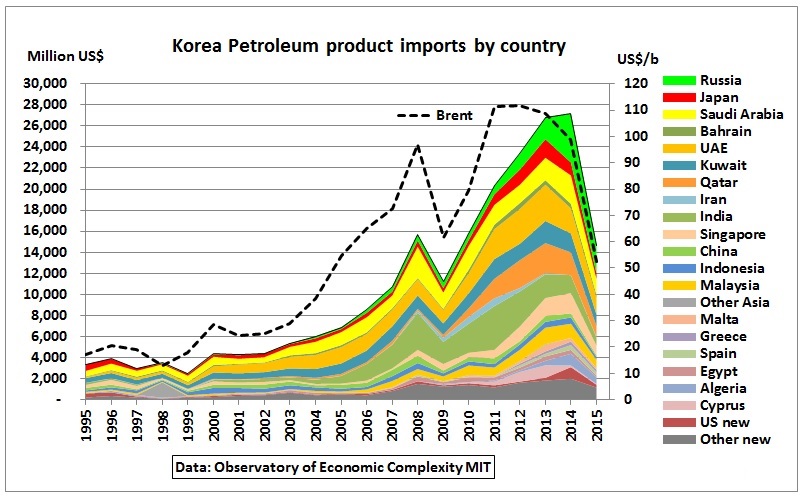

Fig 12: South Korea’s petroleum product imports by country

Fig 12: South Korea’s petroleum product imports by country

These product imports come in small quantities each from many countries in the Middle East, Asia and Europe.

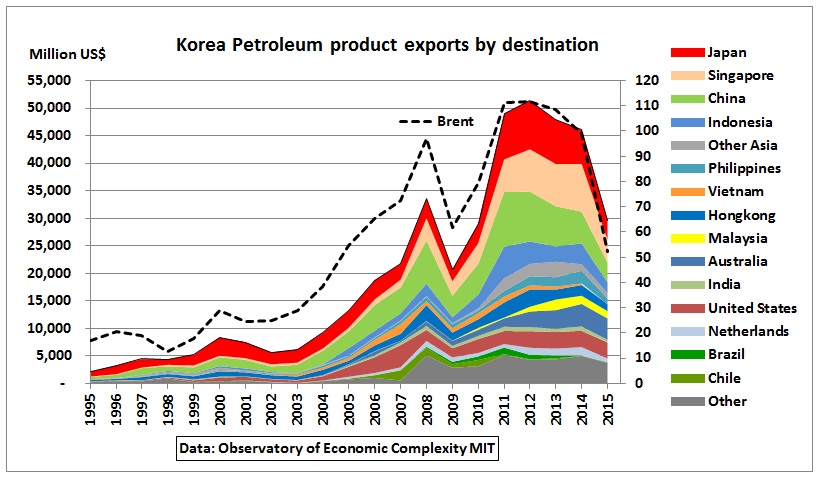

Exports

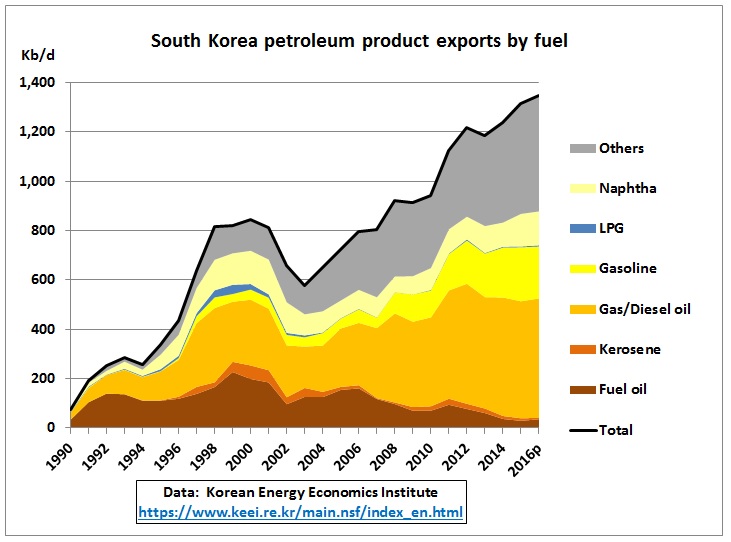

Fig 13: South Korean petroleum exports by fuel type

Fig 13: South Korean petroleum exports by fuel type

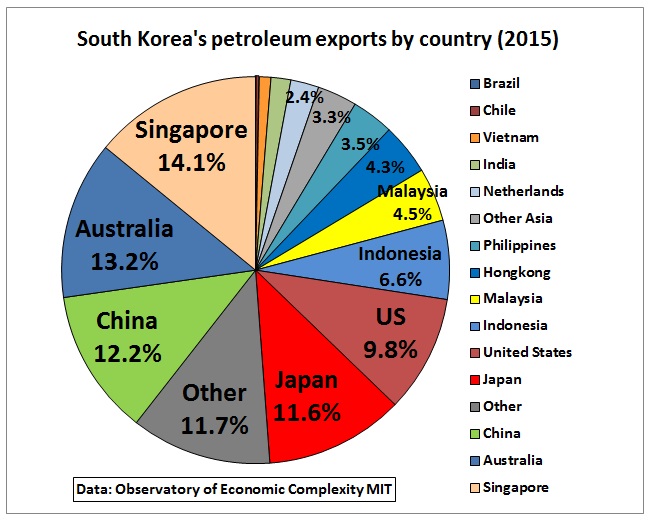

Fig 14: South Korea petroleum exports by country

http://atlas.media.mit.edu/en/visualize/stacked/hs92/export/kor/show/2710/1995.2015/

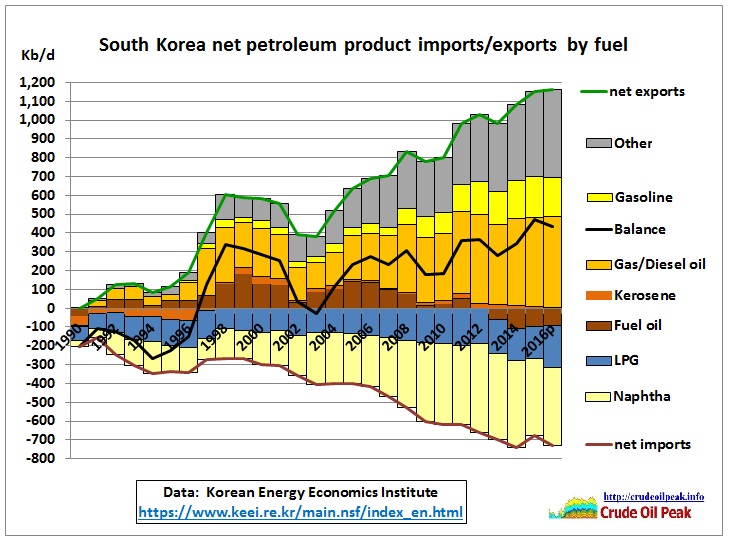

Product balance – net imports/exports

Fig 15: Net import/export balance

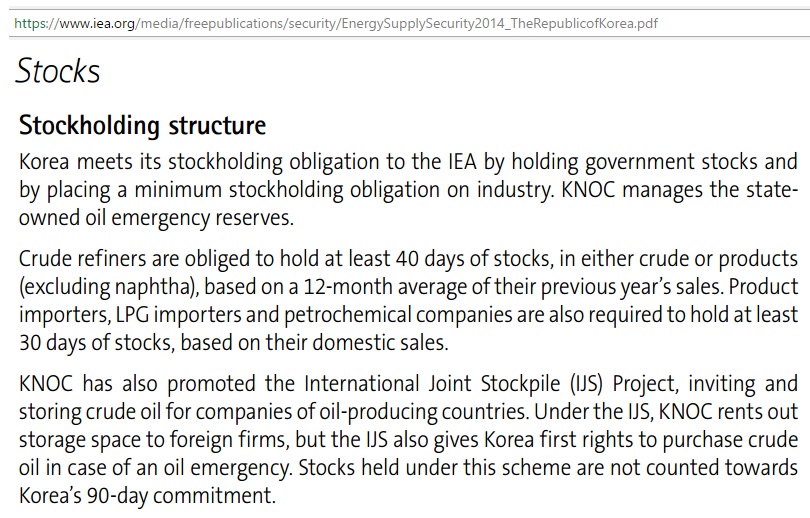

Emergency stock

Fig 16: South Korea’s compliance with IEA requirements (extract)

Fig 16: South Korea’s compliance with IEA requirements (extract)

https://www.iea.org/media/freepublications/security/EnergySupplySecurity2014_TheRepublicofKorea.pdf

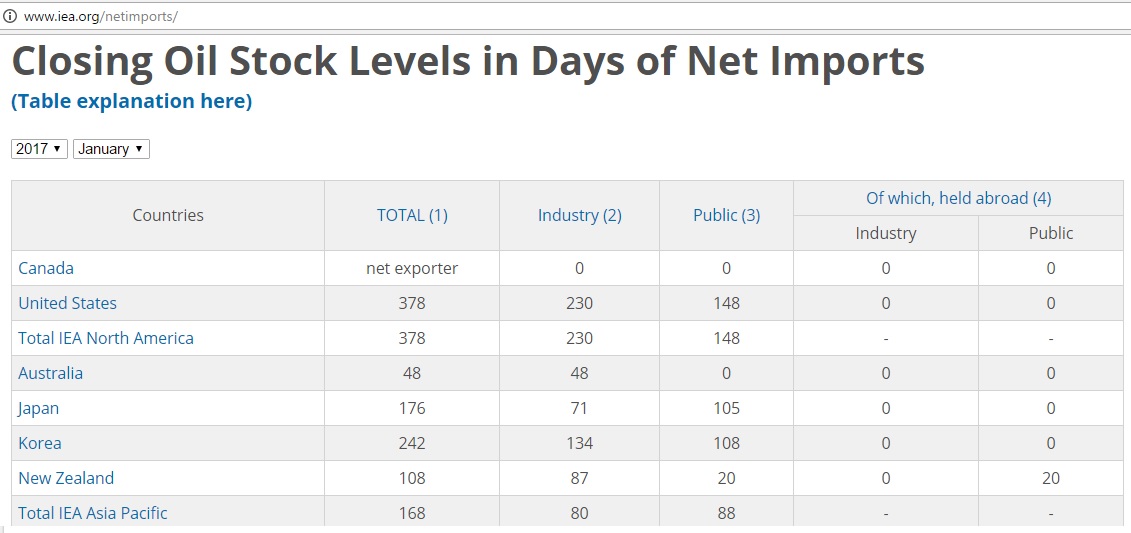

Fig 17: Stock levels in OECD Asia vs OECD Americas, January 2017

Fig 17: Stock levels in OECD Asia vs OECD Americas, January 2017

South Korea’s stock consist of 63% crude and 37% products, according to the IEA energy supply security report 2014 (Fig 2.3). It is much higher than the 90 days minimum requirement.

https://www.iea.org/media/freepublications/security/EnergySupplySecurity2014_PART1.pdf

The most vulnerable in the above list is complacent Australia – which will be hit hardest as it imports petrol, diesel and jet fuel from South Korea. This was covered in the previous post.

Summary

As South Korea is not an oil producing country the impact will be different from other oil crises. But military action around Korea will disrupt Asian and Middle East oil flows and markets. In the worst case scenario in which all tanker traffic to and from South Korea stops there are 8 months worth of crude and product stock available locally. Around 3 mb/d of imported crude oil and 900 kb/d of petroleum products would have to be re-directed to other Asian refineries or chemical complexes provided there is space capacity there. Countries which import petroleum products from South Korea (graph below) would have to procure these fuels from these refineries.

Fig 18: Countries impacted by supply disruptions

Whether other refineries could take over South Korea’s role in the oil market is another question altogether. This would of course depend on the duration of the disruption and the possible damage to South Korea’s oil infrastructure.

Conclusion

Australian context

Australia is continuously dragging its feet over establishing a strategic oil reserve to meet 90 days net import requirements – for cost reasons. The International Energy Agency’s executive director, Fatih Birol, has already visited Australia several times and discussed this problem with both the Energy Minister and the Prime Minister. It may now be too late.

Australian State and Federal governments must make sure that all storage tanks for crude oil and petroleum products are kept at maximum levels by as much as is practical. They should consider renting or buying 2nd hand tankers to increase inventories in order to come closer to IEA stock requirements.

Australian governments have also embarked on new oil dependent infrastructure like road tunnels, highways, tollways and even a 2nd Sydney airport. When there is a war in Asia (or the Middle East), these projects will not be very useful. They should be cancelled and replaced by electric rail projects.